A special guest joins us for this episode of The Hedged Edge, who is well known for his many titles, which include Doctor, Editor-in-Chief, Dean, and Chief Academic Officer, just to name a few. Dr. Channa S. Prakash, Dean of the College of Arts and Sciences (CAS) at Tuskegee University, has served as faculty since 1989 and is a professor of crop genetics, biotechnology, and genomics. He is also well recognized for mentoring underrepresented minority students.

Tune in as biotech guru Dr. Prakash discusses everything from Alabama football, genetics as one of the most extensive agricultural advancements, the most significant risk factors to feeding the world over the next 30-50 years, plus everything in between. And as a bonus, we find out what sport he would be interested in playing if he went professional.

Highlights from this week’s episode include:

The science that has provided our farmers with better varieties of crop lines by using some of the most sophisticated technology on Earth

Why producing crop plants with a much gentler footprint on the natural resources will help feed the growing population

How 75% of the world’s patents in agriculture gene editing are coming out of China

Understanding that trying to impose restrictions on our ability to grow food can be a considerable risk to agriculture and more!

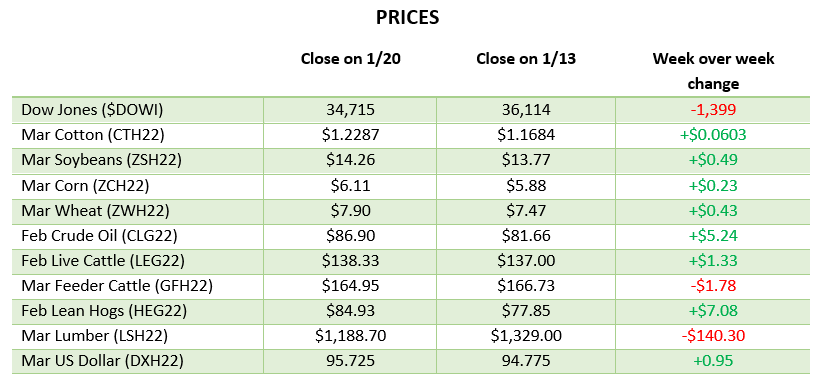

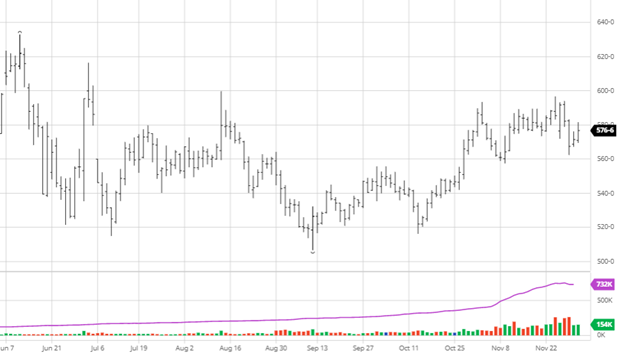

Corn rallied this week with beans with news of trouble in South America continuing and rumors of purchases from China. As we have mentioned before, China buying all ag products is welcome news as they are well behind the Phase 1 targets. The Russia and Ukraine tension, should it boil over, will have major implications for the commodities market as Ukraine’s exports will all but cease. The news of Brazil stopping bean sales is worrisome as there could be more bean and corn yield lost than thought. Energy prices continue their run higher as ethanol demand does not seem to be slowing down. With corn still below recent highs, unlike soybeans, it would appear there is still room for upward movement, but the trade into the weekend, where anything can happen as we know, will be important.

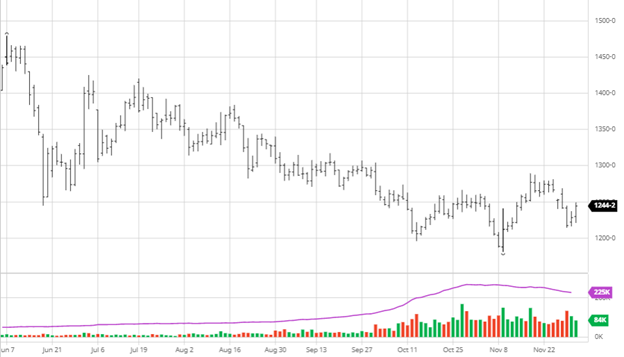

Via Barchart Soybeans rallied this week as soy oil and meal also rallied. The noise around the problems with South America’s crop got a little louder this week with StoneX reporting that Brazil soybeans have gone to “no offer” due to farmers refusing to sell new-crop supplies in the current environment, with drought losses in the south worse than first believed. South American weather remains mixed as southern Brazil and northern Argentina remain hot and dry while southern Argentina received rain over the last couple of weeks. In early February, all areas are expected to revert back to hot and dry in the forecast. These troubles make it sound like the USDA was off on their South America estimates in last week’s report. This is a situation to monitor as any stoppage of sales from Brazil and Argentina would mean purchases from the U.S.

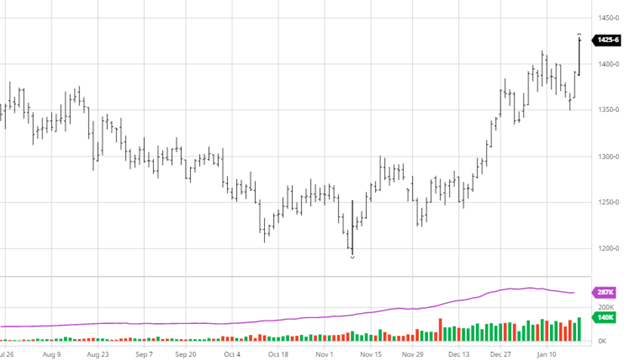

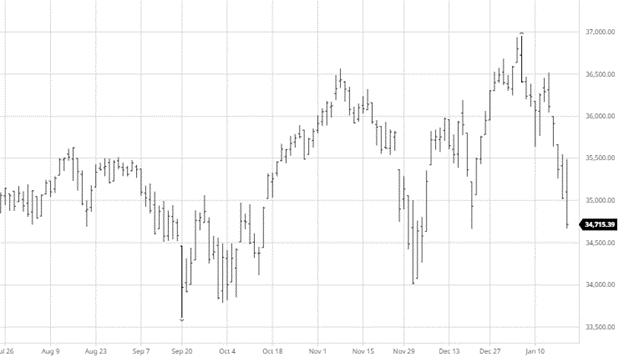

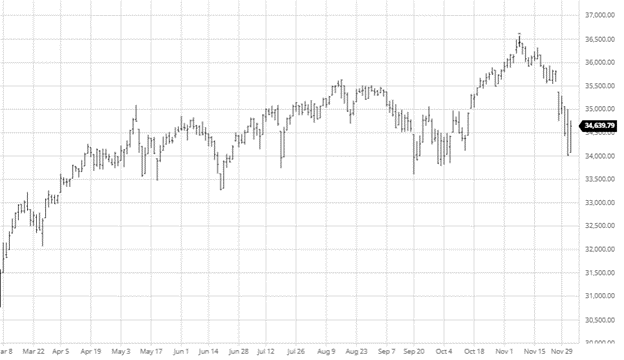

Equities have had a bad week as tech has led the way lower. These rounds of selloffs will offer opportunities to buy back in at some point but as always, timing the market is not an easy job. The market was so hot last year pullbacks are expected, but it is hard to stomach when it falls this much this fast. We are still above the levels we were right after Thanksgiving, but the volatility of the last couple of months looks to still be hanging around.

The 2021 U.S. grain crop has the potential to be one of the largest on record. Where did all the yield come from, what areas were the hardest hit, and why on God’s green earth are grain prices still so high?

Today, we are joined by several RCM Ag Services grain markets experts from around the country to catch up on a post-harvest update and share an outlook for production and marketing in each of their respective regions for the remainder of the 2021 marketing season and the upcoming 22 crops.

Happy New Year! Volatility has been the main storyline in the first week of 2022. There was enough surprise rainfall in the dry areas of South America to spook the markets right before the New Year before a slight bounce. This week’s ethanol production numbers were slightly below last week. Compared to the previous year, monthly ethanol production is running 9% over last year, but ethanol stocks are 8.3% below last year. Ethanol margins are still profitable as gas has rallied since Thanksgiving. The dryness and heat in Southern Brazil and Argentina remain in the forecast while northern Brazil continues to get too much rain. For reference, this time of the year in Argentina is the equivalent to June. If the forecasts prove true in the next couple of weeks, they will continue to stress the crop. Exports this week were nothing to write home about as the USDA described them as the “Marketing year low.” If South America’s crops continue to struggle, we could see an increase in exports, but the opposite could be true if the weather improves.

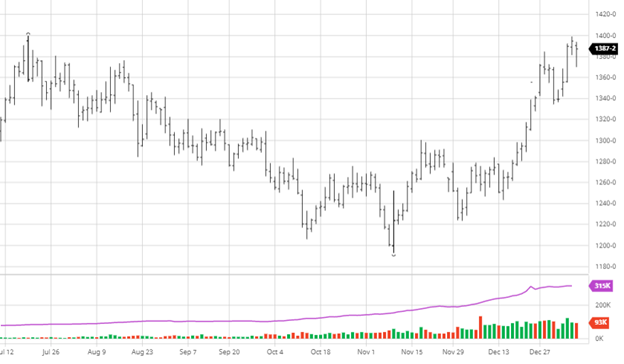

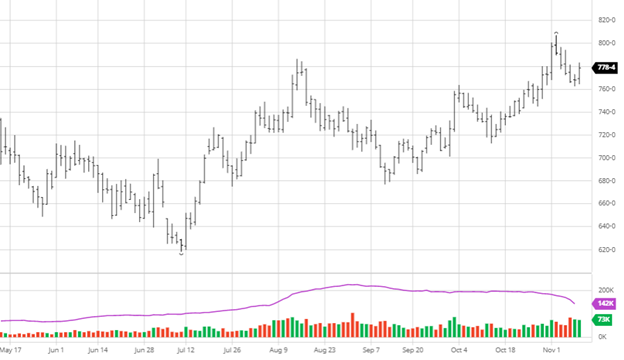

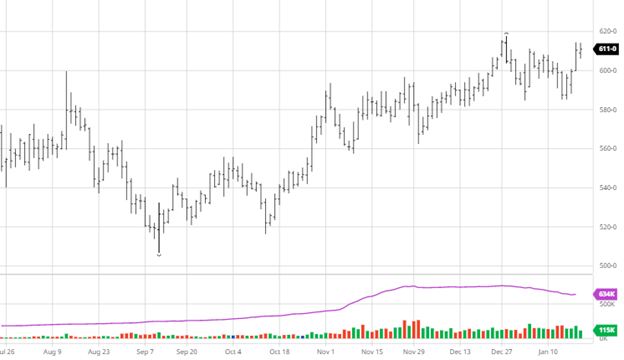

Soybeans have experienced the same volatility as corn but remain at its highs, as seen in the chart below. The story is the same as corn being driven by weather problems in South America. Barchart estimated Brazilian soybean production at 137 million tonnes, with Argentina production at 45 million tonnes. The last USDA projection had 144 million tonnes in Brazil and 49.5 million tonnes in Argentina, showing that the private sector believes the crop has gotten worse and is trending in the wrong direction. The chart below is interesting because you can see the top at $14 this week and back in July. That will be an important number to close above to keep the momentum going.

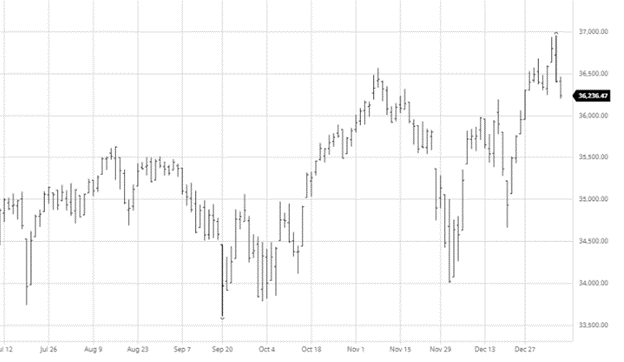

The Dow has had quite a volatile week following a week of the Santa Claus rally. The Fed may increase the rate at which they raise rates which worries some investors, but at this point with the Fed, many investors are waiting until they see the plan. As a new year starts, especially following the impressive year that was 2021, many investors try to predict the story for the year ahead. If we have learned to expect anything while Covid is in the markets, we can’t predict much for the year ahead.

The January USDA Report is Tuesday and should be a market mover. All eyes will be on the report as everyone positions themselves ahead. If the volatility of late shows up, it could be a big market mover.

Podcast

The 2021 U.S. grain crop has the potential to be one of the largest on record. Where did all the yield come from, what areas were the hardest hit, and why on God’s green earth are grain prices still so high?

Today, we are joined by several RCM Ag Services grain markets experts from around the country to catch up on a post-harvest update and share an outlook for production and marketing in each of their respective regions for the remainder of the 2021 marketing season and the upcoming 22 crops.

The 2021 U.S. grain crop has the potential to be one of the largest on record. Where did all the yield come from, what areas were the hardest hit, and why on God’s green earth are grain prices still so high?

Today, we are joined by several RCM Ag Services grain markets experts from around the country to catch up on a post-harvest update and share an outlook for production and marketing in each of their respective regions for the remainder of the 2021 marketing season and the upcoming 22 crops.

This week, corn had a good rally following a couple of big down days last week. The December USDA report was released on Thursday with minimal changes and differences between the numbers and pre-report estimates. World stocks were slightly higher than pre-report estimates at 305.45 million metric tons (304.47 MMT estimate) and marginally higher US stocks. The USDA did not make any adjustments to the South American crop estimates as they remain patient; we should expect next month to see a change. Continue to keep an eye on SA weather as any continued problems could play out in the market heading into the holidays.

Soybeans, like corn, saw a modest bounce following a couple of bad days last week. The expectation of a bearish report proved incorrect as the USDA left the stock numbers unchanged. The exports seem to have been slowing down and remain well short of the Phase 1 deal with China, so we could expect to see the export numbers lowered and ending stocks raised if there is no strong buying into the end of the year. All in all, the report lacked any market-moving fireworks.

The Dow had a strong week bouncing back from its dip as there were plenty of buyers buying the dip. As fear of the Omicron variant relaxes and positive news on the vaccine fighting this strain, this cycle of the variant worry may have already hit and bounced back in the market. Many analystsare calling for a rally into the end of the year with many firms releasing their top picks for 2022. The CPI numbers will be released at the end of the week and will play out in the market on Friday.

Wheat

Wheat prices have been falling the last week and continued falling after the report. Australia and Canada had larger production than expected. Another important development specific to wheat will be the tensions between Ukraine and Russia, as any escalation would cause problems for wheat exports from Ukraine.

Podcast

For the past year, commodity prices have perpetually soared and continue to trend higher. We’re diving into the fertilizer forecast with a unique guest, Billy Dale Strader, a branch manager for Helena Agri-Enterprises in Russellville, KY., who is truly at the epicenter of the rising fertilizer prices.

Billy Dale planted his agriculture roots on his family-owned farm and has managed regional seed and chemical sales at Helena for the past decade. In this week’s pod, we tackle the big question for farmers and ultimately end-users — is the impact of higher-priced inputs, like seeds, chemicals, and fertilizer, on the supply and demand for the major U.S. crops? Listen or watch to find out!

Volatility was the name of the game this week as every market experienced it from, grains to equities. Corn partook in the excitement, as you can see from the chart below. Important to note is following the small rally in the past couple of days to get back to the levels we saw before Thanksgiving. Wheat was a big winner Thursday and pulled corn with it on the intensifying issues with Russia and Ukraine. If wheat rallies, expect it to pull corn with it even on limited corn news. The La Nina pattern continues to form in South America as southern Brazil remains dry, and forecasts have that continuing. Another non-corn-specific factor to keep an eye on will be energy prices, as ethanol production will depend on how the omicron variant will/could affect US travel into the winter and holiday season.

Soybeans, like corn, saw a bounce the last couple of days to get back to close to the range we were in pre-Thanksgiving. The bounce has brought us back in the range we were trading for most of October, which seems like a good place for the market to hang around when there is a lack of news. Exports continued but were on the lower end of expectations this week, while soybean meal and oil were as expected. If beans could close this week over the 20-day moving average, that would be supportive for bulls who are looking for good news. As harvest is wrapped up, all eyes turn to South American weather and their crops this year.

Crude oil has sank following the Thanksgiving holiday as concern over the new Omicron variant, and its impact on demand hit the market. While these concerns are valid as much is still unknown, the largest problem that seems immediate to demand will be air travel and international travel causing, less jet fuel demand. As of right now, it does not appear to be worrying many Americans, but as more cases are found, we will see how it will affect demand. OPEC+ countries also announced they might cut output if demand falls due to the virus, leading prices back higher.

Natural Gas prices have also faltered this week as a warmer U.S. winter is expected to occur, requiring less NG for heating. Diesel prices have also fallen a lot this week following the Omicron variant news and presents farmers with an opportunity to hedge their fuel needs for next year.

The Dow experienced a lot of volatility this week as news of the Omicron variant in the U.S. and more places worldwide spooked some investors. The reports are that it only has caused mild symptoms, which is good, but the reaction was not of fear of the virus itself but how the governments will respond with potential lockdowns and travel bans soon. On Thursday, the strong bounce-back shows that investors are still eager to get in the market, so any large pullbacks will be met with buying if it is seen as a jerk reaction, but any longer lasting weakness could be seen as a correction. The down-trend of the last week has made some investors worried and moved some to the sidelines while we see what happens. Powell will stay as head of the Fed and said they might start tapering and raising interest rates sooner rather than later as inflation does not appear to be transitory.

For the past year, commodity prices have perpetually soared and continue to trend higher. We’re diving into the fertilizer forecast with a unique guest, Billy Dale Strader, a branch manager for Helena Agri-Enterprises in Russellville, KY., who is truly at the epicenter of the rising fertilizer prices.

Billy Dale planted his agriculture roots on his family-owned farm and has managed regional seed and chemical sales at Helena for the past decade. In this week’s pod, we tackle the big question for farmers and ultimately end-users — is the impact of higher-priced inputs, like seeds, chemicals, and fertilizer, on the supply and demand for the major U.S. crops? Listen or watch to find out!

Corn was struggling this week heading into the Nov 9th USDA report, where it saw a good bounce after its release before falling back to only finish up slightly higher on the day. The corn numbers that came out of the report were fairly neutral, with a 177 bu/acre yield and 15.062-billion-bushel U.S. production. The yield was slightly raised from 176.5 the month before but was right in line with estimates, so there was no significant reaction on that number. Overall, there were not many surprises for corn as most bullish reactions came from soybeans pulling them higher with them. With ethanol margins very profitable and crude oil staying higher, the demand side will continue to keep basis levels high. As harvest was 84% complete at the start of the week, there is still time for any weather issues to create issues to finish up harvest, but this is always expected, so being this far along is helpful.

Soybeans had an excellent bounce post USDA report but finished well off the highs of the day. The yield came in at 51.2 bu/acre, down 0.3 from last month, along with lower world-ending stocks. As far as U.S. ending stocks. the USDA pegged it at a manageable 340 million bushels, slightly up from last month —these numbers are not outright bullish. South America’s weather is non-threatening right now; however, with solid world crush margins, there is not much reason for a bearish outlook heading into the winter. With funds currently flat, we may hang around this area trading until new news enters the market.

There were no surprises in the wheat report,, but it did follow beans higher after a down week leading into the report. US wheat stocks came in at 583 million bushels (pre-report estimates were 581 million) and world-ending stocks of 275.80 million metric tons (pre-report estimates 276.5 MMT). Despite the recent pullback, there is still a bullish sentiment in the market moving forward for the time being.

The Dow has continued to trend higher this week as it has put together an impressive month despite Tuesday’s pullback. Many markets have led it higher from tech to industrials, with the new infrastructure bill playing a role.

Side note: The crypto markets have also been on a tear the past couple of weeks. It will be interesting to watch heading into the end of the year after an impressive last year and a half.

Podcast

For the past year, commodity prices have perpetually soared and continue to trend higher. We’re diving into the fertilizer forecast with a unique guest, Billy Dale Strader, a branch manager for Helena Agri-Enterprises in Russellville, KY., who is truly at the epicenter of the rising fertilizer prices.

Billy Dale planted his agriculture roots on his family-owned farm and has managed regional seed and chemical sales at Helena for the past decade. In this week’s pod, we tackle the big question for farmers and ultimately end-users — is the impact of higher-priced inputs, like seeds, chemicals, and fertilizer, on the supply and demand for the major U.S. crops? Listen or watch to find out!

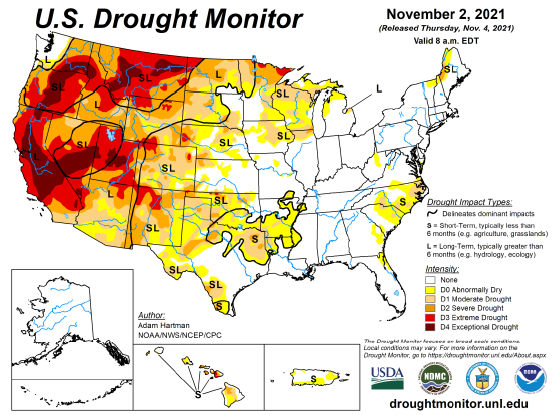

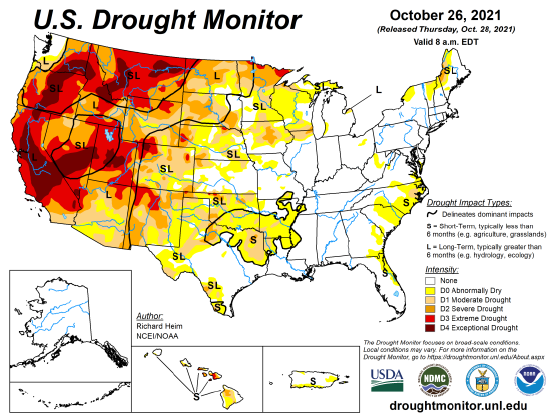

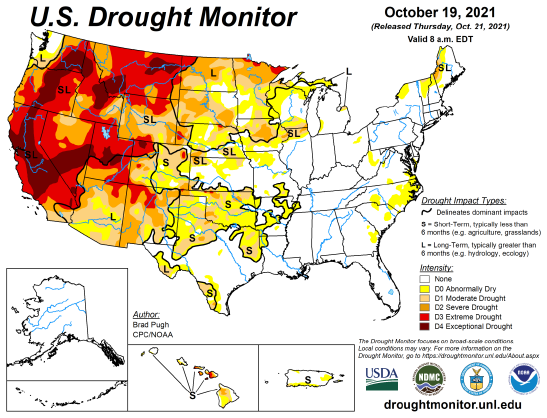

U.S. Drought Monitor

The maps below show the U.S. drought monitor and the comparison to it from a week ago. The outlined areas in black are areas that the drought will have a dominant impact.

For the past year, commodity prices have perpetually soared and continue to trend higher. We’re diving into the fertilizer forecast with a unique guest, Billy Dale Strader, a branch manager for Helena Agri-Enterprises in Russellville, KY., who is truly at the epicenter of the rising fertilizer prices.

Billy Dale planted his agriculture roots on his family-owned farm and has managed regional seed and chemical sales at Helena for the past decade. In this week’s pod, we tackle the big question for farmers and ultimately end-users — is the impact of higher-priced inputs, like seeds, chemicals, and fertilizer, on the supply and demand for the major U.S. crops? Listen or watch to find out!

Find the full episode links for The Hedged Edge below:

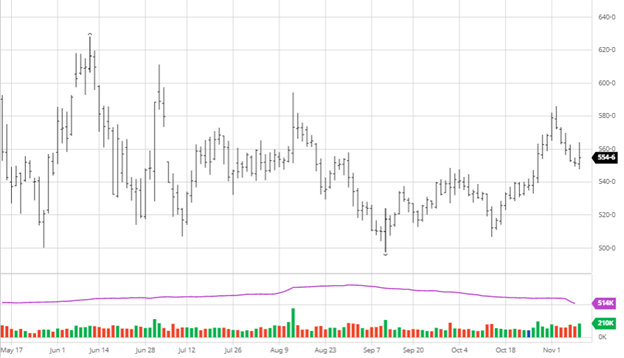

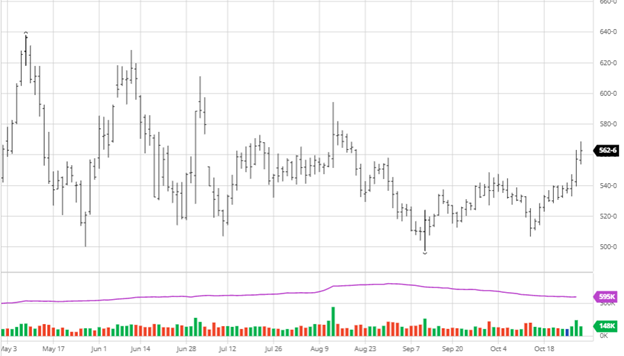

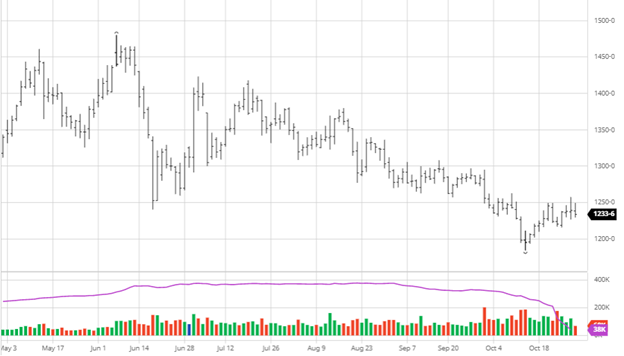

Corn has continued its rally as the bulls seem to have their mojo back following a time where they could have been uneasy. Despite the disappointing export report, corn was able to keep the momentum going Thursday. This week’s weather week will slow down harvest and could cause issues for what is remaining in the field. Higher basis has been seen across most of the country as a lack of available corn continues to put pressure on elevators while ethanol plants are running on great margins and can afford the basis. Going forward it will be interesting to watch how farmers manage the corn they store. Do they hold it until we see much higher prices? Will basis become so favorable it is hard to hold on to it while farmers are making payments for products for next year? These questions do not have any answers right now, and only time will tell, but one thing is for sure, input prices are going up and farmers know how valuable their crop is.

Soybeans have had a good bounce from their low a couple of weeks ago, even if it is not as an inspiring rally as corn. Like corn, the weather will delay harvest and reduce yields in many areas that were off to a great first half. South American weather is generally good for the next week with Argentina receiving their best rains of the season so far. The weather over the coming weeks/next couple of months will be important to getting them off to a good start. Like corn, it will be interesting to see the number of beans stored vs. sold after harvest. As beans continue to struggle to find a pattern, we hope to see one develop in the coming weeks, hopefully, a good one.

The Dow had another good week with one big down day followed by a bounce-back on Thursday. As Q3 earnings continue to roll in, it has been a mixed bag with large companies like Amazon and Apple falling post reporting.

Oats

The Oats market has been on a tear the last two months as Canada’s and the upper plains crop had a multitude of issues due to drought conditions. This has created a supply problem on top of already higher grain prices across the board this year.

Podcast

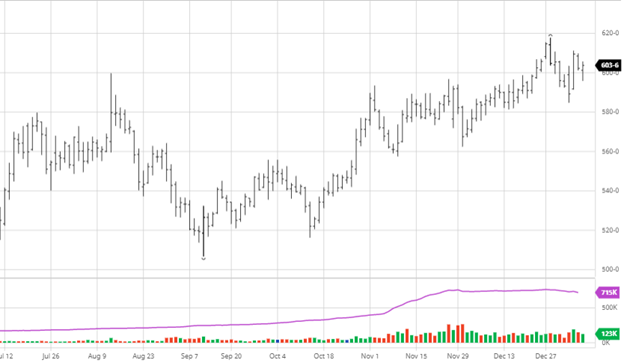

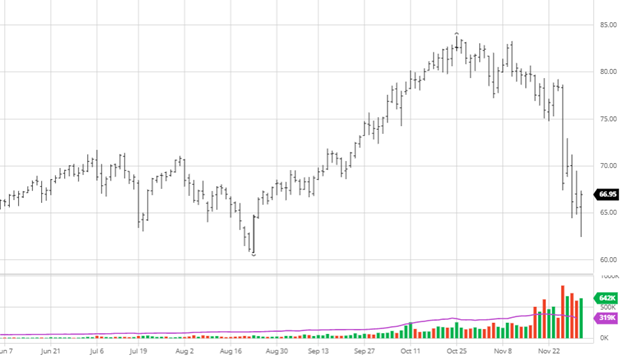

The Hedged Edge is back, and we’re jumping into the thick of the commodity markets with RCM’s own King of Cotton – Ron Lawson. Cotton prices have exploded since the COVID crash, rising more than 236% from the March 2020 lows. While prices have backed off from the October 8th high, cotton is one of the purest supply + demand-driven markets around the world and has caught fire along with the global inflation bug currently running rampant across many commodity markets.

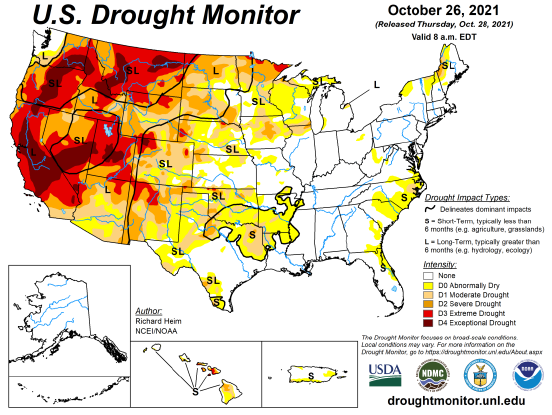

U.S. Drought Monitor

The maps below show the U.S. drought monitor and the comparison to it from a week ago. The outlined areas in black are areas that the drought will have a dominant impact.

The Hedged Edge is back, and we’re jumping into the thick of the commodity markets with RCM’s own King of Cotton – Ron Lawson. Cotton prices have exploded since the COVID crash, rising more than 236% from the March 2020 lows. While prices have backed off from the October 8th high, cotton is one of the purest supply + demand-driven markets around the world and has caught fire along with the global inflation bug currently running rampant across many commodity markets.

Will it be hedge fund influence in cotton that costs consumers more this Holiday season or will the continued logistical issues tie up cotton at ports send consumers scrambling to eBay for their “snuggies”? For cotton producers, merchants, spinning mills, and banks financing the backbone of the cotton supply, risk management must remain at the top of mind for the remainder of this year and into 2022 (as the current cycle is likely to continue to last for at least the next 12-18 months.) We’ll dive into the thick of it in this episode and more — Hold on to your hats and enjoy!

RCM Ag Services is a registered DBA of Reliance Capital Markets II LLC. Trading futures, options on futures, and retail off-exchange foreign currency transactions are complex and involve substantial risk of loss and are not suitable for all investors. Loss-limiting strategies such as stop loss orders may not be effective because market conditions or technological issues may make it impossible to execute such orders. Likewise, strategies using combinations of options and/or futures positions such as “spread” or “straddle” trades may be just as risky as simple long and short positions. There are no guarantees of profit. You should carefully consider whether trading is suitable for you in light of your circumstances, knowledge and financial resources. You may lose all or more than your initial investment. You should not rely on any of the information herein as a substitute for the exercise of your own skill and judgment in making such a decision on the appropriateness of such investments. Opinions, market data and recommendations are subject to change without notice. Reliance Capital Markets II LLC shall not be held responsible for any actions taken based on this website or attached links. Parties acting on this electronic communication are responsible for their own actions. Past performance is not necessarily indicative of future results.

Soybeans rallied this week as soy oil and meal also rallied. The noise around the problems with South America’s crop got a little louder this week with StoneX reporting that Brazil soybeans have gone to “no offer” due to farmers refusing to sell new-crop supplies in the current environment, with drought losses in the south worse than first believed. South American weather remains mixed as southern Brazil and northern Argentina remain hot and dry while southern Argentina received rain over the last couple of weeks. In early February, all areas are expected to revert back to hot and dry in the forecast. These troubles make it sound like the USDA was off on their South America estimates in last week’s report. This is a situation to monitor as any stoppage of sales from Brazil and Argentina would mean purchases from the U.S.

Soybeans rallied this week as soy oil and meal also rallied. The noise around the problems with South America’s crop got a little louder this week with StoneX reporting that Brazil soybeans have gone to “no offer” due to farmers refusing to sell new-crop supplies in the current environment, with drought losses in the south worse than first believed. South American weather remains mixed as southern Brazil and northern Argentina remain hot and dry while southern Argentina received rain over the last couple of weeks. In early February, all areas are expected to revert back to hot and dry in the forecast. These troubles make it sound like the USDA was off on their South America estimates in last week’s report. This is a situation to monitor as any stoppage of sales from Brazil and Argentina would mean purchases from the U.S.