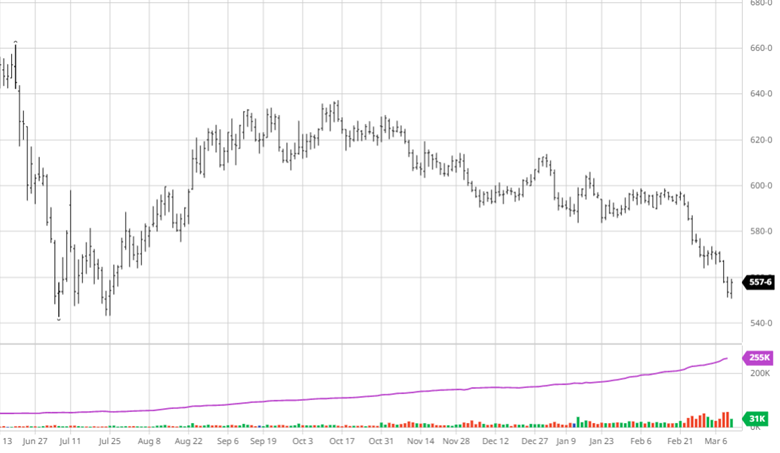

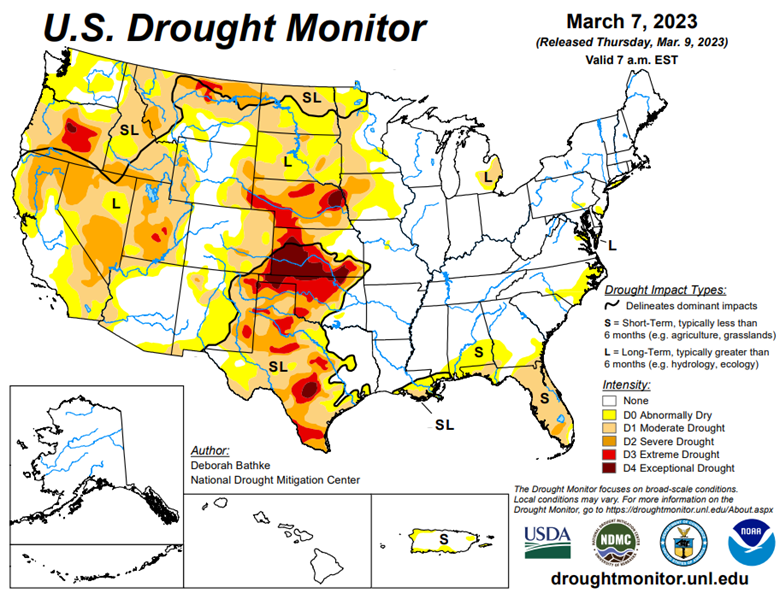

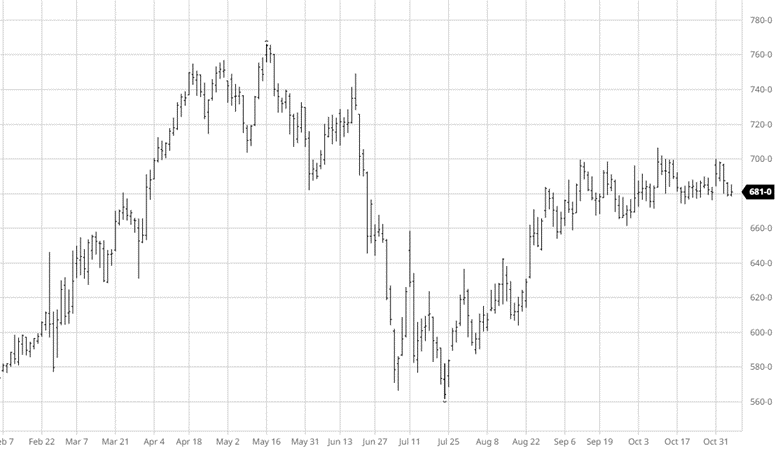

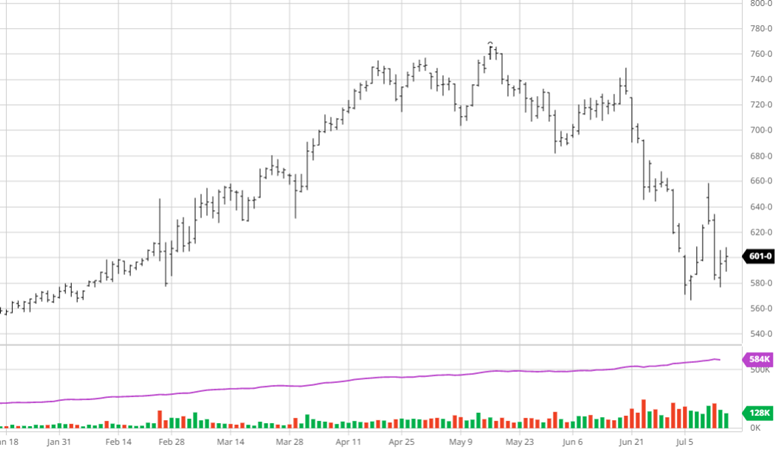

The last 2 weeks have not been friendly to corn despite a neutral to bullish USDA report this week. The USDA lowered Argentina’s production by 40 mmt, but the crop could still be smaller amid a historically poor weather year in Argentina. Corn took a nosedive to end the month of February and has taken another leg lower this week, with the new crop hitting $5.50. After a flat trade for most of February the move lower presents farmers with important decisions regarding what to do for crop insurance. With the Feb average price of $5.91, 40ish cents higher than current levels, farmers should seriously look at the highest level of revenue protection you can get. The premiums will likely be high, but the recent price movement has created an uncertain environment with a long way to go.

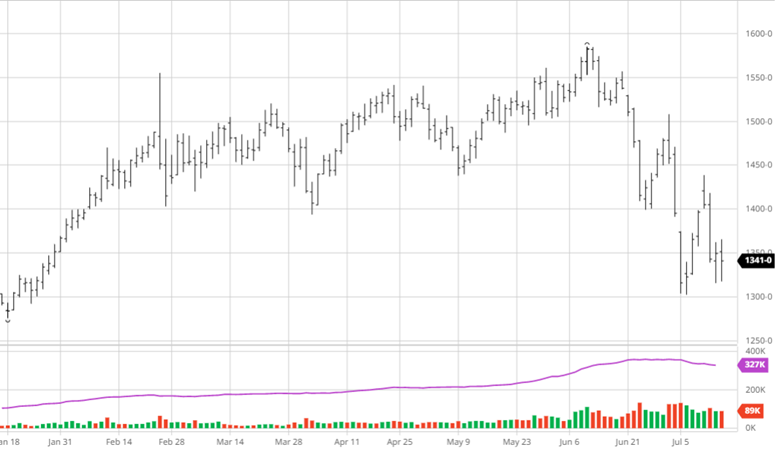

Soybeans moved lower again this week after rebounding last week as soybeans have held together better than corn. Bean stocks were tighter than the trade expected while exports were up 25 mbu but crush down 10 mbu. Global oilseed supply and demand forecasts include lower production, crush and stocks. Like for corn, the USDA lowered Argentina’s production below the average trade estimate. While the news out of the report was mildly bullish, the negativity around corn and wheat bled into beans to end the week.

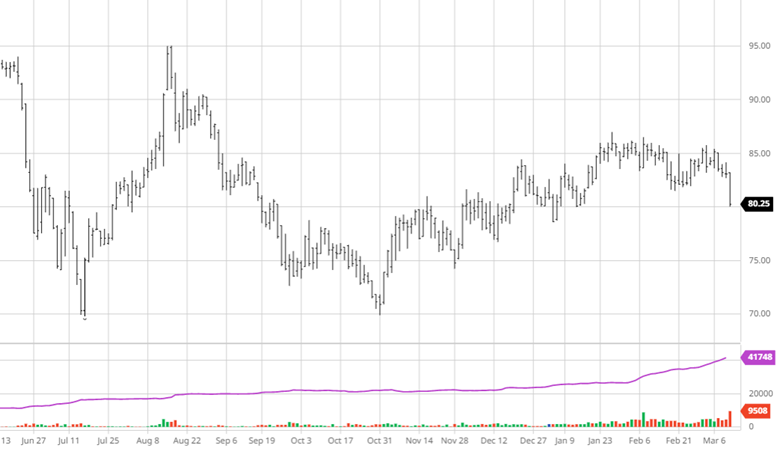

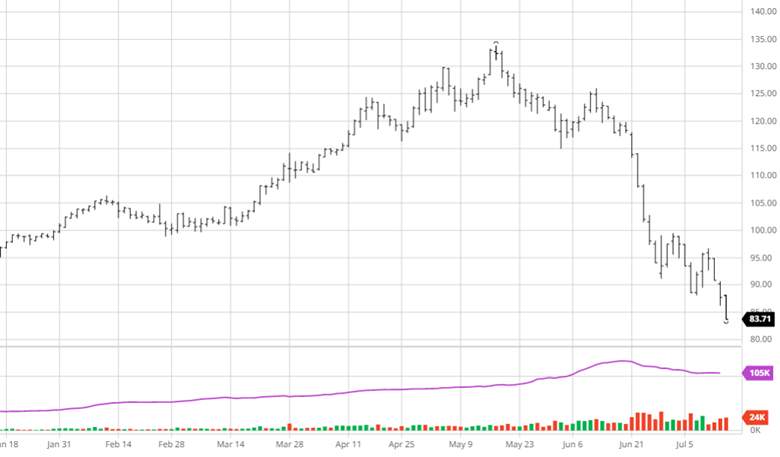

Cotton was punched in the mouth on Friday after trading lower this week. The USDA did not make any significant changes to the supply and demand report. The lack of demand is the main problem as the global 22/23 forecasts this month include lower consumption and trade with higher production and stocks. The world economic outlook is questionable for the coming year and a global recession would hurt cotton more than other areas.

The story for wheat has not changed as markets continue to get crushed. The report made no major changes to forecasts and balance sheets and there has not been any major changes in Ukraine as Russia continues their assault. Russian officials are expected to meet with UN officials in Geneva on March 13 to discuss the grain deal renewal and trade sanctions.

Equity Markets

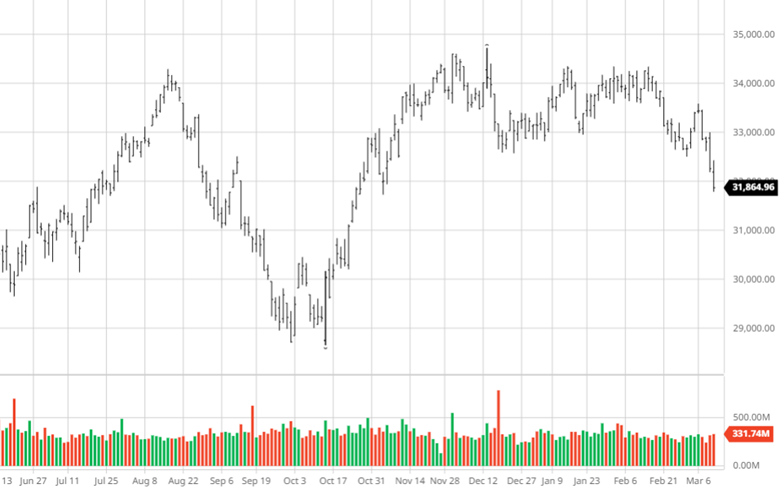

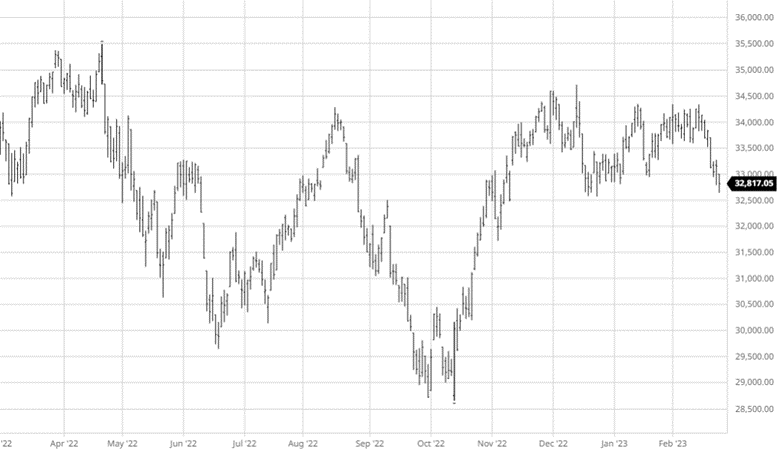

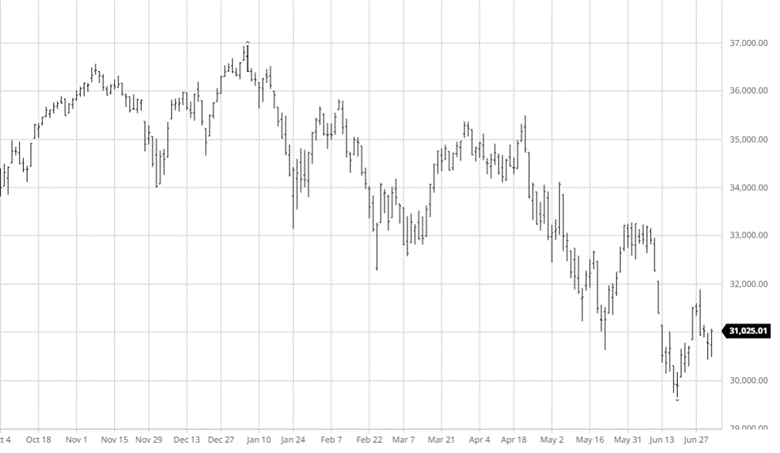

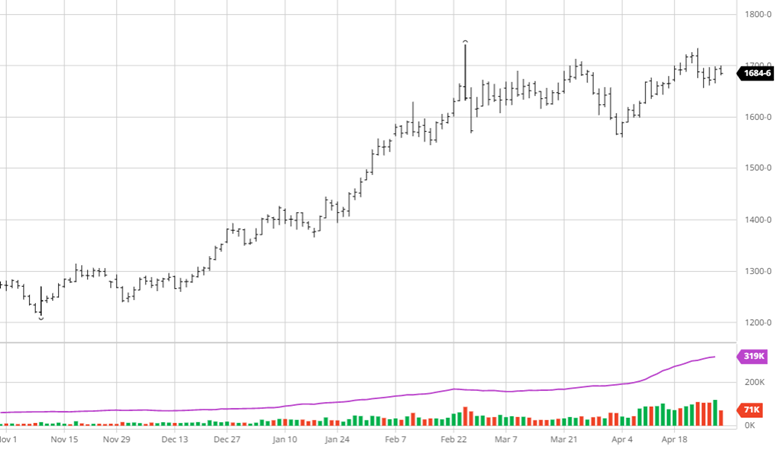

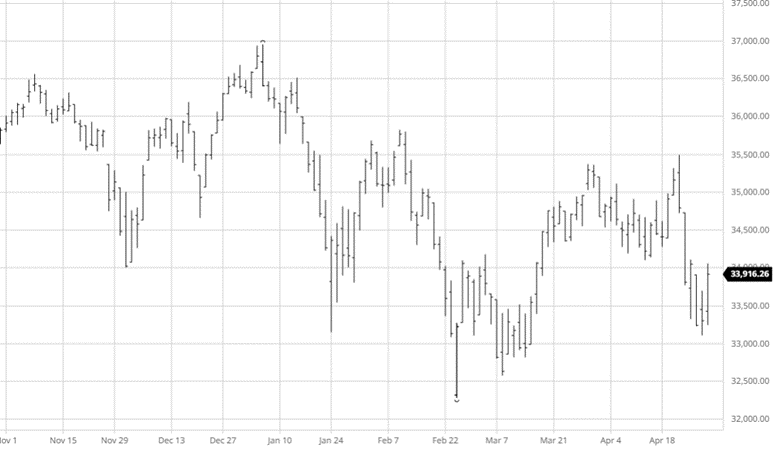

Equity Markets moved lower this week on overall market weakness and the Silicon Valley Bank news. While one day doesn’t make a trend, the trend lower since the start of February looks to have room to move lower with another big jobs added number keeping the Fed rate hikes as a question mark.

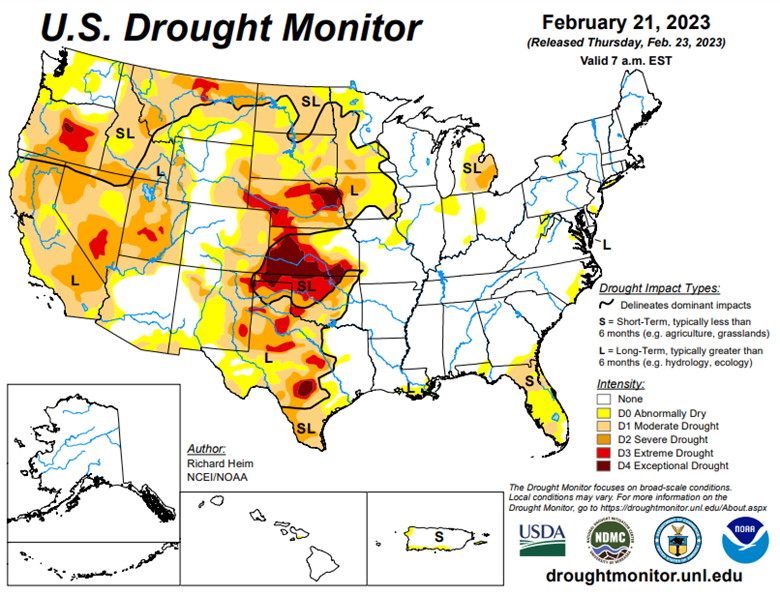

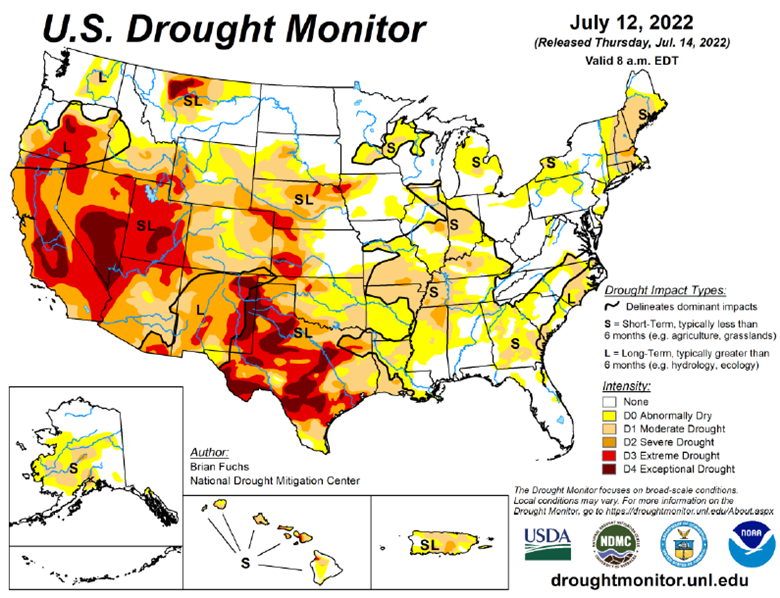

The eastern corn belt has gotten plenty of moisture so far this winter with the western corn belt needing more heading into the spring.

Podcast

With every new year, there are new opportunities, and there’s no better time to dive deeply into the stock market and tax-saving strategies for 2023 than now. In our latest episode of the Hedged Edge, we’re joined by Tim Webb, Chief Investment Officer and Managing Partner from our sister company, RCM Wealth Advisors. Tim is no stranger to advising institutions and agribusinesses where he has been implementing no-nonsense financial planning strategies and market investment disciplines to help Clients build and maintain wealth and reach financial goals since

Inside this jam-packed session, we’re taking a break from commodities, and talking about the world of equities, interest rates, tax savings, and business planning strategies. Plus, Jeff and Tim delve into a variety of topics like:

The current state of the markets within the wealth management industry

Is there a beacon of hope, or is it all doom and gloom for the markets?

Other strategies to think about outside of the stock market and so much more!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

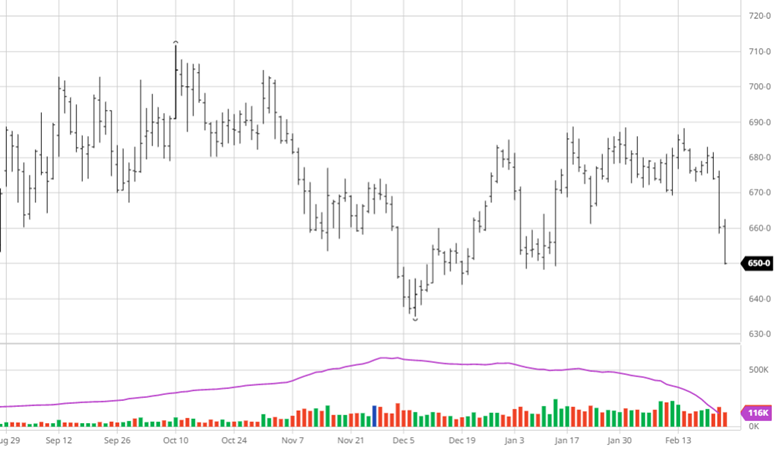

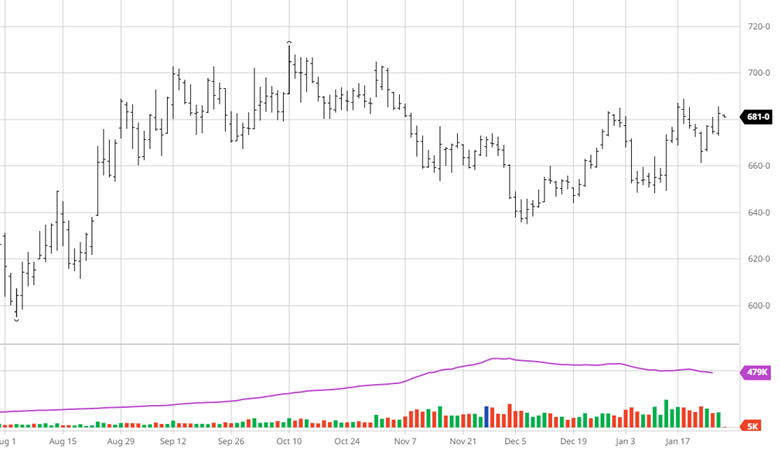

Corn took it on the chin this week as it traded lower to levels last seen in early January. The bulk of the losses came in the second half of this week following the USDA Ag Forum’s bearish numbers. The Ag Forum estimates 91 million acres of corn with a 181.5 bu/ac yield. While these numbers are not surprising as they are mostly just trend line projections the market still reacted in a bearish way as this would raise ending stocks. These numbers also expect neutral external conditions such as weather, politics, etc. While these numbers historically are not the most accurate the market does listen and this was a major bearish factor for the week. They also released their price expectation for the year with December corn being $5.60, this is about 17 cents lower than Friday’s close. February insurance prices for corn sit at $5.95.

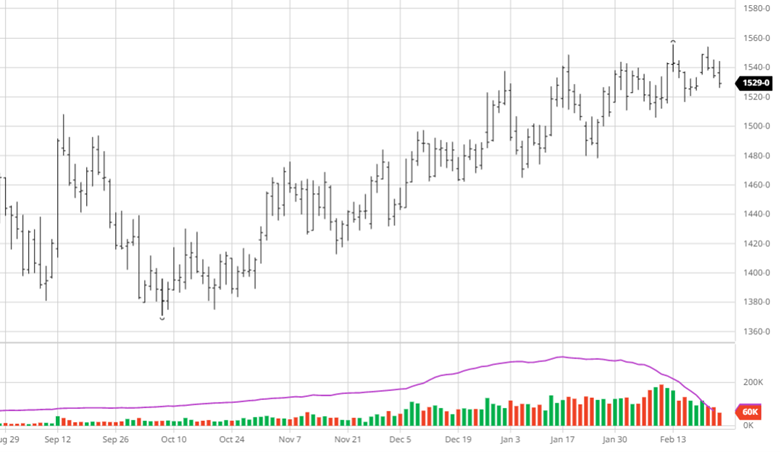

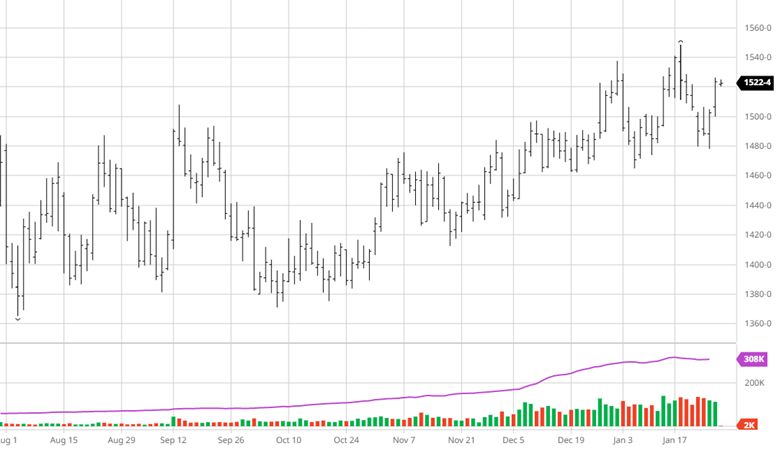

Soybeans moved lower to end the week in sentiment with corn and wheat. The USDA Ag Forum numbers for beans were 87.5 million acres with a yield of 52 bu/ac. These numbers are very realistic and did not send any shock into the market. These numbers would raise stocks by 65 million bushels to 290 mbu which would help alleviate some balance sheet stress. While these numbers were not surprising they did say they expect November bean price of $12.90, so there is room for downward movement in their view. The news that pulled soybeans lower had to do with other commodities as Argentine production estimates continue to fall and Brazil’s harvest is delayed. The insurance average for soybeans is $13.77 for November beans.

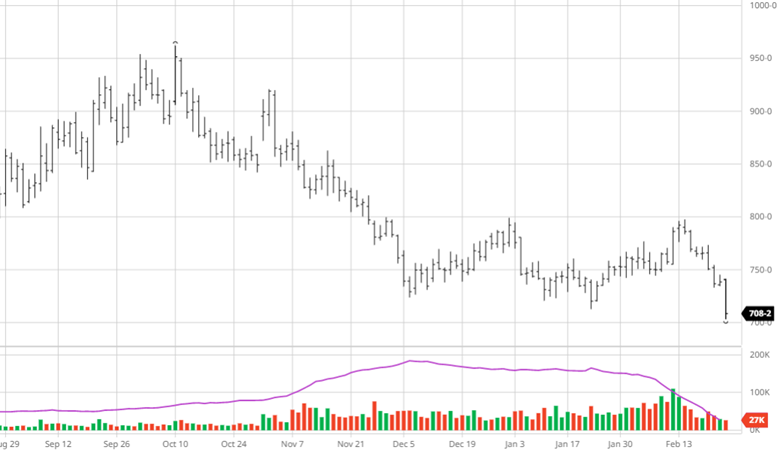

Wheat has struggled the last two weeks after pushing up against the $8.00 mark before falling all the way to $7.08 to end the week. Wheat has moved lower as Russia is selling their wheat the cheapest of anyone, with Egypt purchasing 240,000 tonnes this week. Russia selling their wheat cheaper to gain market share and get money to continue to fund their war on Ukraine. Funds were also sellers this week on the news as they expect Russia to get business as long as countries are saving money. The Ag Forum released estimates for wheat of 49.5 million acres and a trend yield of 49.2 bu/ac. This news combined with Russia were bearish but with first notice day approaches we could see calmer trade than the past few days soon.

The cotton story has not changed much as the supply/demand story has not changed. There is both a lack of demand and a supply surplus here in the US, which has led to less imports of cotton goods. With the potential recession looming the lack of current demand mixed with that does not paint a great picture for cotton as it continues to trade on the lower end of its recent range.

Equity Markets

Equity Markets were down this week as economic data keeps coming in supporting higher rates. Inflation is sticking around and earnings are mixed as February will post big losses across the major indexes. Many market commentors still believe we are heading lower from several different factors including the Fed, inflation, layoffs, valuations and more. Continue to keep an eye on the strengthening USD.

Eastern corn belt has gotten plenty of moisture so far this winter with the western corn belt needing more heading into the spring.

Podcast

With every new year, there are new opportunities, and there’s no better time to dive deeply into the stock market and tax-saving strategies for 2023 than now. In our latest episode of the Hedged Edge, we’re joined by Tim Webb, Chief Investment Officer and Managing Partner from our sister company, RCM Wealth Advisors. Tim is no stranger to advising institutions and agribusinesses where he has been implementing no-nonsense financial planning strategies and market investment disciplines to help Clients build and maintain wealth and reach financial goals since

Inside this jam-packed session, we’re taking a break from commodities, and talking about the world of equities, interest rates, tax savings, and business planning strategies. Plus, Jeff and Tim delve into a variety of topics like:

The current state of the markets within the wealth management industry

Is there a beacon of hope, or is it all doom and gloom for the markets?

Other strategies to think about outside of the stock market and so much more!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Corn made small gains over the last 2 weeks as news was quiet outside of South American weather with China being on holiday for Chinese New Year. Exports were better than expected this week, but Mexico continues to look at increasing their corn imports from Brazil. The forecast for rain in Argentina over the weekend will direct the trade to start the week. The news to look for in the coming weeks will be purchases from China and any changes in South American weather. Any developments in Ukraine will have ripple effects across the commodity space, but trying to predict what will happen there is almost impossible.

Soybeans, like corn, had an up and down 2 week span but ended with modest losses. The uptrend beans have seen since October has been promising but eventually it will run out of steam with Brazil in a good position. If Brazil’s harvest gets off to a fast start we could see a weakening in old crop quickly with new crop following slower. Like corn, bean exports to China as they come out of covid lockdowns and Chinese new year would help provide some support until Brazil starts sending them beans. Keep an eye on any positive trade news from China, don’t expect news out of Brazil to be bullish.

The cotton chart below shows the trade has stayed between 80 and 90 cents for the last couple of months. Cotton is caught in the middle of the markets thinking there will be a recession, and China coming out of Covid lockdowns with capital to spend on consumable goods. Cotton will need some news to get it out of this range, until then expect this trade to continue. While exports increased last week from the previous it is still half of this time last year, showing the demand situation is very different.

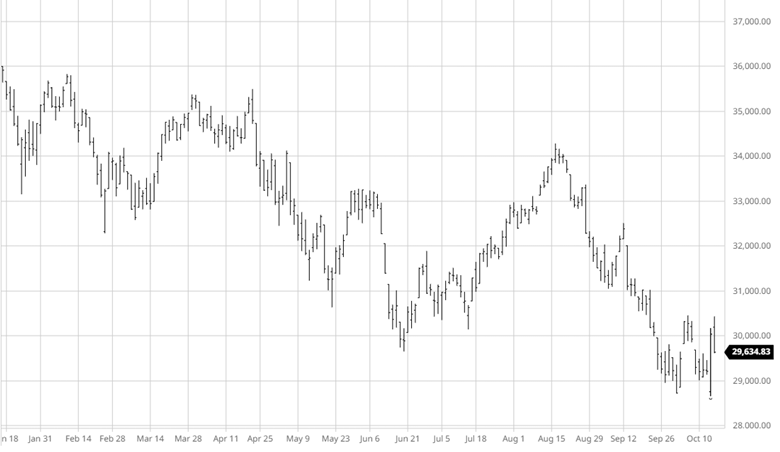

The Dow fell over the last 2 weeks as everyone is playing a guessing game with 1. What the Fed will do and 2. Will there be a recession? The economy is still doing well as jobless claims have not begun to go up and inflation is cooling but still has a way to go. With earnings underway guidance will be important to understand how companies are expecting 2023 to go with jobs and what they think the Fed will do.

With every new year, there are new opportunities, and there’s no better time to dive deeply into the stock market and tax-saving strategies for 2023 than now. In our latest episode of the Hedged Edge, we’re joined by Tim Webb, Chief Investment Officer and Managing Partner from our sister company, RCM Wealth Advisors. Tim is no stranger to advising institutions and agribusinesses where he has been implementing no-nonsense financial planning strategies and market investment disciplines to help Clients build and maintain wealth and reach financial goals since

Inside this jam-packed session, we’re taking a break from commodities, and talking about the world of equities, interest rates, tax savings, and business planning strategies. Plus, Jeff and Tim delve into a variety of topics like:

The current state of the markets within the wealth management industry

Is there a beacon of hope, or is it all doom and gloom for the markets?

Other strategies to think about outside of the stock market and so much more!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Corn strung together several days lower in a row last week with a neutral USDA report in the middle of it. The USDA raised the US yield to 172.3, which was within the range of estimates. While corn had been trading sideways for some time, the move lower remained in its trading range, followed by a bounce back higher this week. The black sea export corridor deal being renewed is welcome news for the world supply chain. Brazil and Argentina got some needed rain while some dry areas missed out. They are still suffering drought conditions, but it is also still early in the year. Exports improved this week from last, as the current price levels attract buyers.

Soybeans fell over the last two weeks, due to two days of large losses this week. Soybean Oil got hit as world veg oil prices fell, pulling beans down with it. The rain in Argentina helped speed up soybean planting but rain will still be needed moving forward as still about 25% of the country experiences drought. Bean exports, like corn, improved and better than expected this week. The lack of news makes this a difficult market to trade in as there are no overwhelming bullish or bearish factors dictating direction.

The US cotton supply was raised in last week’s USDA report with better yields and lower demand. The problem in the cotton market right now is demand. While more money is being spent , fewer units are being bought which translates to less consumption. With the continued high energy prices and inflation issues across the world people are prioritizing eating and heating their homes and fueling their cars (good call) over buying new clothes. The potential for a looming world recession in 2023 does not ease demand concerns as we would not see demand for cotton pick up as producers would sit on inventory they currently have. Until we get more clarity on the world outlook and 2023 it is a time to be cautious. The weakening USD will be worth keeping an eye on.

The equity markets started off November with gains after a cooler than expected October CPI of 7.7%. While a drop is nice to see it is important to remember the target is 2-3% so we are still much closer to the top than the bottom with a Fed rate rise coming in early December. The markets seem to expect a 50-point hike, but there is still plenty of time for that to change and get priced in before. One big question that remains for the markets looking ahead is “what will December bring?”. Will there be a Santa Clause rally? Will markets fall as investors do some tax loss harvesting? Many investors still think a recession is coming in 2023 and the next month and half could give us a better idea what to expect.

The Hedged Edge is back online with a guest who could be this podcast’s most important guest of all time. At a time when inflation is running rampant through the world economy, drought conditions are drying up our rivers, and the global supply of grain is scarce. We are tasked with the question, “what the hell is going on in logistics, and is there any relief in sight?”

To help address these questions and more, I am joined today by a man that needs no introduction to most in the physical commodity sector – Woodson Dunavant with the Dunavant Logistics company based in Memphis, TN.

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

The Hedged Edge is back online with a guest who could be this podcast’s most important guest of all time. At a time when inflation is running rampant through the world economy, drought conditions are drying up our rivers, and the global supply of grain is scarce. We are tasked with the question, “what the hell is going on in logistics, and is there any relief in sight?”

To help address these questions and more, I am joined today by a man that needs no introduction to most in the physical commodity sector – Woodson Dunavant with the Dunavant Logistics company based in Memphis, TN.

And last but not least, don’t forget to subscribe to The Hedged Edge on your preferred platform, and follow us on Twitter @ag_rcm, LinkedIn, and Facebook.

_______

_______

Check out the complete Transcript from this week’s podcast below:

What the hell is going on in logistics and is there any relief in sight? with Woodson Dunavant

Jeff Eizenberg 00:14

Welcome to the Hedged Edge by RCM Ag Services where we’re getting out the field and onto the mic to bring you weekly market updates, commentary from commodity experts in monthly interviews with the biggest names in agribusiness. Welcome to winner at least it feels that way after the one of the warmest falls in recent memory. Today, the hedged edge is back online with a guest who could potentially be the most important guest of all time on this podcast. At a time when inflation is running rampant through the world economy, drought conditions are drying up our rivers and global supply of grain is scarce, are tasked with the question, What the hell is going on in logistics? And is there any relief in sight? To help address these questions and more I’m joined today by a man who needs no introduction to most in the physical commodity sector once and done event with the done event logistics company based in Memphis, Tennessee, what’s in is the Senior Vice President of agriculture and Global Network Development for the company. And as part of the fourth generation of done event family to work for the company. He worked across the globe specializing in cotton trading from 2001 to 2009. And spent four years in equipment leasing, what’s in currently serves as logistics sales and business development for event focusing on the international market. He’s a member of the executive board of directors for Donovan Enterprises, Inc, and is on the board of directors of the Memphis Cotton Exchange and the Memphis cotton Museum. He received a bachelor’s degree in finance from Auburn University. Go War Eagle. What Dr. Woodson, welcome to the show.

Woodson Dunavant 01:59

Thank you. Thank you. Thanks for having me, Josh. I appreciate it. Glad to be here.

Jeff Eizenberg 02:02

Yeah, it’s good times. I mean, my first question your Memphis with the river being as crazy as it is really concerned for the catalyst industry and the restaurant industry. You know, I’ve I’ve had lunch at Blue City cafe over there on Beale Street. The guy told me he’s, he’s, you know, cooking up 180 fish a day. What? How’s he doing in all this? Oh,

Woodson Dunavant 02:26

to be completely frank, he’s doing just fine. Because all his cat fish are not coming out of the river. They’re coming out of the cat fish farms. They’re all in the delta. So he’s gonna be okay. He’s gonna be quite alright.

Jeff Eizenberg 02:36

He’s alright. Okay, well, I thought maybe they were you know, he’s grabbing them off the bottom fish at the Mississippi or something?

Woodson Dunavant 02:42

No, but they are finding each day that goes by you get somebody on the news saying that they found a civil war piece of memorabilia or something, you know that the river hasn’t been this low. And however many years and you know, you’ve got all these treasure hunters that are down there looking for some and things of that nature. But, you know, the real crux of it is what is it doing to the to the grain shippers right now. And it’s a mess. In some cases, you know, the river, where we used to be able to do two barges pass on one another. Now, in some cases, it’s just one line traffic. And then throw on top of that, typically, some of these barges will be able to go to three, you know, far out, and now they’re only able to go you know, back to back, if that makes sense, to lane single. And then add in that to the fact of the river being as low as it is, then they can’t carry the payload that they would be in years past as well. So you push all that back to the farmers pocket. And you know, his supply chain costs have really, really gone up a B, he can’t move the volume that he’s used to moving. So what is he doing? In some cases, you know, they’re just going to sit and put their put their product in their in their bed or their silo, until until things get better, which, you know, there’s there. I don’t know when that’s going to happen. You looked at Long long term forecast, things of that nature, you know, a couple couple inch rain in the Midwest, it isn’t going to move the river level up by 10 feet. So you know, we’ll just have to wait and see how that how that goes.

Jeff Eizenberg 04:26

It’s kind of a wild ride right now. And yet, the pictures and the images are stunning people sending drones to give you pictures. I do sense. I don’t want to get too into this before we get a little bit more background. But I do have a question and maybe we’ll tackle it a little bit later about about those drunk drunk foot photos. I feel like a little more a little. Maybe not exactly the river. They’re like the tributary so kind of make it sound a little worse than it is. Yeah, so what you just described is pretty pretty dire. Um, Before we get too far into into the state of things, Watson, I think it might be best if you could just to share your background of the company. And you know why we’re even talking with you about logistics. I mean, you guys have had an extensive knowledge of logistics systems, both rail, barge, freight, etc. So if you could maybe just share a little bit of that background, and then we can jump into these problems. And hopefully, you’re not going to solve the world’s issues by the end of this call.

Woodson Dunavant 05:32

No, there’s no question that that’s gonna happen for sure. We might need a beer, a glass of wine to really get to the bottom of it. So yeah, so don event is a family company that started in cotton trading with my grandfather, back in the 30s. In the 40s. My father took it over, took over the business in the 50s, when his dad passed away when he was in his late 20s. So he was sort of thrown into the fire. Early on, he was down on on Front Street, where we were all the cotton traders were at that time buying cotton from the Delta and and shipping it to the US textile mills, you know, the manufacturers who were ever on the East Coast, and even in the northeast,

Jeff Eizenberg 06:18

they no longer exist, right? Yeah. So,

Woodson Dunavant 06:21

you know, we used to consume between, you know, call it 10 and 15 million bales a year domestically, and right now, we’re just north of two. And, you know, we’ll talk about this later. But, you know, manufacturing coming back and things of that nature, you know, is that, you know, is that gonna go back to 10? million? No, is it gonna go to five? I doubt it. But who knows? You know, we’ll, again, we’ll hit on Mexico and other things like that later. But yeah, I mean, it is the US textile industry is very, very small. So. So what does that mean? So, as we transitioned into that, it mean, it meant that there was a blow up in the international world for textile manufacturing, primarily in in Asia, Southeast Asia, subcontinent, so on and so forth. So as as manufacturing, went overseas, my father went overseas as well, to be able to sell, sell cotton. So we were buying cotton, you know, from the 80s and 90s, early 2000s. Were buying cotton anywhere in the world, that cotton is being grown, and then we’re selling it to the manufacturers. So

Jeff Eizenberg 07:35

you’re buying from Australia, India, all over the world,

Woodson Dunavant 07:38

anywhere there was yeah, it was Becca, Stan, Brazil, Australia. Tragic. I mean, you name it, wherever it was being, wherever it’s being grown, we were there, buying it, and then selling it to the manufacturers. So in the mid 70s, my dad made the first sale of cotton to China, which was a huge development. I think that was in 72. And then Sunday eight, we made the largest sale of a million bales to the Chinese government. So that was really a big thing for both our company as well as us. cotton industry. And now today, cotton is, excuse me, China is still the largest consumer of us cotton in the world. They have a large crop themselves, but they they have a major surplus of need of imported cotton.

Jeff Eizenberg 08:32

So thank you, Nike and Adidas and everybody else, right?

Woodson Dunavant 08:37

Yeah, yeah, exactly. All clothing, upholstery. But you know, even stuff that you wouldn’t think of what cotton goes into is manufactured over there. And a lot of times brought back over here as well.

Jeff Eizenberg 08:52

So with all those purchases, and sales, then comes the logistics portion. Correct?

Woodson Dunavant 08:57

That’s right. That’s exactly right. So it’s still cheaper for the retailers kind of looking from field to fabric here from for us to ship a bale from St. Mississippi, to Shanghai, and then bring that bring that shirt back here to Memphis, it’s still cheaper to do that than it would be to do it here in the US, which is really, I mean, you can’t blows your mind. Really, the that’s the way it is. But that’s the way it is. So

Jeff Eizenberg 09:25

I got to ask a question about that. So it’s so interesting to me, the way you describe it like that, is it you’re gonna get the bail here, you ship it over, and it comes back. And then is it just because you have this, your network of the supply chain there is so strong that you’re able to from a net con economies of scale, have enough flow that you have enough movement between the vessels that you’re able to then you know, take it over. You don’t have to sit on a container for, you know, six weeks for it to manufac Asher, and come back. But you have enough flow where there’s always a container ready to come back the other way?

Woodson Dunavant 10:06

Yeah, I mean, that’s Jeff, that’s really deep. And I really wish I could tell you that, yes, we were involved from the field in the US all the way to the manufacturer. And then back here in the US. There’s so many different segments of that Donovan is not involved in that entire supply chain. Well, that would be really cool. If we were Yeah, it’s just there’s so many different pieces to make that puzzle all come together.

Jeff Eizenberg 10:31

We don’t need to get too in the weeds. But I’m curious if you were involved

Woodson Dunavant 10:35

with with our customers with helping them move it from the field to the oversee port, and then we sort of lose track of it there. And then on our on our import side, you know, we’re responsible from once the goods hit the port in Asia, to deliver them here to the United States and the distribution facility got because there is there is a dark area, there are a gray area that we’re not involved at all,

Jeff Eizenberg 10:58

leave that to somebody on on their side that can speak a language and manage that process got

Woodson Dunavant 11:03

Correct, correct. That’s right. That’s right. So so we did all the all the cotton trading, you know, the mid 2000s, come along, you know, 2007 2008, I’m sure some of your your, your readers will remember those days now crazy thing for when the spec and hedge funds got really involved in commodities that they thought they needed to commodity bucket in addition to their bond bucket and their equity bucket. And that really changed things from us where we’re trying to keep a hedged book with against our long physicals, the market would run up, we’d have short futures against our physicals. And then, you know, in order to hold those positions, we’re having to send money margin to keep those positions. And it just got, it just got too much for my dad and our family, whereby, you know, our net worth was on the line. And it just, it became really uncomfortable from a family standpoint, from a from a financial standpoint, everything and so he, you know, had the foresight to look at possibly marketing our cotton division. To sell it, we had multiple suitors. At the end of the day, Louis Dreyfus Corporation was the one that came in and bought all of our cotton trading people and divisions around the world. So we had things that they did not have in Central Africa, in Brazil, and Australia. And so it really helped them put together, you know, the full global portfolio footprint that they needed to go to the next level. So

Jeff Eizenberg 12:42

it’s no surprise today, they are the largest of, you know, knowledge. They’re right there. Yeah,

Woodson Dunavant 12:48

that’s correct. And we were in Donovan Donovan was right there with him, we were doing between four and 6 million bales a year globally, you know, between one and $2 billion of revenue, we were spending, you know, upwards of $250 million a year in logistics. And so that’s when the whole logistics thing for us sort of sort of tipped itself off. And when we were when we made that sale to them, you know, they they did not want any of our people that were doing the logistics. So we, we kept those people and we’ve built this this Threepio, which we will go into more detail about.

Jeff Eizenberg 13:25

That’s great. So then how many people that are on the team today, across the globe? As I know, you have global operations?

Woodson Dunavant 13:32

Yeah, it’s really hard to say, to put a number a finger on an exact amount of people, we’ve got a lot of contractors, we’ve got agents, we’ve you know, so it’s a real hard number to put, I mean, it’s north of 200. But it could balloon up to if you include contractors and agents and all that. I mean, it’s a really big number.

Jeff Eizenberg 13:57

Sure, not to mention all the people that are involved in you know, running the rail or you know, trucking etc, you get to put everyone together in the 1000s. So it makes makes good sense. Okay, well, that’s a that’s one heck of a ride for you. You’re in the family and obviously, to get to where you guys are here today. Now, it would have been seen that natural that you’re also still heavily involved in cotton.

Woodson Dunavant 14:27

We are we, we do so we do freight forwarding for a lot of our old cotton competition. We do a lot of a trucking and logistics for them. The whole bucket of Donovan logistics, it’s probably 10 or 15% of what we do. So it’s not it’s not it’s not as big as I would like it. But it’s still it’s a core. It’s a core business for us. And, you know, we do everything like I just said from documentation to try Looking to ocean freight in some cases. So yeah, cotton is in our blood and we can’t get it out of our blood, nor do we really want to so the side that we’re in now, we don’t have any risk for, for cotton and being able to be in the business without risk is a good thing.

Jeff Eizenberg 15:17

Yeah, I agree with that, you know, that’s, we’re all in that business. And it’s, it can be heart palpitating. So, okay. 15% is cotton, what other products are involved in agriculture, or if if it can be shipped your yours,

Woodson Dunavant 15:35

if it’s if it can be moved in a container, Jeff, where we’re going to be involved in it. So, you know, we’ve done everything from Peanuts, to soybeans, to corn to Rice, tobacco, alfalfa, you know, just anything agriculture, you know, we’d like to, for someone to come to us with a challenge of, you know, we’re only able to get 20 tonnes in a container, well, let’s bring it to a major city or a big place where there’s heavy weight, translate it, and we’ll get 25 times in the container. So for every five moves, you’re getting a free container. So every four, so yeah, that those are the types of things we like to look at with with our customers is how can we do things different? How can we maximize our plate payload? How, you know, how can we how can we be a solution to something that they need help with and that that’s how we grow our businesses is people come to us with problems and we help solve.

Jeff Eizenberg 16:32

Yeah, well, listen, that’s, that’s, that’s a great service. And obviously, you’ve been able to continue to grow. So you’re, you’re based in Memphis, would that also then insinuate that a majority of the operations and movements starts and ends there on the river? Or are you also focused on the ports and the International terminals as well?

Woodson Dunavant 16:56

Yep. So Memphis is home. Obviously, Memphis is where our headquarters is. Memphis is, is near and dear to our heart. And Memphis is great. We love Memphis, we see the growth. We’re very bullish on Memphis. As you know, we’ve got all five major railroads here, which only Chicago has that going through them. We’ve got the largest freight airport, with FedEx moving through here. We’ve got our 40 corridor, trucks moving, you know, east to west connecting the east to west coast. 50 fives connecting Mexico with Canada. So we’ve got, you know, road rail runway. You know, it’s all here. And so we’re, we’re very bullish on that. But to your question, no, Donald’s moving product in and out of every major rail hub in the United States, as well as port, we concentrate in the southeast, and then the Gulf, Houston and Dallas, Memphis, Savannah, Charleston, Norfolk, Baltimore, Wilmington, and then an inland we’re, we’re Nashville, and Memphis in Atlanta. And as I said, Dallas, so we’re really focused in the southeast, and then the Gulf. But we’re also moving product in and out of the P and W, in the northeast, as well. And in southern Florida. So there’s no real you know, we’re, we’re spread all across. So we’re lucky in that regard.

Jeff Eizenberg 18:29

That’s great. I guess it really kind of circles back to, like I said, at the beginning, you’re one of the most important people in the world to be talking to you right now. If you’re, you know, you’re so spread out that you are touching so many different pieces of the overall logistics. gameplan, or footprint, let’s call it that. And we all have been hearing about all the problems that are out there. And I guess, before we just say today, this is the problem today. It seems as if this the backups and the issues and the increasing costs and everything kicked off with COVID with the COVID pandemic, and then it’s just really never cleared the system. And then now we have new problems, right, we’ve got drought and other conditions. Was it was this is it fair to say that that was really that was the kickoff the Genesis? And is is that portion of it? Or is it portion of that portion worked itself through and we’re now facing other problems? Where are we at?

Woodson Dunavant 19:31

Yeah, I mean, COVID changed the supply chain. Things are not going to go back to the way they were pre COVID. Right? Post COVID COVID, whatever. I mean, it’s not going back to the way it was right. That’s crystal clear. The question is, what is it going to do in the future because it’s going to change again. You know, rates went through the roof. Now they’re crashing back down, both from mostly frame rates, breakpoint rates, yes,

Jeff Eizenberg 19:58

interest rates are going straight up. Yeah, interest rates going up

Woodson Dunavant 20:01

freight rates going down. I mean, we’re, we’re in a freight recession right now, you know, importers have, you know, they couldn’t get their hands on enough inventory. Well, now they’ve got too much inventory, and they can’t move it. The consumer is not buying as much as he was, you know, they all got scared last year, a lot of the retailers and they couldn’t get their product in for Christmas time. So they brought it in super early this year. And so you know, they are chock a block full these warehouses. I mean, I was reading this morning, Jeff, historically, historically, warehouse levels are about call it 10%. In terms of in terms of vacancy rate, and okay, right now, you’re at, like, want to say, like, around 3%. And it’s literally around 10% For the last decade, and so at 3% Now, it’s a good time to be in the warehouse business. Now. It’s done like, yeah, yeah. So you know, all that’s going to change, you know, everybody’s gonna go out and get their warehouse space, and then then demand is gonna go up, you know, and then things will change. But as it stands right now, being in the warehouse business is a very good business to be in.

Jeff Eizenberg 21:18

Yeah. And then you mentioned, when we talked to a couple of weeks ago, something that kind of speaks to that you said Amazon did their, their Black Friday, Black Friday, a week, thoroughly, which forced even more warehousing to be space to be taken up?

Woodson Dunavant 21:36

That’s right. That’s right. So and it’s not just Amazon. I mean, it’s all these retail guys, they’re all in the same boat together. So, you know, with with, you know, interest rates dealing with they’re doing geopolitical unrest, unrest and Ukraine, and in that area, diesel costs through the roof has really got me concerned, both in North Europe and in here in the, in the United States. I mean, there’s just a lot of uncertainty right now. And, you know, we’re just gonna continue to service our customers and do what we know to do, and just sit back and watch, you know, some of those other things that are outside of our control, but at the end of the day, affect me, my business, your business, my pocketbook, your pocketbook. So, you know, a lot going on right now. And obviously, the China and Taiwan deal. I mean, it, there’s a lot to be keeping around right now.

Jeff Eizenberg 22:34

Right. And there was a period in time when, you know, we saw the pictures on the news of, you know, 500 or 1000 boats back at the LA port. And, you know, a lot of that issue cleared the port issues

Woodson Dunavant 22:50

that cleared up, or I wouldn’t say it’s, I wouldn’t say it’s cleared. But it is, it is working itself out. The issue now is in Savannah, I think they’ve got 20 or 30 vessels awaiting birth there. So you know, once everybody saw everything in LA, they were like, alright, let’s switch everything to the East Coast, into the Gulf. And so you’re having some residual stuff there on the east coast, but you know, it that’ll work itself out, especially with demand dropping right now, I mean, a lot of our import clients have, you know, where they were doing, call it 30 to 50 containers a week of product, you know, they’re less than 10 an hour. And that’s, that’s material, you know, that that’s a massive drop in volume, the ocean carriers are pulling, pulling service out of the market to try to stabilize rates. So where they had four vessels that were on a string from Shanghai to LA, well, maybe they’re only doing two now. So you know, that that’s what they do in order to get their rates back up as they pull capacity on the market.

Jeff Eizenberg 23:58

But sounds like the airline industry, I think I paid like $800 to fly to Dallas a couple weeks ago, like really good. Two years ago, you were giving me a flight for $120.

Woodson Dunavant 24:11

We looked at going out west for spring break. And I can’t even tell you what it’s going to cost to fly a family of five from Memphis to Utah. I mean,

Jeff Eizenberg 24:22

we’re doing it we’re going to Park City and thankfully, I have a friend who has a place to stay but man, aside from that, I’m not

Woodson Dunavant 24:32

Yeah, it’s, it’s, it’s crazy. So so that’s what the that’s what the ocean liners do, as well to take capacity out of the market in order to stabilize rates. So, you know, they’ve done quite the ocean carrier community has done quite quite well in the last couple of years. So we shall see. You know, we should see how they prevail going forward, but I would think they’re going to be okay.

Jeff Eizenberg 24:59

Okay. circling back to commodity markets here. And I’m curious to the back to the river, I guessing that believe something like 60% of all US exports run through the Mississippi, and you were describing this one lane traffic versus multi lane. You know, as I start to think about what this is going to mean, have you seen a shift where people are, your customers are starting to, you know, hire rail and truck and, you know, incur those additional costs that are associated with having to move off the river? Or are you or our or our people, like you said, farmers just stuffing their bins full and the rest of world has to wait?

Woodson Dunavant 25:44

Yeah, I think that’s what you’re gonna see. I mean, you look with demand slowing down. That’s a good thing right now, what you would never say the demand is a good demand slowing down is a good thing from a farmer’s perspective. But to answer your question, I mean, we’re not seeing the grains go from, from a barge to, to the road, for example, me, you’re not, you’re not seeing, because at the end of the day, most of those sales are our bulk sales. So the product has got to move in bulk, you know, and it’s not going to be able, you’re not going to be able to move it to Memphis, and then, you know, I guess you could bulk rail it and translate it at a port. But if you’re not already doing that, in order to set something like that up, I mean, your costs are gonna go through the roof. And so yeah, I think it’s just kind of a sit back and wait, right now do what they can and try to fulfill the contracts if they can, and just just do their best. I mean, look, what the dollar is strong as it is, you know, that’s hurting them as well. So, you know, the farmers are going to be okay. But, you know, they’re just gonna go through a rough patch. And unfortunately, right now, from a timing standpoint, you know, all the crops are coming off right now. And so, you know, they want to get them on the move and get get them out and get ready for new crops. But that doesn’t look like that’s going to be the case next year.

Jeff Eizenberg 27:03

Well, you know, people can wait for close, they can’t really wait for food. So at some point, the basis is going to have to shoot straight up or, you know, they’re gonna have to figure out other solutions to get moving unless, of course, we you get some of the rain. And I guess, you know, you’ve been doing this long enough. 2012 was another drought year, and because we’re reading that the river was, you know, significantly low at that point. What was your experience in that timeframe? And how long did it take before you started seeing things kind of working more normal? Again? Not March or April or May that this? Yeah. potentially even subsides? Yeah. It?

Woodson Dunavant 27:44

I mean, it just depends on on on weather. Really? But yeah, I think spring is what you’re looking at. Once you get the snow melt off from the Midwest. That’s what typically always give the river its strength in its in its last as is that Snowmelt Runoff from north to here. And then that obviously takes it all the way down to New Orleans. So yeah, I think it’ll be spring, at the earliest. So, you know, hopefully, we can get, you know, enough enough rain and wet weather around here to be able to come back up a little bit, but it’s not going to be able to go back up to where it needs to be until until the spring.

Jeff Eizenberg 28:30

Let’s shift over here a little bit. You’ve mentioned the work and expansion of the company over the years. And, you know, I read an article that you guys posted, maybe earlier this year, on the growth in Mexico, do you just maybe talk to us a little bit about what you’re seeing there? Is it? Is it what’s what problem are you solving by expanding into Mexico?

Woodson Dunavant 28:55

Well, we’re, what problem we solve. And so we’re helping solve our customers problems. That’s what we do. And, you know, we saw an opportunity, with things in Asia slowing down of people and things moving, you know, not reshoring to America, but nearshoring to America. And you know that that’s where Mexico comes in. I mean, I’ve talked to multiple people, you know, over the past few months and even years, you know, maybe the quality of the product produced in Mexico doesn’t meet what it is in China, but they are somewhat competitive from a labor standpoint. So if we can get that quality then then I think you would see a massive, massive move to manufacturing in Mexico. So we saw an opportunity we’re it done event has operations at every border crossing from Laredo all the way to Tijuana, and everywhere in between. So we’re moving product both in and out via truck and rail. We have cross docking, we have warehousing. So you We’ve got a gentleman that runs that operation for us who use, I still need to introduce you to and your team, because I think y’all would be benefit to hear from him and what his capabilities are and how, you know, he can help you and some of your customers out with what he’s doing even enter Mexico, not not to mention the border. So we’re very bullish on Mexico, and the US and where that partnership is going to go from here. And so we are

Jeff Eizenberg 30:28

going both ways, right? You’ve got grains and other goods going into Mexico. And then as you’ve just described a little bit ago, how if there’s a chance for us to match the labor and quality, then if we move some of our texts will like, not us. But if some I’ve heard that China is buying up some textile factories and whatnot in Mexico, if they could replicate the work there, but just be closer to us that, then now you’re going the other way, right? You’re bringing it back in?

Woodson Dunavant 30:58

That’s exactly right. That’s exactly right. And, you know, it’s just it’s been a great venture for us. You know, the more and more we look at it, the more and more we like it, and the more bullish we are on it. So yeah, I’m very, very happy with where we’re going there, for sure.

Jeff Eizenberg 31:14

I was talking with a group today, and he was talking to me about Mexican ports, and how the terminals are hardly back over there, and only the largest vessels coming in. Is that been your experience as well, that these port contractors are very long and extensive? And just to break into that it would be difficult? And ultimately, I guess that would mean that there’s better chance for some of this rail and solutions? Yeah,

Woodson Dunavant 31:42

I mean, you know, I think in Mexico is a lot of people know, I mean, you’ve got to know the right people in order to get things done. And, you know, while while there might be longer contracts in place, I think that, you know, you can still get things done if you know, the right people there. Right. So, you know, I think that’s what the name of the game is there for sure.

Jeff Eizenberg 32:04

Is there other any other countries or regions that you’re focusing on other other than, than the Mexico opportunity? And obviously, you’re doing things in Asia? But yeah, I mean, you coming on? You

Woodson Dunavant 32:18

know, we’re, we’re pretty bullish on Vietnam, we’ve got a contingent going over there, I think in the next three weeks or so to go check things out, you know, they suffered from a lack of land and people, but, you know, they, everything that they’ve done is is very impressive. From a port infrastructure standpoint, from a manufacturing standpoint, from a labor standpoint. I mean, you’ve got invest foreign investment from all over the world going into Vietnam right now. And, you know, we’re, we’re quite bullish on on the goings on there, and so much, so I was, like I said, we’re sending sending three executives over there in the next few weeks to go to go investigate further and for sure, do you?

Jeff Eizenberg 33:05

Are you taking a translator? And are you on this? Are you on this contingent?

Woodson Dunavant 33:11

So luckily, we, you know, we don’t really need translators, we have agents and people that we work with, over there that are able to do that for us. So years and years and years ago, when we travel over there, you’d have to, you know, you’d have to have a translator, whether it was in China or Vietnam, or wherever, in Asia, you’re going nowadays, you know, with with as many agents in the network that we have, we’re able to go over there and get around and you know, to be completely honest, English will get you a lot further than you think, especially in Asia. It really will

Jeff Eizenberg 33:45

you heading on this trip, or you’re,

Woodson Dunavant 33:47

I’m not unfortunately, I wish I would I wish I was Vietnam was one of my top countries in the world that I’ve ever visited, both from a food standpoint, from a people standpoint, from a manufacturing. I love love Vietnam is awesome. Vietnam, Thailand and South Africa are the top three for me, for sure.

Jeff Eizenberg 34:10

Sounds good. So you know, this has been a it’s been a great conversation, what’s in it for you know, my takeaway from what you’re saying here is that we all need to think differently in the new environment moving forward, that it’s going to take strategic partnerships, it’s going to take innovation from different companies like yourselves, to come up with better solutions to move products and goods. And achieve really at the end of the day. Our goal of our company and the people with our clients we work with is to help them maximize their margins. And so it sounds like you’re very much aligned with that perspective.

Woodson Dunavant 34:48

Absolutely. Absolutely. If you get if you get if you’re comfortable in your supply chain right now, watch out because there’s a change coming and you know it like I said, we’re here to provide solutions when customers have problems, or they want to look outside the box, that’s, that’s who we are. And that’s what we want to help them do. And, you know, it’s a new normal that we’re in, you know, it may only last another three to six months, and then we could be hair on fire was something else. I mean, who knows? That will happen? Because, you know, I wish I could tell you that, you know, things will go back to the way they were. But as we all know, once you have a catastrophic, cataclysmic shift in supply chain, which we have had pre COVID to COVID to now. It’s a new way of doing business. And yeah, so it’s, it’s fascinating. The one thing that we didn’t touch on, was, I think you want to real quick on the rail issue.

Jeff Eizenberg 35:46

Oh, yeah, please. Yeah. What’s the story? Are they is it Congress is the only one that could solve this or what’s going on?

Woodson Dunavant 35:52

So they did they have originally they had said the 19th of November, they just extended it to December 4. And so they’re gonna have another couple three weeks negotiation, which I view is a very positive development. At the end of the day, Congress and or president are gonna have to step in, because if you were to have that happen, I mean, you talk about you think that the LA Long Beach strike was a big deal. You talked about stoking inflation. I mean, it would be tattered. Strophic, if we had a major rail, strike, I mean, you know, 40%, of, of all goods, in terms of weight is moving on the rail. And if you if you were to stop that, I mean, you can’t get from a food from a retail from you. I mean, you just goes on down the list. I mean, it would be I can’t imagine that the government would allow that to happen, though, they will step down at the 11th hour, if it gets to that point and put their foot down, they have to,

Jeff Eizenberg 36:57

yeah, I mean, everything with the just in time production that we have here and consumption in the United States, if even a day or two delay when we’ve seen with, you know, weather conditions or something backs things up, and it takes months for it to work through. So if you started if you had weeks or months off, oh, my goodness, you’re,

Woodson Dunavant 37:19

I mean, to your point, even even five days, like something like that would set us back by, you know, three or four months. I mean, it’d be crazy. So I do not think that that will happen. So you can come back and poke me when they do strike and then everything shifts.

Jeff Eizenberg 37:36

Instead, it was not gonna happen. Place your bets. Yeah. We get it. I appreciate that insight. Because then yeah, you’re at the pulse of it. I mean, I assume that the people in the rail industry don’t want it to happen either. But they also want to be paired paid fairly and get proper compensation. So

Woodson Dunavant 37:53

that’s right. That’s right. You can’t fault him for sure. Yeah,

Jeff Eizenberg 37:56

that’s exactly it. Well, no, this has been extremely good and extremely helpful beneficial to I think everyone listening and, you know, welcome, welcome. You obviously share it yourself. I always have one final fun question for everybody. And it’s what is your favorite extreme sport that you either participate in or would participate in if you maybe were back in your yet 20 year old buddy?

Woodson Dunavant 38:20

Oh, Lord and mercy, stream sport?

Jeff Eizenberg 38:25

I mean, you talk duck, honey, that’s kind of the kind of counts.

Woodson Dunavant 38:28

Okay, well, if that counts, then I will. You know, it’s an extreme sport, in some cases, for sure. Yeah. And I really enjoy it. So. Yeah, I mean, that would be that would be it for me. For sure. I was thinking more like MMA or boxing. Oh, yeah. Well, you could do that too. I mean, I really miss heavyweight boxing. And, you know, back in our day was was was when Tyson and Lewis but even before that, I mean, you know, we would block an entire night out, you know, to get ready for the boxing match. And I mean, it’s it feels like it’s gone. Like, MMA has just totally taken it over. But I mean, I feel like there’s still a space for good heavyweight boxing, and it just, it’s gone. It feels I just, I really miss that.

Jeff Eizenberg 39:15

Maybe Tyson was the pioneer of it, because when he bit Holyfield’s ear, nowadays, MMA if you’ve met somebody there, they might be like, yeah, that’s okay.

Woodson Dunavant 39:23

That’s right. That’s right. There’s no doubt there’s no doubt so

Jeff Eizenberg 39:26

pretty good. Oh, what’s the what’s the best way to get a hold of you have people had to want to want to connect?

Woodson Dunavant 39:33

Yeah. So reach out to me. My email address is very simple with some data of it. I’ve done have a.com Email me, you can give me a call. And happy to talk through anything with anybody importers, exporters, domestic domestic folks here in the US anything cross border. If I don’t know the answer, I’ll put you in touch with somebody here. That does. We’ve got we’ve got IT experts all over the place. Donovan, I’d be happy to put you in touch with whomever you need to talk to. So we’re, we’re really excited with our growth and where we’re going. And, you know, we’re just we’re in a we’re in a really good place right now. So, Jeff, I appreciate you doing this. I’ve enjoyed getting to know you over the past few weeks, and hopefully this won’t be the last time I talk to you.

Jeff Eizenberg 40:24

Yeah, we’ll do it again. We’ll check back in whenever fills back up. All right.

Woodson Dunavant 40:27

Sounds good, Jeff, appreciate it. So much

Jeff Eizenberg 40:29

Appreciate the time. Yep. Take care. Thank you.

This transcript was compiled automatically via Otter.AI and as such may include typos and errors the artificial intelligence did not pick up correctly.

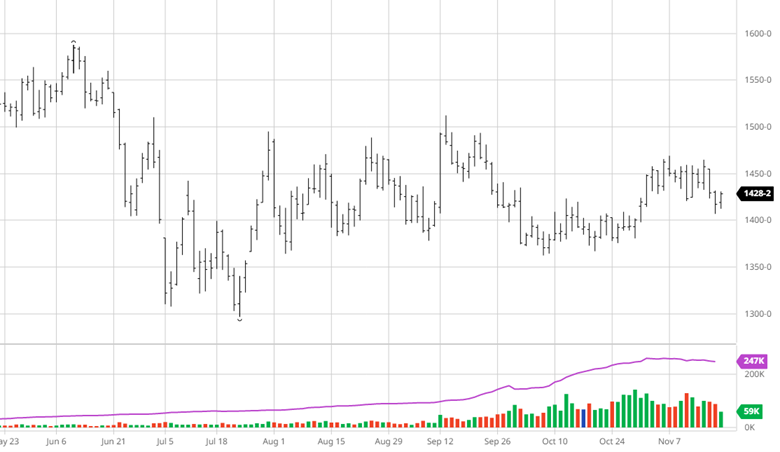

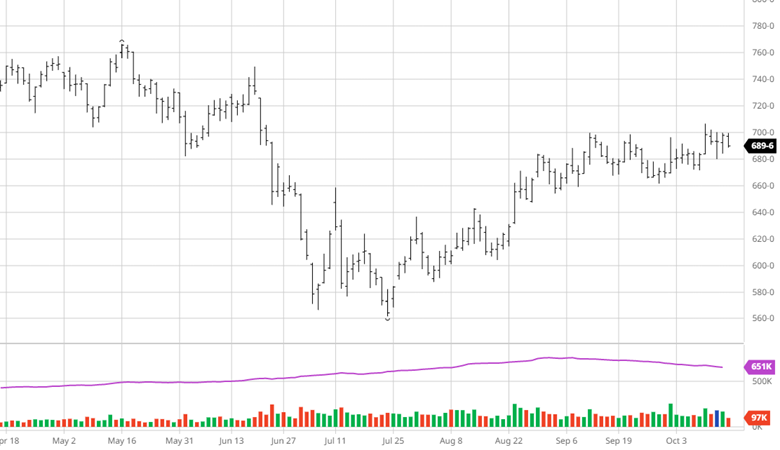

Corn had small losses on the week again as it has been range bound the last month. The market holding at this level certainly is not a bad thing when it traded $1 lower than current levels in July, it just needs a catalyst to push it one way or the other. The catalyst could be next week’s USDA Report as there could always be a surprise or two for the market. Many estimates see the USDA raising production from the October estimates, but by how much will be the question. Ultimately with US harvest coming to a close and South America ramping up, the global outlook and weather will begin to dominate the markets. The US will also need plenty of moisture over the coming weeks and winter to 1. Raise river levels to help grain exports and 2. Improve subsoil moisture heading into 2023. Exports remain underwhelming and will likely be lowered for the year in next week’s report.

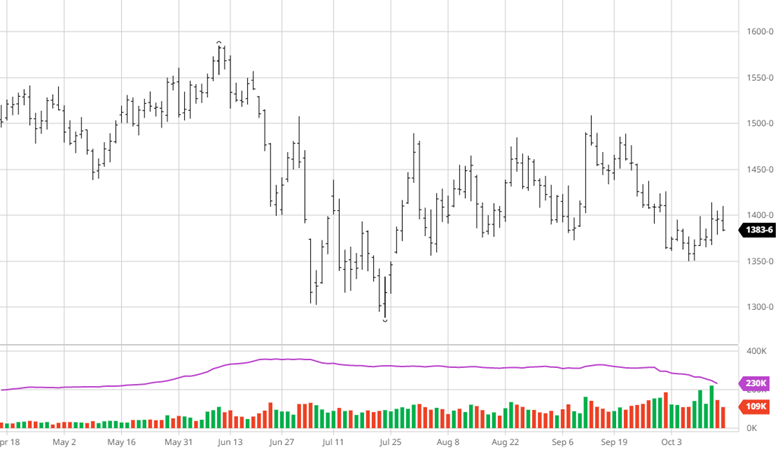

Unlike Corn, Beans have had a much wider range after an initial flat start to harvest have rallied back hard over the past 2 weeks. This move higher is welcome and appears to be heading toward a test of the highs from early September – can it break through? The USDA report will be the big news next week along with any news out of South America for weather and China potentially coming out of zero covid restrictions. Like corn, the USDA will likely raise US production next week and may lower exports. For any sustained move higher China will need to be a regular buyer and South American conditions would need to become less favorable.

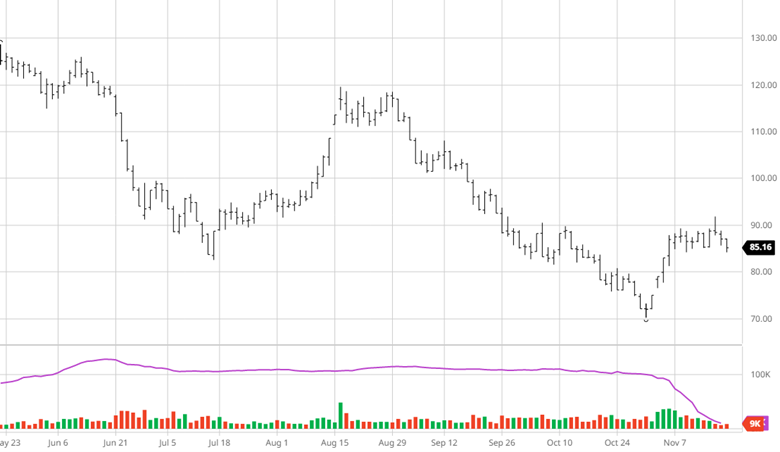

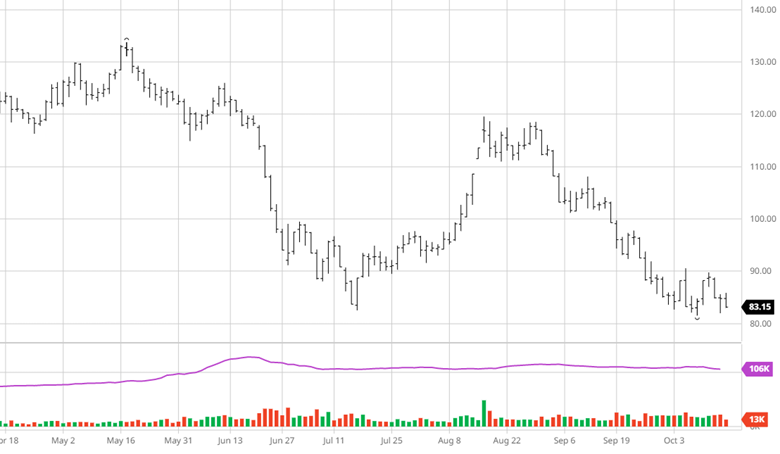

Cotton has had quite the week with 4 days that traded limit up at one point. With a lot of speculative positions in the market being short, this could be seen as a short covering rally as specs must exit their positions before expiration. On the physical side, the global cash market is a mess. Mills have massive inventories of both cotton and converted goods with no companies buying. The lack of buying by apparel companies shows their concern for the holiday season as inflation and market uncertainty will weigh on spending this year.

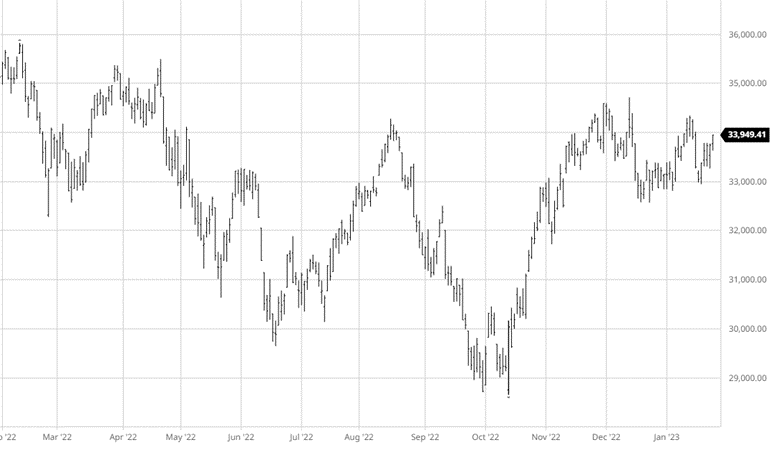

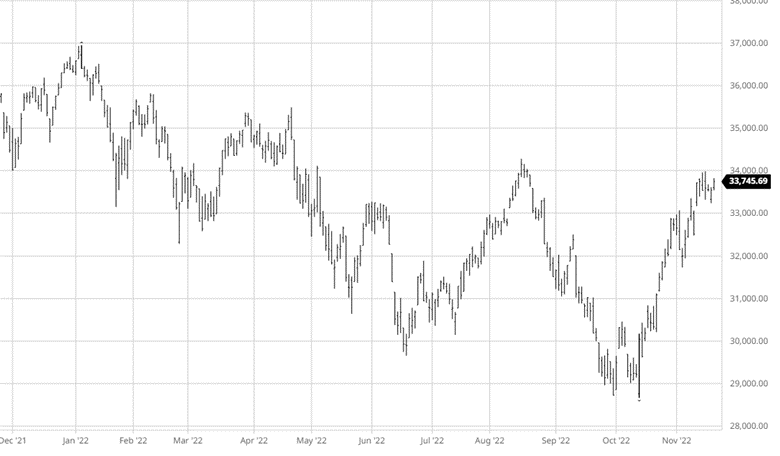

The equity markets have gained over the last 2 weeks; however, gains were muted after the Fed raised rates another 75 points earlier this week. This was expected but the comments by chair Powell after they came out were more hawkish than expected setting up an interesting point in next month’s meeting. Powell said the Fed is not likely to slow down yet setting up the potential for another 75 points in December, while analysts were leaning towards 50 before he spoke. The unemployment rate did tick higher in October while many companies also announced hiring freezes and grim outlooks for the first half of 2023. Crude oil spiked back above $90 a barrel on Friday continuing to bolster energy stocks. Midterm elections next week will also be closely watched as it may lay out what, if anything, will be done over the next 2 years.

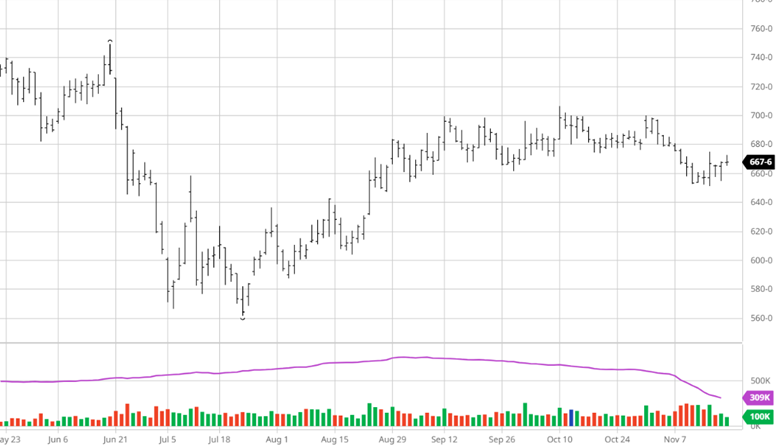

Are the Fed’s hikes starting to dampen inflation? Oil, grains, and metals have all fallen from their highs. But the rarely spoken of Cotton market was one of the first to crack…falling from 1.58/lb to 0.95/lb in just a few short days. We’re digging into this sharp drop and just why and how Cotton is involved in seemingly everything with RCM’s very own cotton king, LOGIC advisors Ron Lawson.

In this episode, Ron is giving us the low down on how and why he believes it’s not Dr. Copper which acts as the global economic barometer, but how Cotton is the real Canary and leading indicator on global demand. In between those talks, we’re covering all things Cotton including crop insurance, irrigated vs dry land, the scam that was Pima and Egyptian Cotton, the process of cotton – which countries have it, which want it, ginning it, spinning it, dyeing it, global commodity merchant co’s pushing it around, and even micro-plastics, climate change, and how Cotton always flows to the cheapest labor source. Finally, we’re walking in some high Cotton putting Ron in the hot seat. Will we ever get the growth back? Tune in to get these critical hot takes — SEND IT!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

The USDA report this week did not make any major changes to the US corn crop estimating a yield of 171.9 bushels per acres, down .6 bu/ac from September. The lack of surprises in the report kept corn trading along its path of late with no major losses or gains. The ending stocks were raised on lower demand with a high USD and world recession fears looming. While the balance sheets remain tight for corn but the recession fears lowering demand eases the balance sheet worries, for now. Harvest is still rolling along with much of the US experiencing drought conditions and no major rains in the forecast for many areas to slow it down much.

Beans were the surprise of the report with estimated yields falling to 49.8 bu/ac, down 0.7 bu/ac from the September report. US ending stocks were also cut with the yield lowering getting an appropriate reaction higher aster the report. The main concern for beans right now is low demand and the potential of a record Brazil bean crop. The strong USD weighs on bean exports with China being slow buyers, as we have said before to start feeling better about the direction of beans’ price, we need China to show up more often in larger quantities.

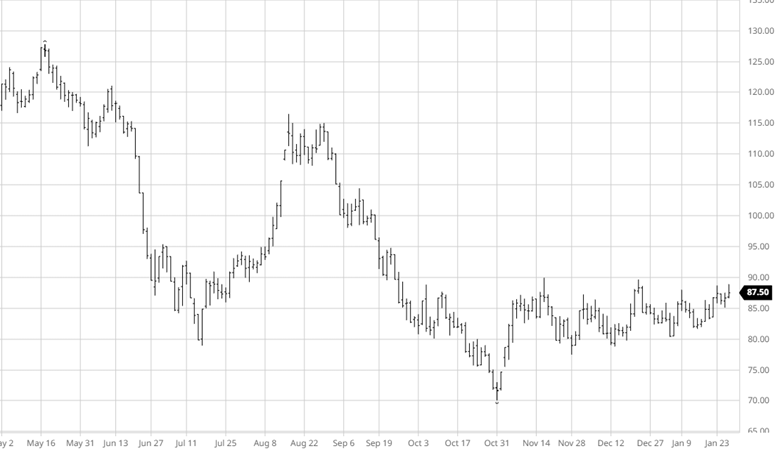

Cotton continued lower this week following the USDA report that saw a bearish reaction despite lower production estimates. Cotton is still fighting the supply vs demand issue to figure out where to go. Right now, the demand, or lack thereof, is winning as prices have been moving lower over the last 2 months. World recession fears impact the demand for cotton with lower demand balancing the lower production. The lack of demand makes it difficult to see a sizeable move higher in the near term but for cotton to be planted in areas that could grow corn and soybeans these price levels will not be attractive. We could potentially see a sideways trade until there is more certainty economically (demand) going forward.

The equity markets were positive this week due to a massive rally on Thursday to gain back the week’s losses and some. Inflation came in hot, again, this week giving the Fed the go ahead to raise rates another 75 basis points in November if they want to with a 15% chance of a 100 point raise. The market rallied on the CPI number, despite it being high, showing that there is still room for bounces in a bear market. It is hard to find much good news in the market with the proposed deal between the Biden administration and Rail workers unions falling apart this week as well, bringing the possibility of shutdowns back.

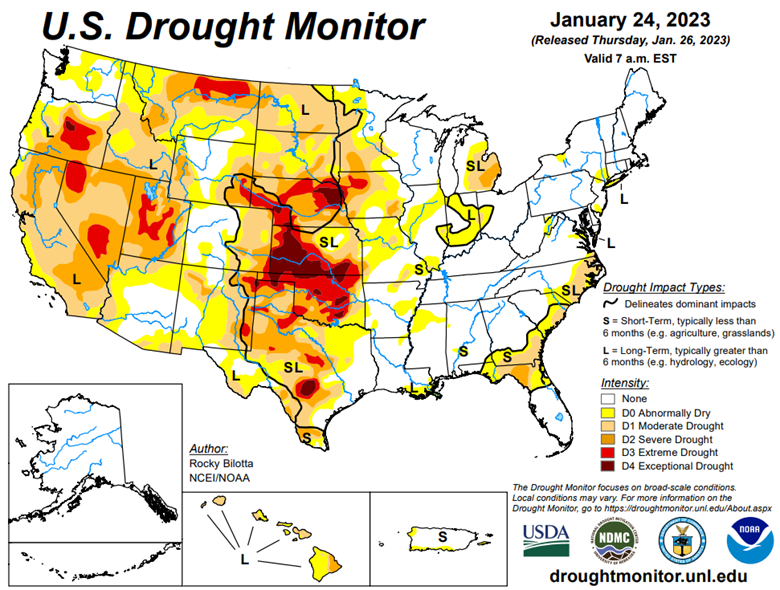

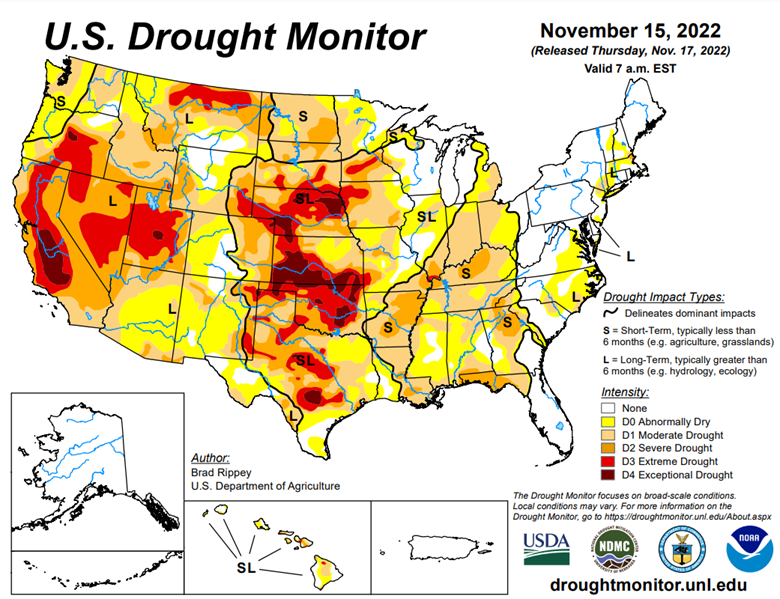

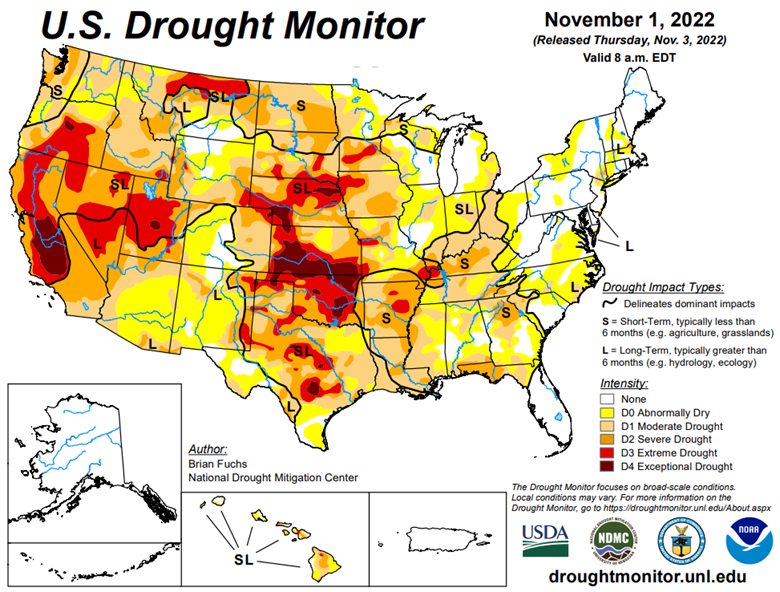

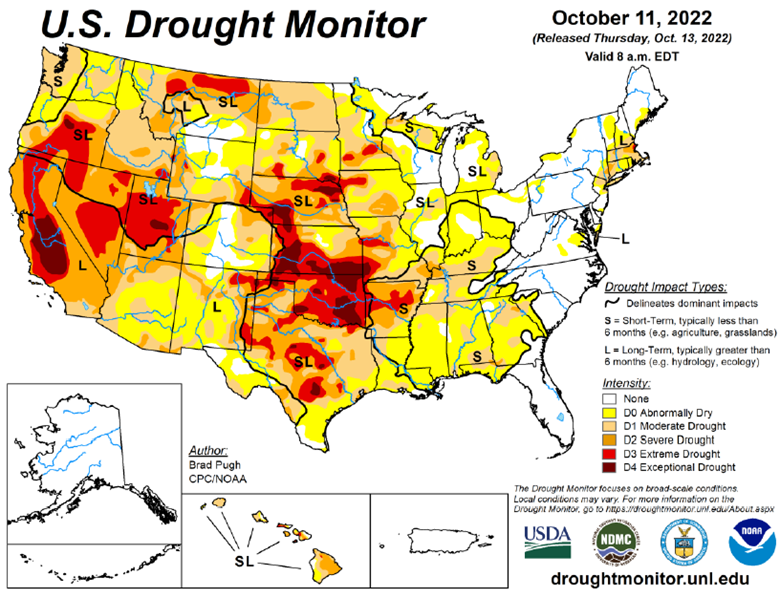

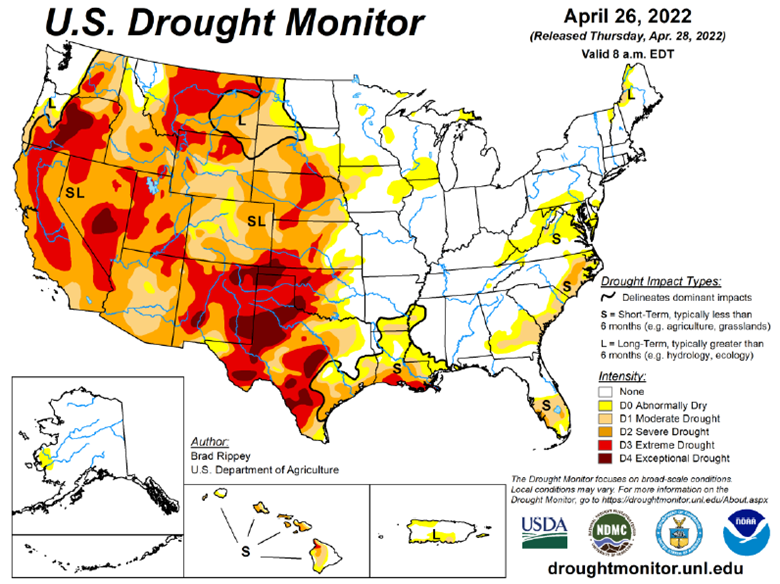

The drought monitor below shows where we stand week to week. As you can see much of the country is in drought conditions and will need moisture over the winter.

Podcast

Are the Fed’s hikes starting to dampen inflation? Oil, grains, and metals have all fallen from their highs. But the rarely spoken of Cotton market was one of the first to crack…falling from 1.58/lb to 0.95/lb in just a few short days. We’re digging into this sharp drop and just why and how Cotton is involved in seemingly everything with RCM’s very own cotton king, LOGIC advisors Ron Lawson.

In this episode, Ron is giving us the low down on how and why he believes it’s not Dr. Copper which acts as the global economic barometer, but how Cotton is the real Canary and leading indicator on global demand. In between those talks, we’re covering all things Cotton including crop insurance, irrigated vs dry land, the scam that was Pima and Egyptian Cotton, the process of cotton – which countries have it, which want it, ginning it, spinning it, dyeing it, global commodity merchant co’s pushing it around, and even micro-plastics, climate change, and how Cotton always flows to the cheapest labor source. Finally, we’re walking in some high Cotton putting Ron in the hot seat. Will we ever get the growth back? Tune in to get these critical hot takes — SEND IT!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

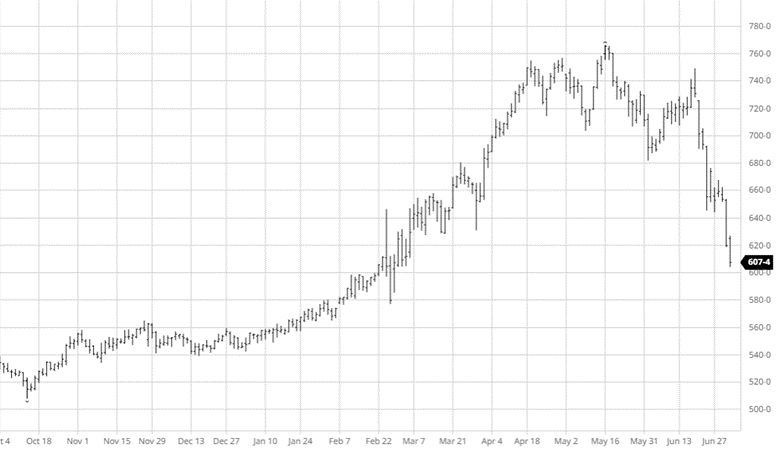

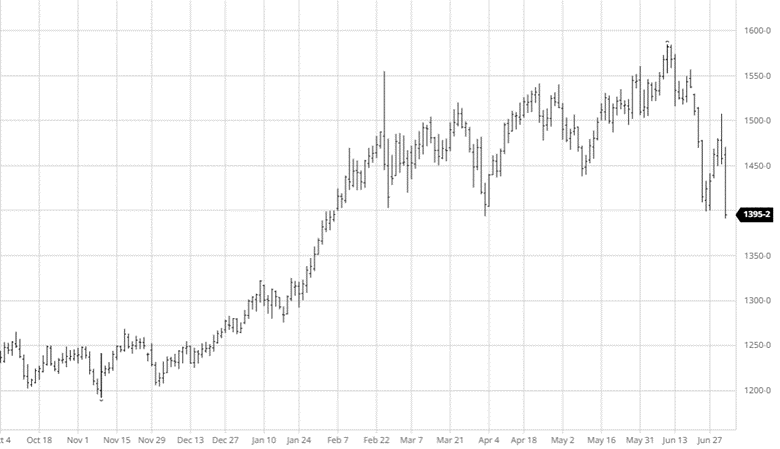

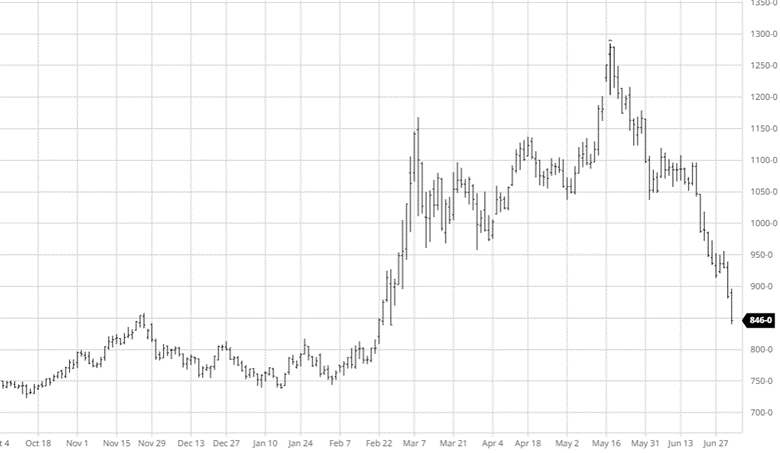

Corn had a volatile week suffering losses to drop back to levels it saw at the start of last week. The USDA report on Tuesday this week wiped out the gains from last week after a bearish report. Ending stocks came in higher than expectations, not by much, but enough to be bearish. The recession fears affect every market and corn is no different as ending stocks will grow as less ethanol is produced and other uses will lower. The weather is the bullish factor in the market right now with hot and dry conditions expected across much of the corn belt during pollination. The longer this weather outlook stays, the more bullish it will become as yields struggle. Russia says they have agreed to a safe export corridor for Ukrainian grain.

Soybeans took it on the chin post report just like corn. While the report numbers were not overly bearish the loss in crude oil and soy oil prices have weighed on beans lately. The weather issues for corn are not as big a concern for soybeans (yet) but will be something that could come up in the future. South American yields are still hard to get a full picture of with the USDA still differing from many estimates. China canceled a bean purchase on top of a poor export report for the week.

Cotton has continued its move lower despite widespread abandonment in west Texas. This comes from the expect of demand destruction with a potential worldwide recession ahead and producers sitting on plenty of supply. Prices could be even worse if the US was having a good growing season, but the demand destruction along with a very strong US dollar does not help cotton. With the loss of many hedgers in the market due to the loss of crop, specs will be the market mover, trading on technical indicators, not fundamentals, for the foreseeable future and will decide the direction with mills on the sidelines too.

The equity markets continue their game of “recession or not” with the up and down trade. Another hot CPI number of 9.1% came in this week, the market was expecting it to be in the high 8s so this was still a bad number. While commodity prices have come down other areas of the market remain painful. Earnings this week were disappointing for banks kicking a market that was down and needed some positive news. The market will continue this back-and-forth game until everyone decides we are in the clear or the recession is unavoidable.

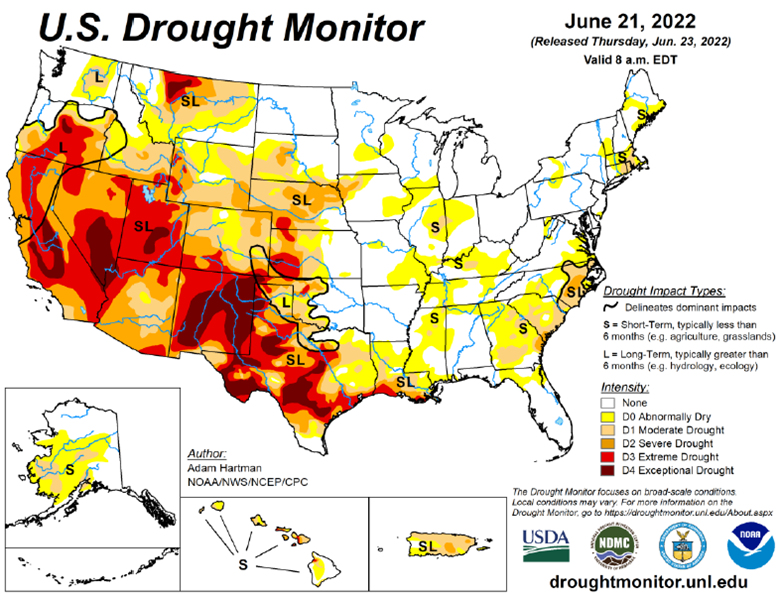

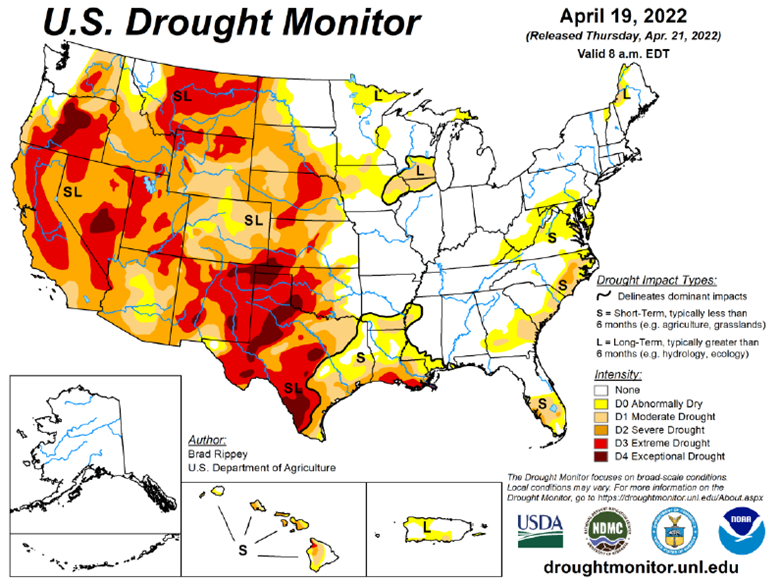

The drought monitor below shows where we stand week to week.

Podcast

There is an agriculture tug of war happening across the nation, impacting America’s farmland. Fertilizer prices are continuously fluctuating, and it has us taking a page the “The Clash” should we stay, or should we go?! And we aren’t the only ones. Many farmers are asking their agronomist and chemical salespeople, “what will fertilizer cost me the rest of the season, and what are my options if I don’t want to go all-in on my typical fertilizer treatment plan?”

In this episode of the Hedged Edge, we are joined by a special guest who needs no introduction in his local circle, Dick Stiltz. Dick is a 50-year veteran of the fertilizer and chemical industry and is the current Agronomy Marketing Manager of Procurement fertilizer and crop protection at Prairieland FS, Inc in Jacksonville, IL. He is at the pulse of the current struggle and here to discuss the topic at hand.

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Corn reacted negatively to the Stocks and Acreage report this week despite there not being any surprises and the numbers coming out close to pre-report estimates. Planted acres came in at 89.921 million acres (89.861 million estimate) and June 1 stocks were 4.346 billion bushels (4.343 billion estimate). The bearish news is improving weather after the 4th of July with rains expected across most of the corn belt. The concern over the wet spring causing prevent plant acres in ND and MN does not appear to have come to fruition with high prices motivating farmers to get the crop in the ground. Trading resumes Tuesday morning after the long weekend so any change in weather or world news could lead to a volatile opening after another kick in the teeth on Friday.

Soybeans had a good week making solid gains before dipping after the report and then getting crushed today (Friday). The bean planted acres was 88.325 million acres (90.446 million estimate) and June 1 stocks was 971 million bushels (965 estimate). The acres number was surprising as it came in 2.121 million acres below pre-report estimates. While the favorable weather for corn is also favorable to beans, they have a different story than corn to follow. Chinese demand needs to return to the market but 2+ million acres of production is a lot to be off by. The inability for Soybeans to break out higher following the report shows that they still have a fight ahead of them and that outside market risks likely have an impact on prices. Friday’s trade hit beans hard and the long weekend holds uncertainties.

Wheat moved lower on the week pre-report and continued lower after it with no surprises only to get crushed on Friday. All wheat planted acres were 47.092 million acres (47.017 million estimate) and 660 million bushels in June 1st stocks (655 million estimate). After a tough Friday, wheat has plenty of non US weather related news to follow and any developments over the 4th of July weekend will be seen on Tuesday.

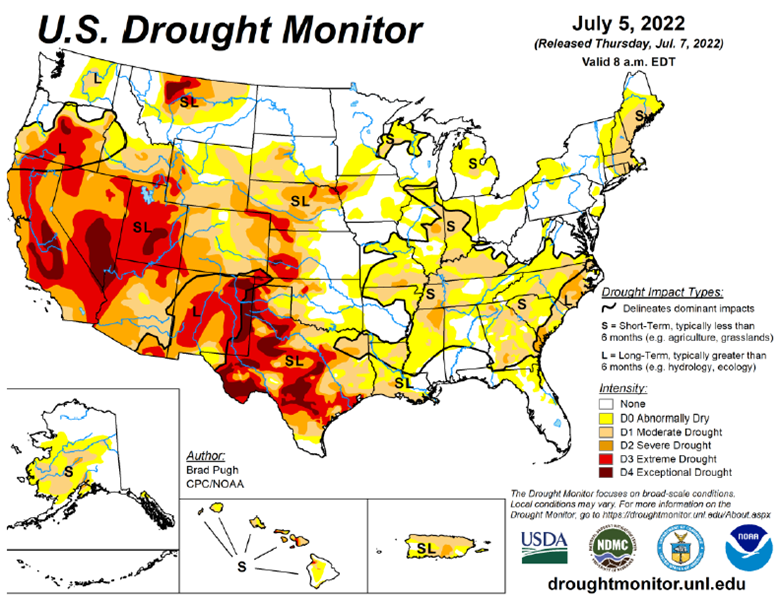

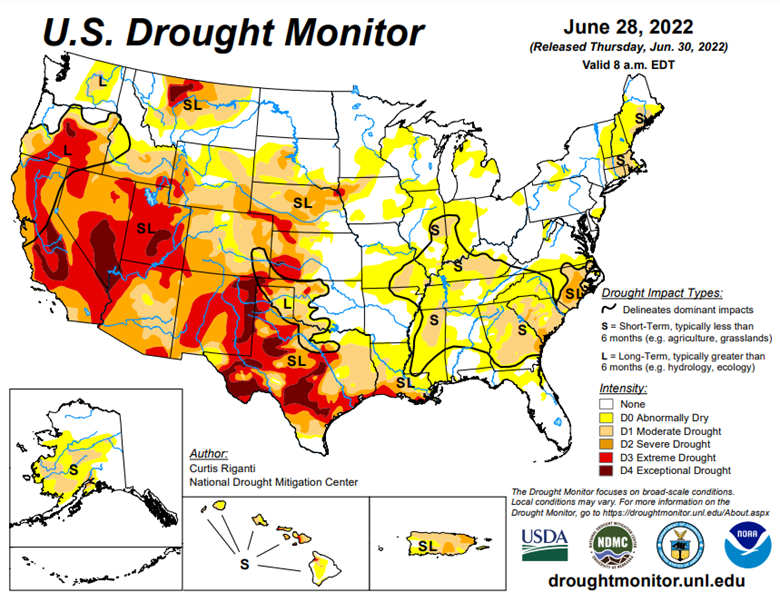

As you can see in the chart below cotton has had a rough 2 weeks. With demand expected to decrease with the possibility of a recession coming, this reaction is clear and puts fiber prices at the mercy of the economy’s future. The other side to this is that US production will likely be lower than expected with so much dryland in west Texas and other serious drought areas (see map below) expected to not produce a crop. Growers planted 12.5 million acres in 2022, up 11% from last year.

The equity markets were relatively flat on the week after a few up and down days. The market headlines keep being “market rallies as fear of recession lessens” or “market falls as recession fears remain” so the market is still looking for guidance as it continues lower. July’s news will be similar to June with inflation and the Fed being the main drivers.

The drought monitor below shows where we stand week to week.

Podcast

There is an agriculture tug of war happening across the nation, impacting America’s farmland. Fertilizer prices are continuously fluctuating, and it has us taking a page the “The Clash” should we stay, or should we go?! And we aren’t the only ones. Many farmers are asking their agronomist and chemical salespeople, “what will fertilizer cost me the rest of the season, and what are my options if I don’t want to go all-in on my typical fertilizer treatment plan?”

In this episode of the Hedged Edge, we are joined by a special guest who needs no introduction in his local circle, Dick Stiltz. Dick is a 50-year veteran of the fertilizer and chemical industry and is the current Agronomy Marketing Manager of Procurement fertilizer and crop protection at Prairieland FS, Inc in Jacksonville, IL. He is at the pulse of the current struggle and here to discuss the topic at hand.

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Corn continues to move higher as planting has gotten off to a slow start in the US and Brazil’s safrinha crop is facing drought conditions, shrinking their crop. The wet and cool forecasts remain into May for the north and eastern corn belt which will make it unlikely to see much planting progress in those areas. The rain will be welcome in the western corn belt that has been dry and making slow progress in planting, but the rain will be welcome for the soil even if it slows planting for a day or two. The ongoing conflict in Ukraine continues to decimate their infrastructure as Russia destroys ports and has seized stored corn to sell as their own. China was a buyer of corn this week and will hopefully continue to show up on exports as demand from other buyers has slowed. Limits have been increased at the CBOT for some commodities and corn will now have a 50 cent limit starting May 1 from the current 35 cent limit.

Soybeans had a small dip this week after its nice run higher from the previous dip at the end of March. Soyoil prices continue their move higher pulling beans with it while meal struggles. Indonesia placed a palm oil ban on both refined and unrefined product. The slow start to planting will ultimately roll into affecting soybeans like corn but we aren’t at panic mode yet. The start to the year has been less than ideal when the world stocks need a great year. Beans daily trading limit will move up to $1.15 effective May 1st.

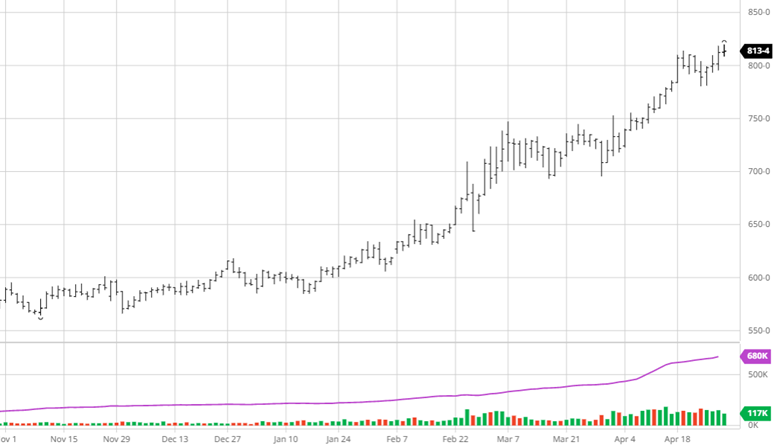

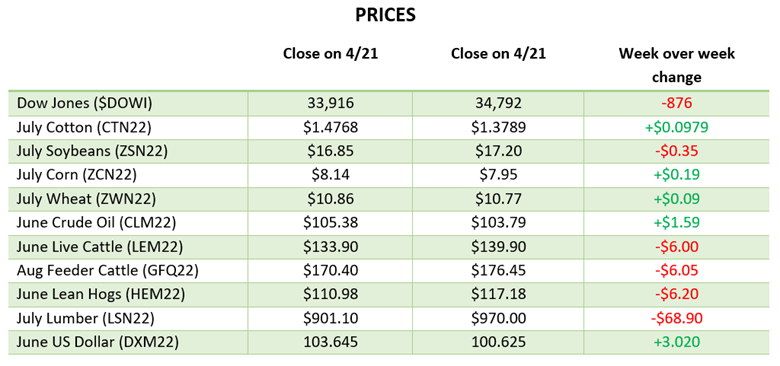

July cotton traded limit up (7 cents) on Thursday to set a new contract high at $1.4768. Export data from last week was better than the last few weeks. Cotton’s problem appears to be a lack of world supply mixed with (so far) not ideal growing conditions in Texas. Forecasts for rain in Texas are very welcome but will need to be widespread and a large amount to help the drought. (See drought map below)

Dow Jones

The Dow was down this week as volatility continues to be in the markets as earnings continue to come across with some large companies getting crushed and others posting solid numbers. Tech companies have had a good week after getting run over the past couple months. This may not be the bottom for tech but it is nice to see some good numbers and some support.

The drought monitor below shows where we stand week to week.

Podcast

RCM Ag Services put a unique spin on National Agriculture Day by going international. That’s right, we jumped right into international waters with Maria Dorsett from USDA’s Foreign Agriculture Services for an interesting discussion about linking U.S. agriculture to the rest of the world.

Each year, March 22 represents a special day to increase public awareness of the U.S.’s agricultural role in society, so why not take it one step further by bringing in a global component? As the world population soars, there’s an even greater demand for producing food, fiber, and renewable resources. That’s why we’re taking a deeper dive into the USDA’s trade finance programs, like the GSM-102, which supports sales of U.S. agricultural products in overseas markets and supports export growth in areas of the world that are seeing some of the fastest population growth.

So, jump aboard (no passport needed), as Maria discusses how U.S. companies use GSM-102, what the program features, and the benefits that it offers!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

RCM Ag Services is a registered DBA of Reliance Capital Markets II LLC. Trading futures, options on futures, and retail off-exchange foreign currency transactions are complex and involve substantial risk of loss and are not suitable for all investors. Loss-limiting strategies such as stop loss orders may not be effective because market conditions or technological issues may make it impossible to execute such orders. Likewise, strategies using combinations of options and/or futures positions such as “spread” or “straddle” trades may be just as risky as simple long and short positions. There are no guarantees of profit. You should carefully consider whether trading is suitable for you in light of your circumstances, knowledge and financial resources. You may lose all or more than your initial investment. You should not rely on any of the information herein as a substitute for the exercise of your own skill and judgment in making such a decision on the appropriateness of such investments. Opinions, market data and recommendations are subject to change without notice. Reliance Capital Markets II LLC shall not be held responsible for any actions taken based on this website or attached links. Parties acting on this electronic communication are responsible for their own actions. Past performance is not necessarily indicative of future results.