Recap:

The futures trade was dominated by the roll last week. That said, it made a new contract low and then rallied. We saw that pattern a week earlier—and frankly, we’ve seen some version of it for nearly two years now. Rallies continue to lack momentum, fail quickly, and ultimately find themselves testing new lows.

A technician put it best last week: these trends are neither bullish nor bearish—they’re bullshit. There’s no trend, no follow‑through, and no conviction.

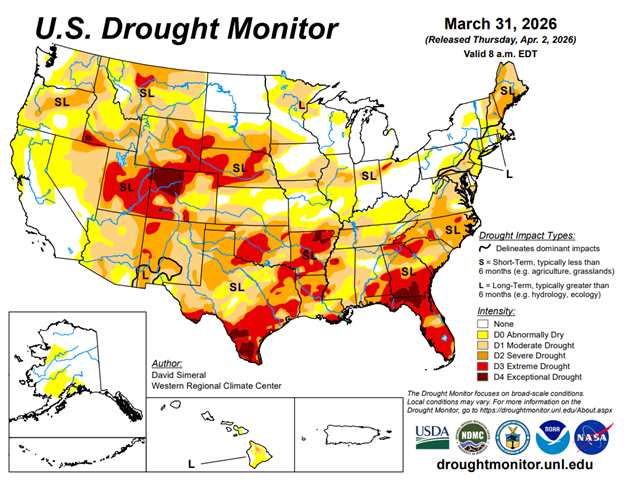

The broader economic backdrop for housing remains decisively neutral, and neutral markets have a nasty habit of killing their own rallies without outside help. That’s exactly where we sit today.

So, let’s look at a few housing headlines for more color.

Housing Headlines

• Existing home sales remain sluggish.

March existing‑home sales fell 3.6% month‑over‑month to an annualized pace just under 4.0 million units, the weakest March pace since 2009. Sales declined in all four regions, underscoring just how little organic momentum exists in the market. [markets.bu…nsider.com]

Existing home sales are projected to stay in line with 23-24 and 25. Without a rate cut expect slow sales and low inventories.

The macro effect:

“This has caused multifamily executives to lower their expectations for total 2026 multifamily sales volume and starts.”

• First‑time buyers are effectively sidelined.

First‑time buyers accounted for only 21% of transactions, a record low and well under the historical norm near 40%. The market is increasingly split between equity‑rich owners and would‑be entrants who simply can’t make the math work. [crosscount…rtgage.com] Can’t make it work…. nice.

From NAR, first time home buyers fell to a record low. They made up only 21%. That group was always in the high 30 percentile.

• Inventory is improving—but not enough to matter .

Active listings are rising year over year, and months’ supply has crept above four months, technically closer to “balanced.” But inventory is still well below pre‑pandemic norms, offering just enough supply to cap prices—not enough to stimulate volume. [mortgagetech.ice.com]

• Prices refuse to break—only flatten.

Despite weaker sales, median prices continue to grind higher on a year‑over‑year basis, driven by limited supply and locked‑in owners. Zillow expects roughly flat price appreciation in 2026, reinforcing the idea of a capped, sideways market rather than a corrective one. [zillow.com]

Builders I work with are staying on course and keeping production at the planned 2026 amount. “Head down and grind ahead” seemed to be the common theme.

• Mortgage rates remain a headwind, not a catalyst.

Rates dipped briefly below 6% earlier this year, but volatility tied to macro uncertainty pushed them back toward the mid‑6% range. That swing was enough to choke off affordability gains but not enough to force capitulation selling. [cnbc.com]

To sum it up:

There’s nothing here that argues for sustained upside—and nothing ugly enough to force a structural reset. Housing is stuck in neutral, and lumber reflects that reality perfectly. Rallies fail because they’re supposed to. Weakness finds buyers because costs, supply, and discounts still matter.

Until affordability actually improves or demand meaningfully breaks—this remains a market that chops itself to death, one failed rally at a time. It bothers me every time we use the affordability excuse. The is more fundamental issues involved.

Technical:

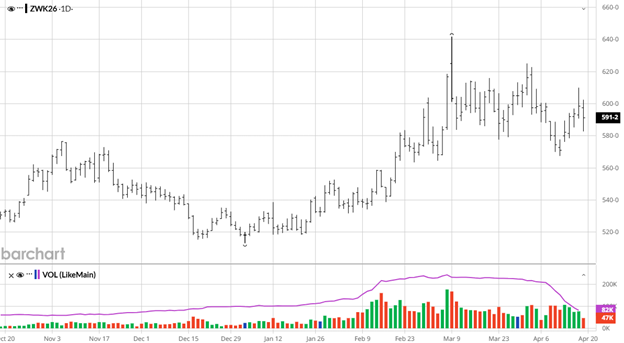

The May contract has found support in the $570 area. The fact that there are EFP’s available this time has brought the buyers back to the futures market at a price. This hand to mouth environment tends to magnify deals. Today it is in futures.

The starts projection is for 1.38. Permits are 1.39.

The weekly wedge pattern keeps getting tighter. The breakout looks to be a few weeks from now. May expiration could be interesting.

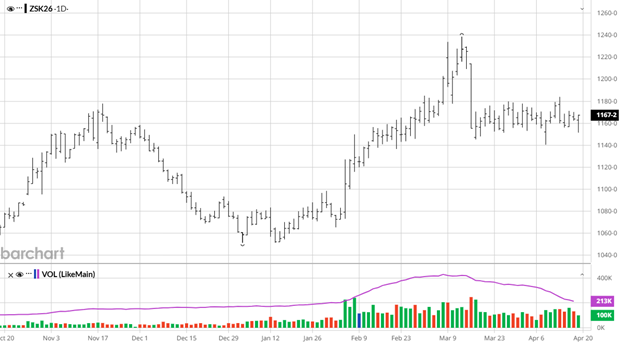

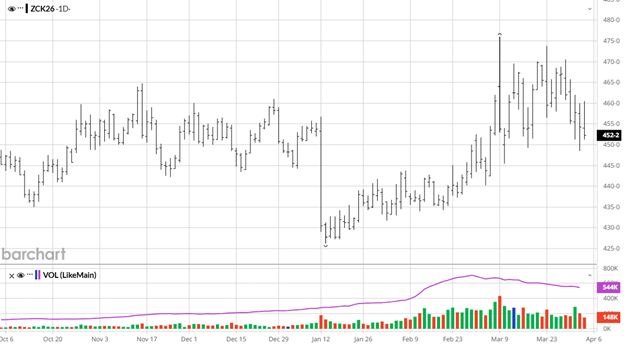

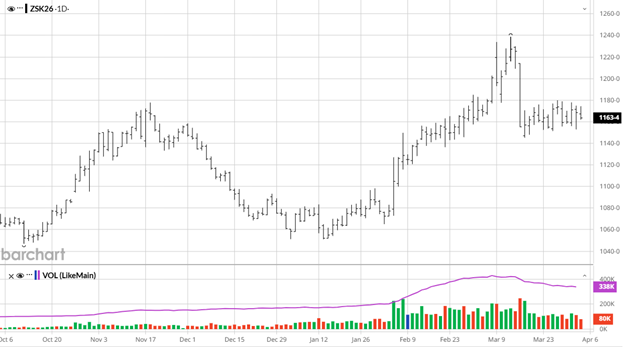

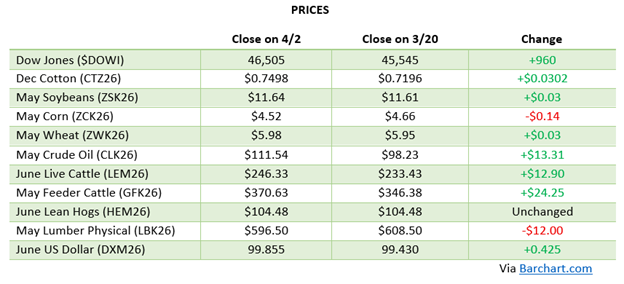

Soybeans have largely remained in a sideways grind, trading between $11.50 and $11.83 on July futures for most of the last 2 weeks. The April WASDE showed U.S. ending stocks unchanged at 350 million bushels with adjustments netting to zero, crush estimates raised while exports were trimmed by the same amount. The season-average price forecast was nudged 10 cents higher to $10.30 per bushel. Brazil’s CONAB raised its 2025/26 soybean production estimate again, this time to 6.582 billion bushels, keeping the global supply backdrop heavy and capping any sustained rallies. On the positive side, strong domestic crush margins, board crush pushing above $3 per bushel, have been the primary support story for the complex. NOPA March crush is expected to come in well above year-ago levels when reported. U.S. planting progress debuted at 6% complete as of April 13th, ahead of the 2% five-year average, with Mississippi and Tennessee leading at 39% and 36%, respectively. The market is waiting for a significant new headline to break out of the current range. Talks between President Trump and China’s President Xi, which were delayed amid the Iran conflict, remain a key watch item as any resumption of Chinese buying interest could quickly change the demand narrative for U.S. soybeans.

Soybeans have largely remained in a sideways grind, trading between $11.50 and $11.83 on July futures for most of the last 2 weeks. The April WASDE showed U.S. ending stocks unchanged at 350 million bushels with adjustments netting to zero, crush estimates raised while exports were trimmed by the same amount. The season-average price forecast was nudged 10 cents higher to $10.30 per bushel. Brazil’s CONAB raised its 2025/26 soybean production estimate again, this time to 6.582 billion bushels, keeping the global supply backdrop heavy and capping any sustained rallies. On the positive side, strong domestic crush margins, board crush pushing above $3 per bushel, have been the primary support story for the complex. NOPA March crush is expected to come in well above year-ago levels when reported. U.S. planting progress debuted at 6% complete as of April 13th, ahead of the 2% five-year average, with Mississippi and Tennessee leading at 39% and 36%, respectively. The market is waiting for a significant new headline to break out of the current range. Talks between President Trump and China’s President Xi, which were delayed amid the Iran conflict, remain a key watch item as any resumption of Chinese buying interest could quickly change the demand narrative for U.S. soybeans.