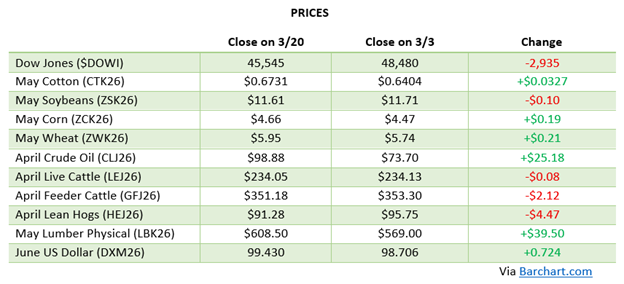

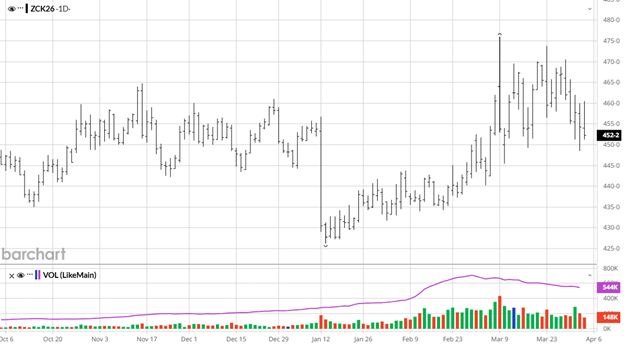

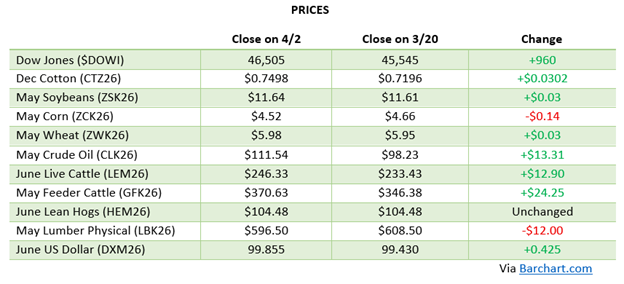

Corn has remained supported but volatile following the March 31st USDA Prospective Plantings and Quarterly Stocks reports, which reinforced a tighter-than-expected balance sheet narrative. The USDA came out with 95.338 million acres, near the lower end of trade expectations, confirming earlier concerns that higher input costs, particularly fertilizer due to war in Iran, would limit corn expansion, while stocks data did not show burdensome supplies. This has helped underpin prices despite sluggish export demand and limited Chinese participation, keeping the market more focused on supply risk than demand weakness. Combined with continued strength in energy markets and inflation-driven fund interest, corn remains in a supportive environment, though the large speculative long position leaves it vulnerable to sharp downside if macro sentiment shifts.

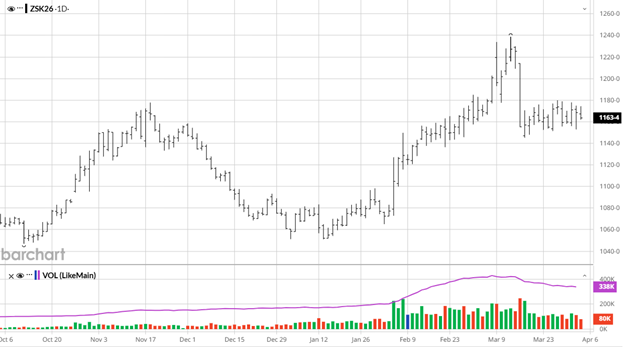

Soybeans have struggled to find sustained strength even after the March 31st USDA reports, which confirmed expectations for increased U.S. acreage and relatively comfortable stocks levels. The larger planting outlook reinforces the idea of ample new crop supplies, especially when paired with ongoing pressure from South America’s record production. While periodic rallies have been driven by energy market spillover and inflation concerns, the lack of consistent export demand, particularly from China, and fading optimism around biofuel policy have kept the market defensive. Overall, the USDA data solidified a more bearish supply outlook, leaving soybeans reliant on external market strength rather than supportive fundamentals. Talks between president Trump and China’s president Xi will be watched under a microscope if they end up happening after already being delayed with the conflict in Iran continuing.

Soybeans have struggled to find sustained strength even after the March 31st USDA reports, which confirmed expectations for increased U.S. acreage and relatively comfortable stocks levels. The larger planting outlook reinforces the idea of ample new crop supplies, especially when paired with ongoing pressure from South America’s record production. While periodic rallies have been driven by energy market spillover and inflation concerns, the lack of consistent export demand, particularly from China, and fading optimism around biofuel policy have kept the market defensive. Overall, the USDA data solidified a more bearish supply outlook, leaving soybeans reliant on external market strength rather than supportive fundamentals. Talks between president Trump and China’s president Xi will be watched under a microscope if they end up happening after already being delayed with the conflict in Iran continuing.

Energy Markets

Energy markets have continued to dominate the macro landscape, with crude oil holding elevated and volatile levels as geopolitical tensions involving Iran persist and uncertainty around the Strait of Hormuz remains unresolved. The sustained strength in energy has amplified inflation concerns globally, driving investment flows into commodities and influencing planting decisions, input costs, and overall sentiment across agricultural markets.

Equity Markets

Equity markets have remained under pressure since late March, as the combination of higher energy prices and the inflationary implications highlighted in recent economic data have weighed heavily on investor sentiment. The indexes continues to reflect a risk-off environment, with concerns centered on slowing economic growth, tighter margins from rising input costs, and ongoing geopolitical uncertainty overshadowing otherwise stable underlying economic conditions.

Other News

– Cotton acres in the prospective plantings report were 9.64 million for 2026, a 4% increase from last year.

– All wheat acres from the report were 43.8 million acres, down 3% from 2025.

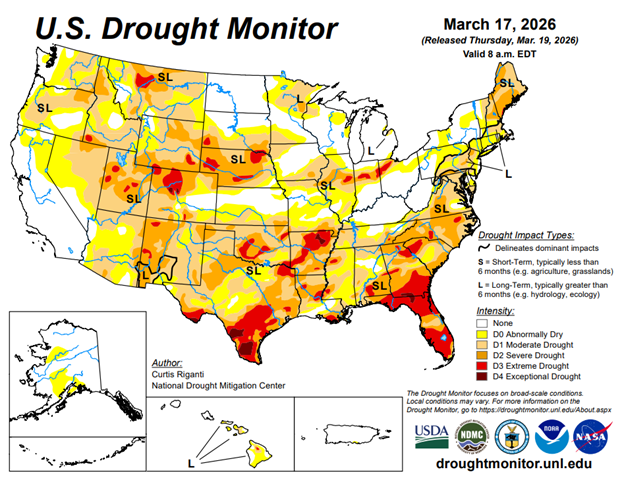

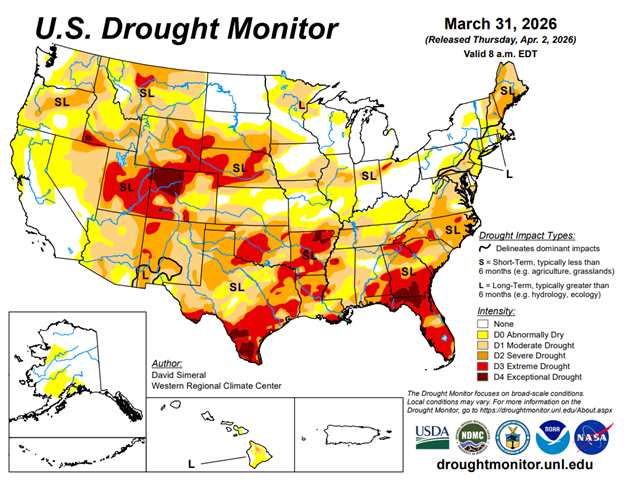

Drought Monitor

Here is the most recent drought monitor. With planting starting later this spring, we need rain in a lot of places in March.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.