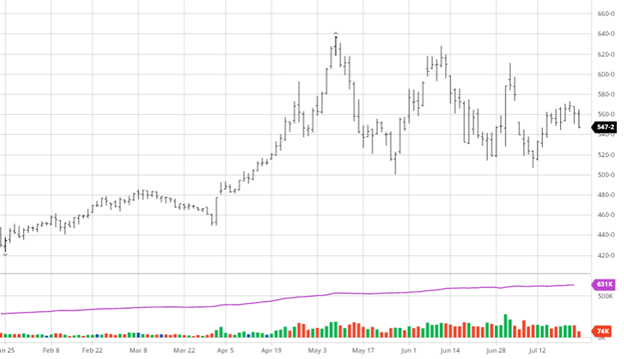

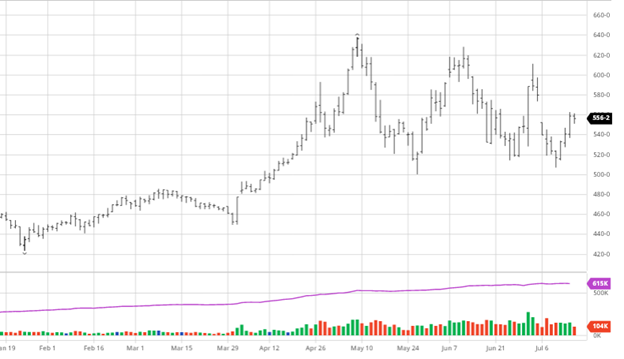

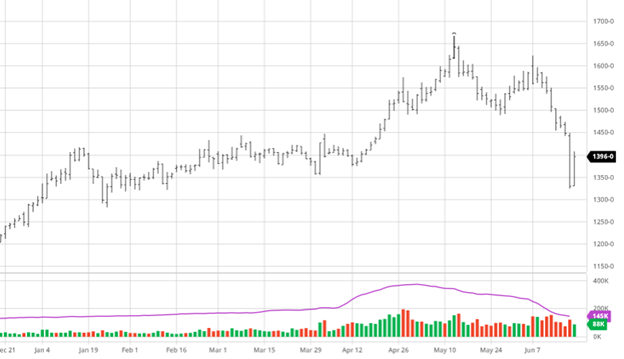

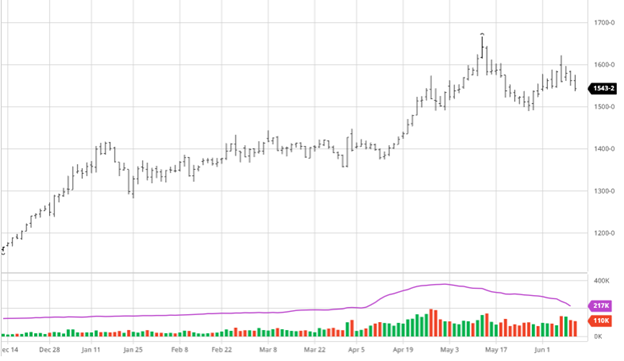

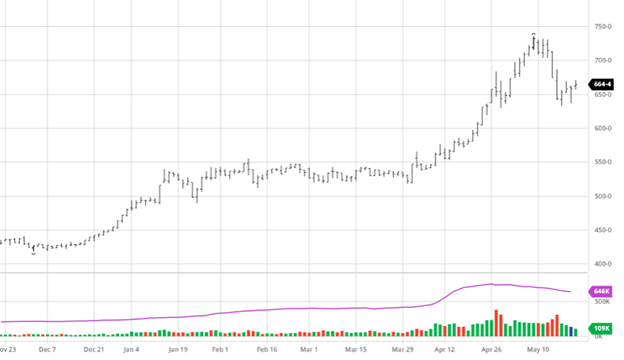

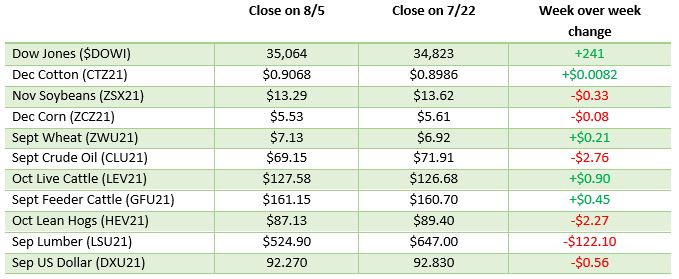

Corn lost over the last 2 weeks, but as you can see below the range has been much tighter than in the last 3 months. Next week’s reports will be the best chance to trade out of this range, whether it is higher or lower is the billion dollar question. Many private firms have come out with estimates recently ranging from the USDA’s number of 179.5 to the mid 170s. Anything lower than 178 would help the price of corn, along with the continued demand rebound and a smaller Brazil crop tightening world supply. CONAB will update the expected yield for Brazil on the 10th of August (next week) kicking off a week of important reports. Brazil is expected to continue to get smaller BUT will the USDA adjust their world ending stocks appropriately in the report on the 12th? Currently the USDA has Brazil’s production pegged at 300-320 million bushels higher than CONAB so a correction would seem to be coming this week.

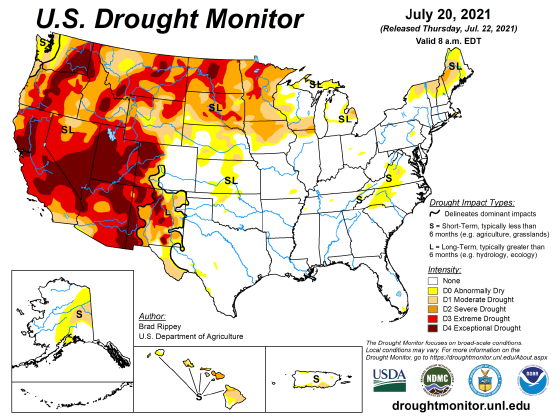

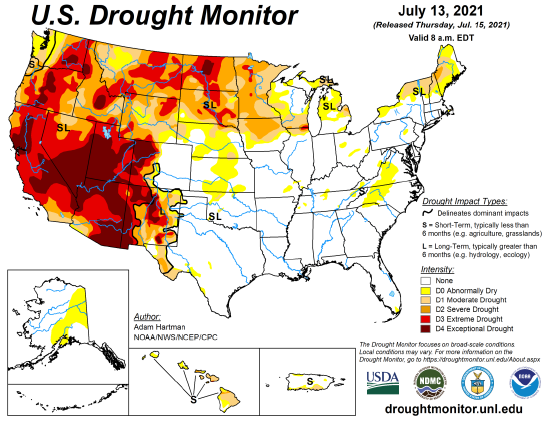

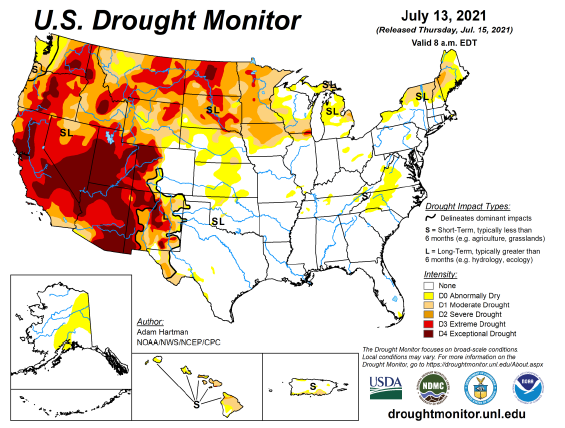

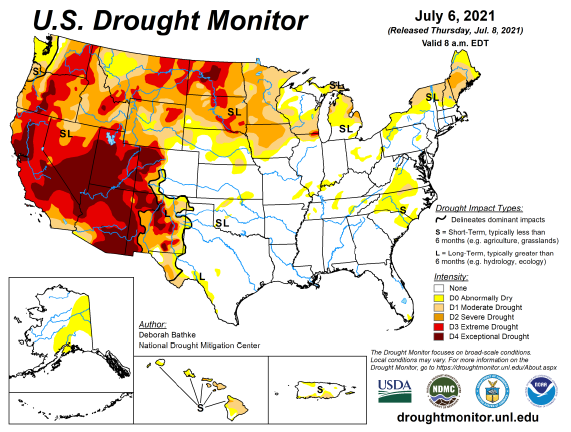

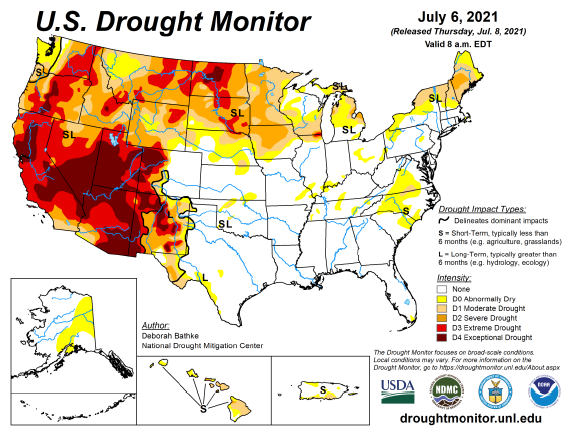

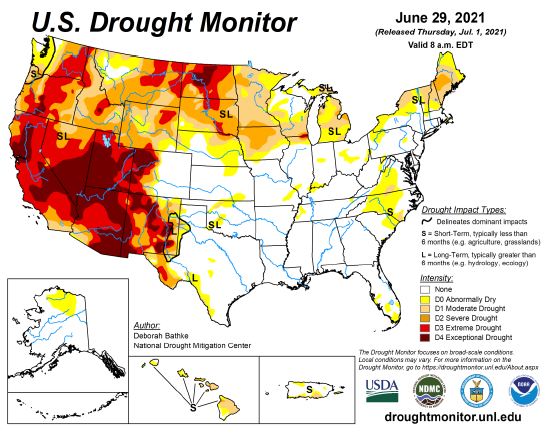

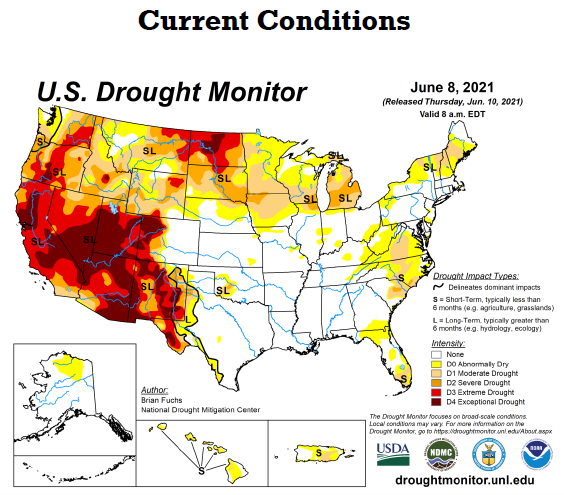

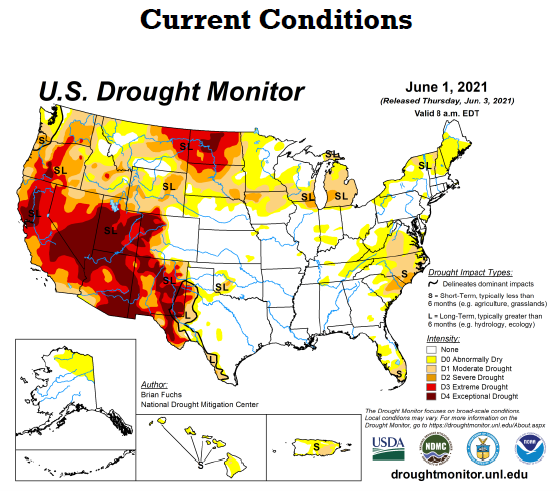

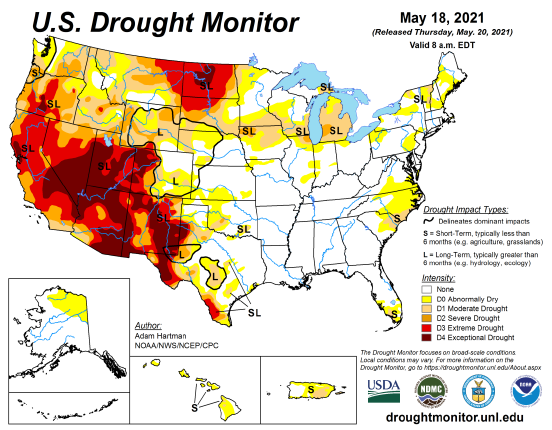

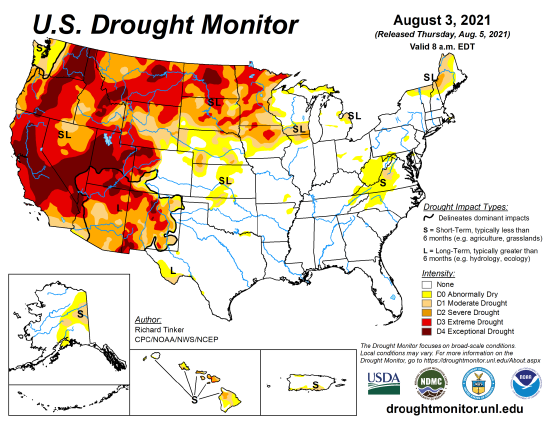

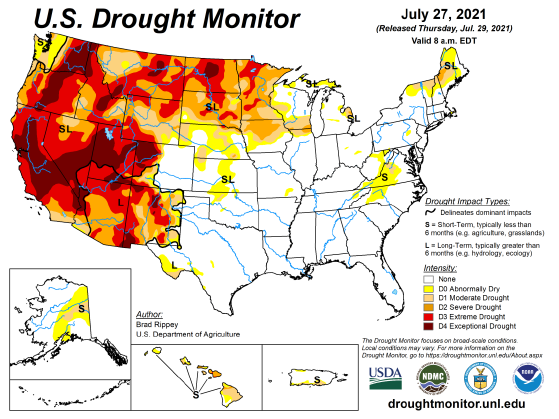

As you can see in the drought monitors at the bottom many areas are still suffering from a lack of rain and recent heat did not help the situation. Heat is expected to return by the middle of the month after this small break so rain continues to be welcome across the corn belt. Exports were better than expected this week; however not that large numbers that were expected.

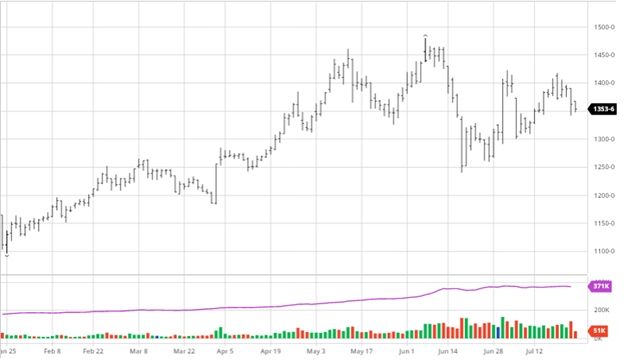

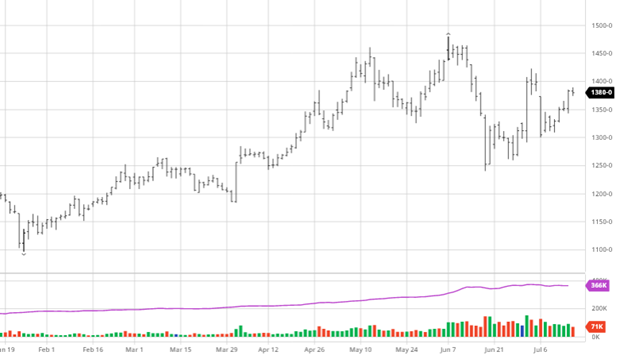

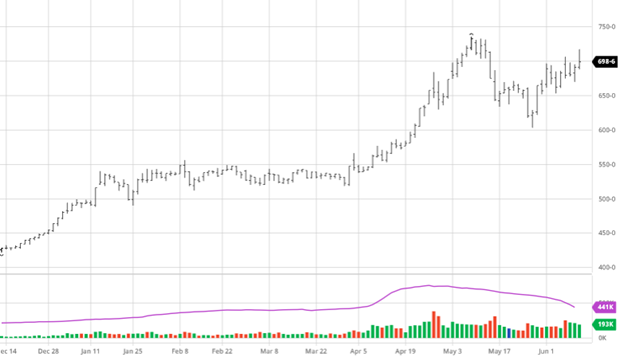

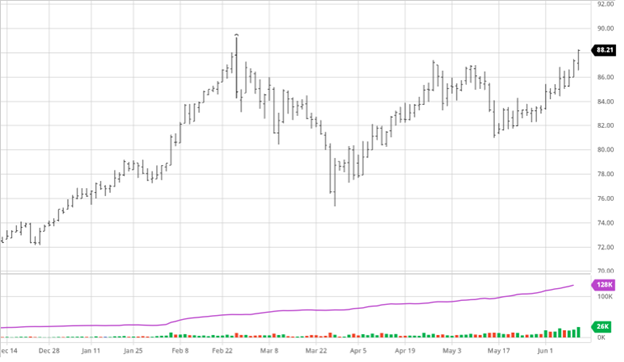

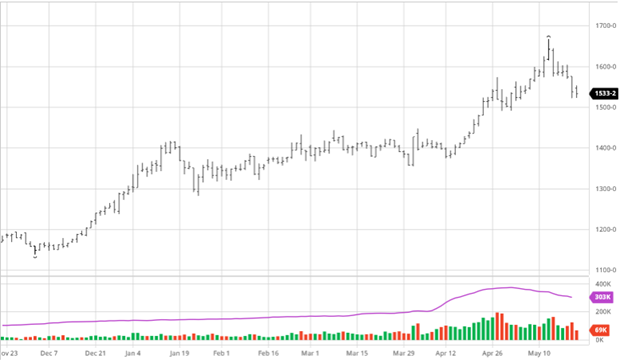

Soybeans had a rough week as bean conditions continue to be strong with solid expected yields. Beans have a more bearish feel right now with weather not playing a major factor one way or another. The demand has not ramped up like it did this time last year in the export markets = the bulls need to see that level of demand return to spark additional buying. The USDA’s report next week, like corn, should give us an important update on the expected demand. Current yield estimates are all above 50 bushels an acre with several over 51 bushels. Oil and meal markets have experienced weakness recently as well attributing to soybeans continued decline.

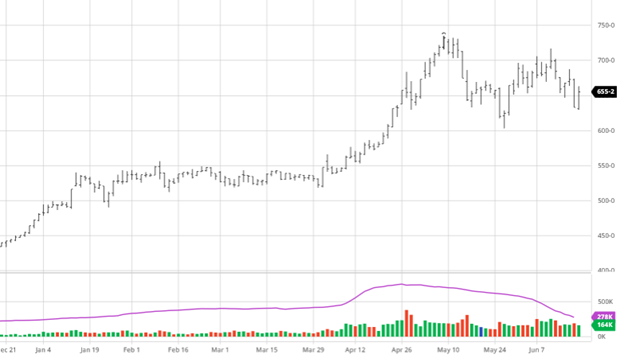

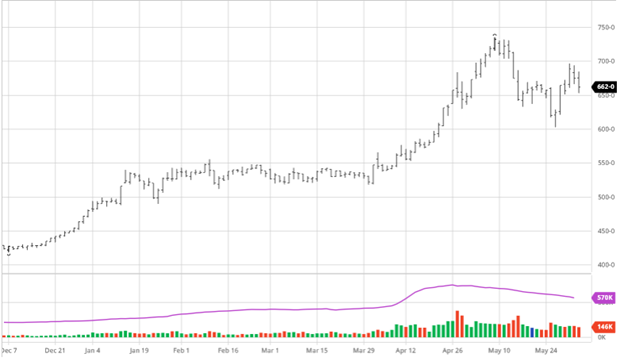

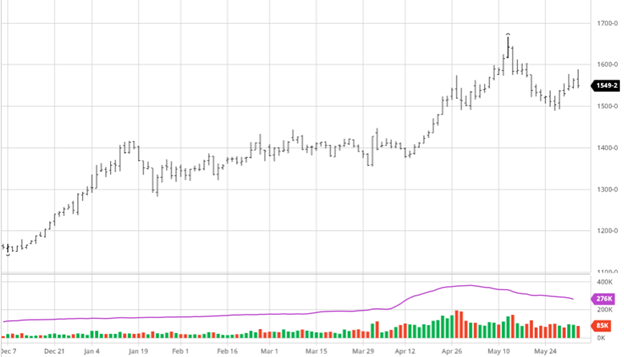

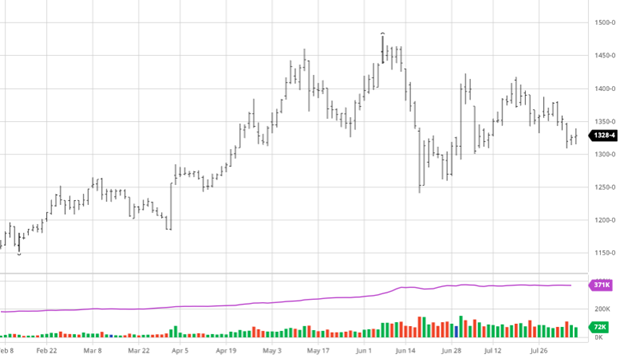

Dow Jones

Despite worries about the Delta Variant, the Dow gained over the last couple weeks and finally broke out to new all-time highs today (Friday, August 6th) as companies continue to beat earnings across the board. Some states/cities have begun readopting mask mandates in hopes to slow the spread while vaccine rollouts continue.

Podcast

Check out our recent podcast where we’ve brought on one of our real-life firefighters from RCM Ag – Jody Lawrence along with Tim Andriesen from the CME Group to provide us with some inside baseball knowledge of the current state of the agriculture markets and to discuss the real-world application of the use of short-dated options to potentially fight the current blaze of volatility surrounding agriculture markets.

https://rcmagservices.com/the-hedged-edge/

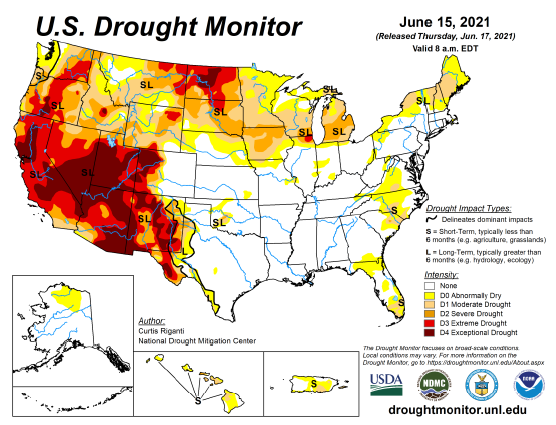

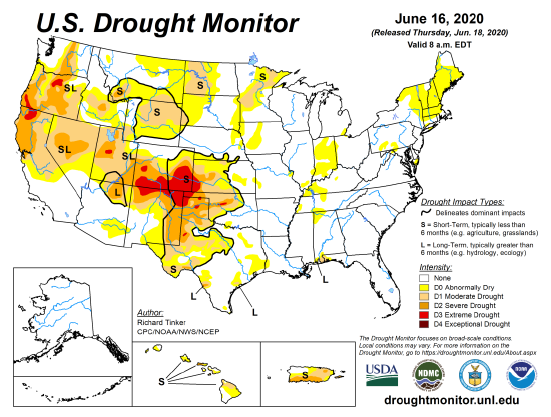

US Drought Monitor

The maps below show the continued drought conditions in the northern Midwest that reaches into the Canadian planes.

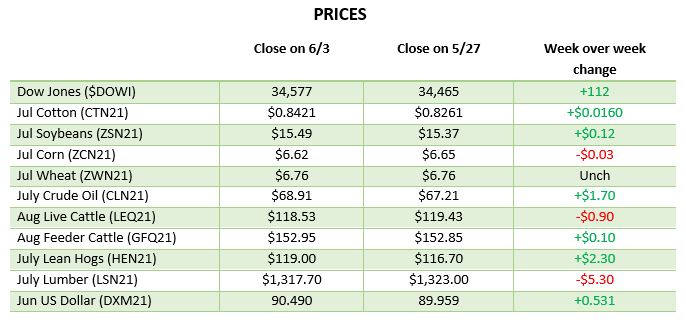

PRICES

Via Barchart.com