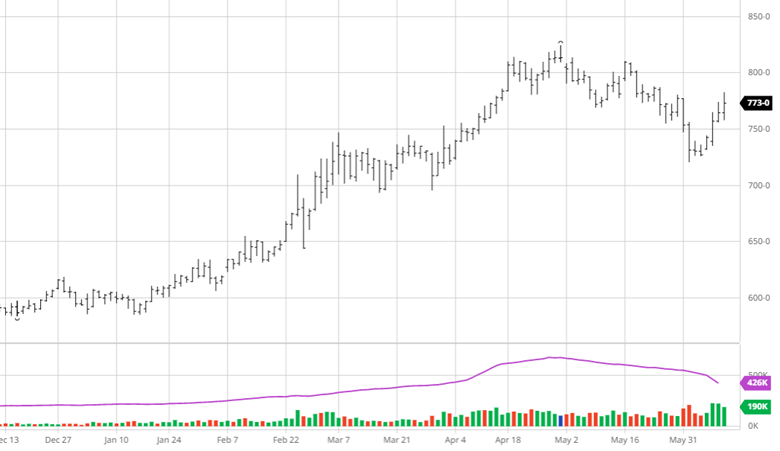

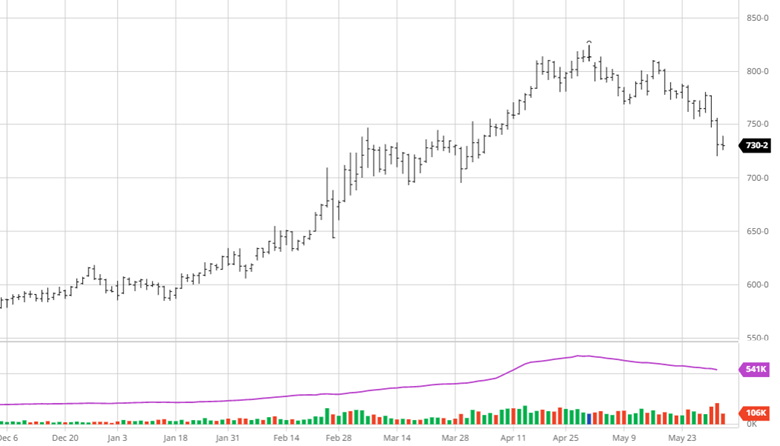

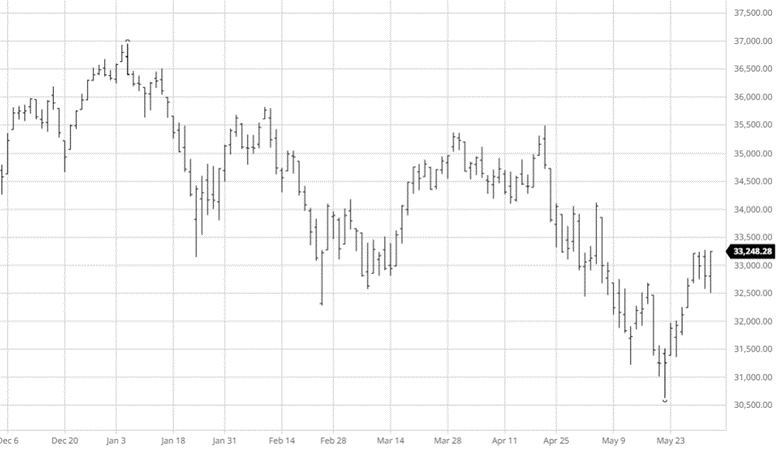

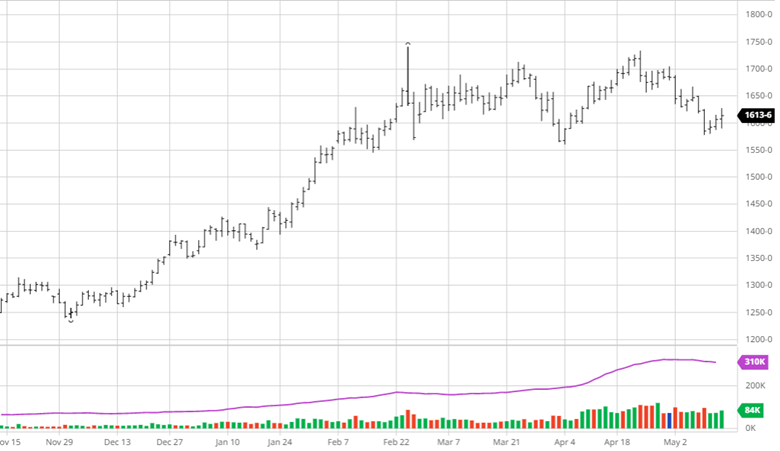

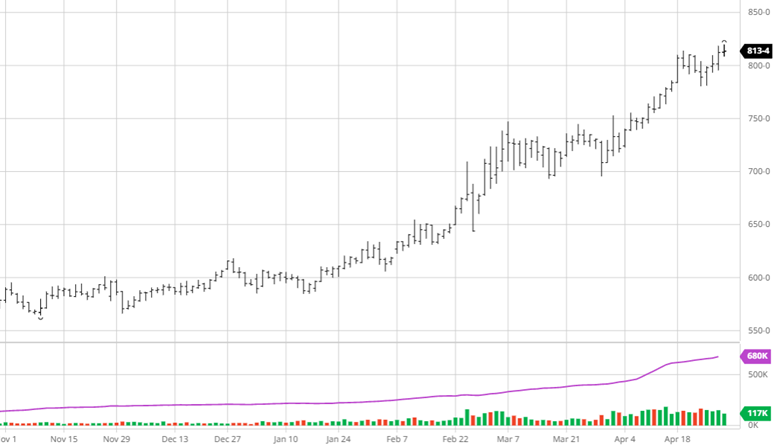

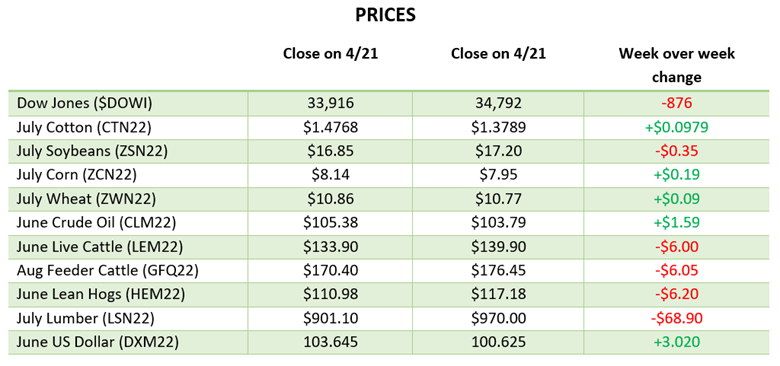

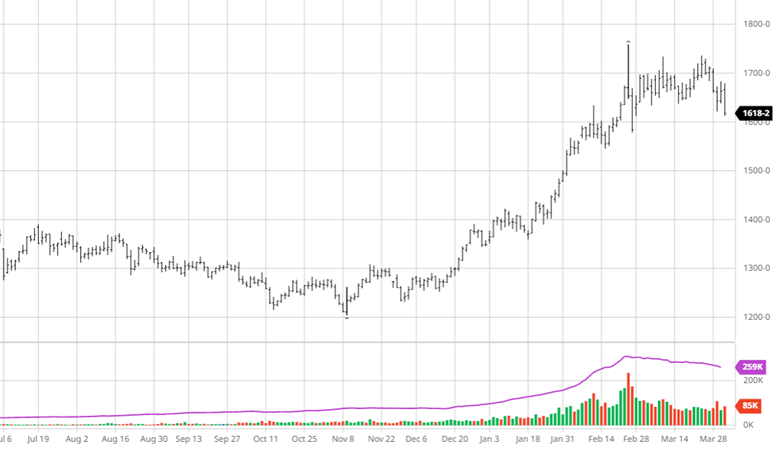

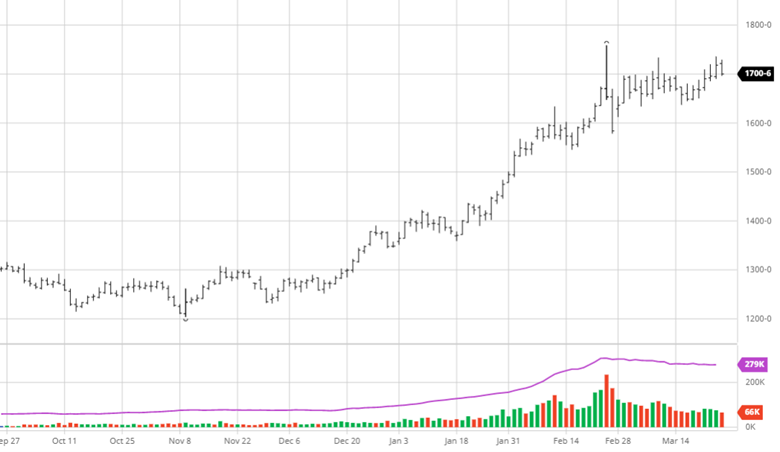

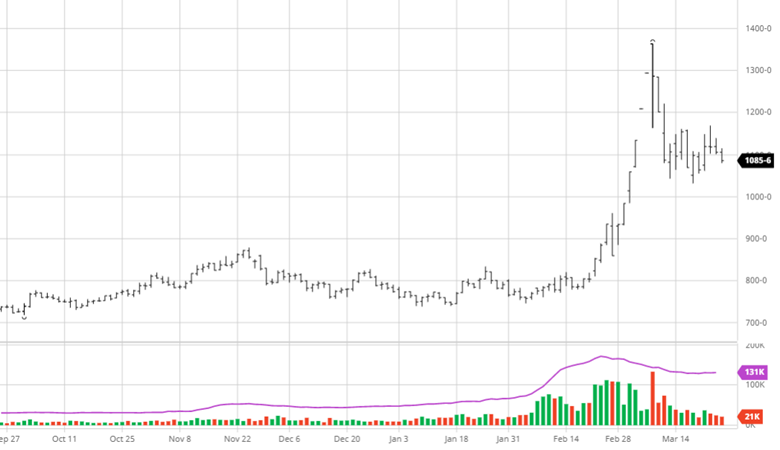

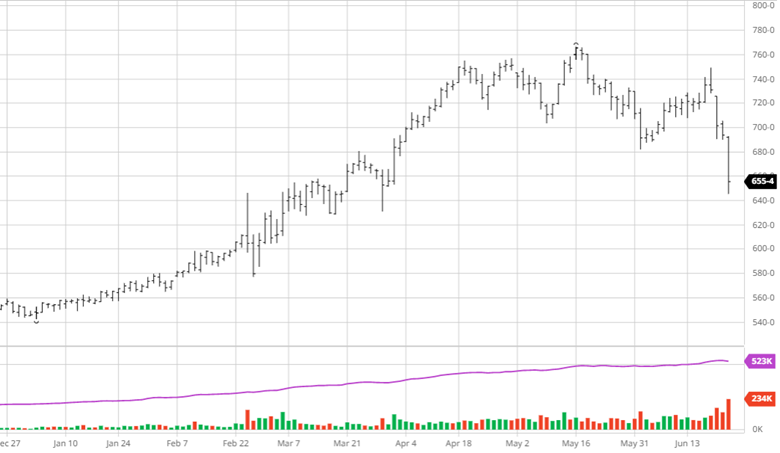

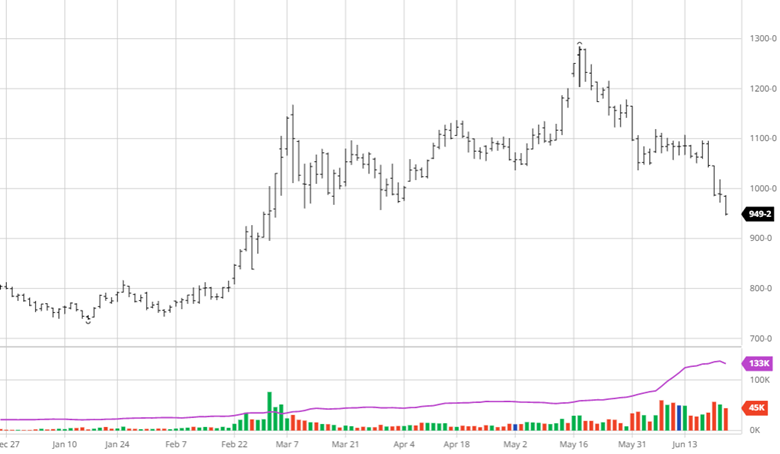

Corn had a rough week along with the overall commodity selloff the past few days. While the weather forecast has become cooler it is still going to be hot, and a lack of rain remains across much of the corn belt for the next week with higher chances in the 2-week forecast. Do not be mistaken – we are in a “weather market” where positions will change along with the forecasts.

Outside of weather, it has been the funds who have helped propel the move higher over the past year – naturally, when funds liquidate their large long position, you get a gut punch like we’ve seen this week.

With unknown weather, a potential recession looming, and fund profit taking the current market condition are flat out tough to speculate on and require the utmost discipline and focus on profit margin management.

The Planted Acreage and Quarterly Stocks report comes out next week followed by a 3-day weekend for the 4th of July.

Give us a call today to get your plan set for tomorrow (i.e next week!) 312-858-4049.

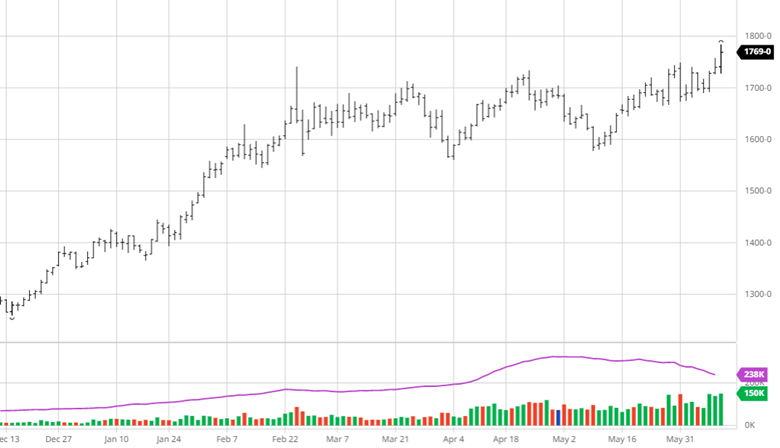

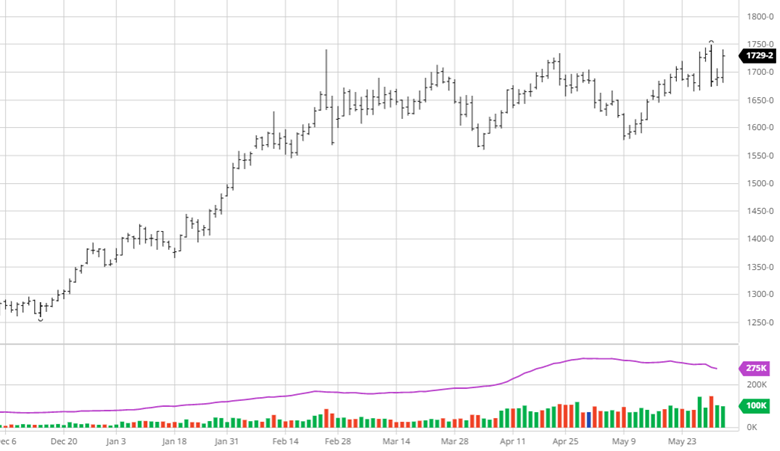

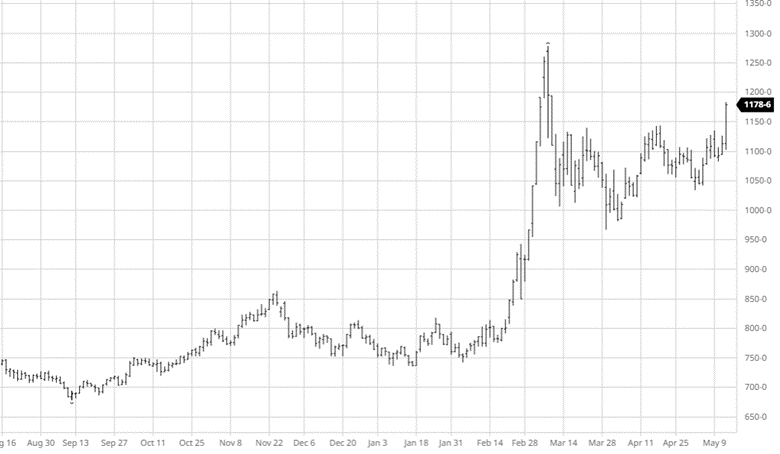

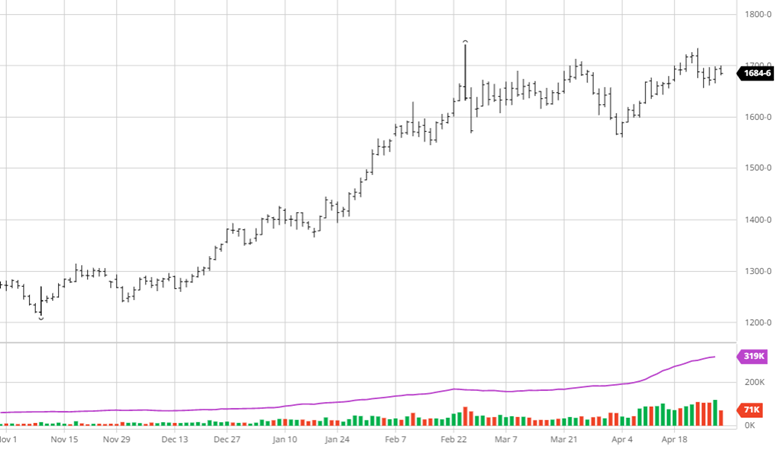

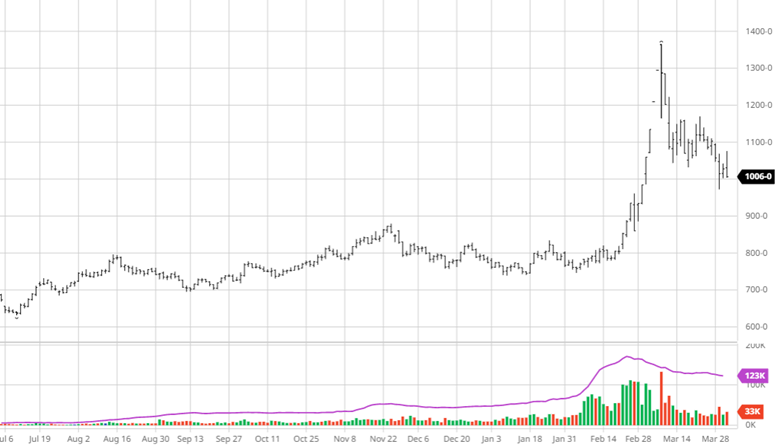

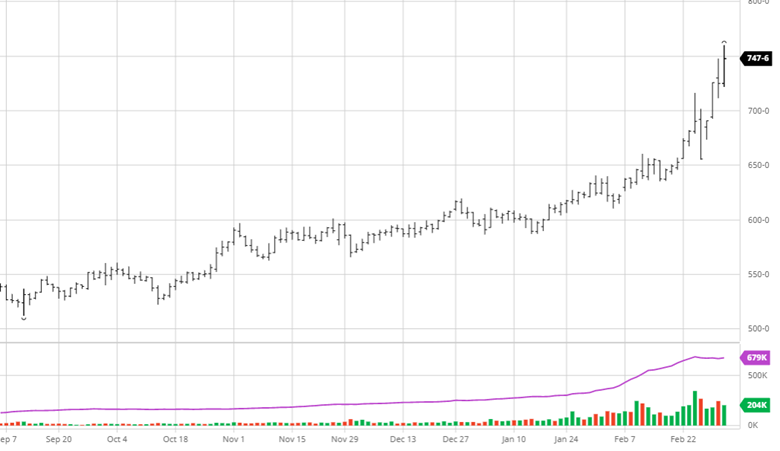

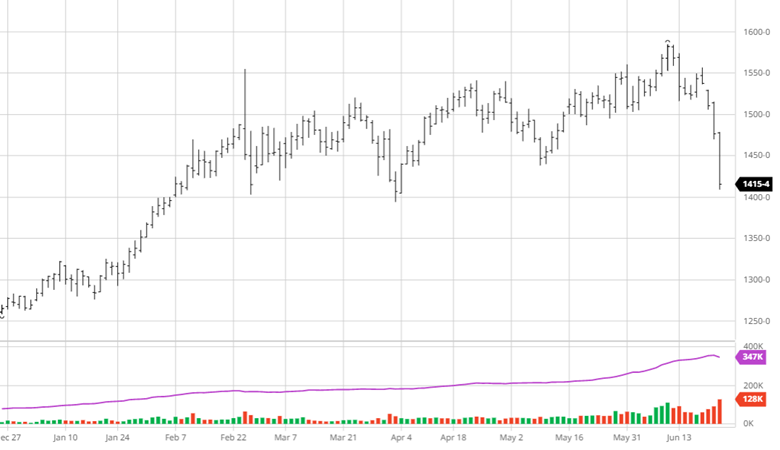

Soybeans suffered like corn from the cooler forecast and long liquidation this week. Collapsing world veg oil prices added pressure with the forecast change. Chinese Covid lockdowns and continued political friction will be in and out of the news but will always spook the markets. Beans and corn will be weather sensitive going forward but have suffered from outside forces like potential recession and lockdowns as well. The planted acres and stocks report will be important next week as well as weather over the 3 day 4th of July weekend.

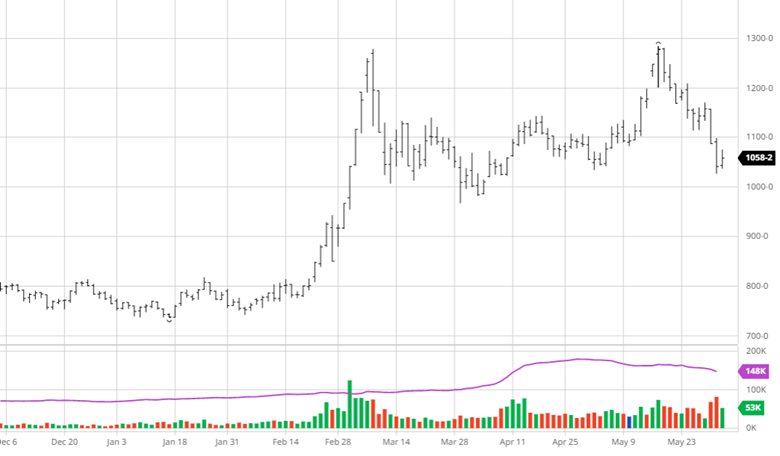

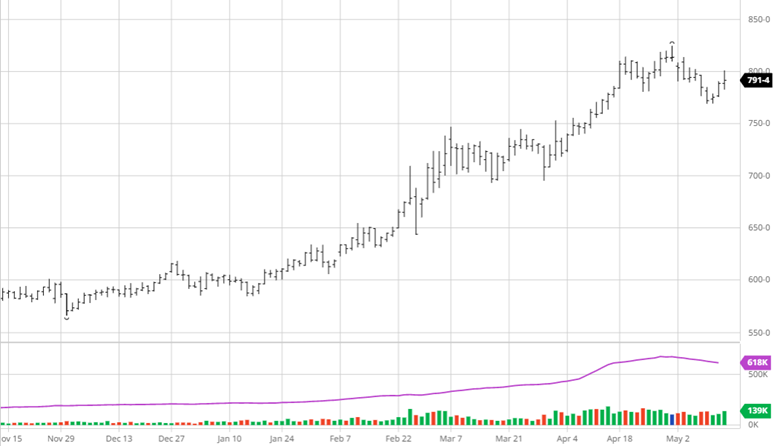

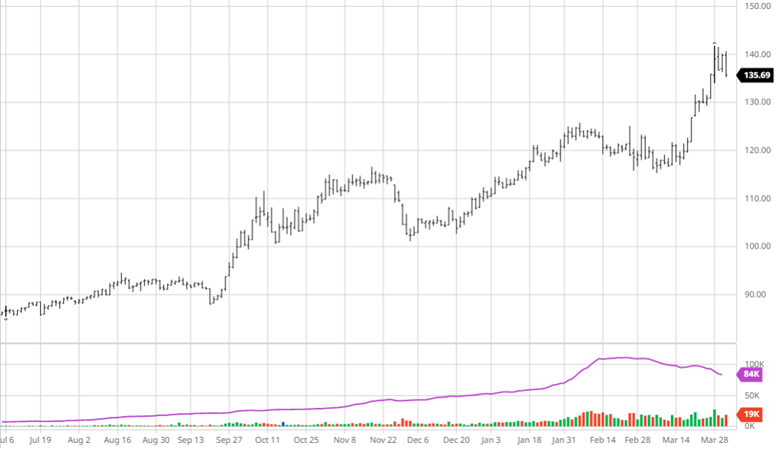

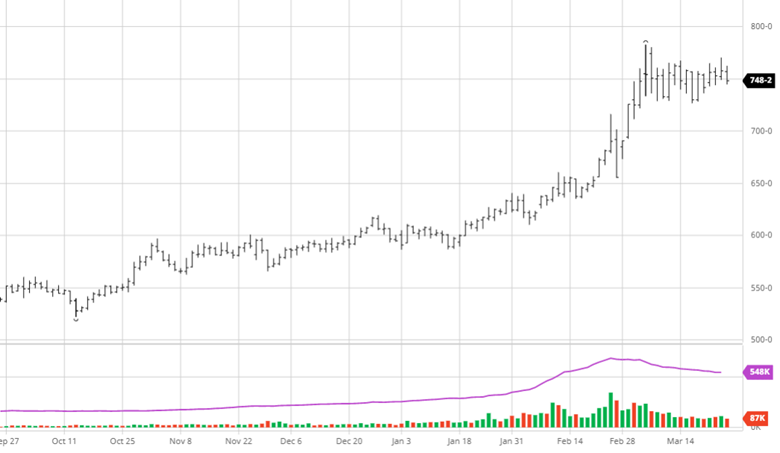

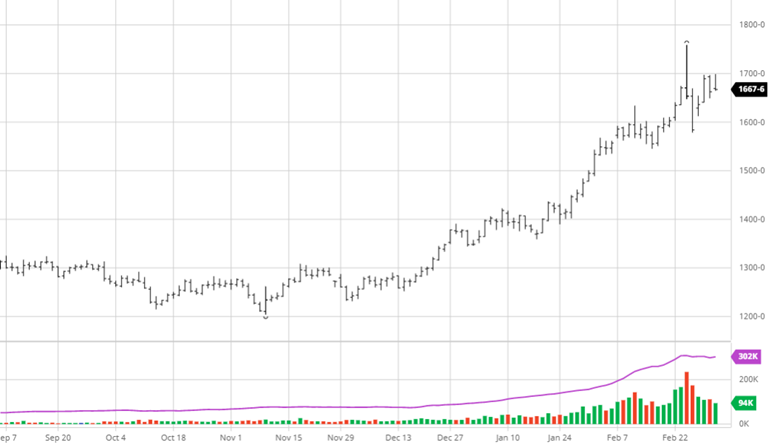

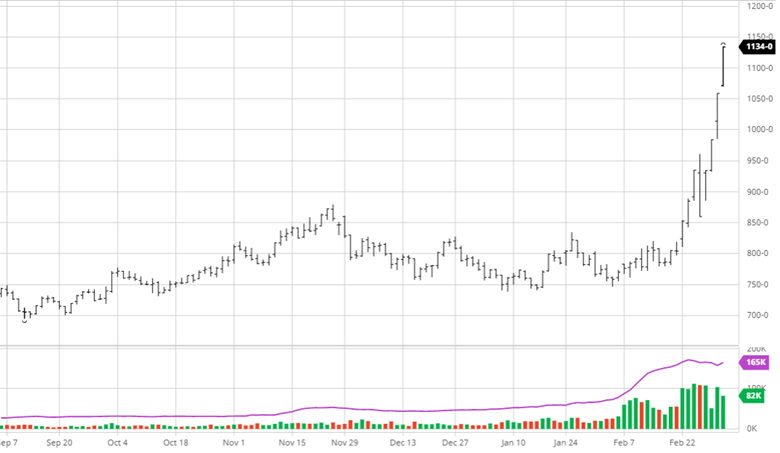

Wheat suffered along with other commodities with indications that Ukraine may be able to export more wheat than originally expected (not sure if this will come to fruition as the destruction of ports and shipping paths is continuing). Russian production estimates have risen, adding to the questions about what will be produced in Russia and Ukraine to be exported. The losses in wheat in recent weeks is confusing as the US yields are not spectacular, war continuing in Ukraine, and India is still in a drought, none of these are bearish factors yet we have come well off the highs.

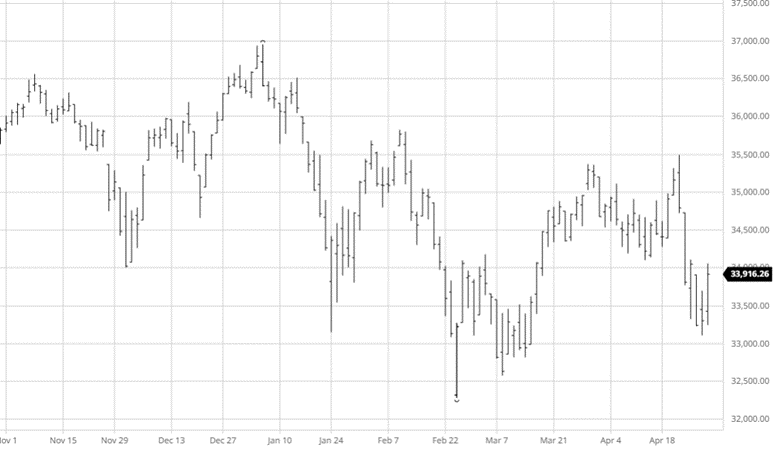

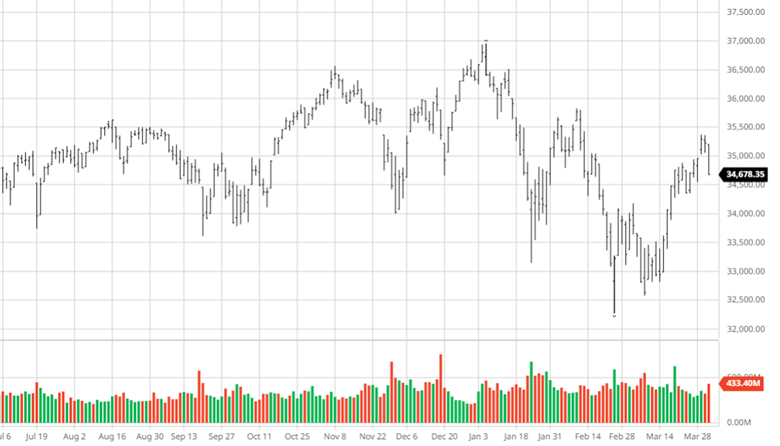

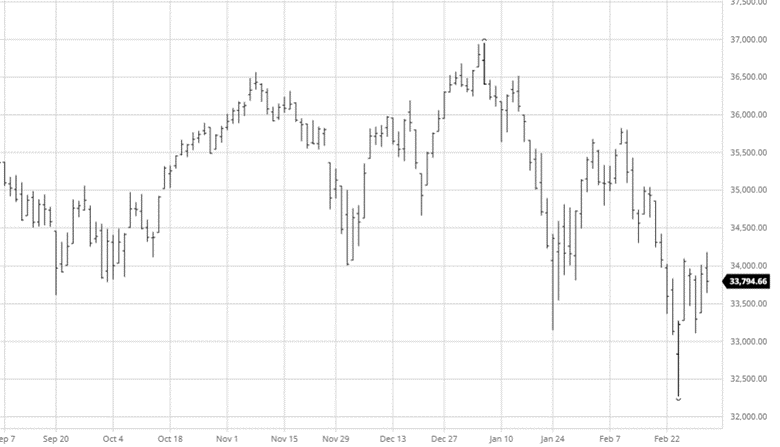

Equity Markets

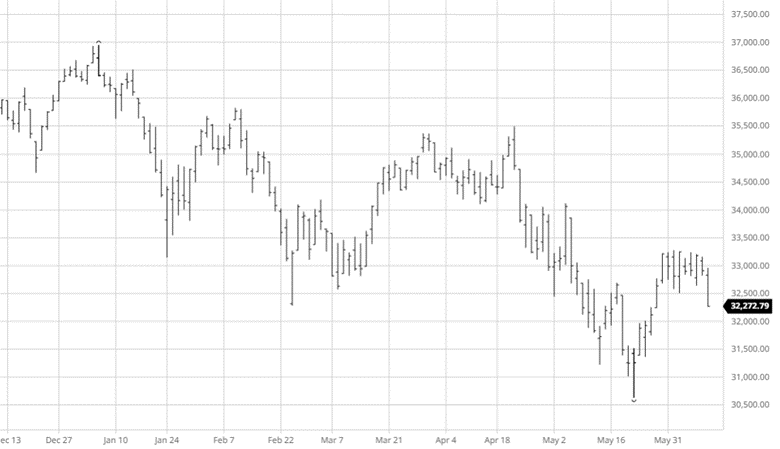

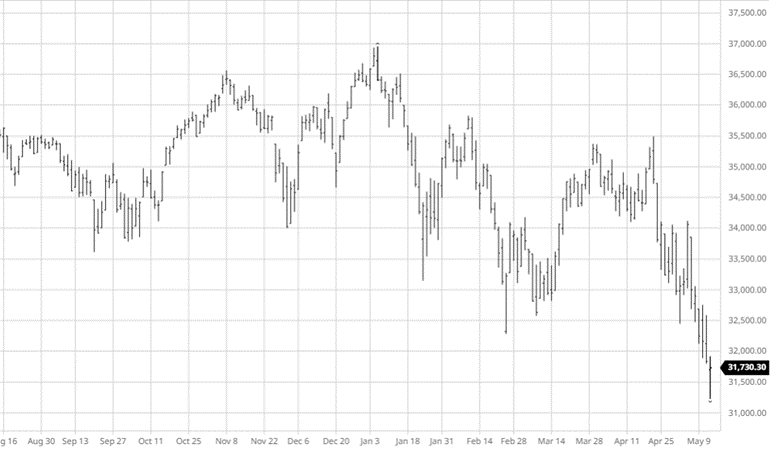

It has been a bad past couple weeks for the equity markets as they fell lower following the Fed raising rates 75 points and lots of debate of a recession in the future. While the Fed tries to make up for late moves and inflation continues to affect the country it is important to look what has gotten us here. As companies are likely to lower future earnings expectations, it will be important for markets to figure out fair value after the last 2 years of staggering valuations.

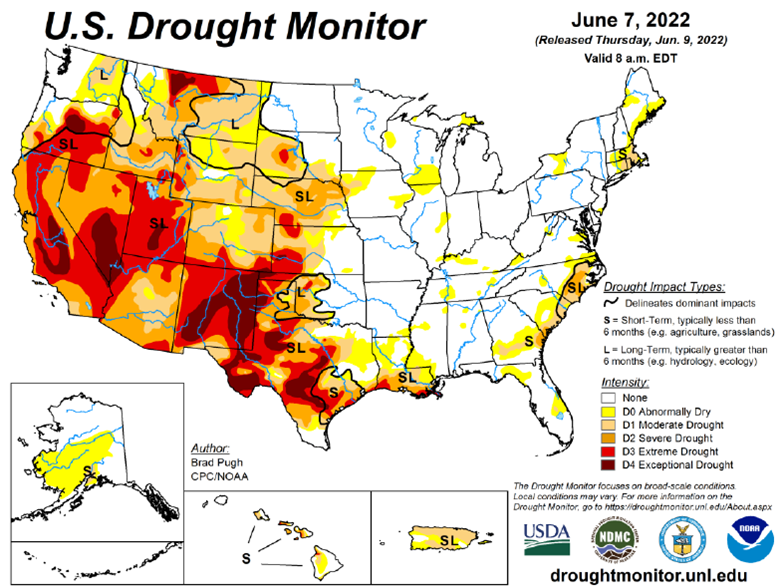

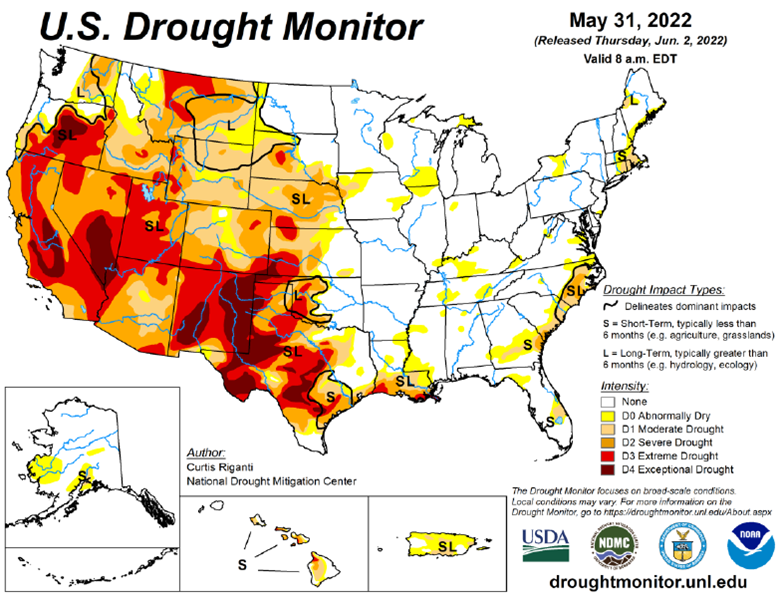

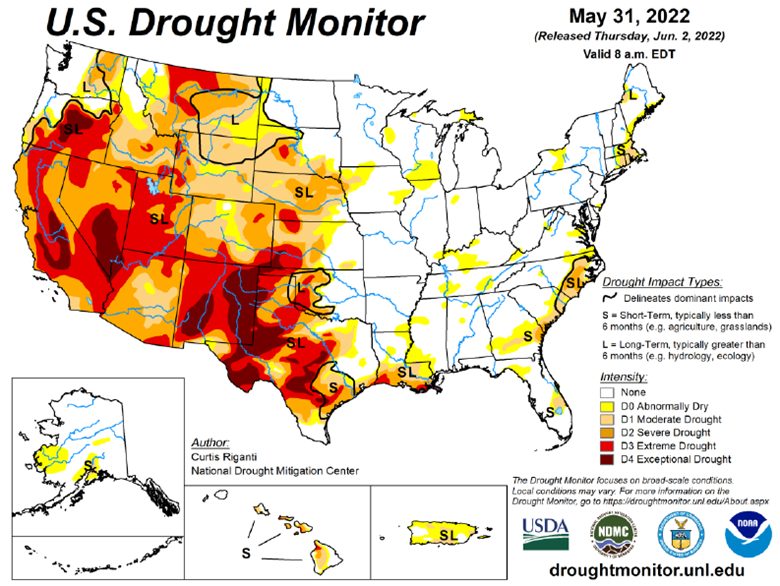

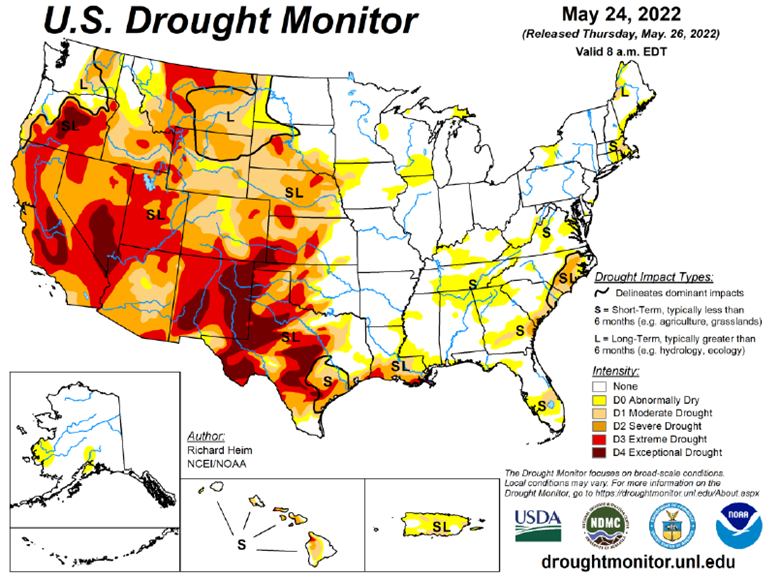

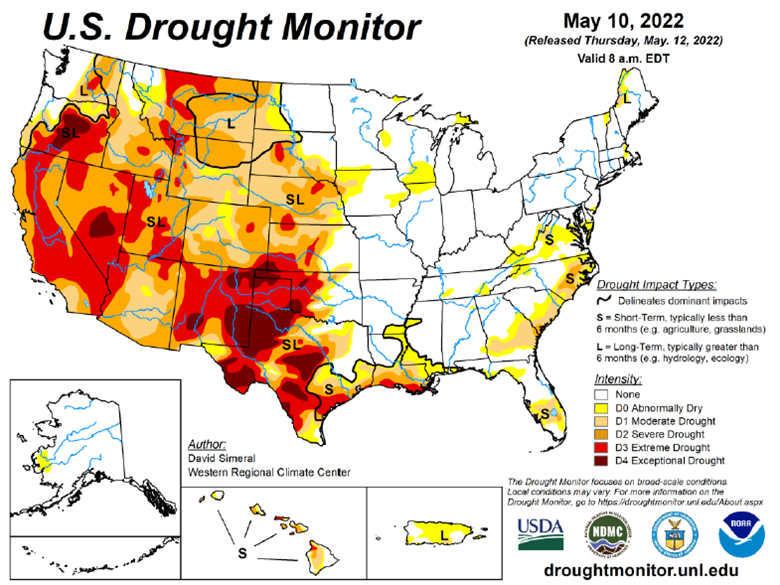

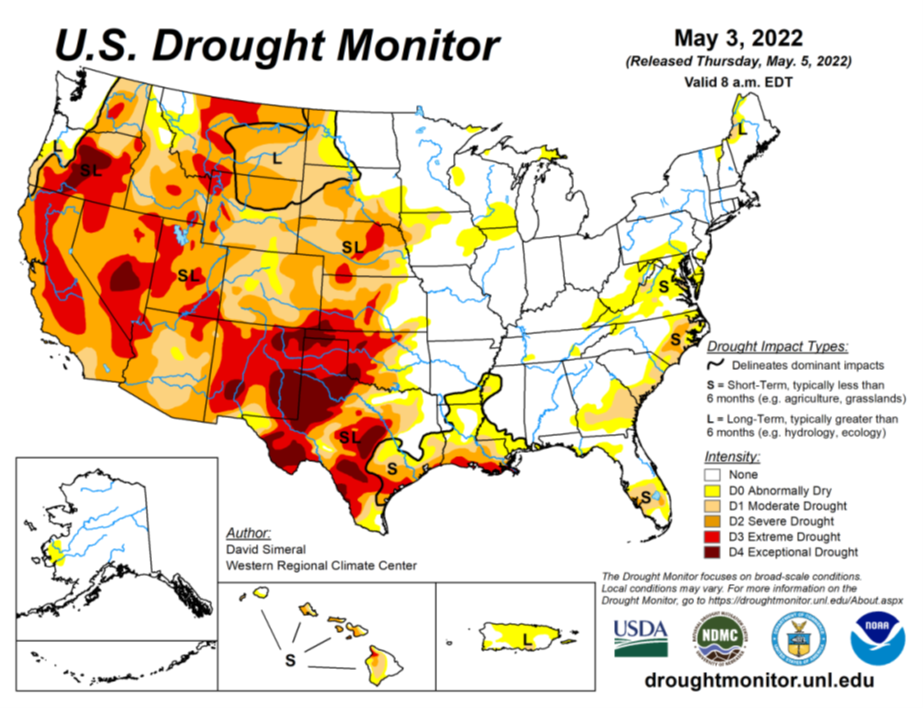

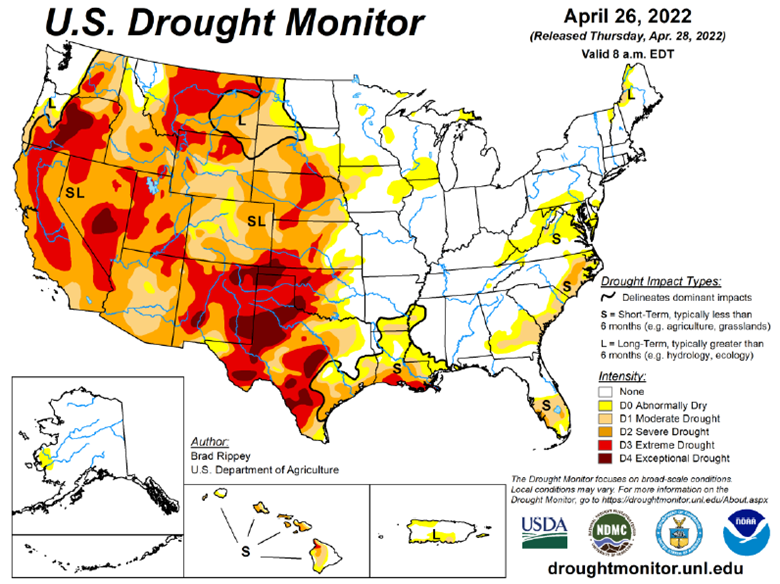

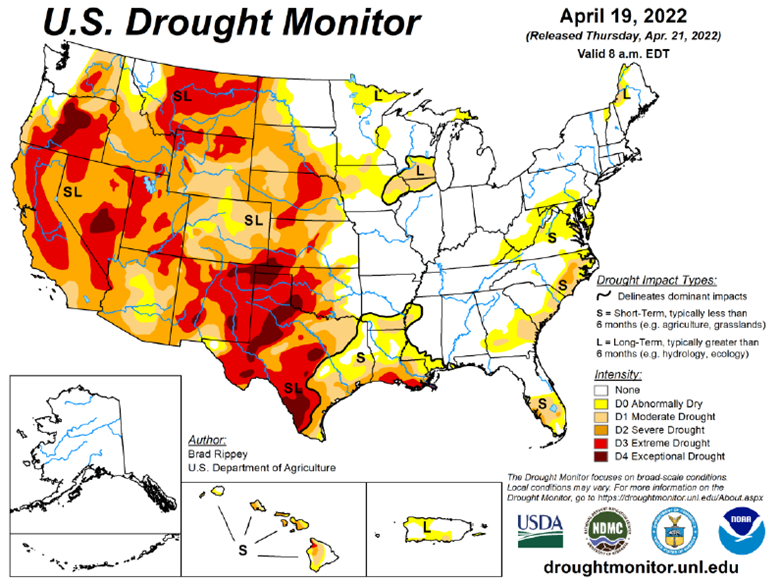

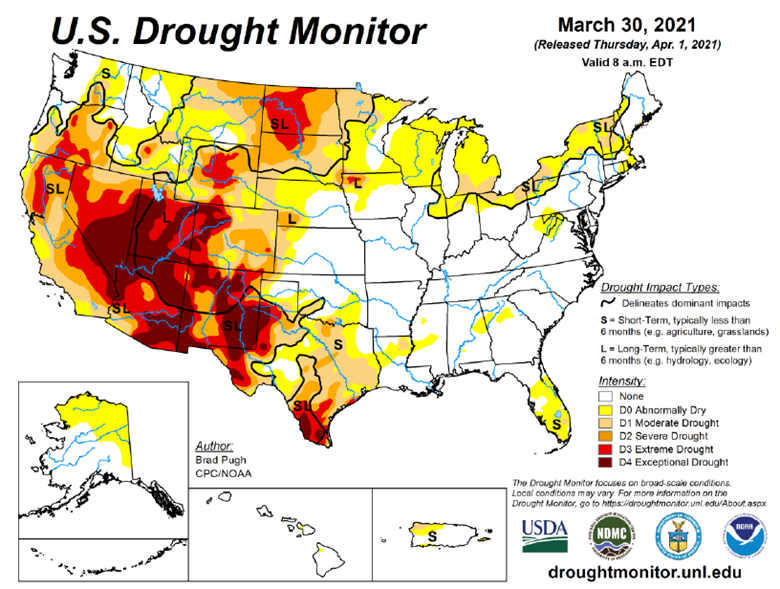

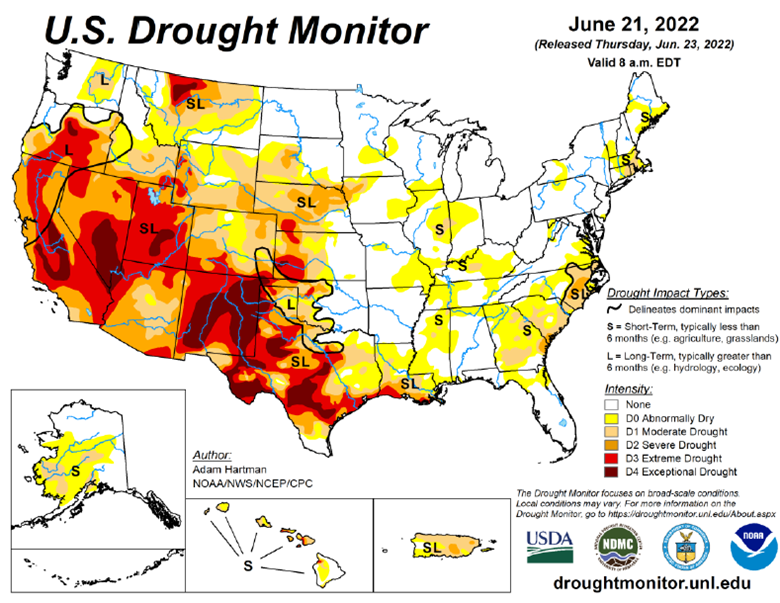

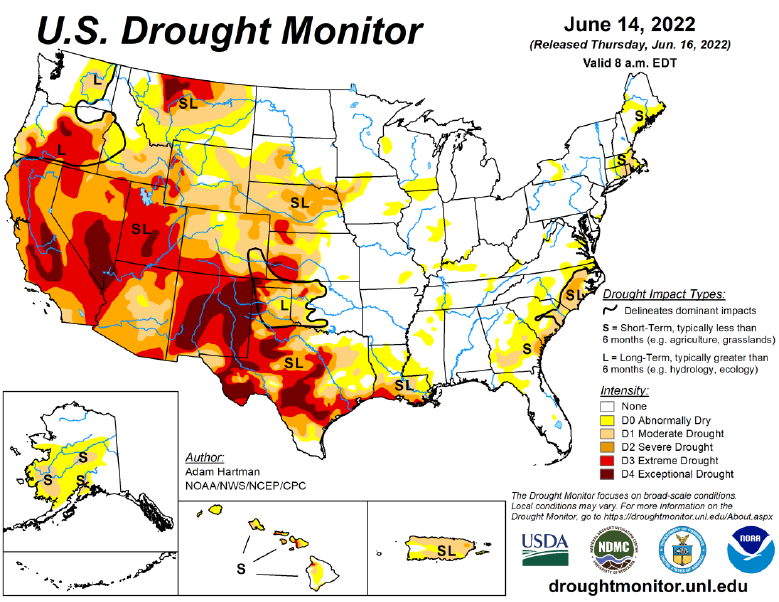

Drought Monitor

The drought monitor below shows where we stand week to week.

Podcast

There is an agriculture tug of war happening across the nation, impacting America’s farmland. Fertilizer prices are continuously fluctuating, and it has us taking a page the “The Clash” should we stay, or should we go?! And we aren’t the only ones. Many farmers are asking their agronomist and chemical salespeople, “what will fertilizer cost me the rest of the season, and what are my options if I don’t want to go all-in on my typical fertilizer treatment plan?”

In this episode of the Hedged Edge, we are joined by a special guest who needs no introduction in his local circle, Dick Stiltz. Dick is a 50-year veteran of the fertilizer and chemical industry and is the current Agronomy Marketing Manager of Procurement fertilizer and crop protection at Prairieland FS, Inc in Jacksonville, IL. He is at the pulse of the current struggle and here to discuss the topic at hand.

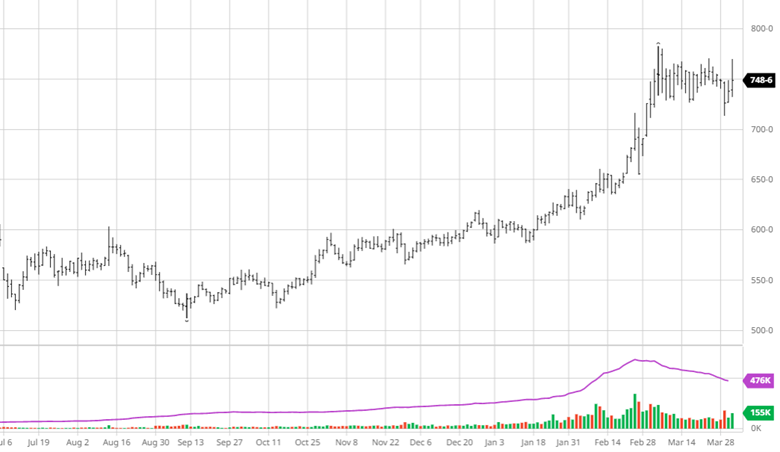

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.