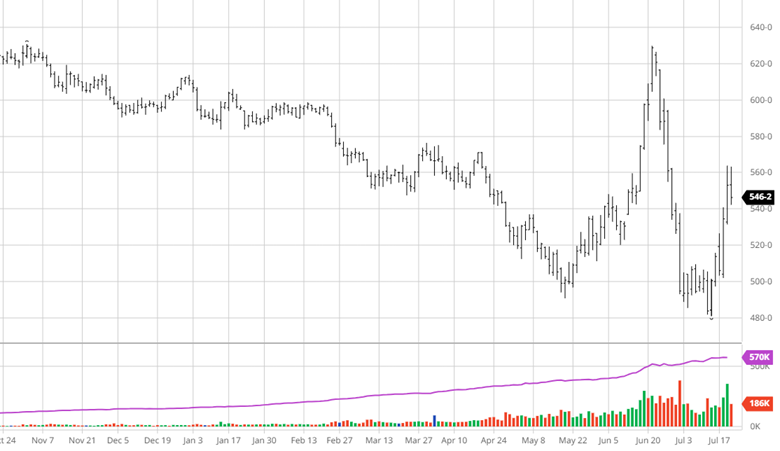

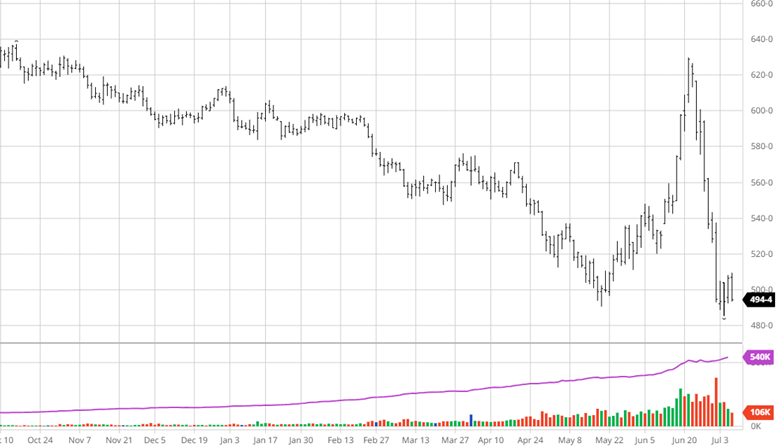

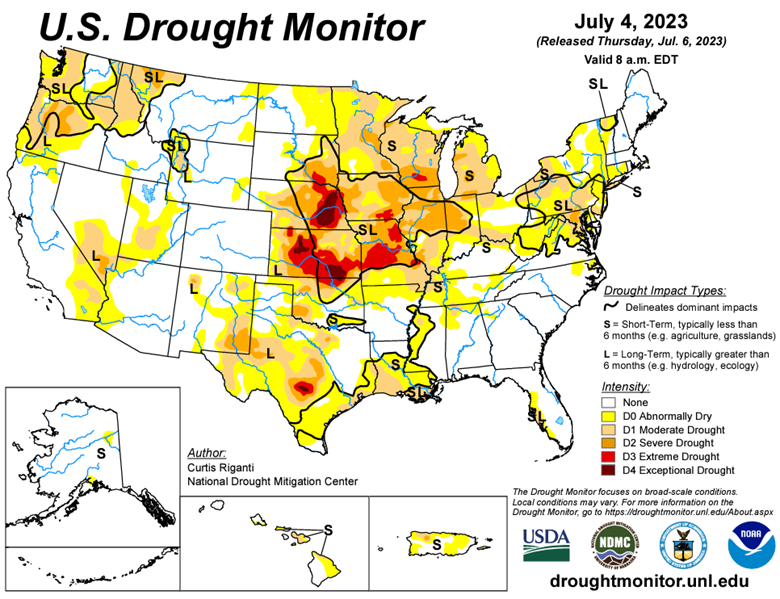

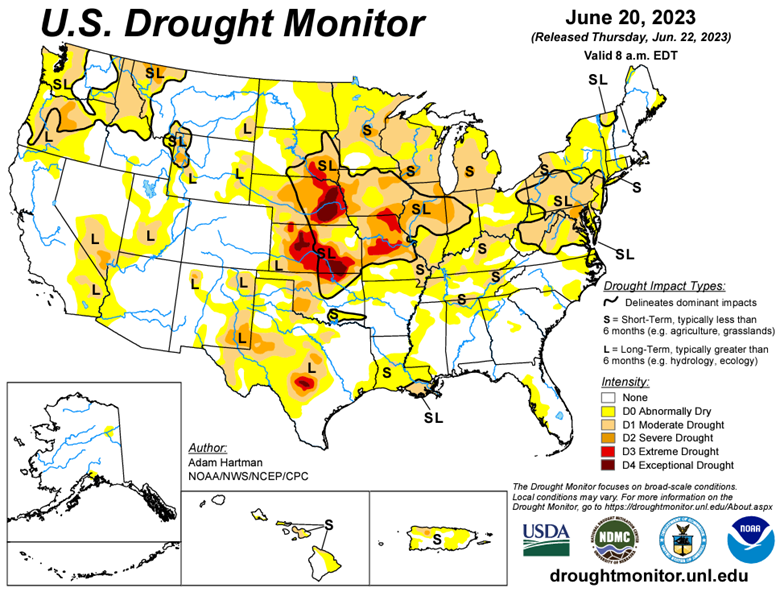

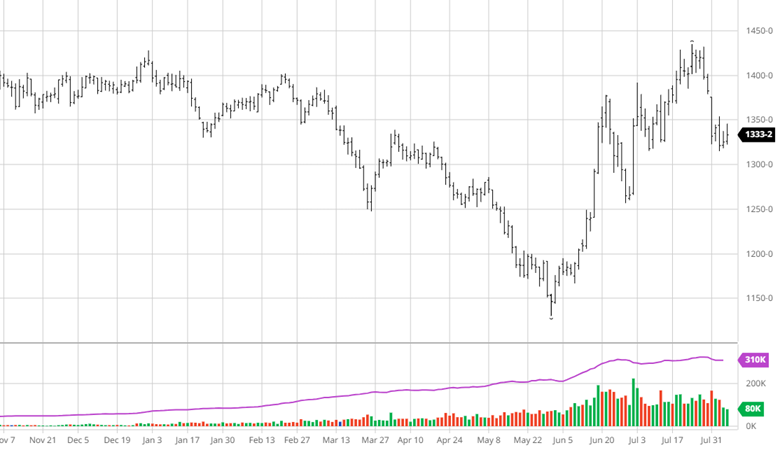

As quickly as corn rallied to get back over $5.50, the rains and favorable forecasts for August led it back below $5 just as quickly. The rains in late July provided much needed moisture over much of the corn belt, but as you can see in the drought charts below, varying levels of drought conditions remain. The forecast has shifted drier for August but after a record hot July, August is forecasted to be cooler. Reports of how much damage the first half of summer did to this crop are all over the place, which usually means it is somewhere in the middle. A 180+ yield is probably off the table, but a 172 yield seems to be just as unlikely unless the forecasts change to hot and dry for a long stretch soon. Russia’s bombing of Ukrainian ports in Odesa and the Danube River continue as the markets seem to shrug off any new damage. Over the weekend any forecast changes, new developments in Ukraine or world news will determine what the trade does to start the week.

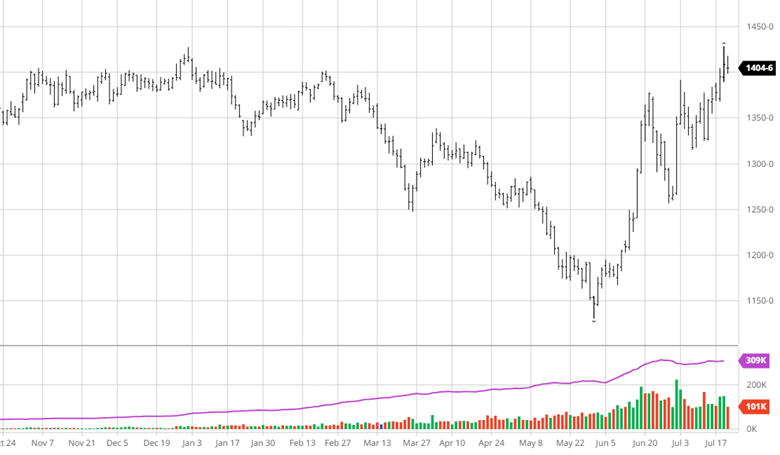

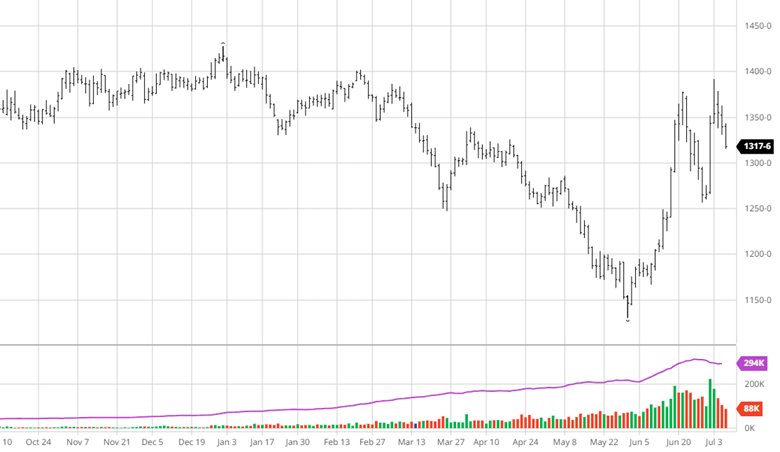

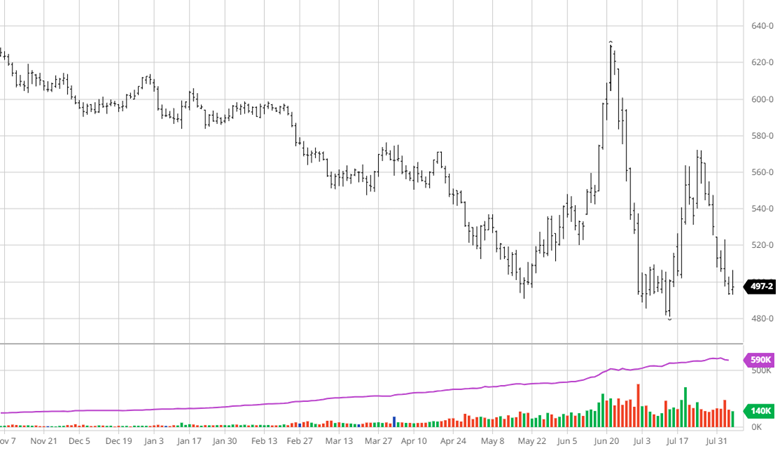

Soybeans have a similar story to corn this week but were able to avoid the late June collapse that corn saw thanks to the low acreage number. StoneX estimate for bean yield this week was 50.5 bu/ac which would be a supportive number for beans, especially if the acreage number is accurate. China has begun showing up as frequent buyers in export reports helping the demand story that was questionable on world economic worries not too long ago. The lack of bullish news is good news for the bears as no news markets rarely tend to move higher. Weather in August will be important for this crop and next week’s USDA report will give us more information on US production.

Recent News

Click HERE to listen to RCM Ag Services’ Jody Lawrence join AgriTalk a couple weeks ago to discuss the current market.

Wheat

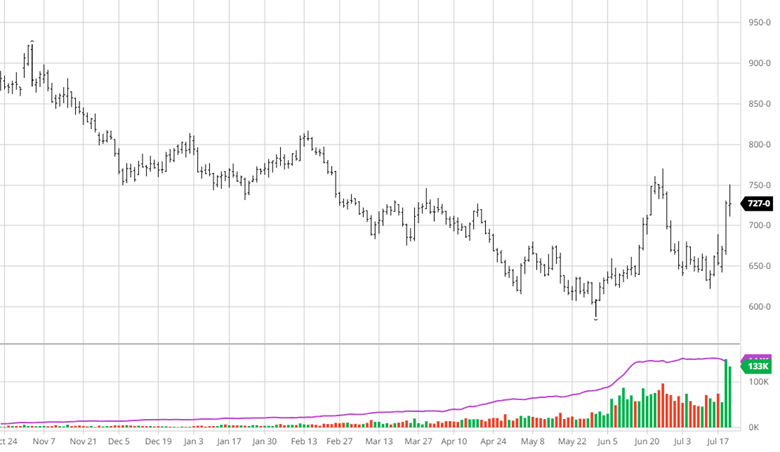

Wheat followed corn and beans lower for similar reasons. The markets have shrugged off Russian aggression of late but will be watching over the weekend for any escalation.

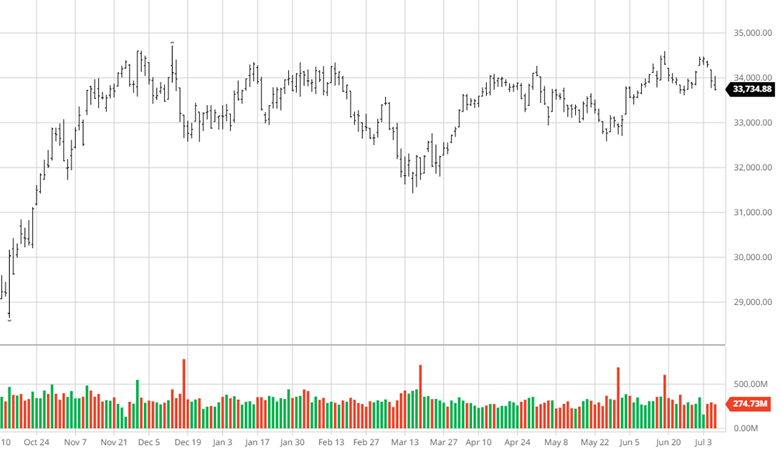

Equity Markets

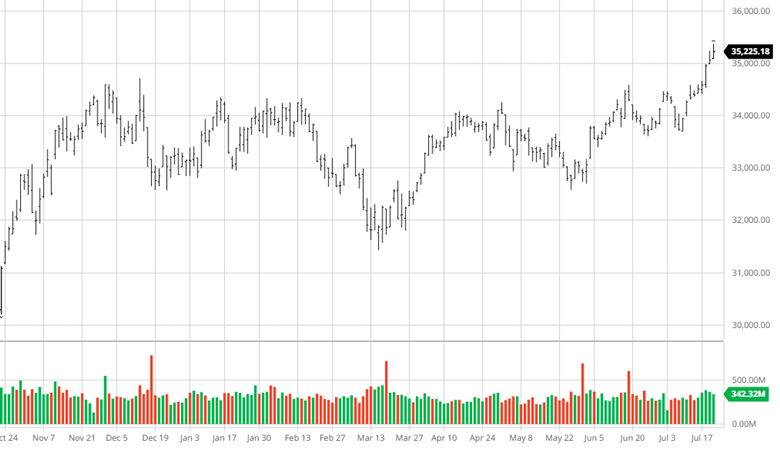

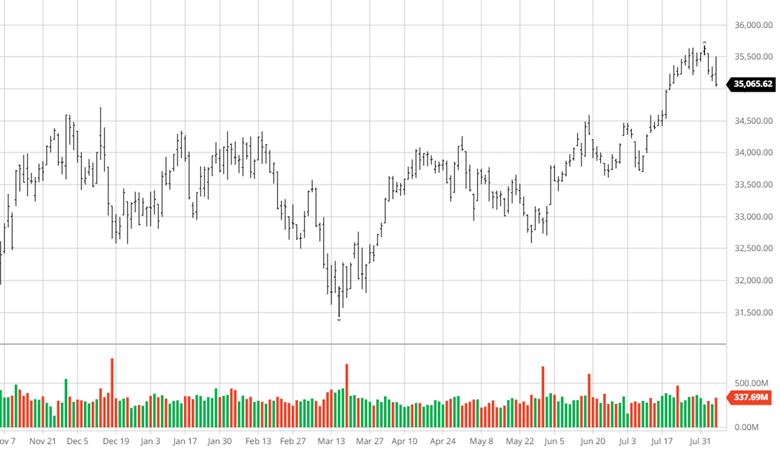

The equity markets suffered losses this week with a big down day on Wednesday when Fitch downgraded US debt to AA+ and earnings continue to roll in. The job market seems to be moderating as hiring was slightly weaker than the previous month. The markets are looking for numbers that will keep the economy and markets going while also giving the Fed the signal to stop raising rates. This is a fine line that can feel like walking on eggshells with a long-predicted recession still the worry of most investors.

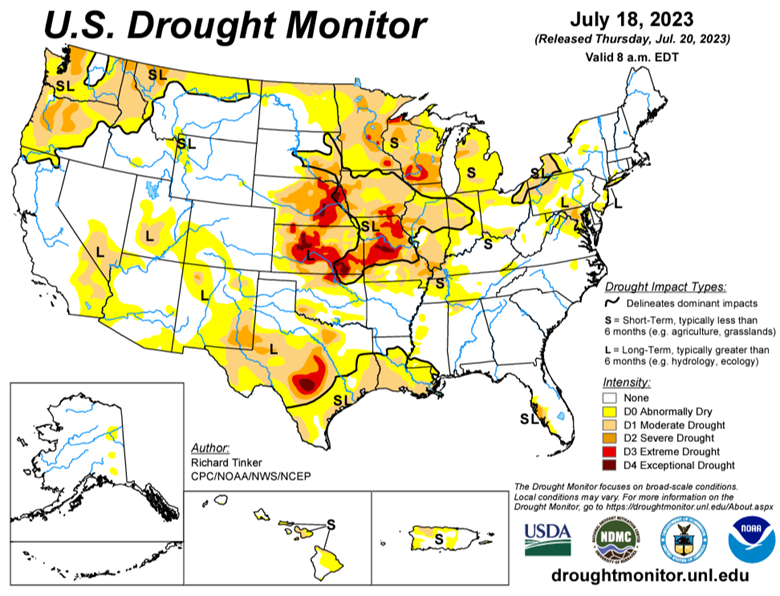

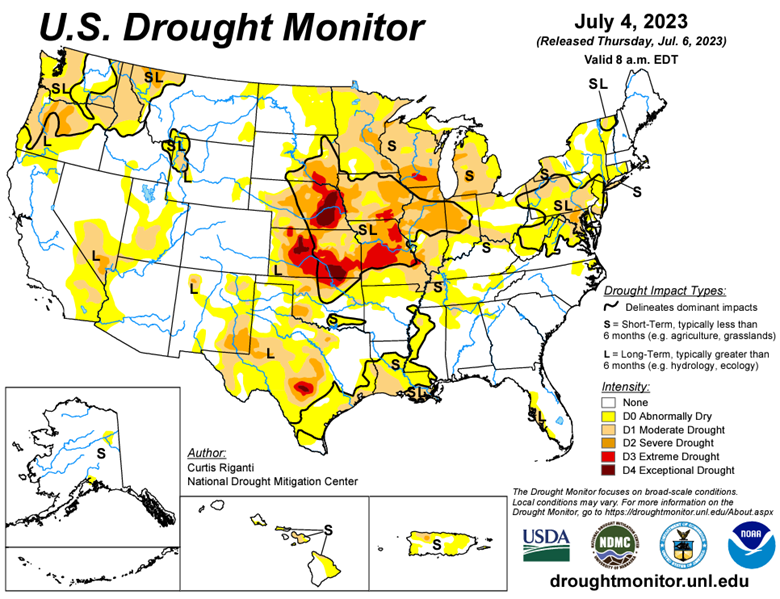

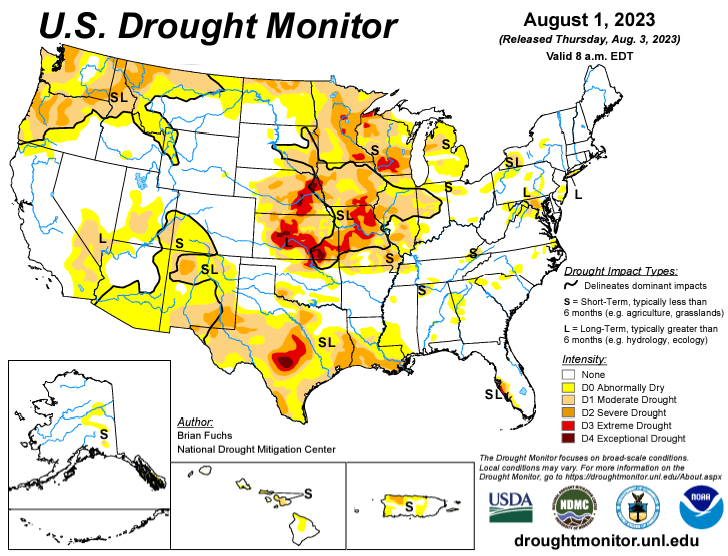

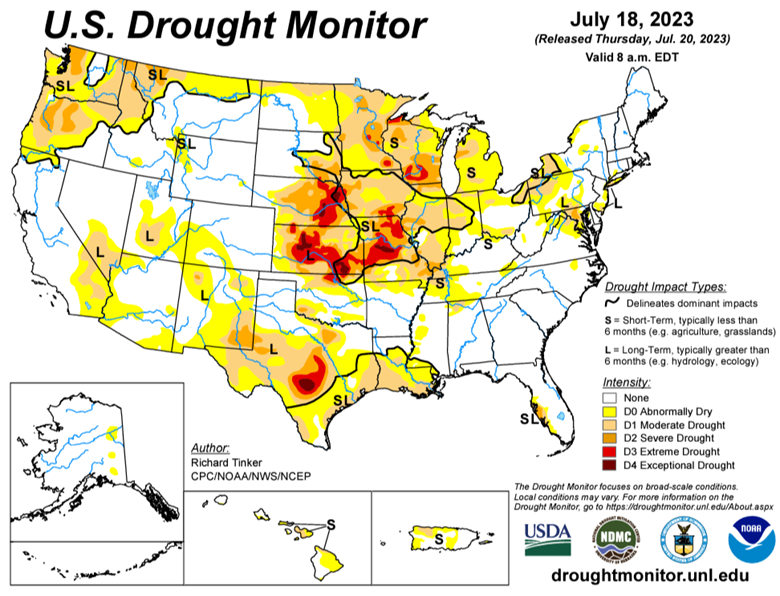

Drought Monitor

The drought monitors below show the change in drought conditions over the last 2 weeks.

Podcast

With every new year, there are new opportunities, and there’s no better time to dive deeply into the stock market and tax-saving strategies for 2023 than now. In our latest episode of the Hedged Edge, we’re joined by Tim Webb, Chief Investment Officer and Managing Partner from our sister company, RCM Wealth Advisors. Tim is no stranger to advising institutions and agribusinesses where he has been implementing no-nonsense financial planning strategies and market investment disciplines to help Clients build and maintain wealth and reach financial goals since

Inside this jam-packed session, we’re taking a break from commodities, and talking about the world of equities, interest rates, tax savings, and business planning strategies. Plus, Jeff and Tim delve into a variety of topics like:

- The current state of the markets within the wealth management industry

- Is there a beacon of hope, or is it all doom and gloom for the markets?

- Other strategies to think about outside of the stock market and so much more!

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.