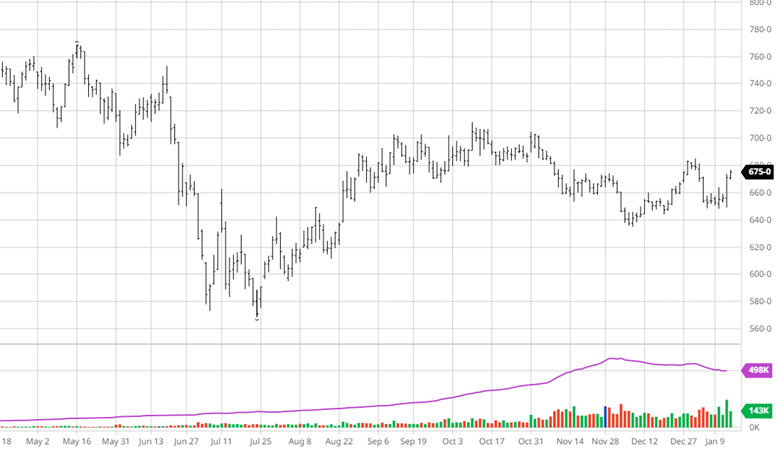

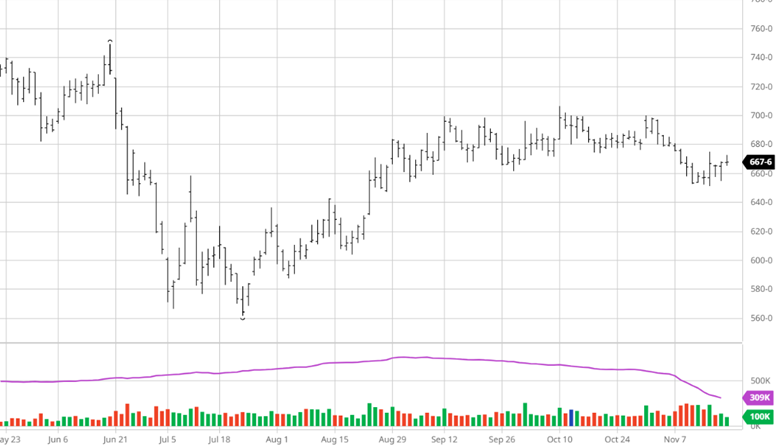

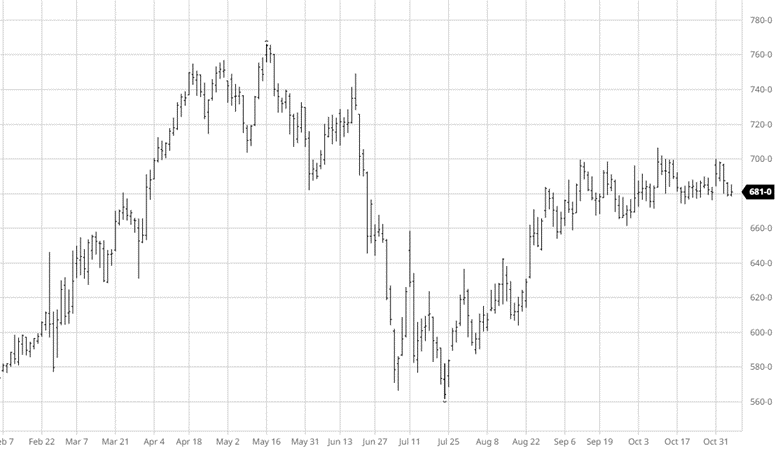

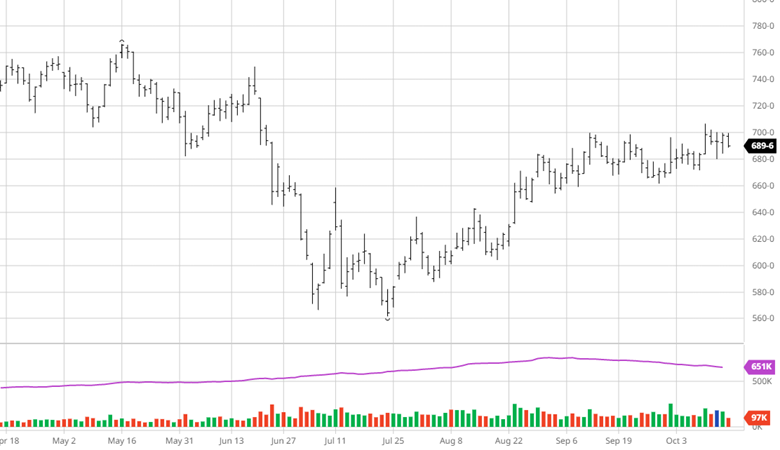

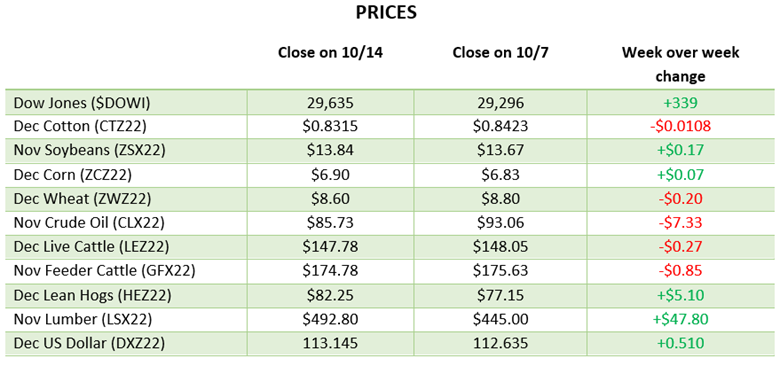

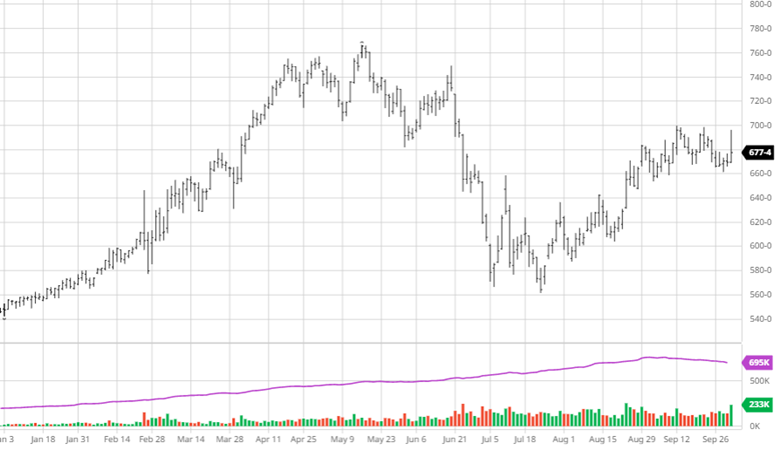

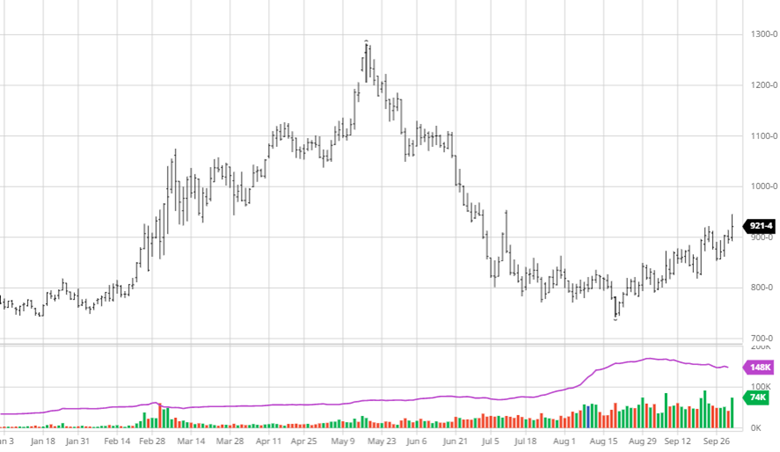

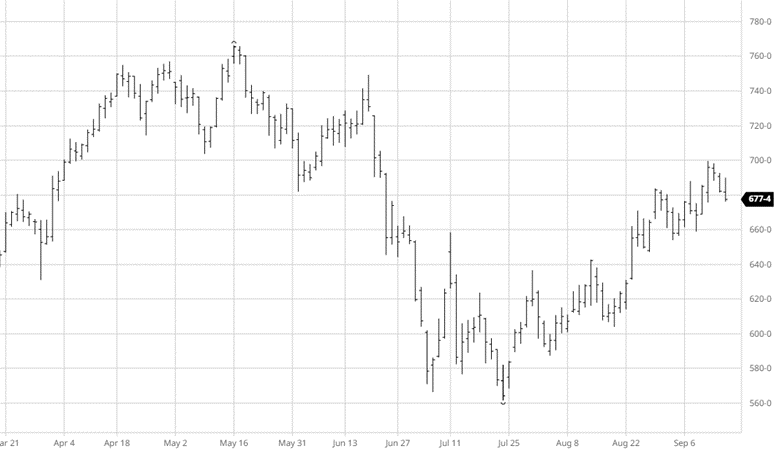

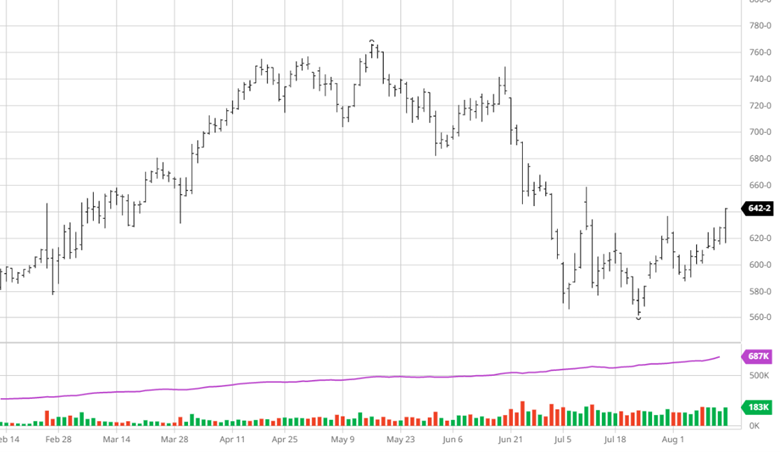

Corn has been relatively flat over the last two weeks as it has continued to trade in a tight range the last 3 weeks. This week’s USDA Report did not provide any fireworks as there were no big surprises. The USDA lowered Argentina’s production while leaving Brazil’s unchanged from the January report. While the lowering of Argentina’s yield was expected, analysts still believe it will be lower. The main change to the US balance sheet was a 25-million-bushel reduction in ethanol consumption of corn, leading to a slight rise in ending stocks. World stocks received a boost from smaller world feed usage while stocks remain historically tight. Exports got off to a good start in February, with the week ended 2/02, coming in at the top end of estimates.

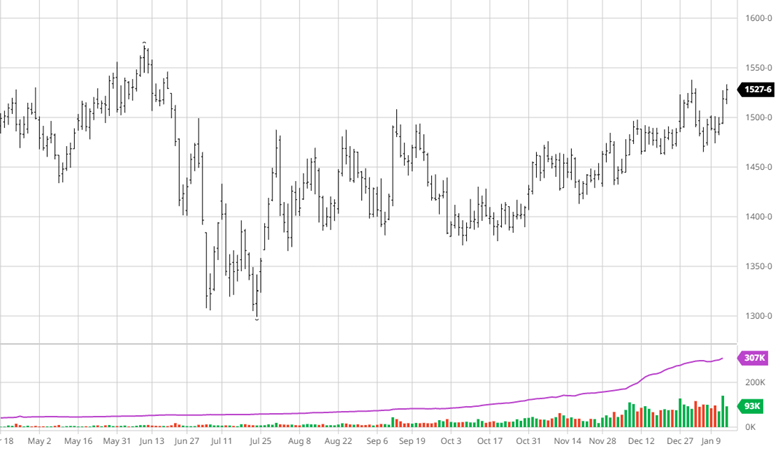

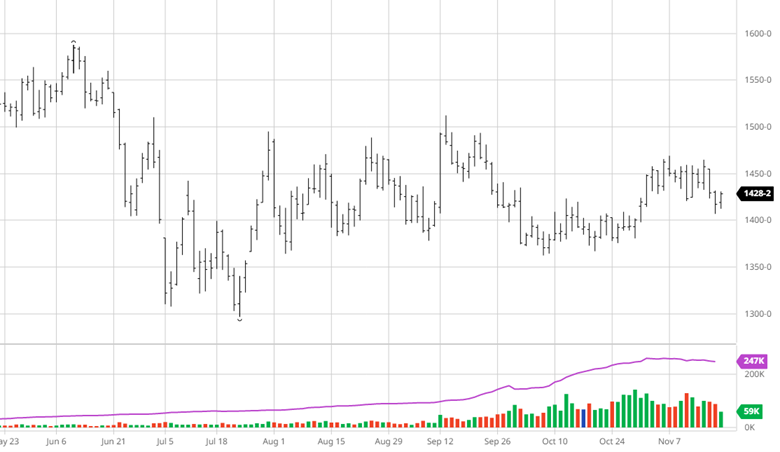

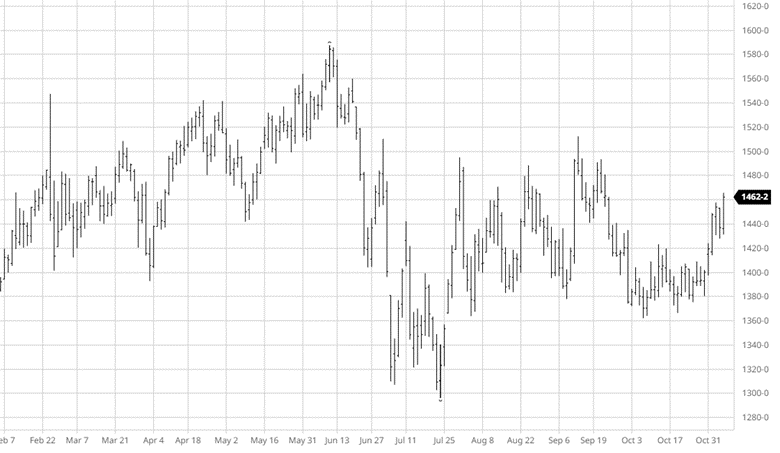

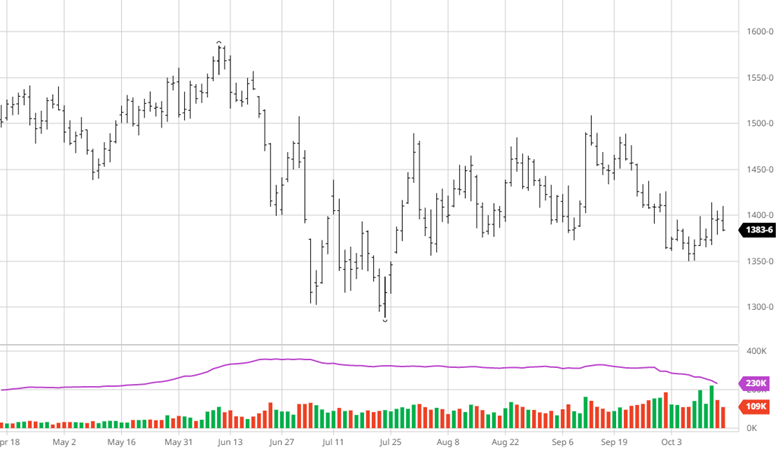

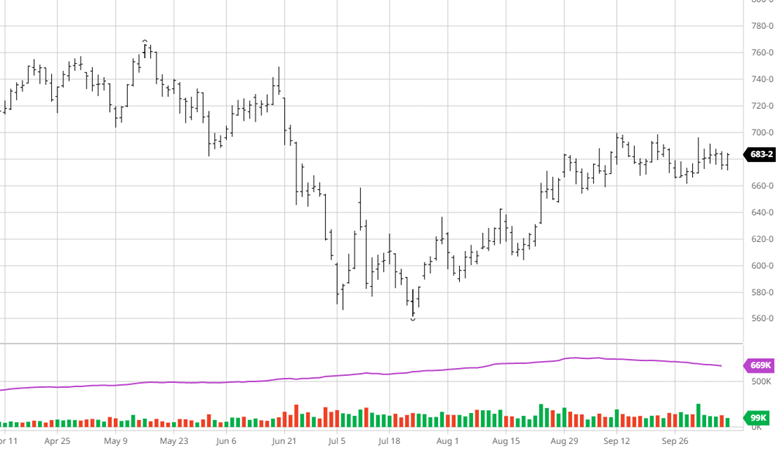

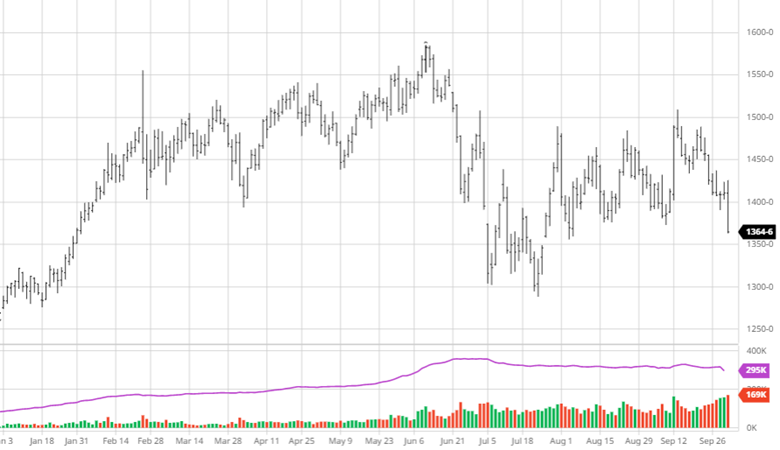

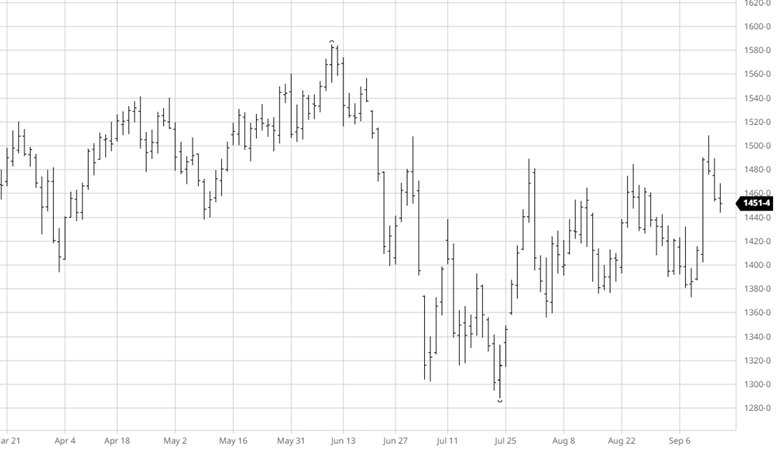

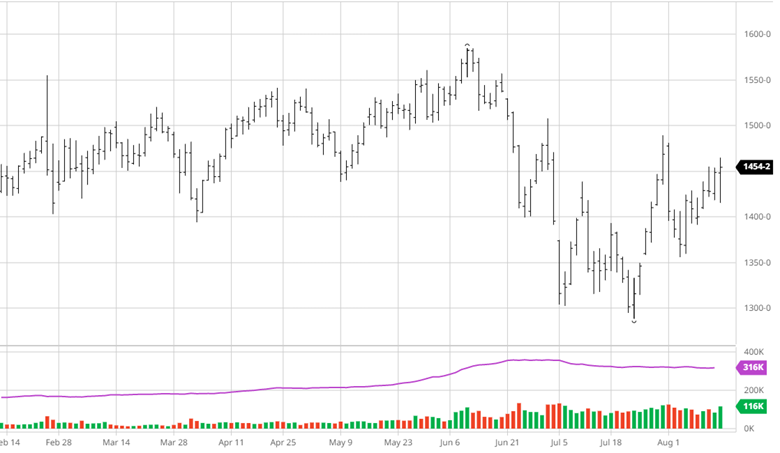

Soybeans had not moved much over the last two weeks until Friday’s trade saw the march futures get a 24 cent boost while new crop gained 13 cents. Like corn the USDA report was a non-event for beans with no major news. The only notable changes were lowering Argentina’s total yield and lower crush numbers in the US. The lower crush in the US was more newsworthy as the markets had priced in lower Argentinian yield. World ending stocks were right on estimates.

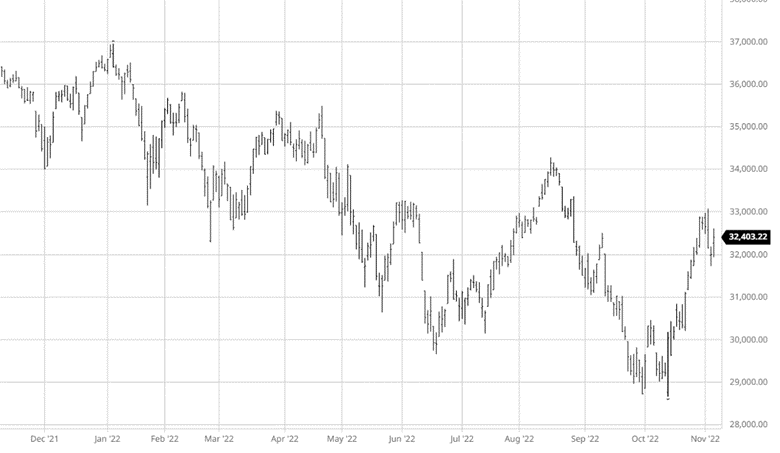

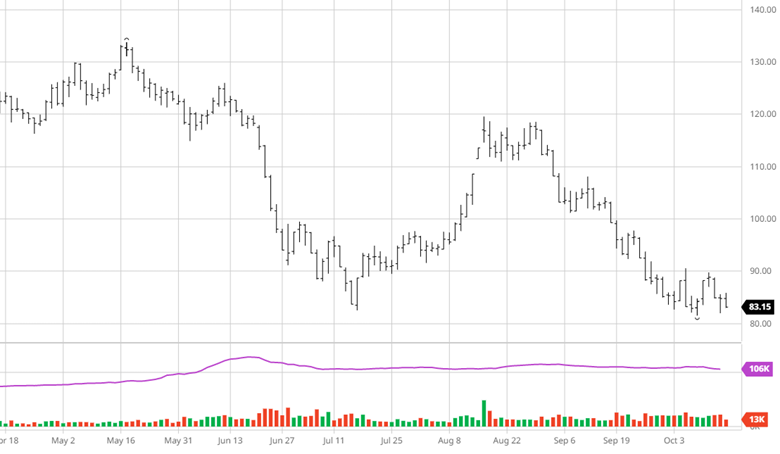

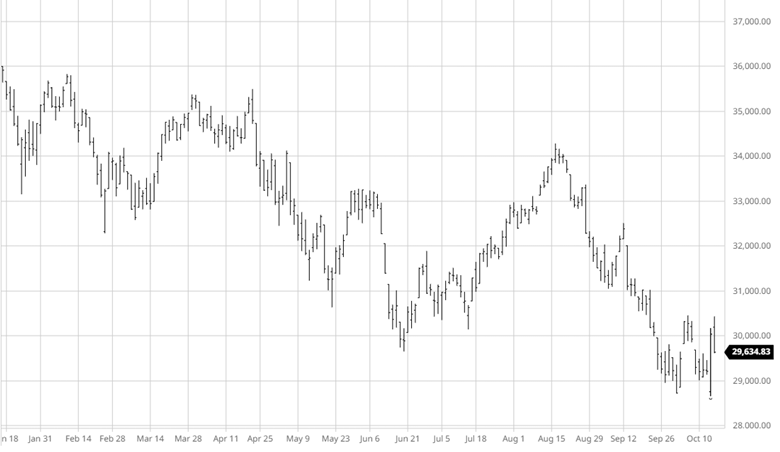

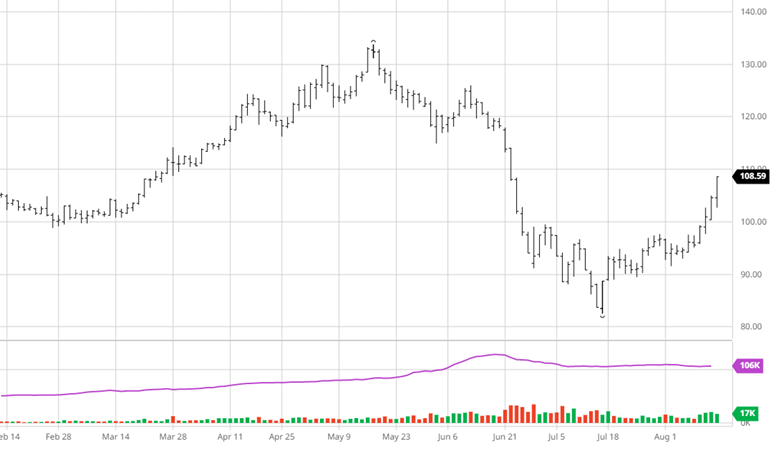

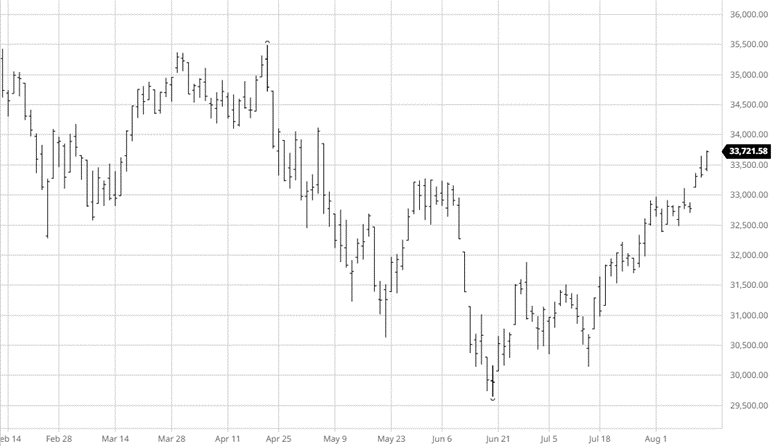

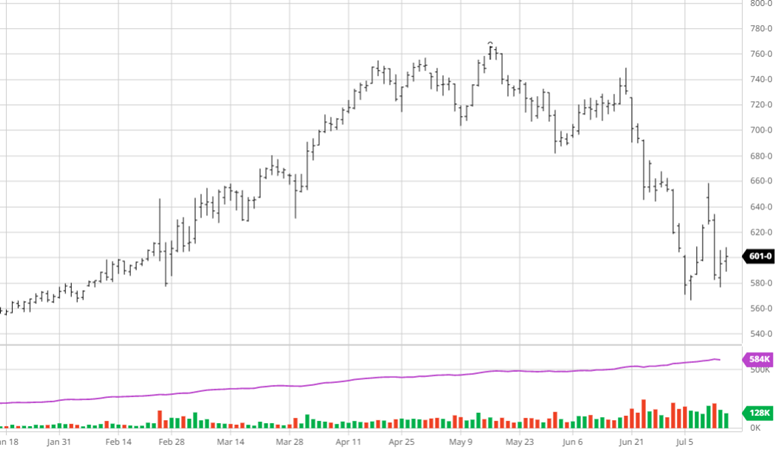

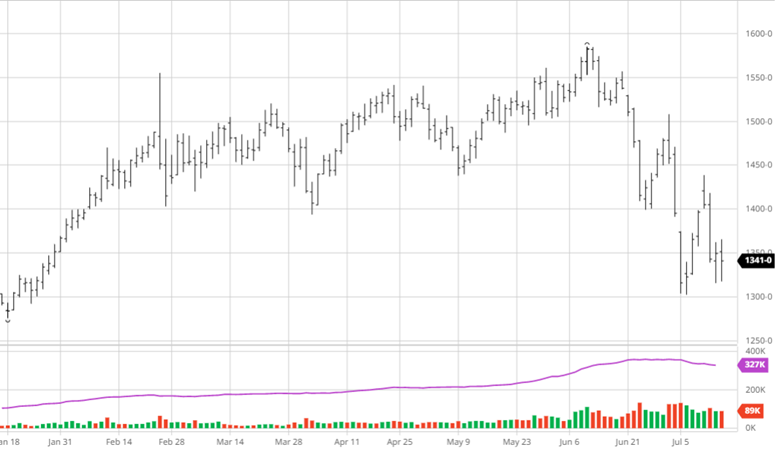

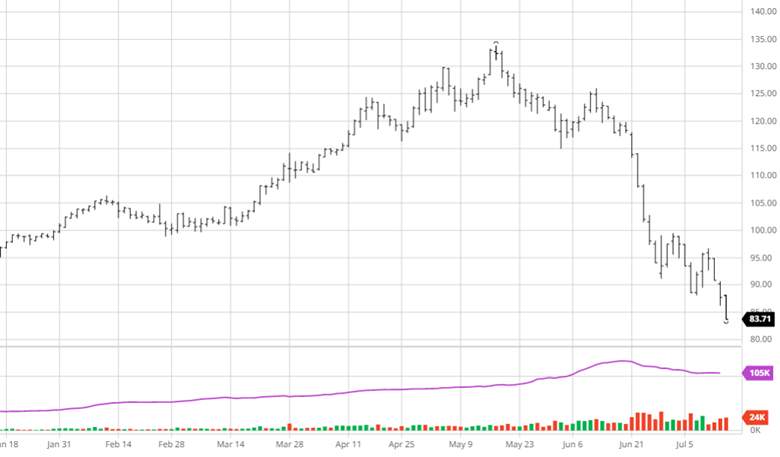

Equity Markets

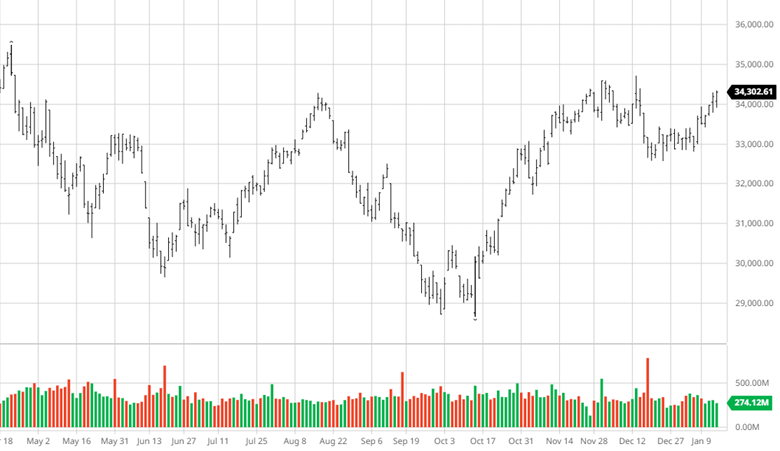

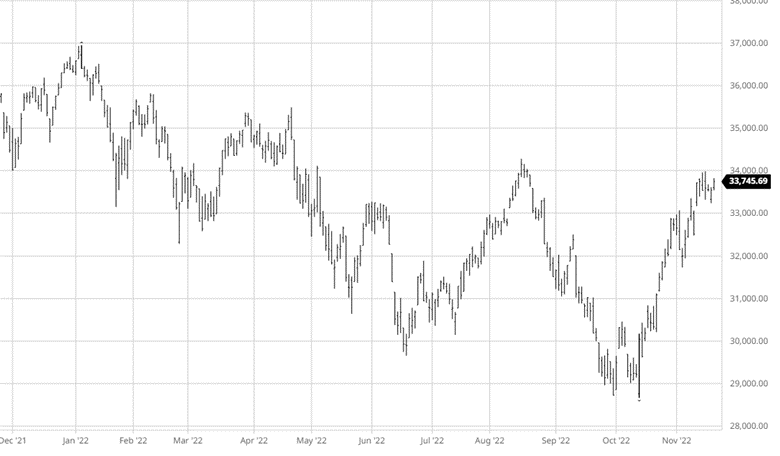

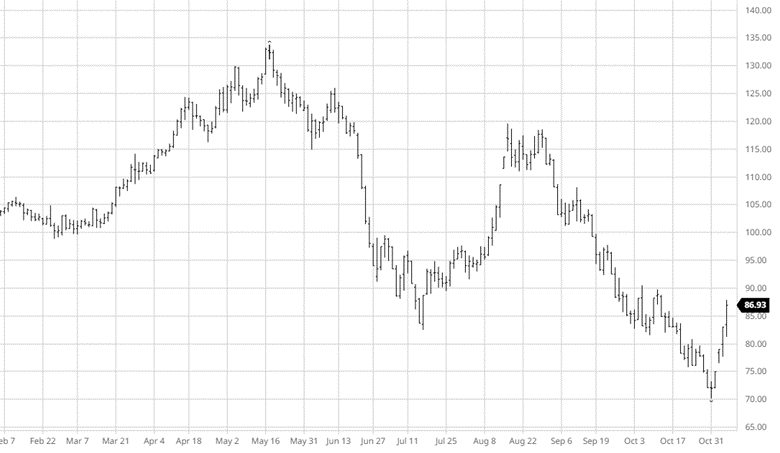

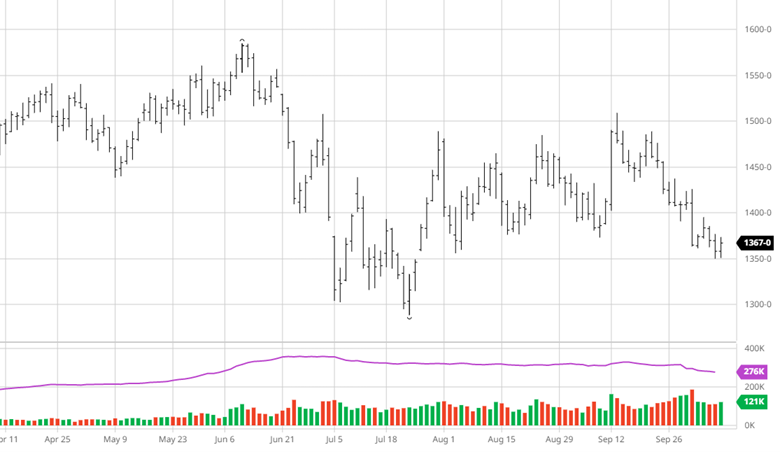

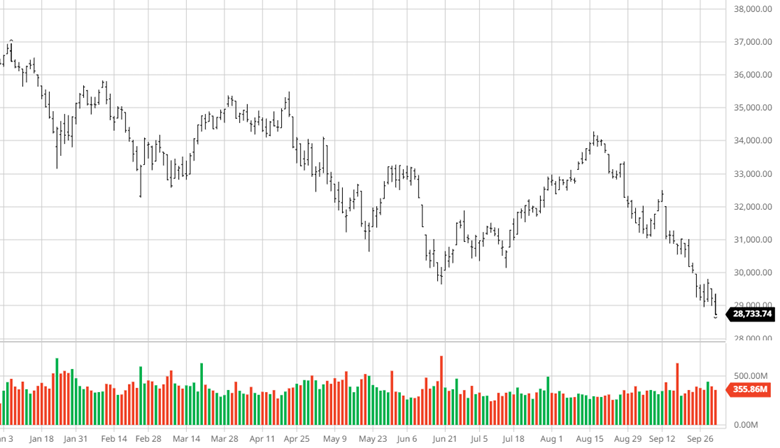

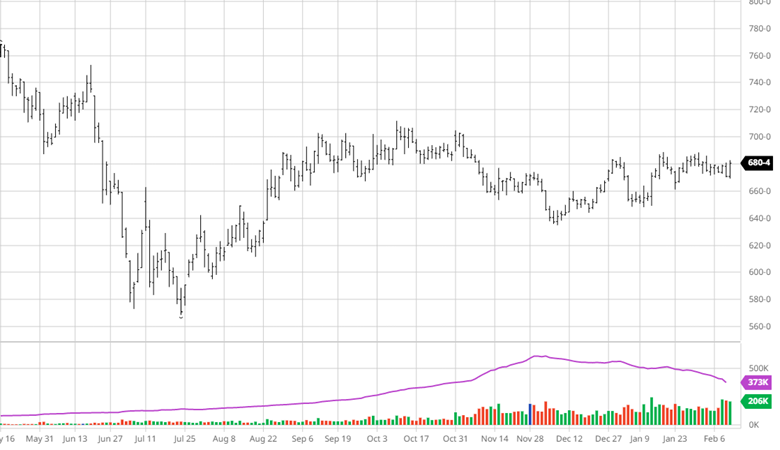

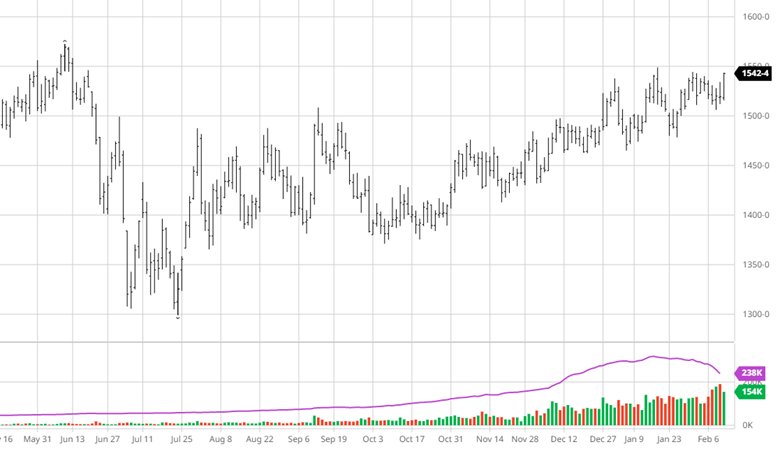

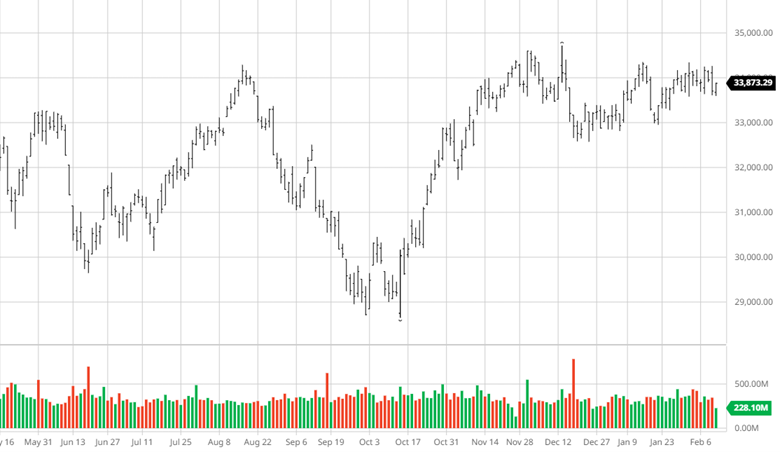

Equity Markets were down this week after having a good run following the Fed raising rates another 25 points. Earnings and AI were the storylines the last 2 weeks, causing big swings in many markets. Crude Oil also rallied this week after dipping down into the $72 range and Russia announced they were cutting production by 500,000 barrels a day in March in retaliation for international sanctions. Earnings moving forward will help give an idea if this rally can continue or if we hit a near term high.

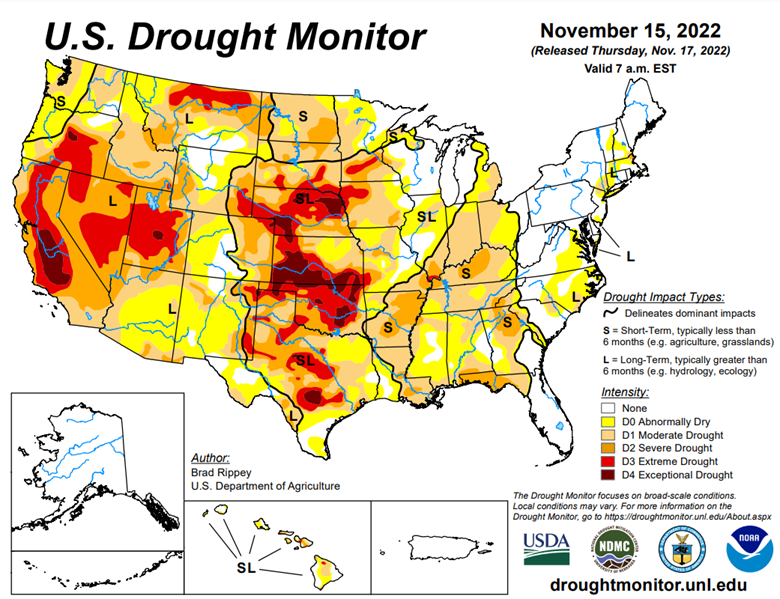

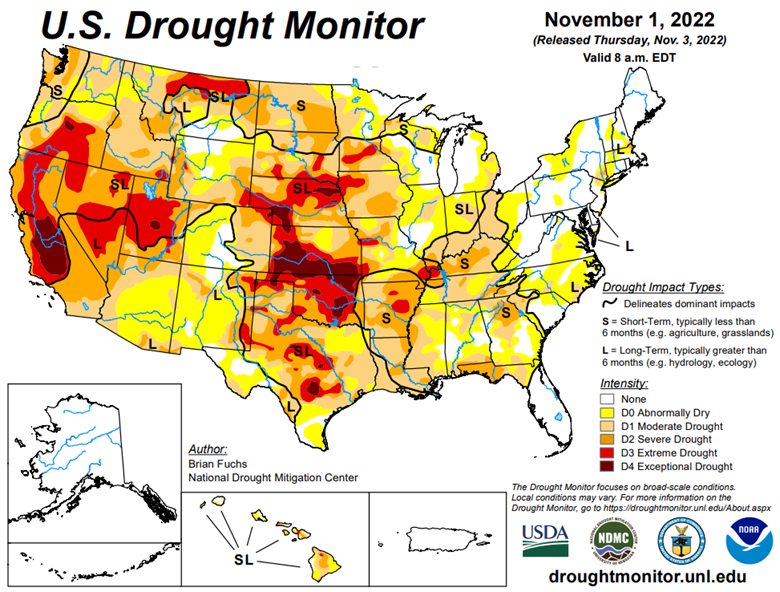

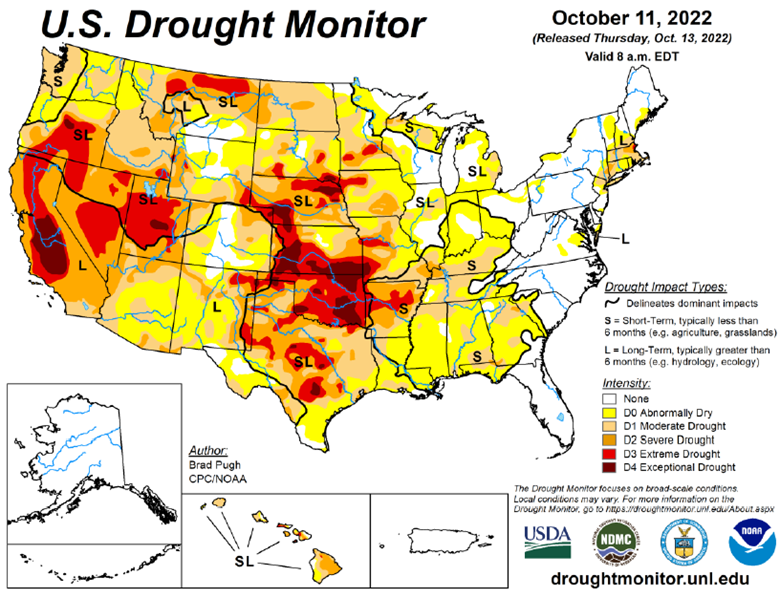

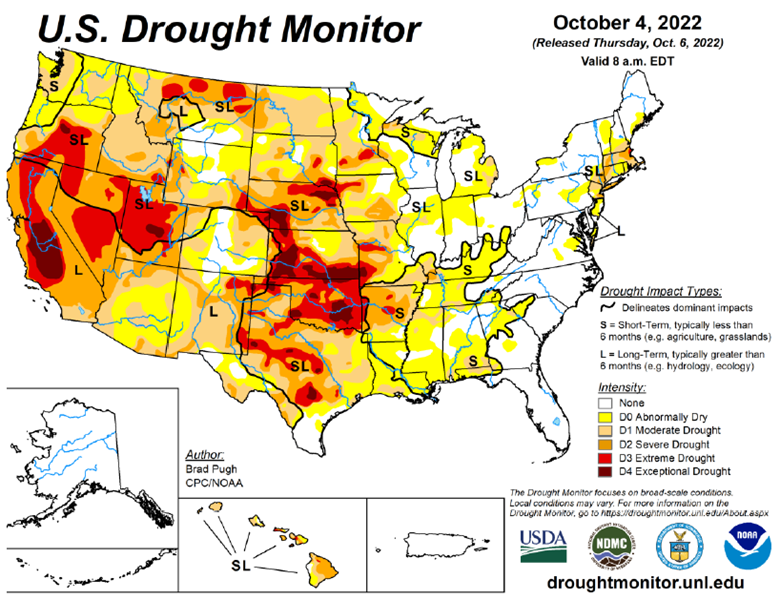

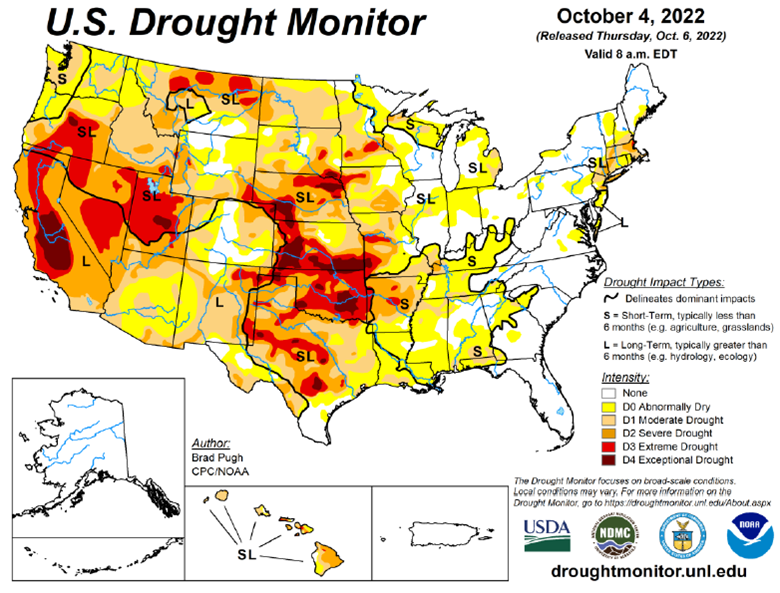

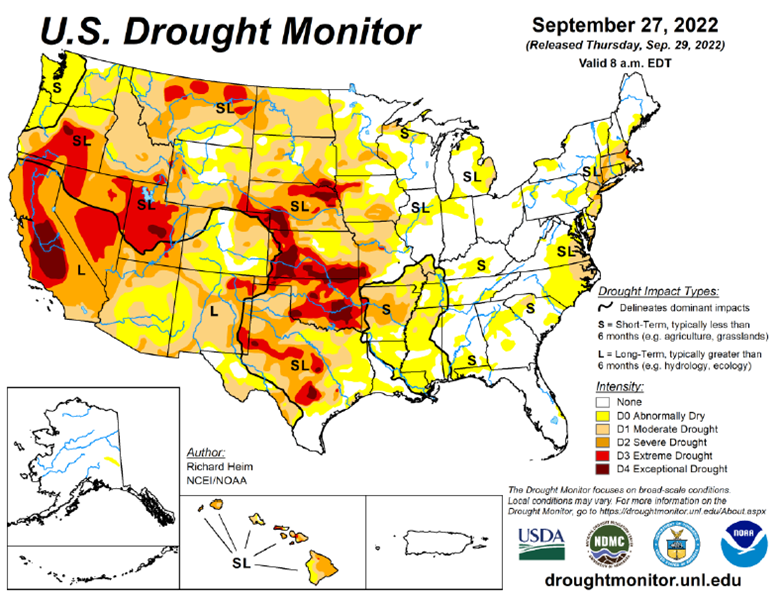

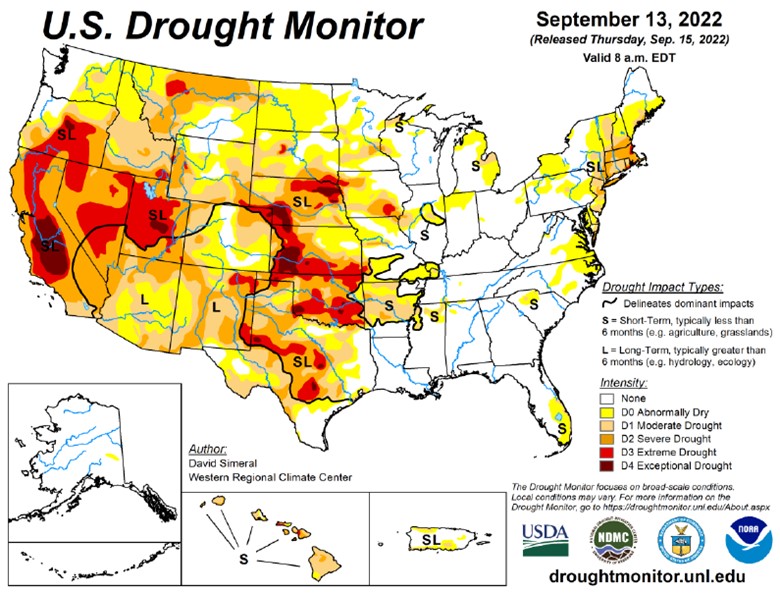

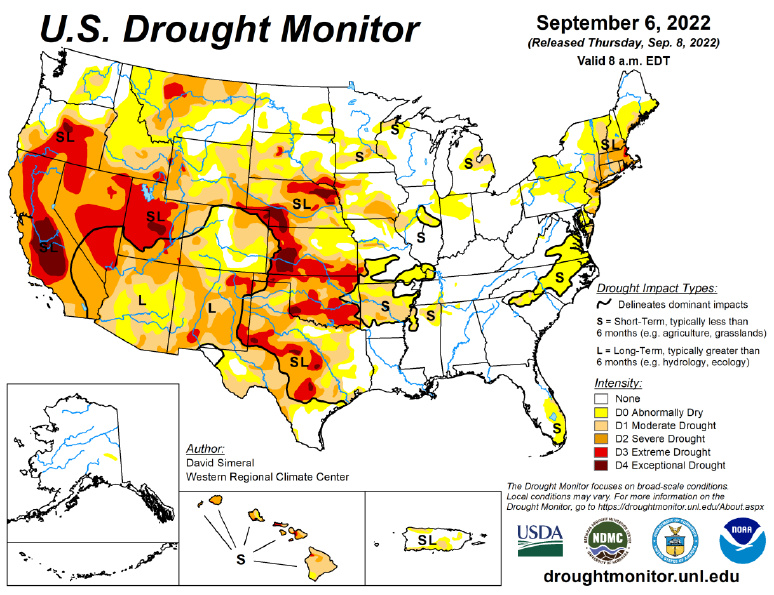

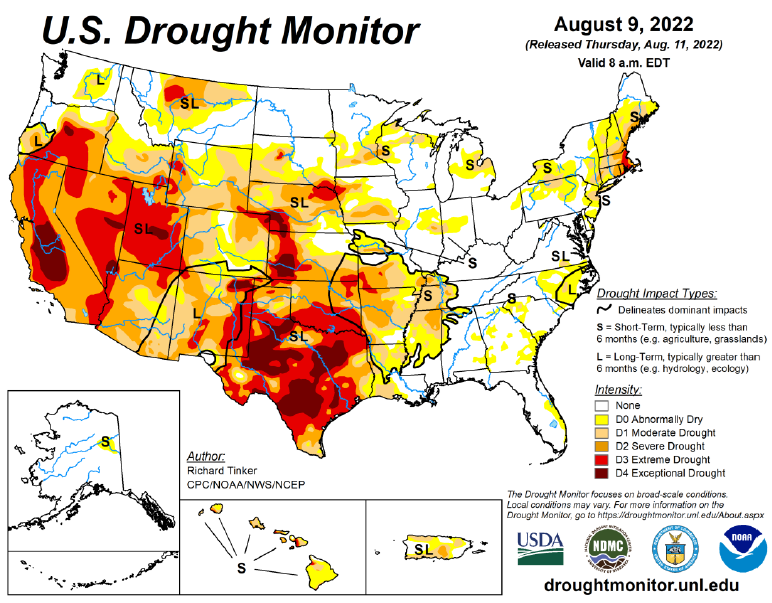

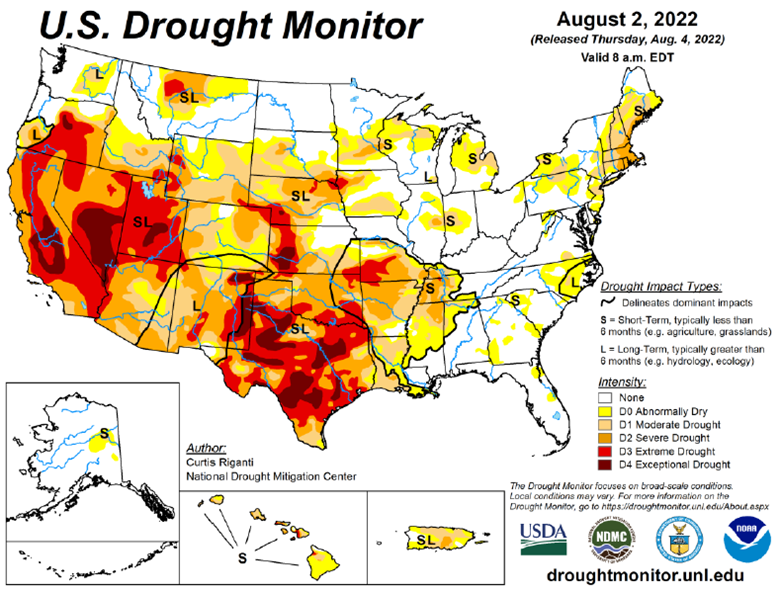

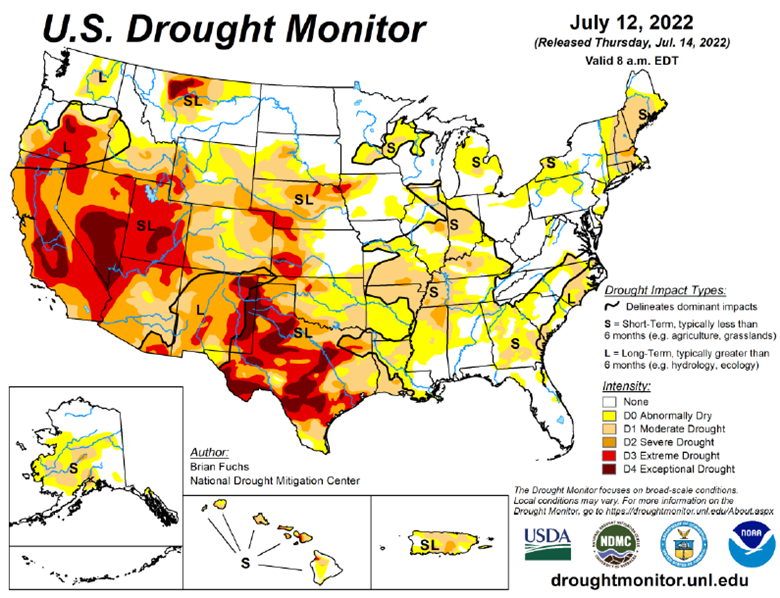

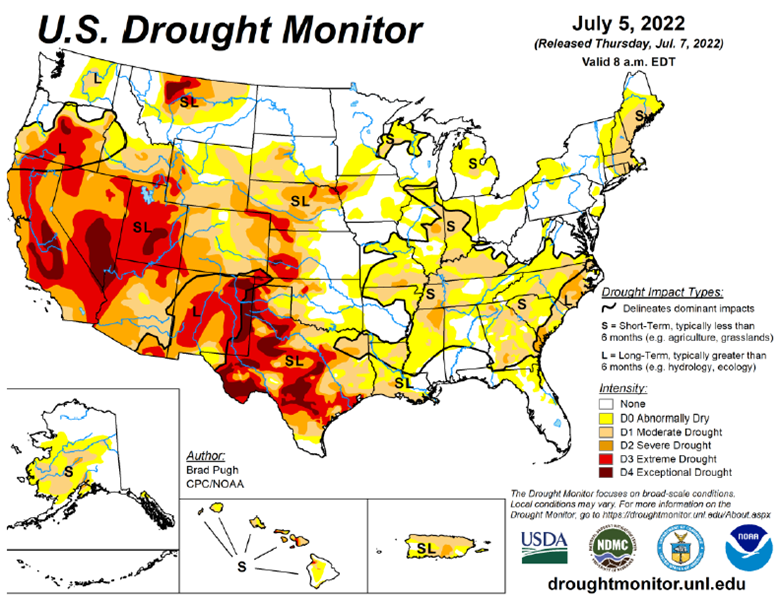

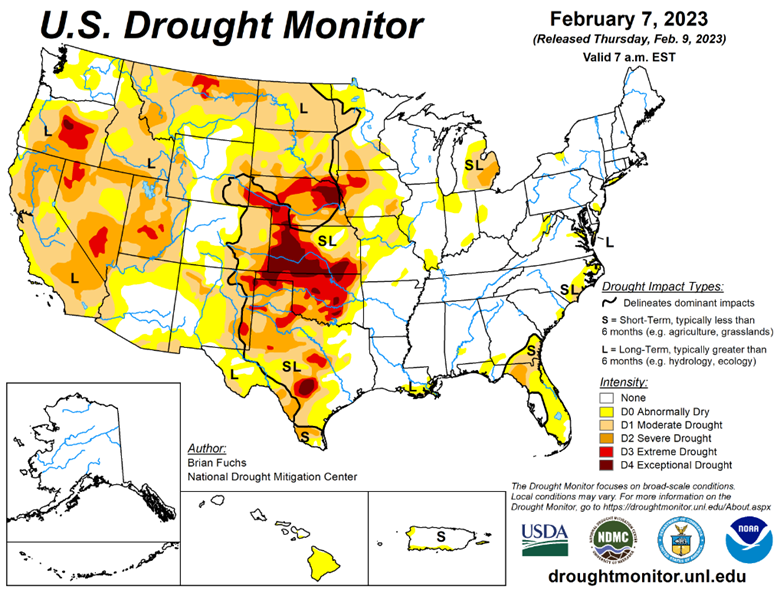

Drought Monitor

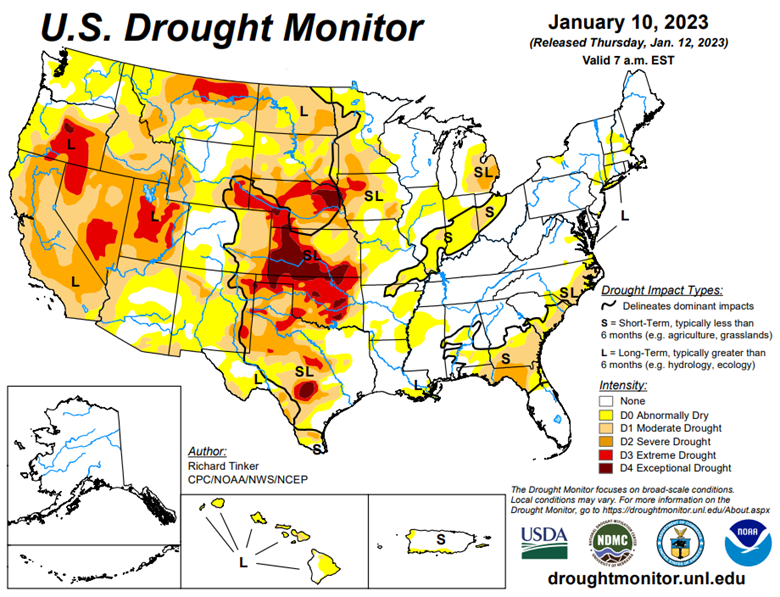

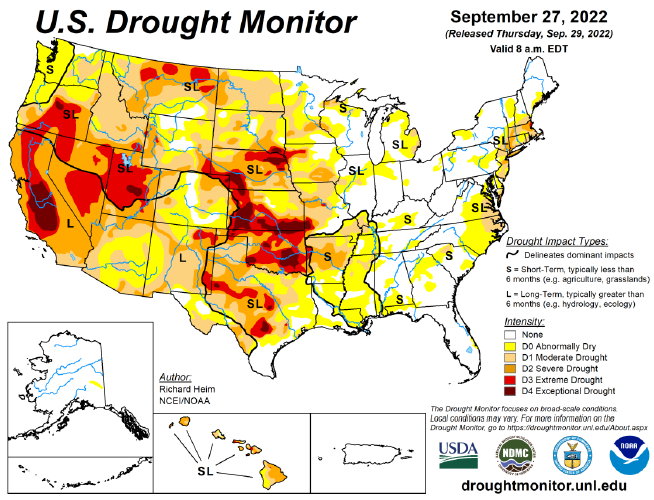

Eastern corn belt has gotten plenty of moisture so far this winter with the western corn belt needs more heading into the spring.

Podcast

With every new year, there are new opportunities, and there’s no better time to dive deeply into the stock market and tax-saving strategies for 2023 than now. In our latest episode of the Hedged Edge, we’re joined by Tim Webb, Chief Investment Officer and Managing Partner from our sister company, RCM Wealth Advisors. Tim is no stranger to advising institutions and agribusinesses where he has been implementing no-nonsense financial planning strategies and market investment disciplines to help Clients build and maintain wealth and reach financial goals since

Inside this jam-packed session, we’re taking a break from commodities, and talking about the world of equities, interest rates, tax savings, and business planning strategies. Plus, Jeff and Tim delve into a variety of topics like:

- The current state of the markets within the wealth management industry

- Is there a beacon of hope, or is it all doom and gloom for the markets?

- Other strategies to think about outside of the stock market and so much more!

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.