Corn was pretty flat on the week, but it did not lack volatility. The war in Ukraine and the constant news make for wild swings on unconfirmed reports such as peace talks and Russian demands. The volatility has caused many headaches, but the volume has decreased, showing that many traders are watching from the sideline and not trading volatile rumors that may or may not be true. The next month of weather will be important as some areas of the US are very dry and will need moisture heading into the spring. Corn export sales were above expectations this week, helping the bounce back Thursday.

Soybeans fell on the week as the news affecting beans is not solely out of Ukraine. South America has had better weather conditions the last couple weeks and forecasted ahead. While the drought conditions did plenty of damage to the crop early on, the improved conditions are good but not great to help out. Bean exports were within expectations this week as beans have traded relatively flat the last couple of weeks.

Wheat’s volatility continued this week as the war in Ukraine continued. Reports of peace/ceasefire talks have been in the news that seems to move markets whenever a new one is reported, but the volatility will continue until there is a resolution. There will still be massive fallout from this war as Ukraine’s infrastructure will be devastated, and sanctions on Russia will be large. Ukraine’s crop year drastically change, and it will be hard to get a full read on the damage until much later. Rain fell on some of the drier areas in the US that grow wheat, but the market did not seem to care. For now, the news will continue to be Ukraine and Russia.

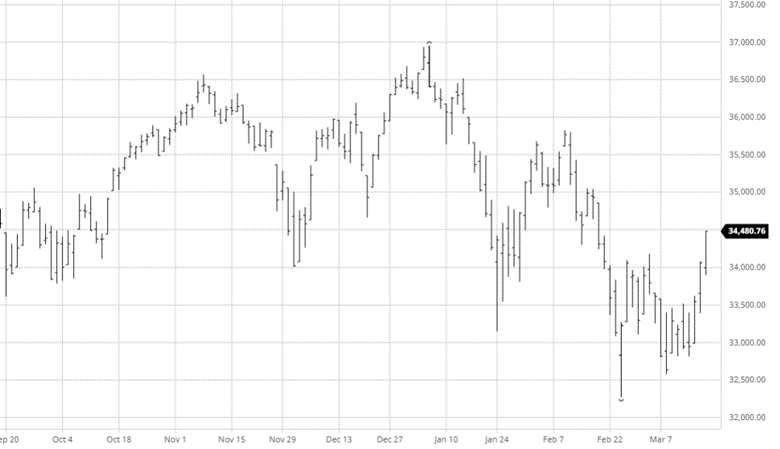

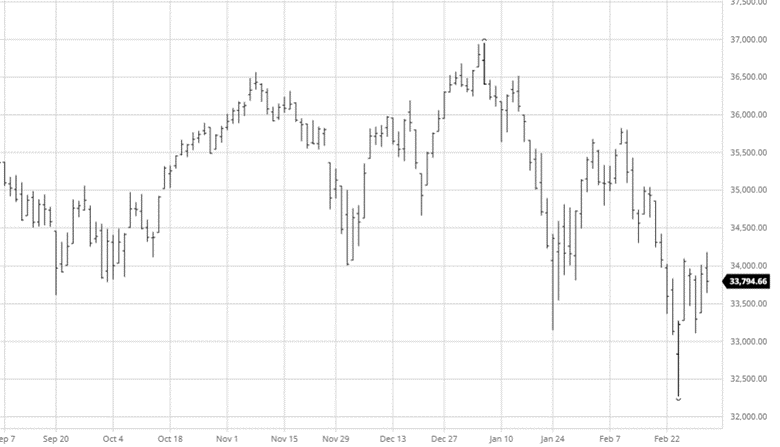

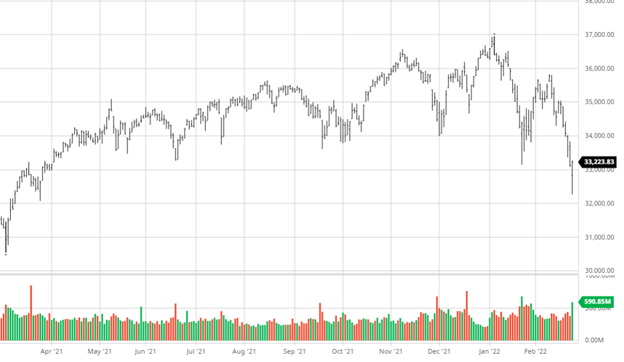

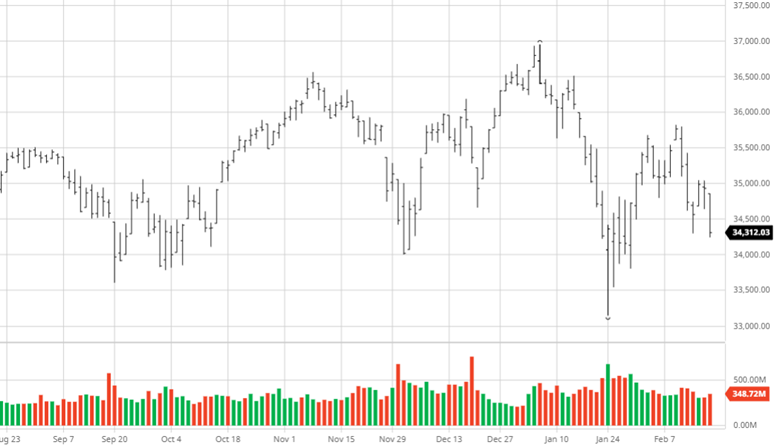

The equity markets rallied this week as investors aren’t sure if we bottomed but felt the market had fallen enough to be an excellent area to get back in. The fed decided to raise rates for the first time since 2018 raising it a quarter of a point. They also announced to expect six more raises as the year goes on to fight inflation. The market had already priced this news in, and after a short dip down, markets finished the day after the news higher. China has had a new round of Covid lockdowns, which is something to watch.

Tune in as biotech guru Dr. Channa S. Prakash discusses everything from Alabama football, genetics as one of the most extensive agricultural advancements, the most significant risk factors to feeding the world over the next 30-50 years, plus everything in between.

Why producing crop plants with a much gentler footprint on the natural resources will help feed the growing population. How 75% of the world’s patents in agriculture gene editing are coming from China. Understanding that trying to impose restrictions on our ability to grow food can be a considerable risk to agriculture. Listen to hear about these topics and more!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Corn made slight gains on the week with very volatile intraday markets. The Ukraine and Russian news continue to stay in the market and will likely dominate headlines until it ends. Other news worldwide is that South America got rains in southern Brazil and Argentina, with dry central and northern Brazil. Russian officials announced that they would suspend fertilizer exports through the end of the year, presenting a supply crunch across the world. This week’s USDA report was nonexistent in the markets as there were no surprises. As mentioned last week, Ukraine’s corn crop may not get in the ground as only 60% of seed is on farm; this will be important moving forward as world balance sheets get tighter.

Soybeans made small gains this week despite the wild intraday volatility. The USDA trimmed South American production again in this week’s report as they continue to baby step lower to what will be a smaller crop. World edible oil prices were up on the week pulling bean oil and soybeans higher. The Black Sea area’s worry and trade have affected the oils market, not just wheat.

Wheat fell hard this week with an expanded limit down the day with a small bounce on Friday heading into the weekend. All the short wheat positions that were getting run over had the opportunity to get out this week with the move down. However, the unknown in eastern Europe and China having its worst winter wheat crop on record means there is still upside with volatility. Friday’s gains were welcome to see after three days of large losses. The cash market will be essential to follow as it will help determine the fair market value.

The equity market fell again this week as continuing war, and another record inflation number was challenging for the market to figure out. While the market seems like it is struggling to make up its mind, there are pockets that are performing alright. The world economic outlook appears to be teetering, and trying to digest what to do with Russia will be a major decider.

Tune in as biotech guru Dr. Channa S. Prakash discusses everything from Alabama football, genetics as one of the most extensive agricultural advancements, the most significant risk factors to feeding the world over the next 30-50 years, plus everything in between.

Why producing crop plants with a much gentler footprint on the natural resources will help feed the growing population. How 75% of the world’s patents in agriculture gene editing are coming from China. Understanding that trying to impose restrictions on our ability to grow food can be a considerable risk to agriculture. Listen to hear about these topics and more!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Corn made large gains this week following wheat, but not with the same panic. While Ukraine is a major corn exporter, it is not on the same level of wheat. Corn’s moves will be similar to wheat as the news from eastern Europe, and war will be problematic for the world balance sheets. While it has not moved with the same vigor as wheat, the $1 gain in the last eight trading days shows the potential fallout from this spooks the market. It is hard to tell how many acres will be lost this spring, but it is estimated that only 60% of corn seed is on farms. How likely is it the rest will make it to the farms? We cannot be sure, but it certainly won’t be much more if the conflict drags out. We are still in an inflationary environment, and fund money is very much in these markets, so when they decide to take profits, we will see the same volatility we have of late.

Soybeans gained on the week but barely when compared to corn and wheat’s gains. Corn and wheat are major exports for Ukraine and Russia out of the black sea area where beans are not, so they are not immediately affected. South America’s weather outlook has improved but will not turn around the crop too much after its rough start. Soybeans will benefit from the corn and wheat stories, but they also have their own story to follow in South America.

The soft red winter “Chicago” wheat is in full-on panic mode, as you can see from the limit move days in the chart below. The war in Ukraine does not seem to be ending soon, and the sanctions on Russia will last and hurt their economy. Eventually, the market will figure out what fair value wheat is, but for now, with the potential for Ukraine to not do their regular care of the crop, it is on a ride. If Ukrainian farmers cannot apply the fertilizer they usually do, the crop will shrink by several metric tons and could be double digits. Ukraine is the 5th largest exporter of wheat globally; Russia is number 1; this conflict will have major ramifications in the wheat market for the foreseeable future.

This week, the equity market made decent gains as they have had a mixed trade the last few days. Jerome Powell said this week that it is all but a certainty that rates will be raised 25 basis points in the March meeting, lower than the 50 thought a few weeks ago before the war with Russia and Ukraine. Inflation has been bad the last year and will not improve soon with higher commodity prices across the board and Russian sanctions presenting a problem for some trade. Look for investors to focus on U.S. equities for the time being, as Europe and emerging market countries use Russia for a lot of their energy and could see issues with production and energy crunches.

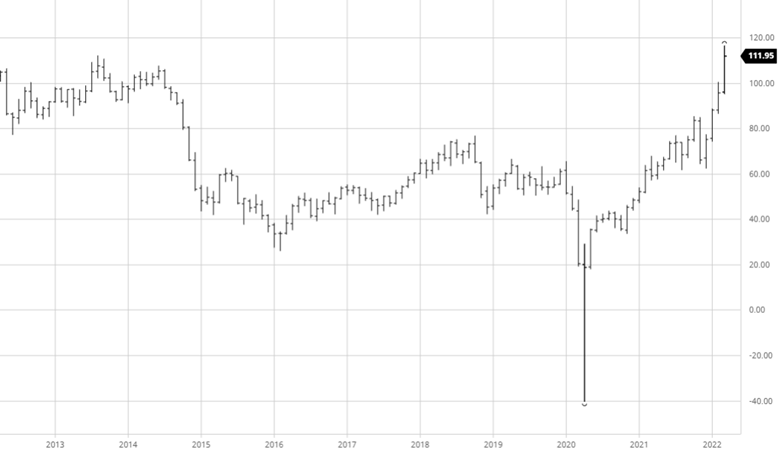

Crude moved higher this week as sanctions against Russia have made the future of Russian oil exports cloudy. The U.S. purchases roughly 600,000 barrels of crude from Russia a day, which does not help our already high gas prices. Crude still has room to go higher as ramping up production to make up for any lost oil takes months to do. If this conflict drags out, we will see elevated fuel prices through the summer and be a larger expense on the farm than the last few years going back to 2014. The 10-year chart below shows the current levels to 2014 to help you budget if you did not hedge your fuel prices.

Tune in as biotech guru Dr. Channa S. Prakash discusses everything from Alabama football, genetics as one of the most extensive agricultural advancements, the most significant risk factors to feeding the world over the next 30-50 years, plus everything in between.

Why producing crop plants with a much gentler footprint on the natural resources will help feed the growing population. How 75% of the world’s patents in agriculture gene editing are coming from China. Understanding that trying to impose restrictions on our ability to grow food can be a considerable risk to agriculture. Listen to hear about these topics and more!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

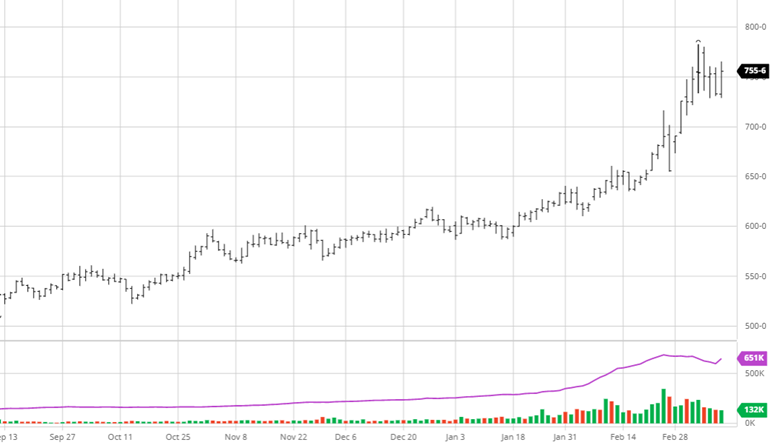

Corn was up a lot this week for similar reasons as wheat, with the Russian invasion of Ukraine pushing commodities higher. The conditions have improved in South America, but the length of trouble still caused large amounts of damage to the crop that we still do not know the depth of. The USDA Ag Outlook Forum came out with 92 million acres for corn, with some acres going to soybeans along with a 181 yield. A 181 yield would be a record crop, but with the supply chain issues, fertilizer prices, and availability of chemicals, many factors could affect yield if farmers can’t get all the inputs. Ukraine and Russia will be the market-moving news for now until we get a better idea of the long-term consequences. The February insurance price for corn is $5.89 ½. Friday’s early selloff will test the bulls for all markets.

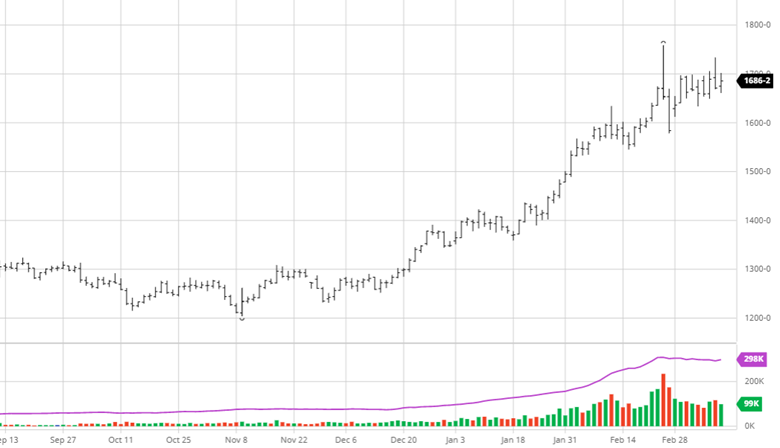

Soybeans gained on the week as the Russia and Ukraine news dominated headlines. Outside of this news, the weather outlook improved for South America that would have been bearish for bean prices if the eastern European turmoil was not going on. The USDA Ag Forum came out with an estimated 88 million acres with a 51.5 bu/acre yield for beans this year in the U.S., which is a bearish number but not surprising at these current price ranges. The November bean price had a more visceral reaction as it fell quickly Thursday off the highs having over a $1 trading range for the day, ultimately falling 36 cents to $14.51 ½. The February insurance price for beans is $14.33 ½.

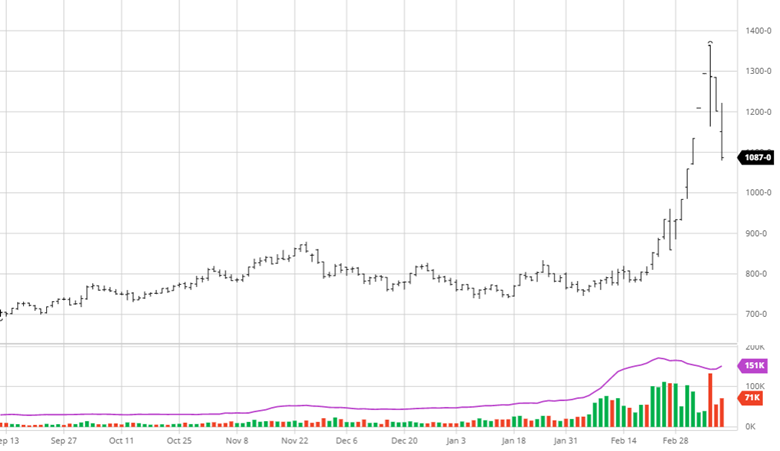

After days of large gains earlier in the week, wheat was limit up on Thursday after Russia invaded Ukraine. Ukraine is a major exporter of wheat and other agricultural goods as it is the 5th largest wheat exporter in the world, with Russia being #1. Not only is the world wheat supply threatened, but all trade in the Black Sea area will be affected, potentially only for a short period but disrupted, nonetheless. Russia accounts for more than 18% of the world’s wheat export and is a large oil and natural gas exporter, so any sanctions that hit their export economy could see ripple effects. This is only the beginning of this conflict, and wheat will be along for the whole ride, so you should expect volatility.

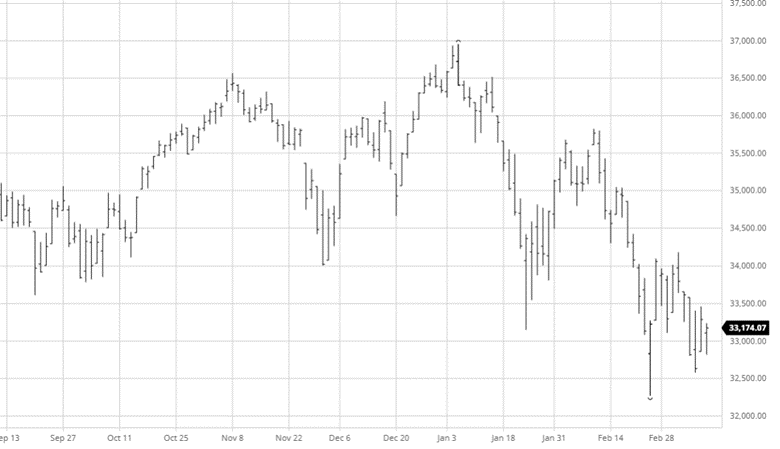

The equity markets continue to get crushed as, along with the struggles since November, we now have a war between Russia and Ukraine. This will make the Fed hesitant to raise interest rates, but as the bond rates have already risen, we are heading that way, whether it is a 25-point or 50-point bump. Tech stocks (NASDAQ) hit a 20% decline since November highs on Thursday before bouncing off the lows. Volatility will remain in the market as Russia remains a threat and China is a large unknown moving forward. Commodity prices have risen even more with oil nearing $100, so the inflationary pressure on the markets will not disappear any time soon.

Tune in as biotech guru Dr. Channa S. Prakash discusses everything from Alabama football, genetics as one of the most extensive agricultural advancements, the most significant risk factors to feeding the world over the next 30-50 years, plus everything in between.

Why producing crop plants with a much gentler footprint on the natural resources will help feed the growing population. How 75% of the world’s patents in agriculture gene editing are coming from China. Understanding that trying to impose restrictions on our ability to grow food can be a considerable risk to agriculture. Listen to hear about these topics and more!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

How Financial Institutions and Insurance Companies Play an Essential Role in Feeding the World

The cost of farming has grown over the years, which means financial institutions are amping up their reviewal process for loans and increasing insurance deductibles for protection to reduce their loss risk. What does this mean to supporting food production for the world? Well, as part of our “What It Takes To Feed The World” series, we are diving into critical agriculture sectors and bringing awareness to their roles in the food production cycle.

Financial institutions and insurance companies are the starting point in the process and are essential in providing the necessary funds to farmers on through to commercial entities. For farmers, they help finance EVERYTHING from the seed and chemical to hedge lines for farmers to help manage their price risk and everything in between. For commercial and end user entities, financing includes loans to build and maintain infrastructure and logistics to short term bridge loans to buy directly from farmers on to their own hedge lines of credit to support carrying of positions both pre and post harvest.

What financial and insurance options are available to the agriculture industry, and how are they beneficial to farmers, commercials, and end users? We’ll discuss the answers to these questions and more below.

Farmer Direct Loans

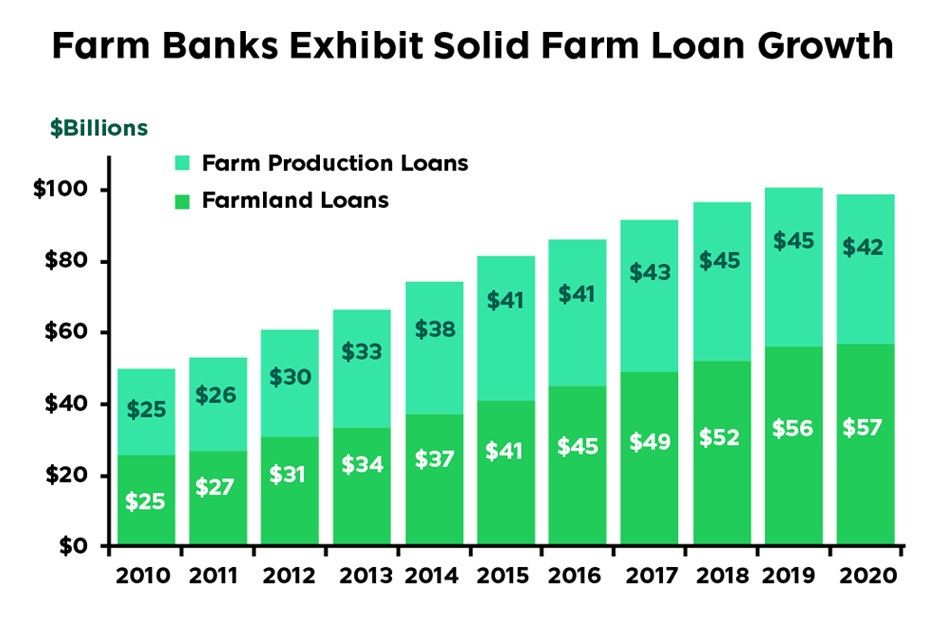

Farm direct loans are loans that the government makes available via the Farm Service Agency, while banks provide similar farmer direct loans. In 2021 the FSA reported loan obligations of $6.67 billion. Meanwhile, in 2020, U.S. farm banks loaned $98.6 billion. The American Bankers Association defines farm banks as banks whose ratio of domestic farm loans to total domestic loans is greater than or equal to the industry average. These amounts show just how much money is needed to produce the U.S. crop each year before farmers even harvest and sell the crop. These loans range from rent payments to fertilizer costs to machinery. But farm banks aren’t just offering loans to the agriculture sector. In 2020 total bank lending reached $174 billion in farm and ranch loans (including the $98.6 billion). These banks play a significant role with billions in small farm loans and even microloans. Small farm loans are less than $500,000, and microloans are less than $100,000. These two categories alone totaled over $55 billion in 2020.

Hedge Margin Lines

Banks also help finance hedge margin lines to help farmers manage their price risk. By financing the hedge lines, banks allow farmers to place hedge positions in a brokerage account, protecting against adverse price movements that could lessen the value of their crop. When banks loan out money, they expect to be paid back; hedge credit lines are a tool banks use to help support the farmer being able to do so. If your bank is NOT willing to extend a hedge line – please give us call!

By financing hedge margin lines, banks support the farmer and themselves. With loans comes default risk and hedging is one tool to help mitigate the price risk that ultimately will be how the farmer pays back the loan.

Banks and the Rest of the Sector

There’s no question that banks are involved in the food production supply chain. When you think about it, commercials, end-users, and other units that touch grain utilize bank loans to enhance their businesses. Like feed yards and elevators, end-users use banks to improve their infrastructure by adding more storage or drying systems, using short-term loans to purchase grain and make other improvements to their business. These improvements ultimately improve the efficiency of the entire system and potentially lead to reduced costs of the final product, which helps the end consumer, people. Just like improvements to city and towns infrastructure are necessary, through the support of bank financing, these improvements are necessary to the health of the agriculture industry’s infrastructure.

Farming is not getting any cheaper, and more capital is required to produce excellent crops year after year. Banks’ loaning capacities play a major role already, but if we are going to keep up with growing demand in a growing world, their role will be even more critical going forward.

Crop Insurance

Crop insurance brings continuity to the industry year-over-year as the ups and downs of weather and prices can cost farmers millions of dollars if unprotected. There are two types of insurance for major field crops: yield-based, which pays an indemnity (covers losses) for low yields, and revenue that ensures a level of crop income based on yields and prices.

Insurance offerings and prices vary on where you are located and your land, but like other forms of insurance in your life, it is better to have it and not need it than need it and not have it. While the listed above are the main types of insurance, others can be purchased, like drought insurance for pastureland and hail insurance if your crop gets damaged by an ice storm. These are more specific to your geographic location but play an essential role.

Like banks, insurance companies help with the continuity of the agriculture sector. These companies along with government subsidy programs, provide the opportunity to continue farming when disaster strikes and threatens the financial stability of a farm.

How RCM Ag Services Partners Financial Institutions & Insurance Companies

For our Farmer Direct customers, RCM Ag Services partners with banks and insurance companies to provide our mutual customers daily expert market knowledge and advice. We are firm believers that the long term health and growth of our local farming communities requires a team approach that starts with the farmers and their banking and insurance teams.

For our commercial and end user customers, we are focused on evaluating profit margins and the cost of capital for managing the current and futures market risks. Our Ag Services team is working directly with lenders, 3rd party credit suppliers, as well as USDA government programs to support the long-term financial health of the commercial business sector.

Along with market knowledge, our brokerage services allow us to establish hedge accounts that banks can fund with a credit line, as discussed above. Our brokers have over 150 years of combined experience in the market that helps them provide hedge advice that is customized to each operation, not cookie-cutter advice. Take advantage of these benefits and call one of our knowledgeable ag specialists today at 888-875-2110 or email agsupport@rcmam.com

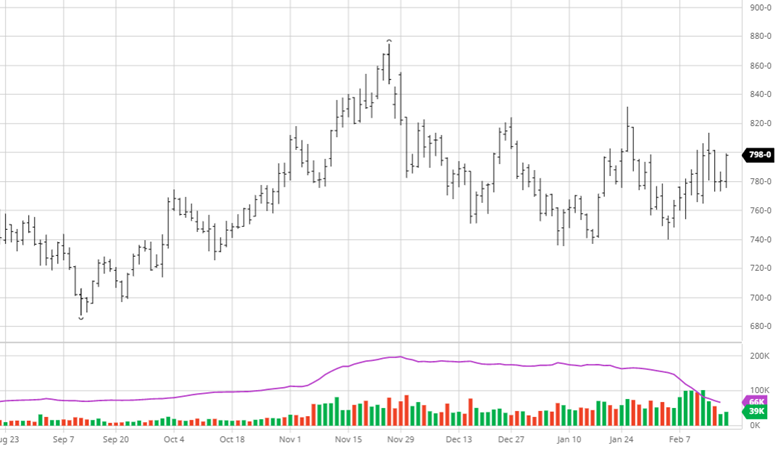

Corn made small gains on the week as grains did well across the board. The forecast for South America can’t seem to make up its mind switching back and forth on rain amounts. Argentina has consistently had rain in the forecasts, but what parts of the country and the amount has been inconsistent. Exports were better this week than last, but nothing crazy; potential conflict in Ukraine and further issues with the South American crop could see those numbers pick up soon. The markets are not open for President Day on Monday the 21st, so there is more time to develop around the world. Based on the Dec ’22 futures for corn after today, the February insurance price is $5.84 ¾.

Soybeans were up slightly on the week but have been relatively flat (relative to other weeks) the last two weeks, as you can see in the chart below. The continued weather issues in South America and the Russia v Ukraine possible invasion have been the movers for beans just like corn and wheat. Bean exports this week were the best of the group, with a flash old crop sale being announced on Thursday. We have seen private estimates continue to roll in for production in South America and what to expect this year in the US. The USDA Ag Outlook Forum will start next Wednesday, and we should find out what they are expecting for the year ahead and how the US will affect balance sheets. The insurance price for beans is $14.22 ½.

Wheat has been on a roller coaster the last two months with the ups and downs and uncertainties around Russia and Ukraine. A Russia invasion would be bullish for wheat as countries would shy away from trade with Russia, and Ukraine would stop exports as they try to keep Russia at bay. The Black Sea is a major world trade region. This conflict could lead to potential stoppages, shortages, or even a possible blockade in the region that would cripple a major trade corridor. Keep an eye on this developing story as it could have potential long-term consequences as the US has also threatened Russia with sanctions (they don’t seem to be fazed at all by Washington’s threats).

This week, the equity markets fell as confusion and concerns of post-Olympic wars between a few countries inch closer. Russia was reported to have changed their mind on invading Ukraine, only for that news to switch to them adding troops at the border. China invading Taiwan post-Olympics is also a possibility as that has seemed to be forgotten as the Russia news took over the market. Earnings season has been mixed with losers and winners in all sectors as inflation has begun to show up more in guidance for the year ahead.

Tune in as biotech guru Dr. Channa S. Prakash discusses everything from Alabama football, genetics as one of the most extensive agricultural advancements, the most significant risk factors to feeding the world over the next 30-50 years, plus everything in between.

Why producing crop plants with a much gentler footprint on the natural resources will help feed the growing population. How 75% of the world’s patents in agriculture gene editing are coming from China. Understanding that trying to impose restrictions on our ability to grow food can be a considerable risk to agriculture. Listen to hear about these topics and more!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

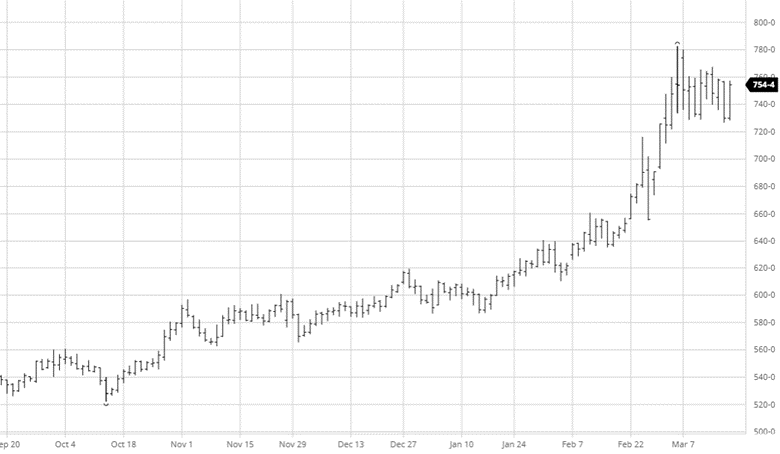

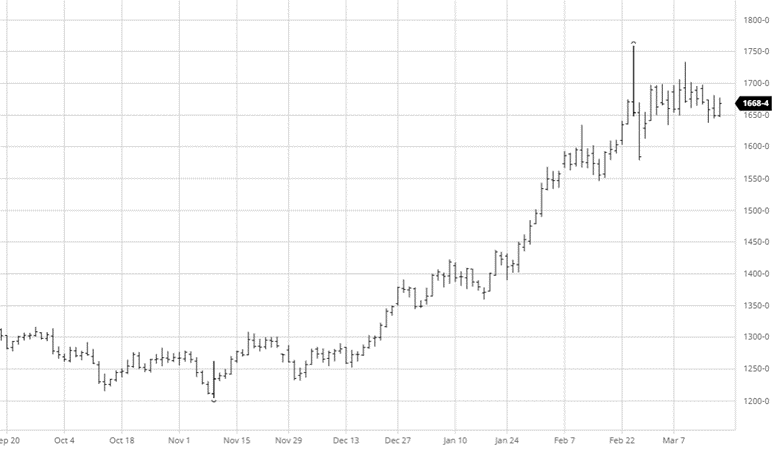

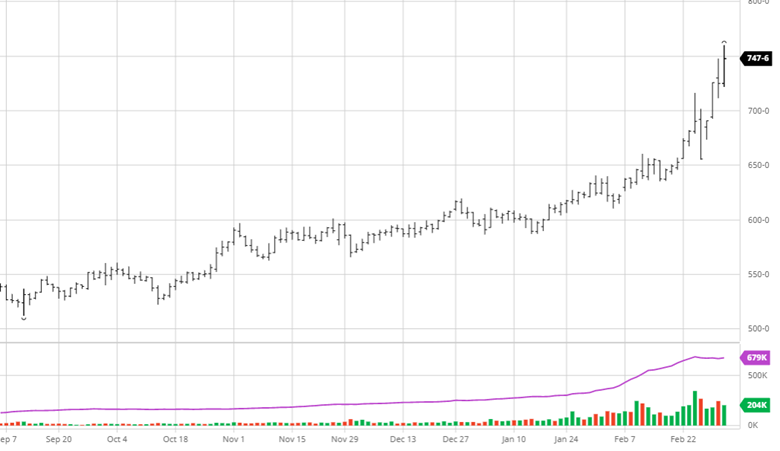

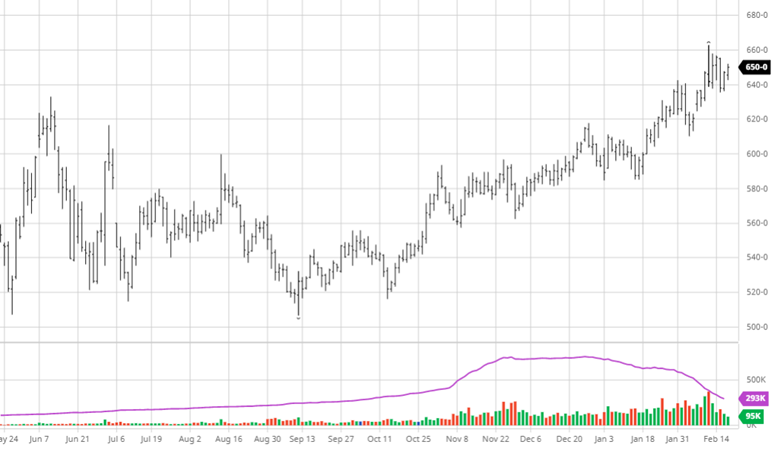

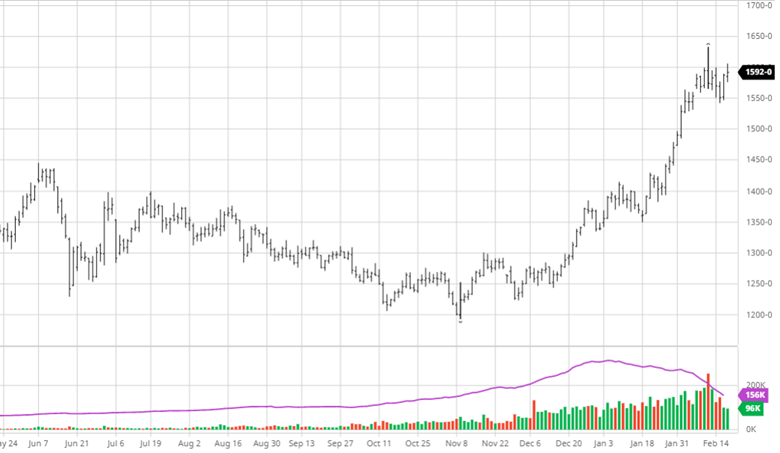

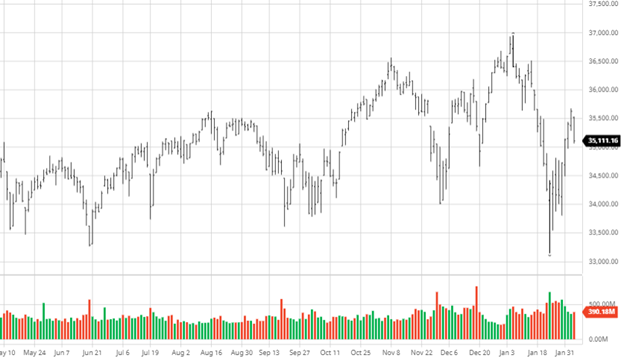

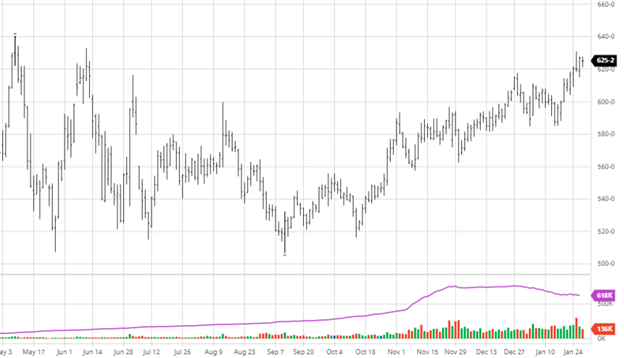

The numbers came in above trade estimates but were lower than the previous months’ report. The USDA kept the U.S. ending stocks at 1.540 billion bushels and lowered the world ending stocks to 302.22 million tonnes while reducing Brazil’s yield. Following the report, it came off the highs for the day before roaring back up to end the day. Thursday’s trade was interesting as halfway through trading, the markets did a 180-degree turn and fell lower on the day after being sharply higher across the board for a large intraday range. This was brought on by producers selling and speculative positions taking profits. The large intraday volatility has not been as present in the market as this summer, but Thursday’s trade is a sign that volatility should be expected at these price levels. The USDA’s numbers for Brazil and Argentina are still above what private analysts and CONAB are reporting. The market seems to be on the analysts’ side when it comes to the struggles in South America. The weather outlook remains the same for the trouble areas as it will be hot and dry in the same areas and wet in the same.

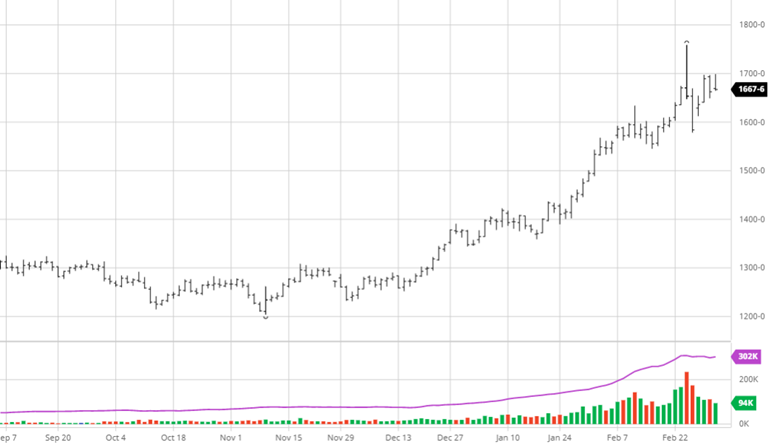

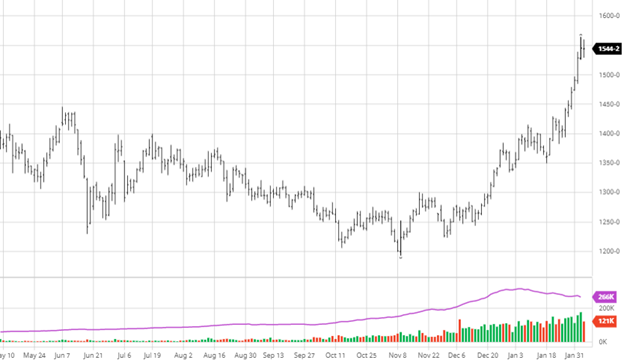

Soybeans continued their run higher despite Thursday’s pullback. The most significant change in the report came to soybeans as the USDA lowered Argentina’s production by 1.5 million tonnes and Brazil’s 5 million. As much of a correction that the USDA made, some analysts still feel these are too high, and their crop will continue to get smaller. With the continued hot and dry weather in Argentina and southern Brazil mixed with the wet harvest in northern Brazil, mother nature is not doing South America’s crops any favors. CONAB released their estimates on Thursday and were well below the USDA numbers, so it’s safe to listen to their numbers and analysts over the USDA right now, it would appear. The two-year chart is below so that you can see the journey of how we got to this point with the great run since early November. Thursday produced the same wild volatility as corn, which saw a 67 ½ cent range while falling off the highs.

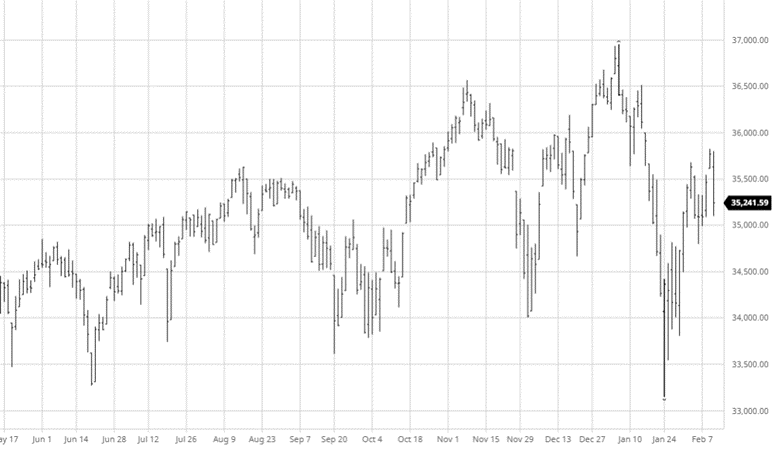

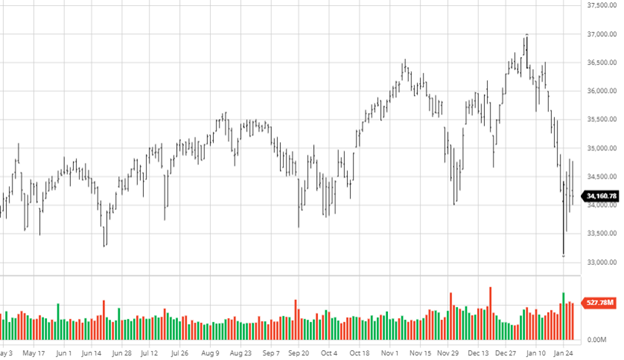

The equity markets have been quieter lately, with small gains on the week, but the uncertainty of what lies ahead remains. The inflation number came in at 7.5% year over year, the highest increase since February 1982. With inflation sticking around and treasury yields jumping, the 10-year treasury topped 2% for the first time since August 2019; it is understandable why the markets have the jitters. Will the market hang out where it is, retest the lows, or try to continue to claw back its losses from January? The market can’t figure it out, so I won’t try to predict for you.

Tune in as biotech guru Dr. Channa S. Prakash discusses everything from Alabama football, genetics as one of the most extensive agricultural advancements, the most significant risk factors to feeding the world over the next 30-50 years, plus everything in between.

Why producing crop plants with a much gentler footprint on the natural resources will help feed the growing population. How 75% of the world’s patents in agriculture gene editing are coming from China. Understanding that trying to impose restrictions on our ability to grow food can be a considerable risk to agriculture. Listen to hear about these topics and more!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Corn suffered small losses this week, going a different direction than beans. Private estimates of the South American crop are consistently lower than the USDA’s last estimate, and we should see an adjustment on next week’s USDA report. The Chinese’s cancelation of 380,000 tonnes of corn was a drag on the market on Thursday. One cancelation is not the end of the world; it happens, but should we see a trend develop that could damper the bull sentiment right now. The driest areas of South America will continue to dry over the next couple of weeks, hurting their crop in those regions. Private estimates think that Argentina’s corn yield could be 43.5 million metric tons, while Brazil’s could be 112 MMT. These are well below the last USDA report’s numbers, so next week will be interesting to see how much the USDA adjusts their estimates.

Soybeans continued to move higher this week as the South American weather issues will probably significantly impact the soybean crop. The continued heat and dry weather will continue to stress the crop like corn. The market can’t go up every day, no matter what it seems like; the closing off the highs the last two trading days suggests the market may want to take a break until there is more news. Brazilian producers are still not selling, which has interior cash bids competitive with exporter bids. With this playing out in Brazil, the U.S. could see some more business as a result. Especially if China steps in and makes purchases out of the Pacific Northwest, keep an eye on drought conditions around the U.S. even though we are well out from planting as we have seen drier than normal weather in some growing areas to this point of the year.

Equities have made a strong rebound off the lows until Thursday’s struggles following some bad earnings report lead by Facebook’s (now Meta) major fall. Amazon posted a good quarter which may give investors some relief that Facebook’s problems were their own and not market wide. The bounce was nice to see from an investors point of view as a correction seemed to be done, but guidance from many companies has not been as growth friendly looking forward as the last year. Volatility may stick around for a while so do not expect the markets to recover as quickly as they fell.

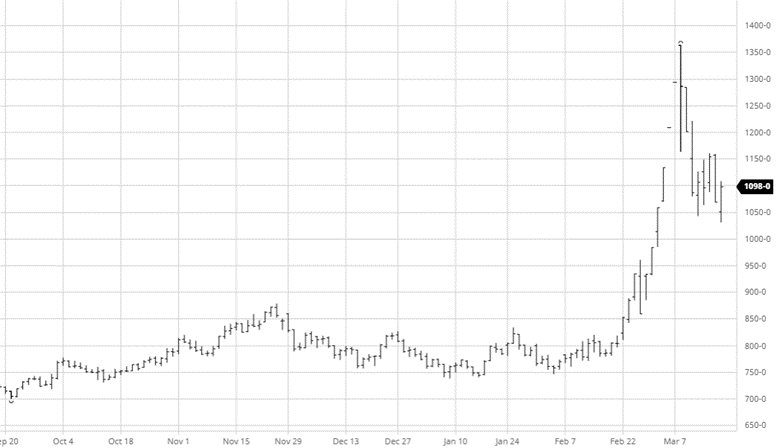

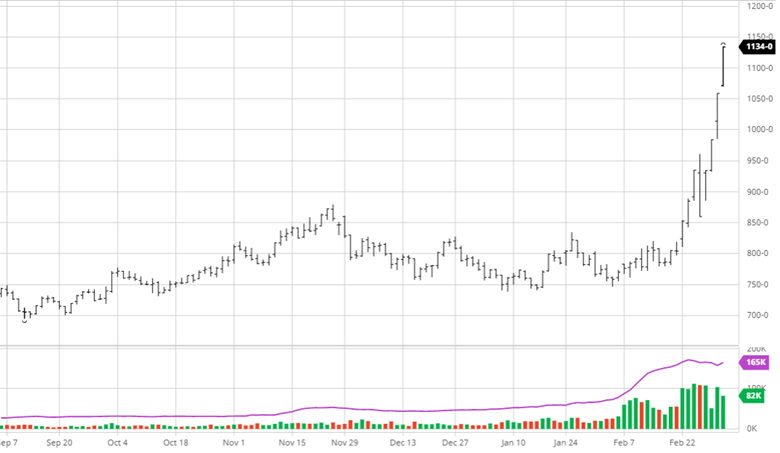

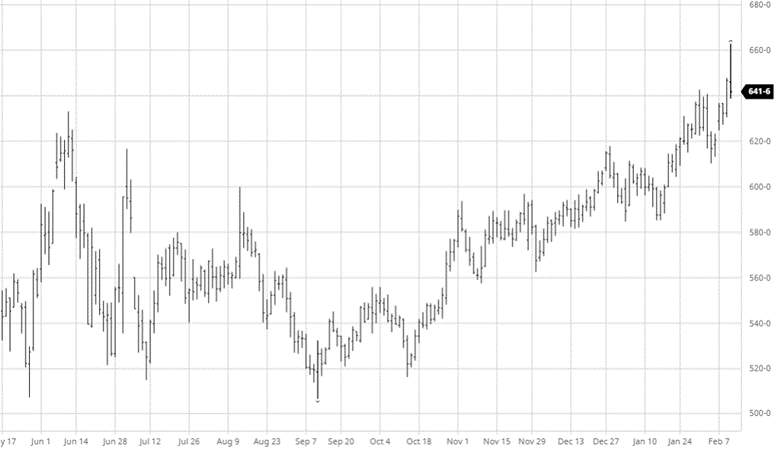

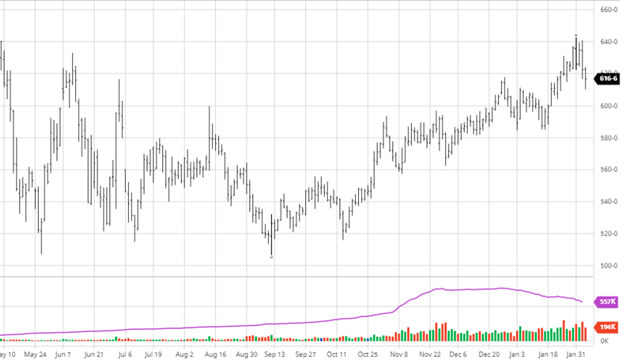

Crude hit $90 this week for the first time since 2014, while Natural Gas also rose to over $5.500 before dipping back below $5 this week. Crude continues its move higher as OPEC+ does not plan to expand production while consumption remains strong. This is a classic higher demand without more supply price raise over the last two months, and many analysts see $100+/barrel as a possibility this spring. Higher fuel prices will affect farmers’ bottom lines as fuel expenses and shipping for other chemicals and fertilizers will be much higher this year on top of higher input costs. (5-year chart below for reference)

The February WASDE report will be released next Wednesday, February 9. This will be the primary driver of the week after weekend weather has its say in the market on Monday. This is not usually a major market mover, but it never hurts to be well-positioned and ready before a report.

Podcast

Tune in as biotech guru Dr. Channa S. Prakash discusses everything from Alabama football, genetics as one of the most extensive agricultural advancements, the most significant risk factors to feeding the world over the next 30-50 years, plus everything in between.

Why producing crop plants with a much gentler footprint on the natural resources will help feed the growing population. How 75% of the world’s patents in agriculture gene editing are coming from China. Understanding that trying to impose restrictions on our ability to grow food can be a considerable risk to agriculture. Listen to hear about these topics and more!

As of 2022, there are 7.9 billion people in the world, which is anticipated to hit 10 billion by 2050

Did you know that by 2050, the world is expected to feed almost 2 billion more people than we do today? As the global population continuously rises, a significant amount of food will need to be produced over the next 30 years.

But before you get to overwhelmed with that thought, it’s imperative to know that the need for more production creates opportunities. In fact, in 2020 alone, 19.7 million jobs were related to the agriculture and food sectors. We cover these areas in this What It Takes To Feed the World infographic. So, let’s take a closer look into how each of these categories work together to help pave the way to feeding 25% more of the population over the next couple of years. Here’s everything you’ll need to know:

Download the Infographic

FINANCIAL INSTITUTIONS / INSURANCE

Due to inflation (we cover farm inflation here) and superior advancements in farming technology (seed, equipment, etc.), the cost of doing business is extraordinary.

As a result, banks and other financial institutions have become the pillar of the agriculture community. From financing farmers, purchase of seeds and chemicals to providing insurance to protect the farmers on through to commercial lending and trade finance programs; without banks, agriculture, as we know it today, does not exist. As a standalone example, consider that in the U.S. alone, during 2020, farm bank’ lending was $98.6 billion despite the global economic slowdown. As the demand to produce continues to grow, there is minimal question that the need for capital will grow along with it.

Source: Federal Deposit Insurance Corporation & American Bankers Association Analysis

SEED / CHEMICAL:

Before the farmers can get to work, they need seeds and, subsequently, fertilizers (watch our fertilizer forecast here) to reach the full potential of every acre of land. From the genetics to the production to the distribution companies, one could argue that continued innovation of this industry is vital to the future of agriculture.

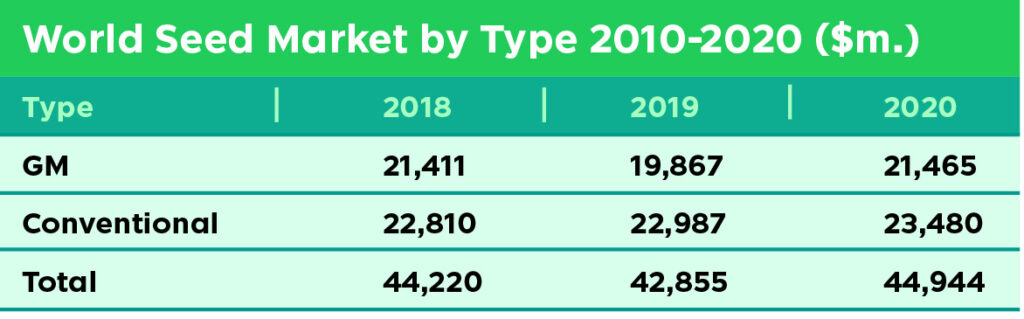

In 2020, the commercial seed market alone reached an estimated $44.9 billion in annual revenue. With the global pressure on to produce, the world can no longer afford to have underperforming years of production, placing even more pressure on this sub-sector of agriculture to continue to develop treatments on both the organic and GMO sides (watch The Future of Feeding the World Podcast here).

Source: IHS Markit – @2021 IHS Markit

EQUIPMENT

With the growing demand for food-producing land due to the world’s growing population, advances in technology have seamlessly made the farming process more efficient, profitable, and undoubtfully safer. Modern farms and agriculture equipment have significantly evolved by incorporating sophisticated technologies like sensors and GPS to driverless equipment with new autonomous machinery.

These enhancements to heavy equipment are essential to farmers, allowing them to no longer apply certain things uniformly, like fertilizing or watering the field. But instead, farmers can use minimal effort to target specific areas of their fields. Let’s look at some of these added benefits due to technology:

Farmers have higher crop productivity.

There is a reduction in the overuse of water, fertilizer, and pesticides.

The price of food production is at a lower rate due to less manual labor.

Improves the safety of farmworkers and machine operators due by incorporating the use of drones and various software. Check out this podcast with Dr. Steve Irwin on technical platforms here.

Groundwater and rivers are experiencing less runoff of chemicals.

Undoubtedly, innovation of this business sector will continue to evolve and play a major role in the necessary production increases ahead.

GRAIN PRODUCERS

One hundred fifty years ago, work was hard for grain producers, but the job was simple – till the land, plant the seed and let mother nature do her job. As time passed and our global population grew and the demand for our arable land has grown exponentially; all of which, leads to the grain producers of today having the most important job in the world.

The work of the few is to feed the many. Since the post-WWII era, the number of farms has steadily been reducing, placing even greater pressure on those in production areas to continue managing their operations, focusing on profit margins, and working the inherently volatile world of commodity prices.

Imagine a 5,000-acre farm producing trendline yield corn of 180 bushels per acre. Quick raw math based on today’s price per bushel of $6.00 puts gross revenue at 5.4 Million dollars. Noting the rapidly rising costs of inputs (seed and chemical), labor and energy prices, a return to August 2020 prices of $3 would be a massive hit and likely take down such an operation.

All of this is to say that today’s job requires greater collaboration with others in the business than ever before (see section below on intermediaries and risk management).

INTERMEDIARIES/RISK MANAGEMENT

Commodity markets are highly unique in that both end-users and physical producers of a product can proactively buy and sell their input and or production in an open market before being produced via a forward contract or hedge.

To hedge is to manage risk and, in most cases, lock in or protect the profits margins. As discussed above, grain production is a highly volatile business, just like the purchase side (see end-users and commercials below).

Through intermediaries and risk management experts, farmers and end-users gain timely market information, access to markets, and ultimately execute the majority of their forward pricing. Whether through the use of futures, options, swaps, or even physical contracts developing and coordinating a risk management plan is essential to the long-term health of our global commodity infrastructure.

The CME Group is the world-leading commodity exchange, and their global branding says it best – “CME Group, where the world comes to manage risk.”

RCM Ag Services also falls into this category. We provide full-service risk management and advisory solutions to our local area producers and commercial agriculture operations around the globe.

TRANSPORTATION/LOGISTICS

COVID introduced unexpected stresses on global food systems, creating many immediate and rapid challenges to secure food availability. If a worldwide pandemic taught us anything, we know that supply chain management and transportation play a vital role within the agriculture industry. Agriculture logistics ensure that items like food, machinery, and livestock from all over the world are transported with a continuous, optimal flow from the manufacturers and suppliers to the producers and ultimately delivered to consumers.

Some of the most imperative agriculture supply chain and logistics management activities include production, acquisition, storage, handling, transportation, and distribution. Effective logistics is critical for guaranteeing customer satisfaction and meeting demands on time with high-quality products. In addition, logistics should also meet specific standards and operational objectives for efficiency in agriculture policies like:

Protection of the environment

Sustainable distribution practices

Food safety and security

Animal welfare (for transporting livestock)

With the growing population largely expected in developing countries, most of which have poor infrastructure, we can expect the need for massive investments into transportation and logistics operations in the years ahead (this is NOT a stock tip!).

COMMERCIAL AND END USERS

The penultimate step of the process is grain reaching a commercial elevator before going on to the end-user to be converted to a final product. Some producers deliver straight to the end-user in areas where that is an option.

Traditionally, commercial elevators accept farmers’ grain and then ship it to the end-user, either by rail, barge, or other means.

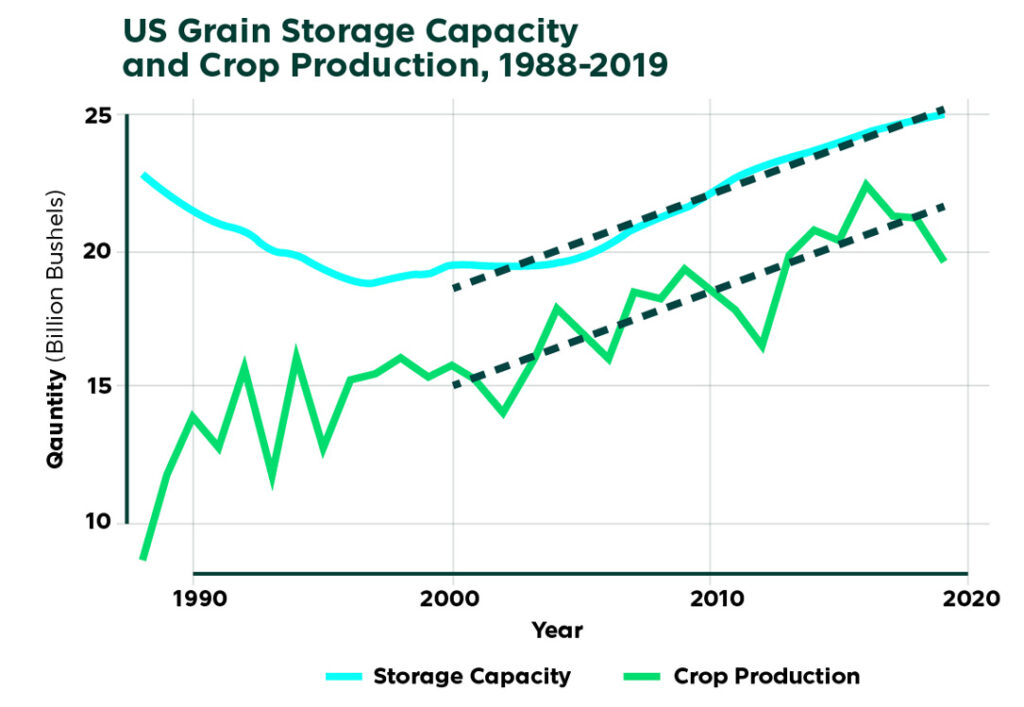

With the continued upward trends of production, it is no surprise, that grain storage capacity has consistently grown. In fact, it is on pace with increases in crop production over the last 20 years and by all accounts is likely to continue to grow.

Source: Farmdocdaily

Along with the enormous capacity, commercials and end users also carry a tremendous amount of of price / volatility risk requiring a proactive and disciplined risk management approach to maximize the margins of their operation and keep the system moving forward.

In 2018, $139.6 billion worth of American agricultural products were exported worldwide, with elevators playing a significant role in that process. The commercials and end-users are essential for getting the product from the farm into your home on the table.

FEEDING THE WORLD IN THE FUTURE

Bringing awareness to how the agriculture industry is vital to feeding the rapidly growing world is pivotal as we continue to face unprecedented challenges in global food security. However, there is a silver lining. We already know what must be done; it is figuring out how to do it that could be problematic. The world must unite and understand that each of these areas highlighted in the infographic is very complex, employs millions of people worldwide, and is vital to the growth of the agriculture industry as well as producing the necessary food for the future.

Download the Infographic

CONTACT AN AG SPECIALIST TODAY

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact us today to speak with an ag specialist at 888-875-2110!

Corn continued its rally this week as grain bulls and inflation continue to drive it higher. The yield losses in South America continue to have news around it as the reality of significant losses begins to set in. Too much rain and heat or not enough rain and heat have been driving the issues, with very few areas having excellent growing conditions. With the Chinese New Year coming up, China will disappear from the export reports for a little bit, but once they come back, the market will have a better idea of where Brazil and Argentina sit. If the rumored losses come to fruition, we could see China increase its purchases. Corn has continued its rise while wheat struggles to make up its mind with confusion around the Russia and Ukraine situation. Any escalation there will result in more bullish factors in the market. Despite some volatility, energy prices continued their rise, with crude oil hitting a new high this week. Ethanol plants will continue to produce even with higher corn prices as long as their margins remain strong despite resulting in less fuel consumption. Many energy companies think we could see $100+ Crude in the next few months.

Soybeans continued to move this week on similar news as corn with South America’s issues and continued world veg oil strength. With strong veg oil prices pulling beans along with it as long as that lasts, we can expect some support under beans with any lower moves. Like corn, if private estimates of losses to the South American crop become a reality, we should continue this run higher. If China comes back from Chinese New Year and starts picking up bean purchases, mixed with world veg oil prices could see this rally continue. Acreage estimates for 2022 have been coming out, with Informa pegging the US bean crop at 87.8 million acres. This is slightly higher than the 87.2 million acres from 2021, but we have a long way to go before we get to that point.

Equities had quite the week with large intraday trading ranges as the market does not seem to make up its mind. This week, the Fed’s decision to leave interest rates as-is means we should expect a raise from the March meeting. The Fed also said they would adjust asset purchases moving forward. The tensions between Ukraine, Russia, and NATO remain a large question mark, but it appears Putin may not do anything until after the Olympics. This will be important to keep an eye on for equities and commodity prices.

The cotton market has held in this $1.20 range for the last ten trading days. World demand is there, and this bull market could have room to run if inflation sticks around with other supply chain bottlenecks. We could continue to see this strength last into the spring when planting starts until we get a better idea of what the U.S. cotton crop will look like this year. With rising consumer demand, the cost of production and transportation in the next few months could see volatility.

Podcast

Tune in as biotech guru Dr. Channa S. Prakash discusses everything from Alabama football, genetics as one of the most extensive agricultural advancements, the most significant risk factors to feeding the world over the next 30-50 years, plus everything in between.

Why producing crop plants with a much gentler footprint on the natural resources will help feed the growing population. How 75% of the world’s patents in agriculture gene editing are coming from China. Understanding that trying to impose restrictions on our ability to grow food can be a considerable risk to agriculture. Listen to hear about these topics and more!

RCM Ag Services is a registered DBA of Reliance Capital Markets II LLC. Trading futures, options on futures, and retail off-exchange foreign currency transactions are complex and involve substantial risk of loss and are not suitable for all investors. Loss-limiting strategies such as stop loss orders may not be effective because market conditions or technological issues may make it impossible to execute such orders. Likewise, strategies using combinations of options and/or futures positions such as “spread” or “straddle” trades may be just as risky as simple long and short positions. There are no guarantees of profit. You should carefully consider whether trading is suitable for you in light of your circumstances, knowledge and financial resources. You may lose all or more than your initial investment. You should not rely on any of the information herein as a substitute for the exercise of your own skill and judgment in making such a decision on the appropriateness of such investments. Opinions, market data and recommendations are subject to change without notice. Reliance Capital Markets II LLC shall not be held responsible for any actions taken based on this website or attached links. Parties acting on this electronic communication are responsible for their own actions. Past performance is not necessarily indicative of future results.