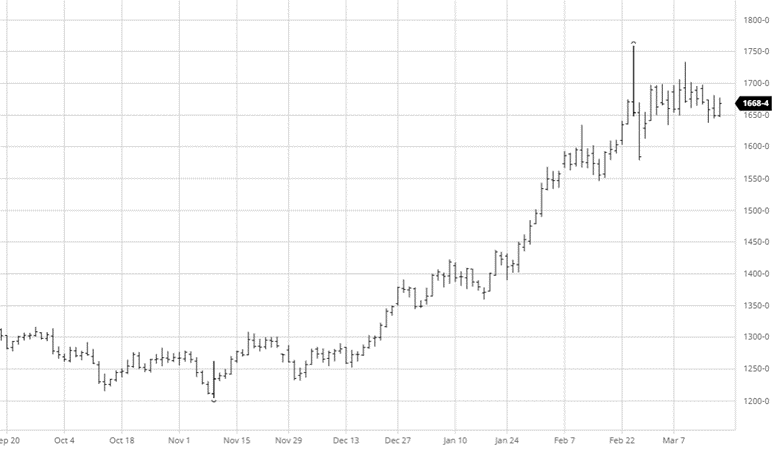

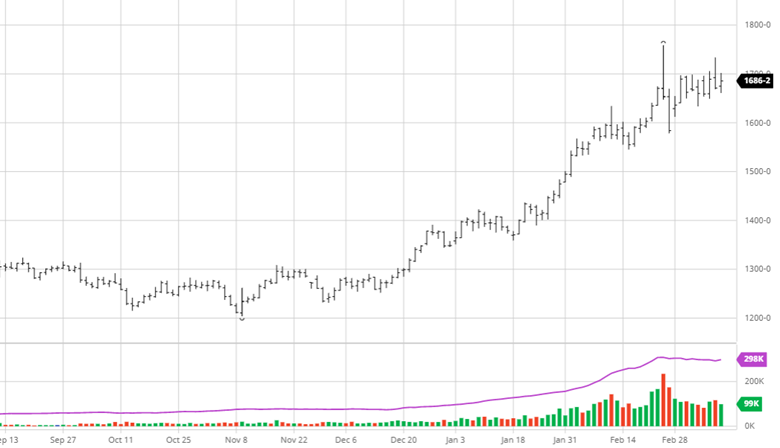

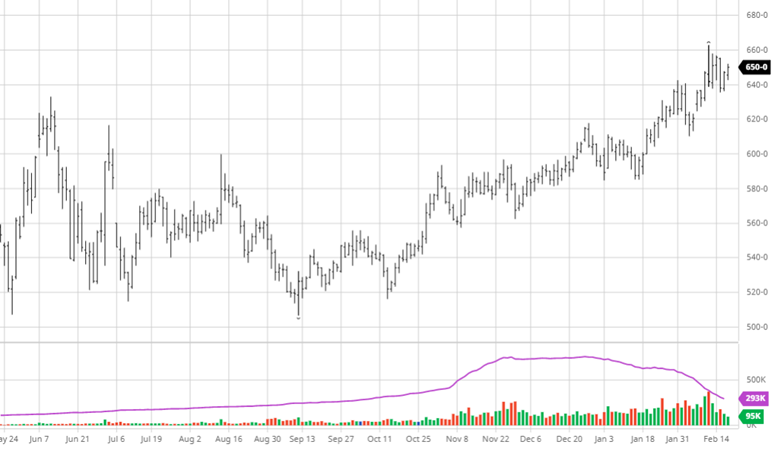

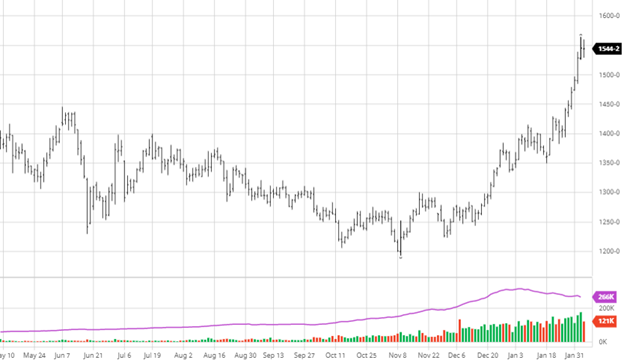

Corn has continued to trade in the same range since early March as the markets wait for next week’s acreage report from the USDA. This is a major market-moving report historically, so expect volatility either way. IHS Markit’s current estimates were for 91.42 million acres of corn, while Pro Farmer came out with 91.9 million. While these numbers seem realistic and may ultimately be right, I would be surprised if the USDA came out with anything lower than 92 million. The big question is, will higher inputs cause fewer acres even though there are higher prices, or will it be flipped? All eyes will be glued to the markets for the report, with the only other market-moving news until then will be developments in Ukraine.

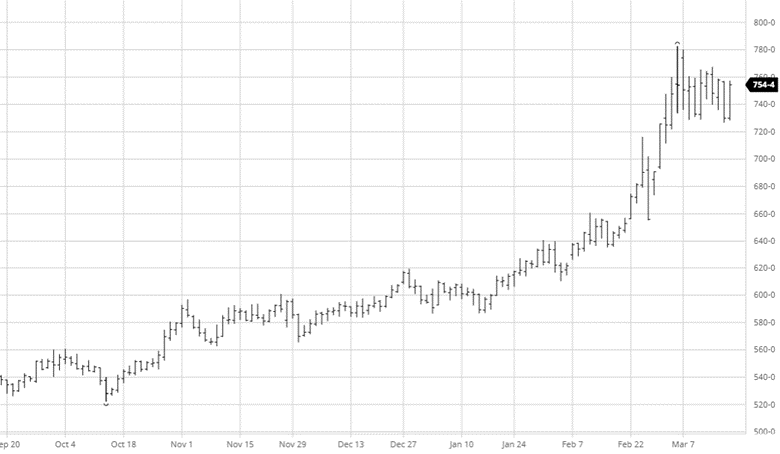

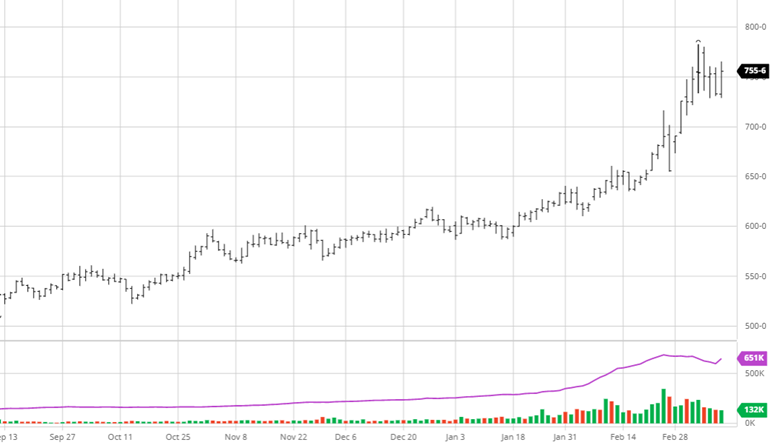

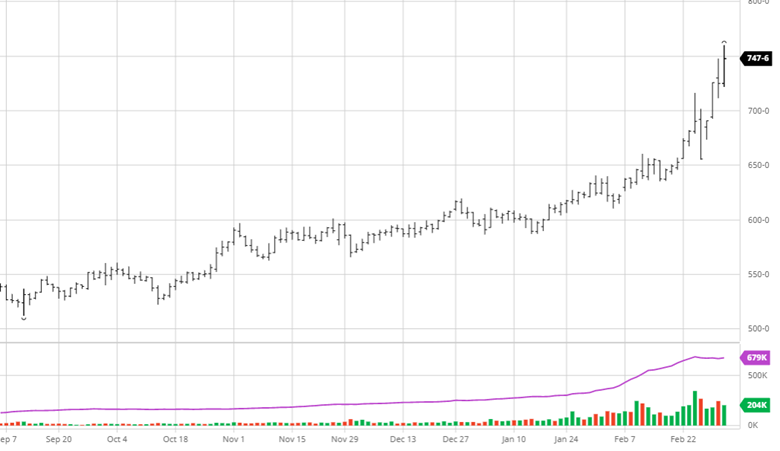

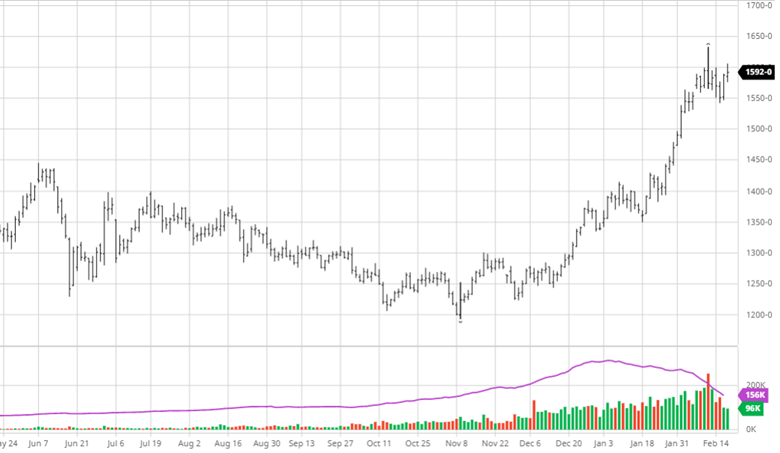

Soybeans continued their steady climb while corn and wheat calmed down. Next week’s report will be important for beans as well. Some analysts expect more bean acres this year as some farmers switch corn to beans in favor of lower input costs. IHS Markit estimates 88.58 million acres while Pro Farmer estimates 87.8 million. This is a good size difference showing uncertainty around the bean number with prices this high. South America’s weather has become less newsworthy so expect the market to position itself into the report unless there is any unforeseen news.

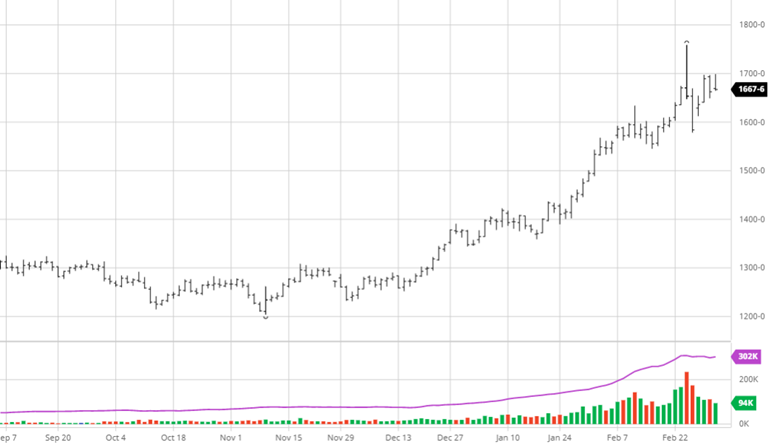

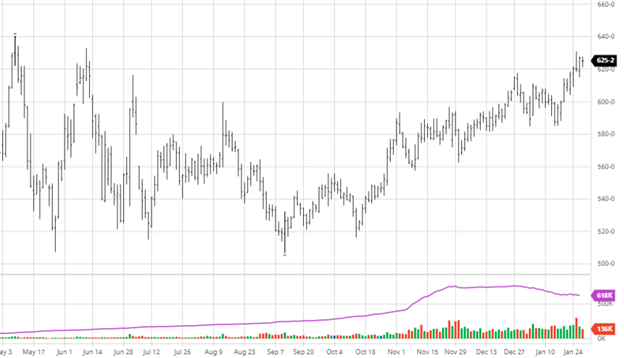

Wheat’s craziness cooled off this week as many people have completely gotten out of the market until there is less uncertainty. With no significant news this week on the path of the fighting in Ukraine, the markets stayed in a smaller trading range compared to the past few weeks. The world wheat outlook is not very bright with the problems in Ukraine, China’s awful crop, and the struggles with the US crop, expect balance sheets to get tighter. World sanctions on Russia will play out in the wheat market if everyone stops buying Russian wheat; China will likely shift their buying to them and change up the trade dynamic of countries. The major news moving forward is still Ukraine.

Cotton

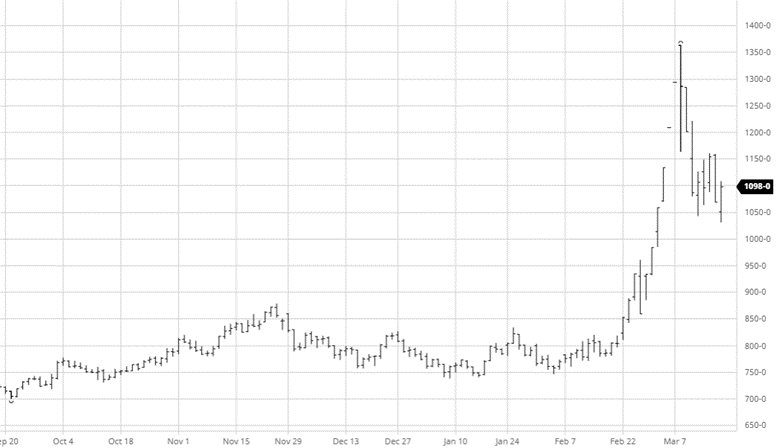

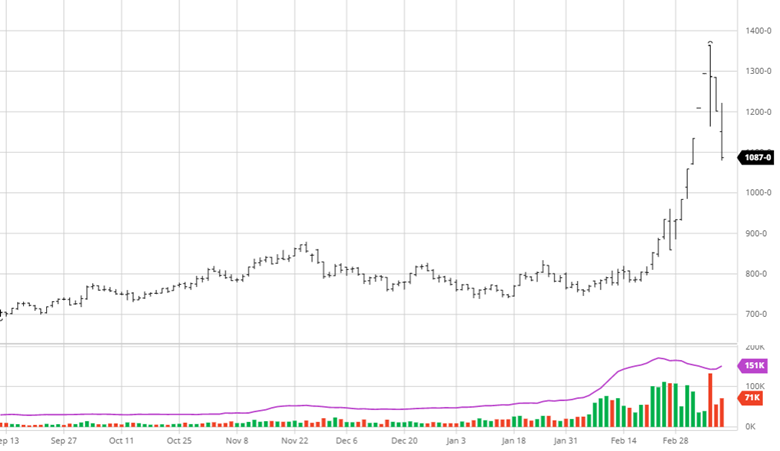

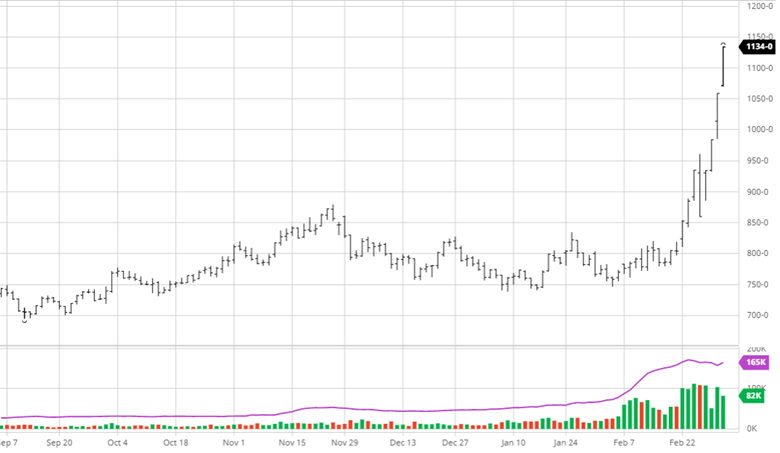

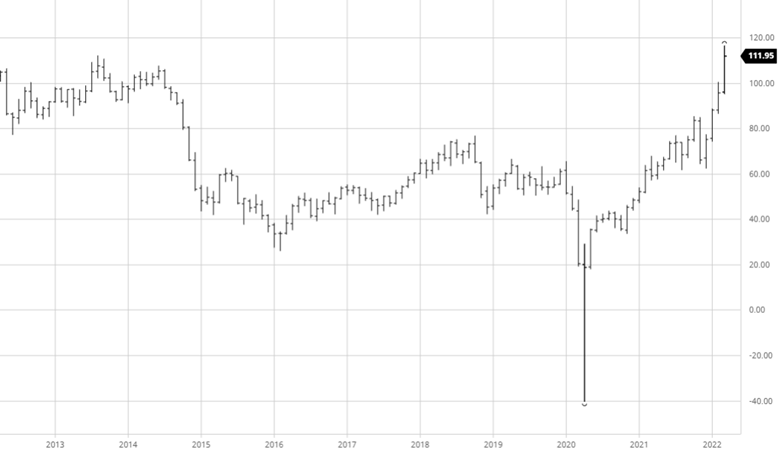

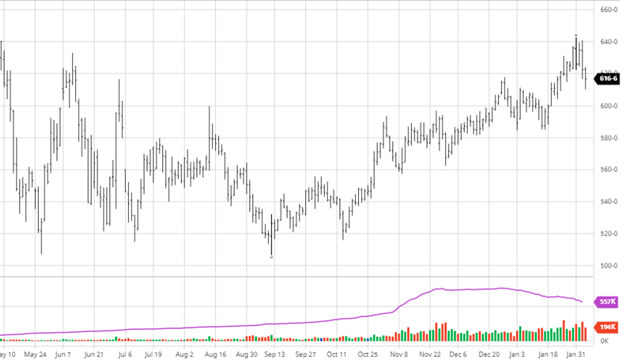

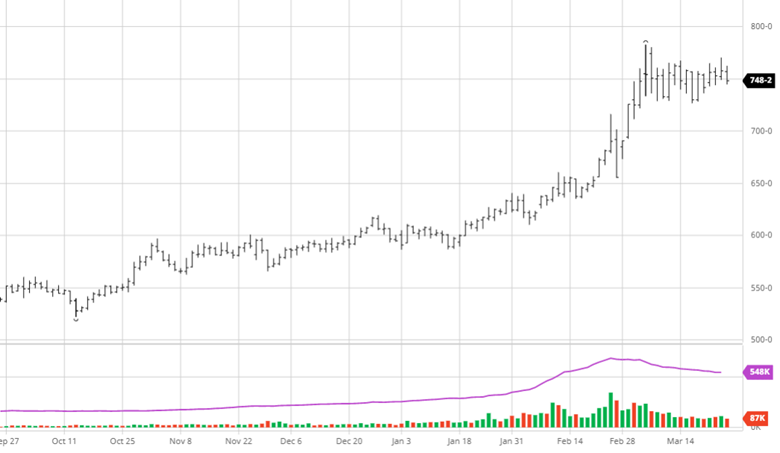

Cotton has had a good few weeks with the May contract topping $1.30. Many in the industry have expected this move higher, but its reluctance to do it has been frustrating. With a tight market and world demand, this growing season will be important. Analysts estimate that between 11.7 and 13 million acres will be planted, which is much higher than last year’s 11.2 million acres.

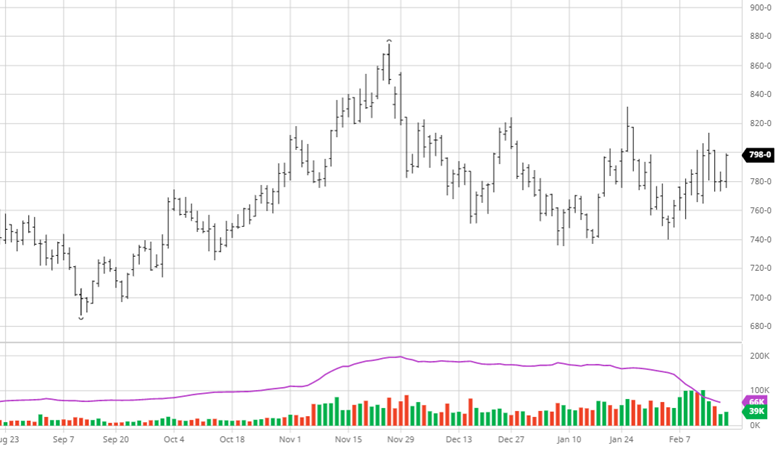

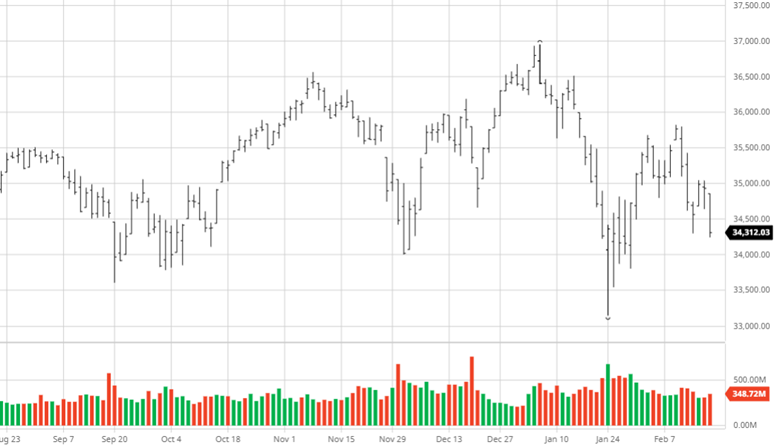

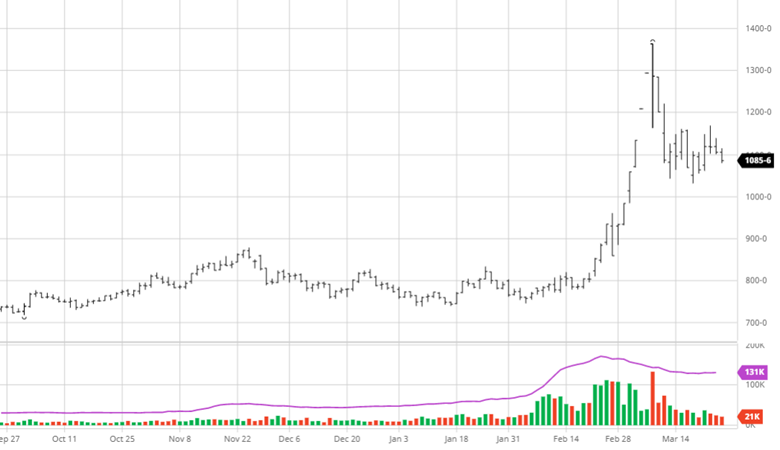

Dow Jones

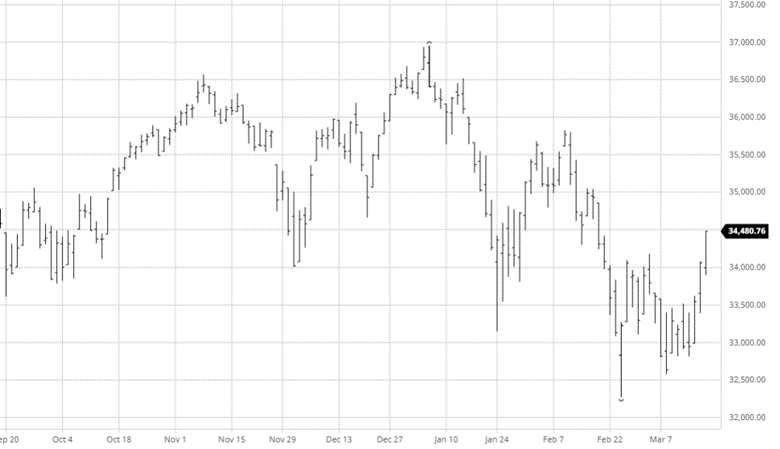

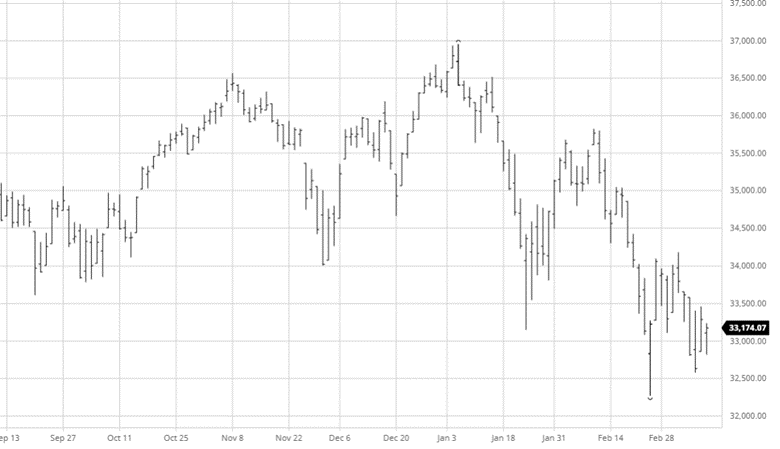

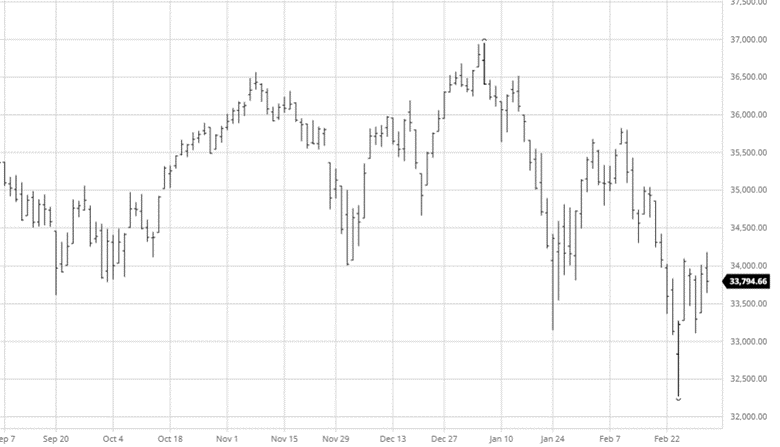

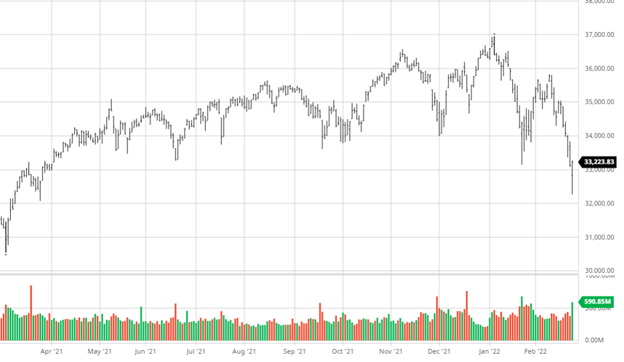

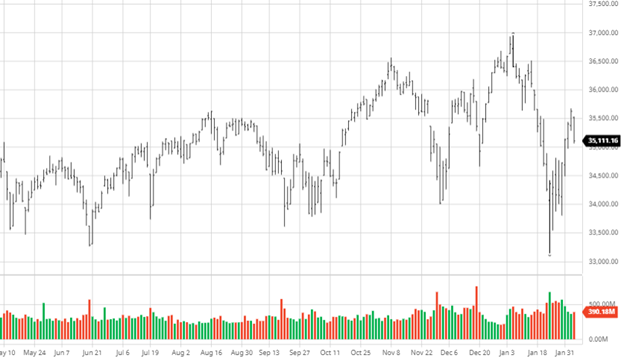

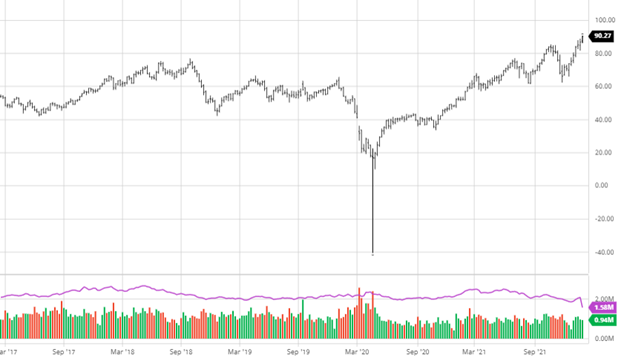

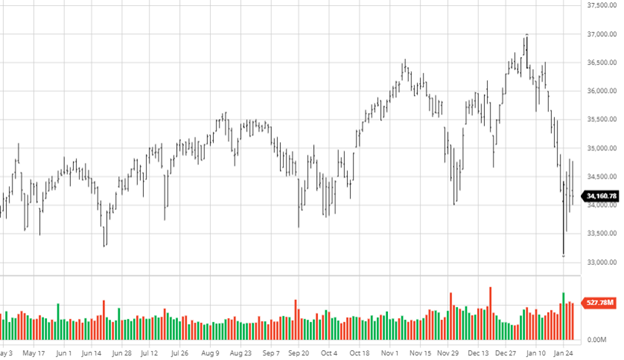

The equity markets made gains again this week as markets appear to be holding their breath, hoping that we have bottomed while also figuring out what to expect ahead. With several rate hikes expected this year, the markets will price those in accordingly and should not be shocked when it happens. Inflation concerns remain as oil prices bounced back over $100 and may stay there for the foreseeable future with no resolution to the war in Ukraine in sight.

Podcast

RCM Ag Services put a unique spin on National Agriculture Day by going international. That’s right, we jumped right into international waters with Maria Dorsett from USDA’s Foreign Agriculture Services for an interesting discussion about linking U.S. agriculture to the rest of the world.

Each year, March 22 represents a special day to increase public awareness of the U.S.’s agricultural role in society, so why not take it one step further by bringing in a global component? As the world population soars, there’s an even greater demand for producing food, fiber, and renewable resources. That’s why we’re taking a deeper dive into the USDA’s trade finance programs, like the GSM-102, which supports sales of U.S. agricultural products in overseas markets and supports export growth in areas of the world that are seeing some of the fastest population growth.

So, jump aboard (no passport needed), as Maria discusses how U.S. companies use GSM-102, what the program features, and the benefits that it offers!

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.