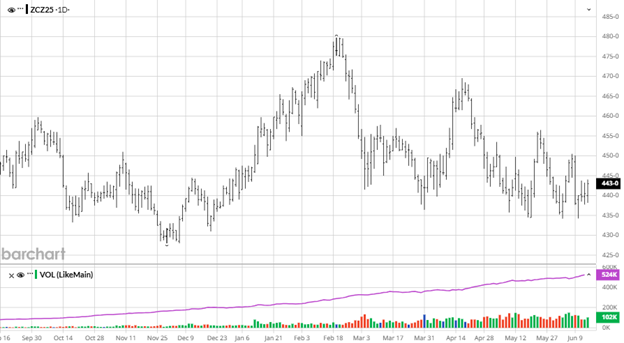

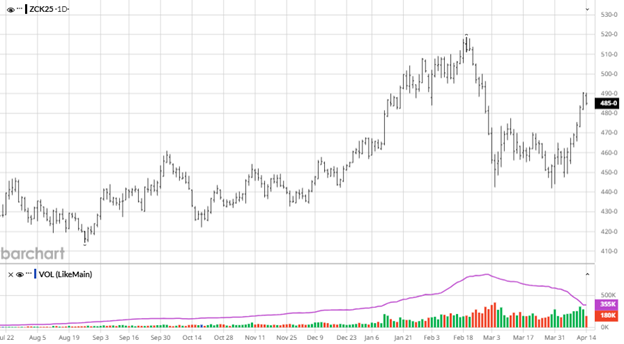

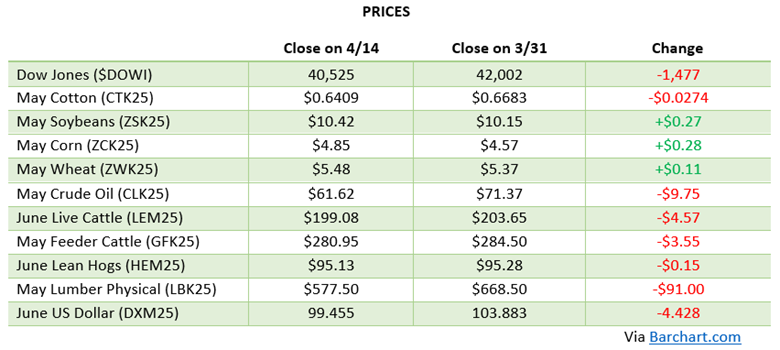

Corn continued to move higher off last month’s lows following the September USDA Report. Most of the numbers came in along estimates but they increased planted acreage 1.4 million acres. This brings the US corn crop to 98.7 million acres, a new record. With about 90 million acres expected to be harvested, we will harvest 7 million more acres this year than in 2024, which equates to about 2 billion bushels larger crop than last year. Despite the added acreage corn bounced post report as weather issues, a dry finish, and disease pressure have caused speculation on the real size of this crop. As harvest gets rolling we will learn more about this crop.

Corn continued to move higher off last month’s lows following the September USDA Report. Most of the numbers came in along estimates but they increased planted acreage 1.4 million acres. This brings the US corn crop to 98.7 million acres, a new record. With about 90 million acres expected to be harvested, we will harvest 7 million more acres this year than in 2024, which equates to about 2 billion bushels larger crop than last year. Despite the added acreage corn bounced post report as weather issues, a dry finish, and disease pressure have caused speculation on the real size of this crop. As harvest gets rolling we will learn more about this crop.

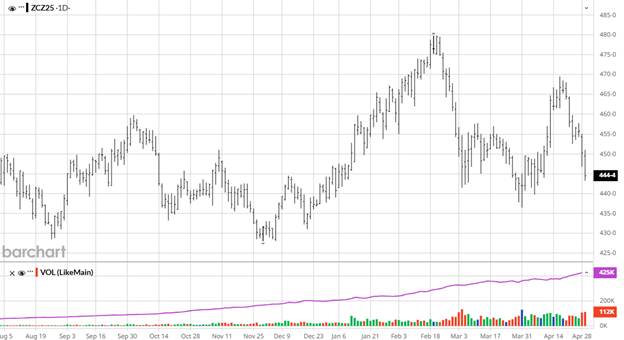

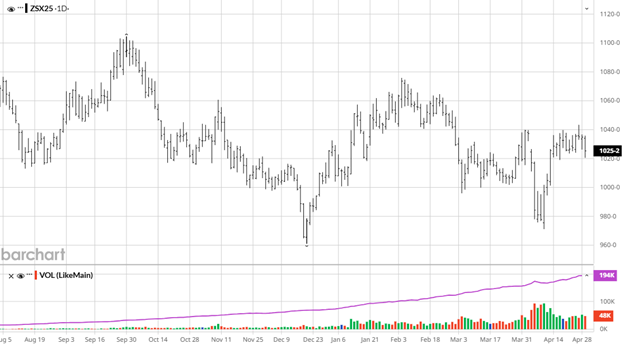

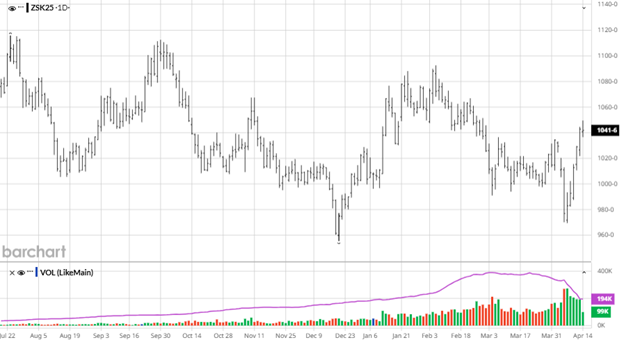

The USDA Report did not have any surprises for beans as most numbers were close to estimates, but the report could be viewed as slightly bearish. To get beans moving higher, China needs to show up as a buyer and trade talks with China need to make progress. China and the US are reportedly close to a deal over Tik Tok which can hopefully build some momentum for progress between the two countries. The size of the soybean crop, like corn, has been hurt by lack of rains down the home stretch but with the solid start the end result is still in question as harvest rolls.

The USDA Report did not have any surprises for beans as most numbers were close to estimates, but the report could be viewed as slightly bearish. To get beans moving higher, China needs to show up as a buyer and trade talks with China need to make progress. China and the US are reportedly close to a deal over Tik Tok which can hopefully build some momentum for progress between the two countries. The size of the soybean crop, like corn, has been hurt by lack of rains down the home stretch but with the solid start the end result is still in question as harvest rolls.

Equity Markets

Equity markets continue to make new highs with the Federal Reserve expected to start cuts this month. With the downward revision of 911,000 jobs from March ‘24 to March ’25 the labor market weakness gives the Fed some ammunition to lower rates with unemployment being one of their mandates.

Other News

- Secretary Rollins is in the process of looking into payments to farmers for this year with the low prices.

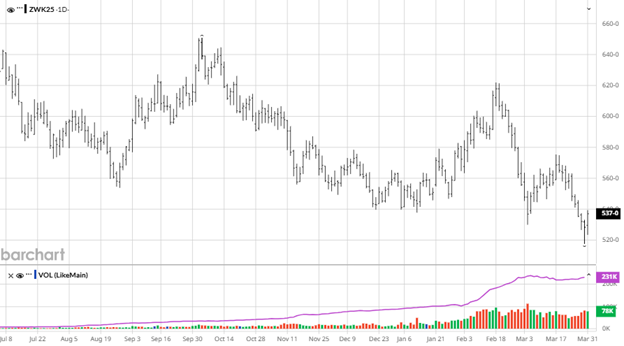

- The wheat numbers were actually a bit supportive but lower world cash prices (Black Sea mainly) continue to plague prices. Wheat will remain an anchor for any potential corn rally as more wheat will be swapped in for corn in feed. Prices are back testing the 5 ½ year Covid lows.

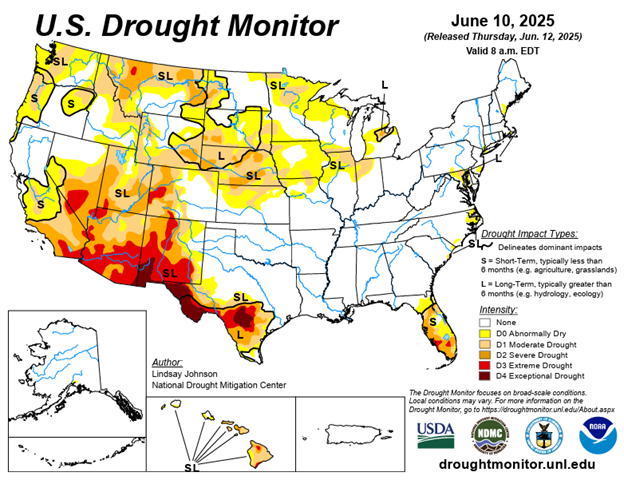

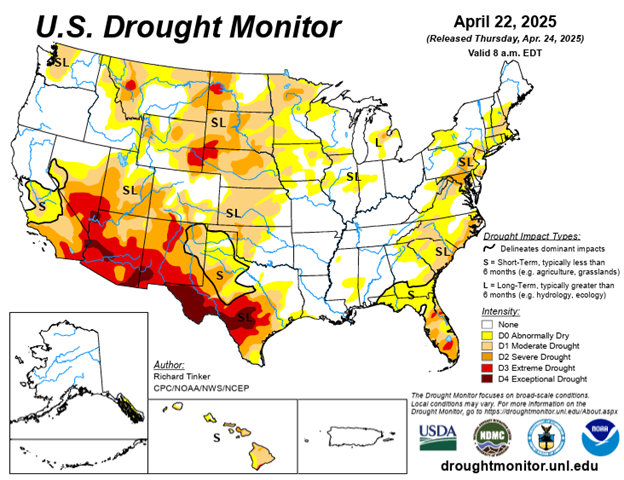

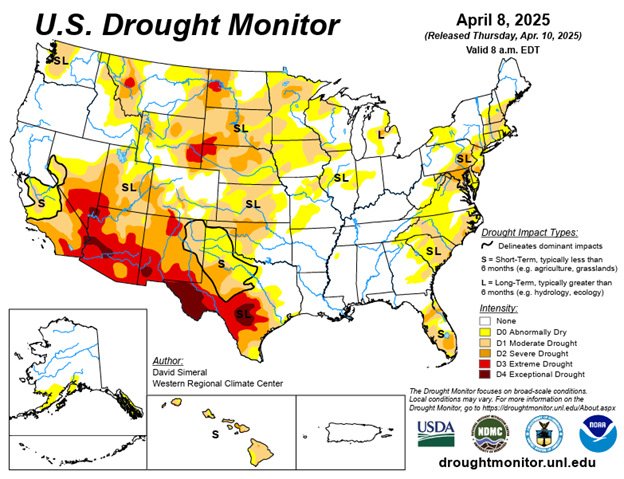

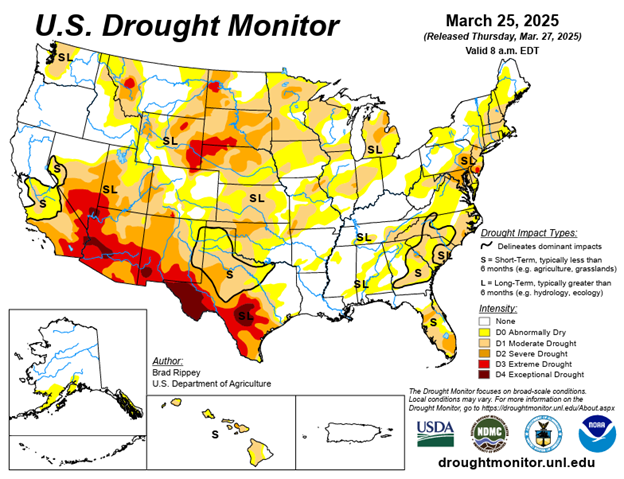

Drought Monitor

Here is the most recent drought monitor as harvest begins.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Check it Out: