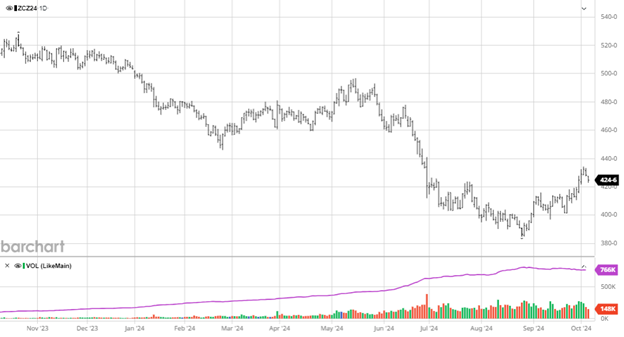

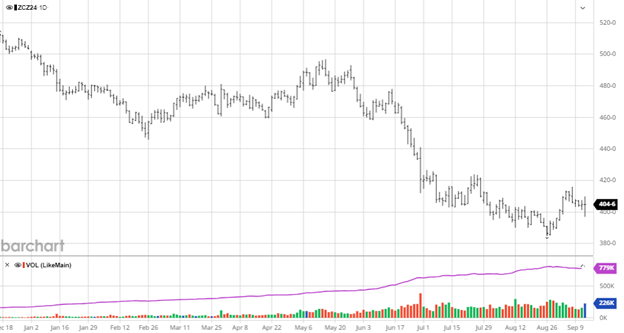

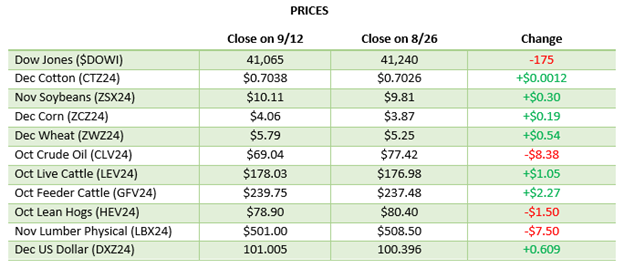

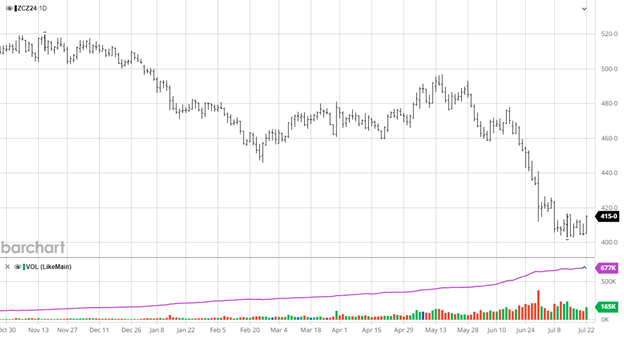

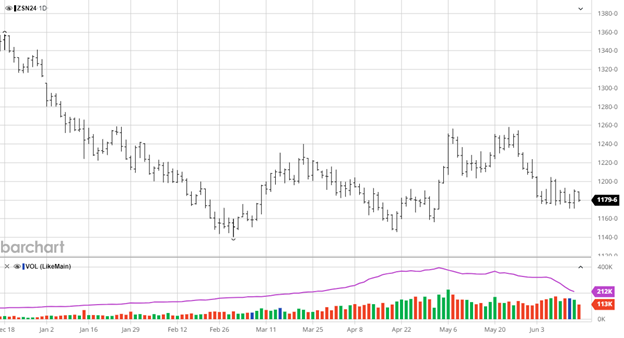

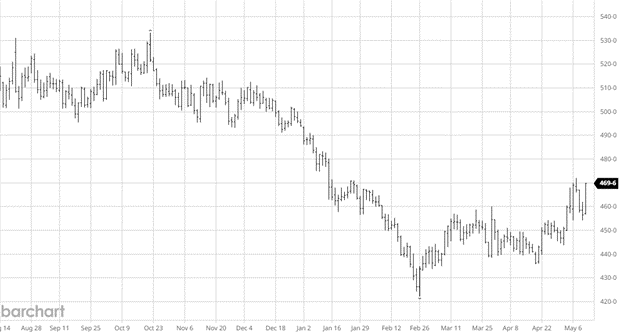

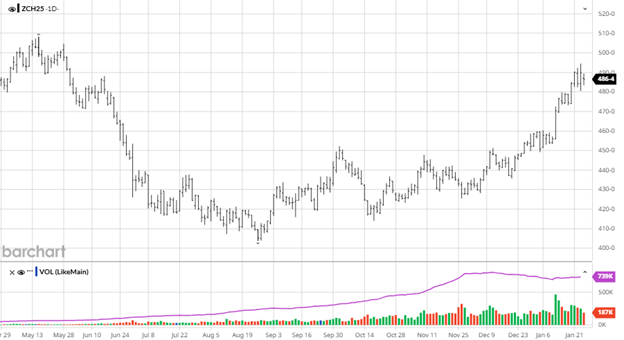

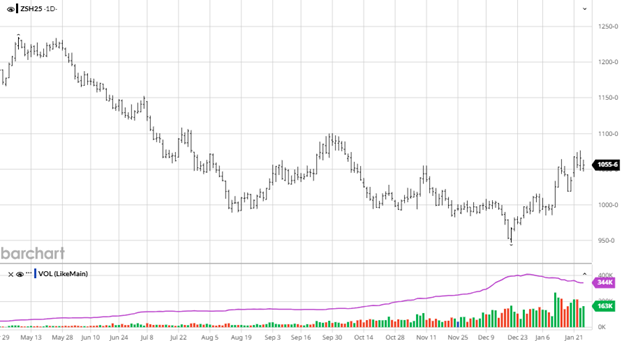

A lot has happened in the corn market since our last update, from a new administration taking office to a surprise USDA report. The final yield and stocks for 2024 came in well lower than previous USDA estimates leading to a solid rally for a market that needed it. The USDA lowered the final average yield to 179.3 bu/ac, down from their estimate of 183.1 bu/ac in November. The market had been priced in for a 182+ yield so as you can see in the chart below the market responded appropriately. The market popped higher to reach new 6-month highs following the report and has continued higher with funds having long positions in the market.

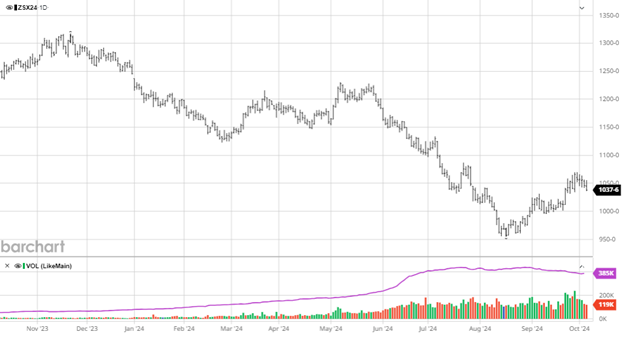

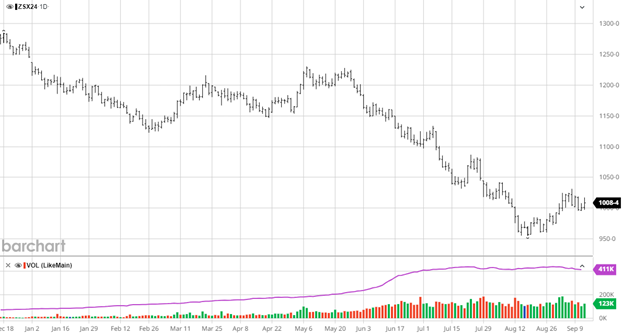

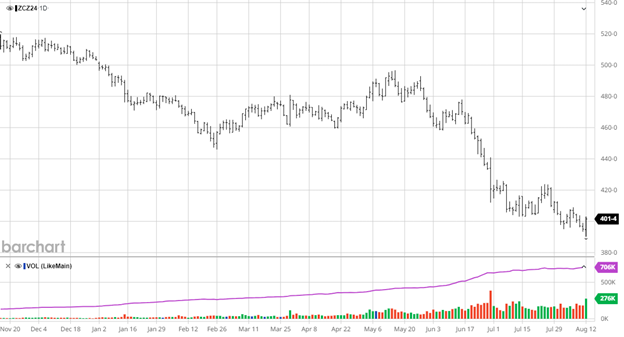

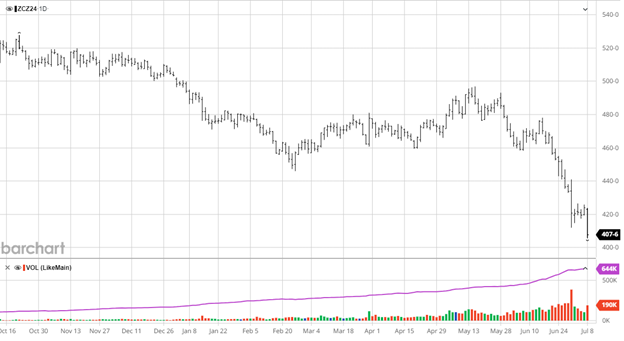

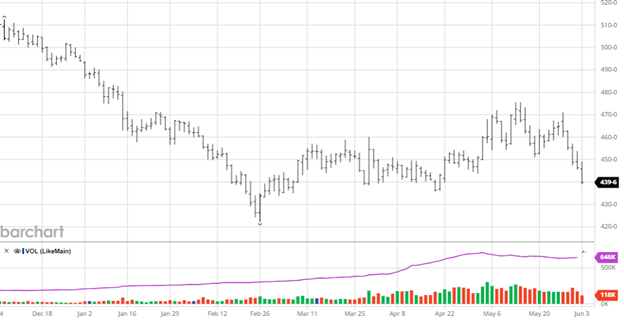

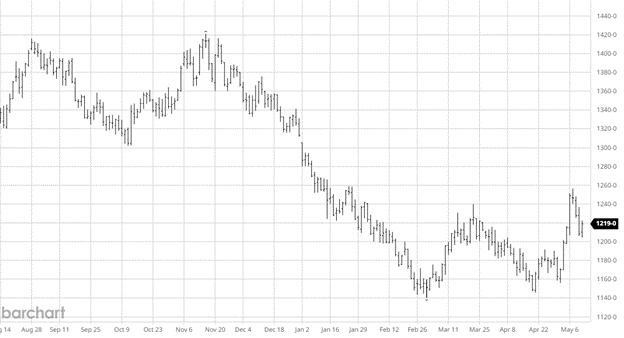

Soybeans’ also got a bump following the January USDA report. The USDA lowered the US crop from 51.7 bu/ac in November to 50.7. The yield cuts worked through to ending stocks but did not completely match as demand numbers were slightly trimmed with harvested acres raised. The Biden administration did not help out the SAF industry on their way out as bean crush plants remain in limbo on its future as a less eco friendly Trump administration takes over. What was projected to be a huge win for soybean growers now is a cloud that you do not know how long it hangs around before it rains. South America’s yields were barely changed with their forecasts now the most important thing to the markets (outside of President Trump starting any trade wars).

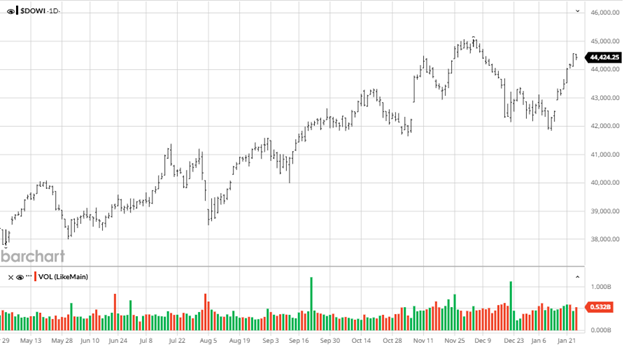

Equity Markets

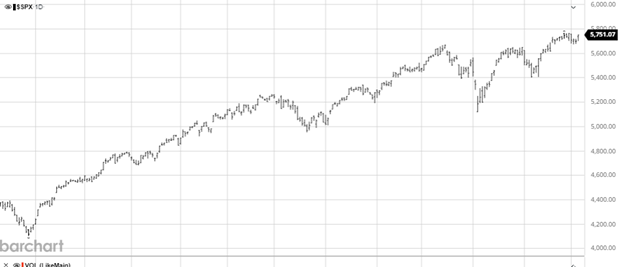

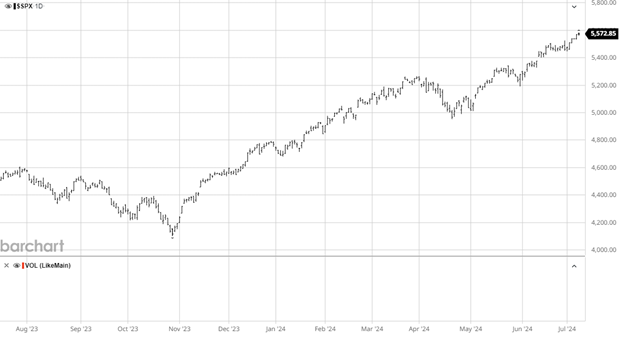

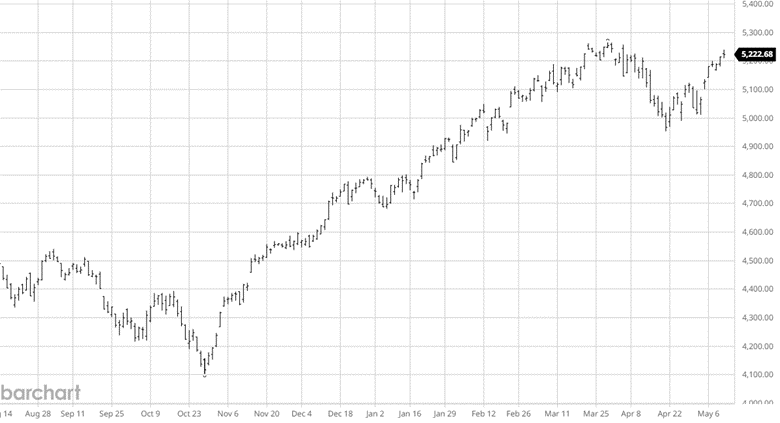

The equity markets have had a volatile end to 2024 and start of 2025 but overall seem to be in a good place as Q4 earnings start to come in. A wave went through the market with Chinese DeepSeek coming out with an opensource AI model that is much cheaper than anything in the US. This caused tech stocks to plummet to start the week with Nvidia losing over 15%. With no immediate tariff action by the Trump administration the market sighed some relief as this administration appears to be taking a more measured approach than in President Trump’s previous term.

Other News

- The USDA’s revisions lower were both surprising in a positive way and frustrating how they were so wrong on the data the market traded for the last few months when farmers had to sell.

- The Trump administration had their first spat over deporting illegal immigrants with Colombia president Petro while mutually threatening tariffs over the handling of the situation.

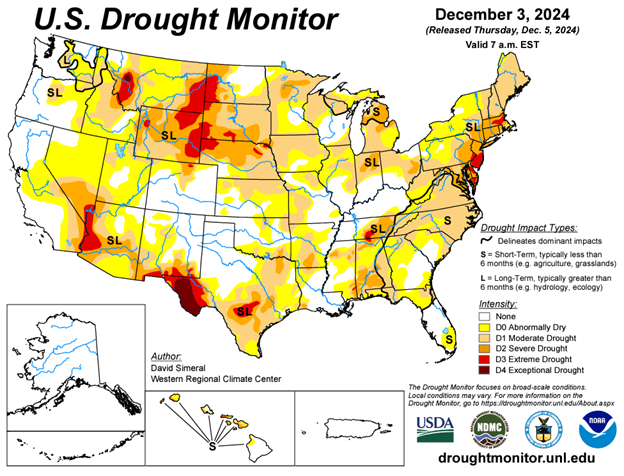

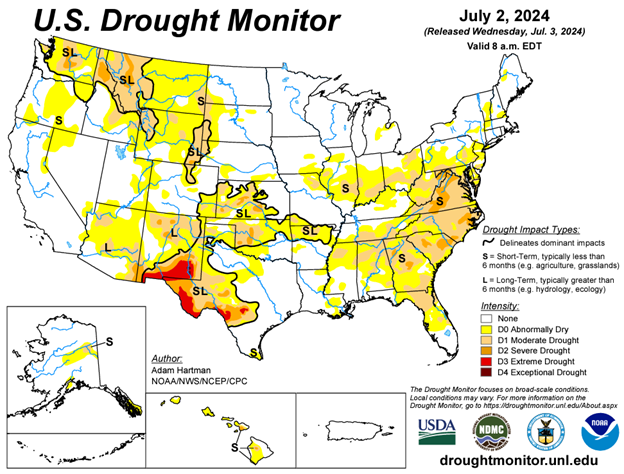

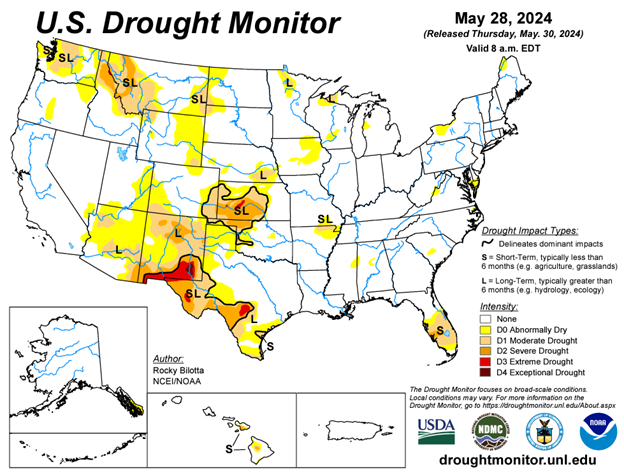

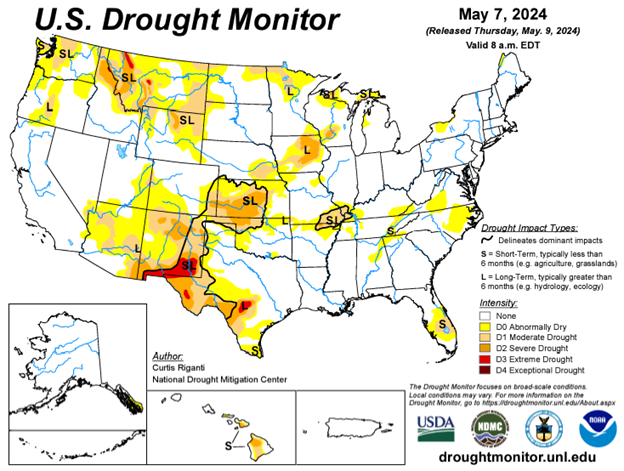

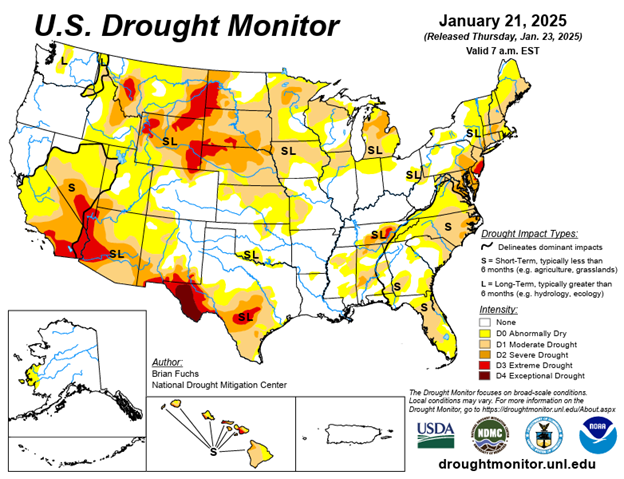

Drought Monitor

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.