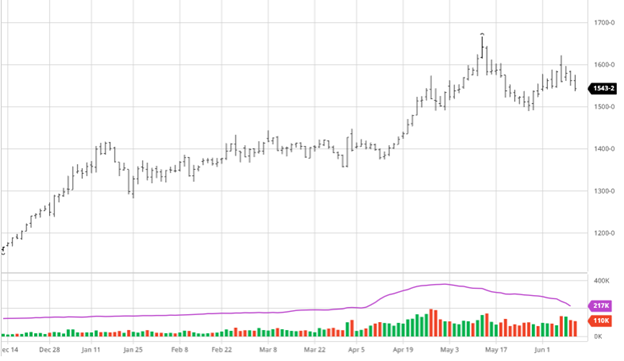

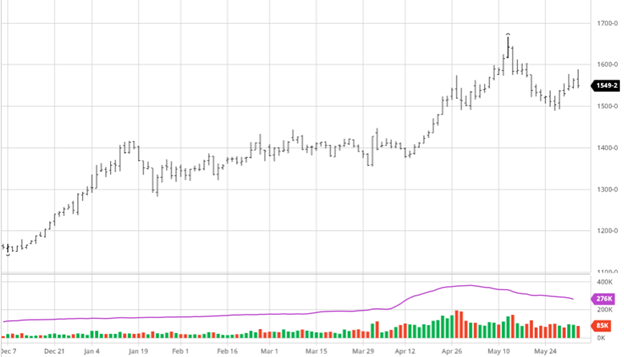

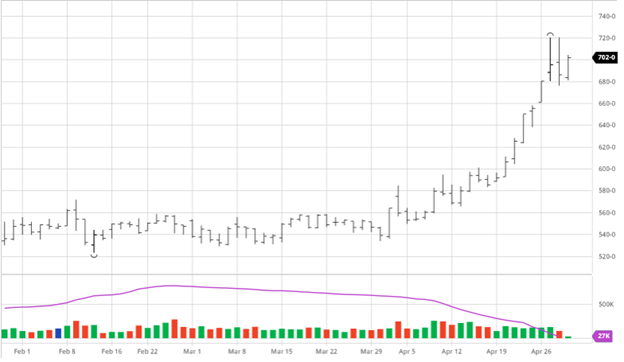

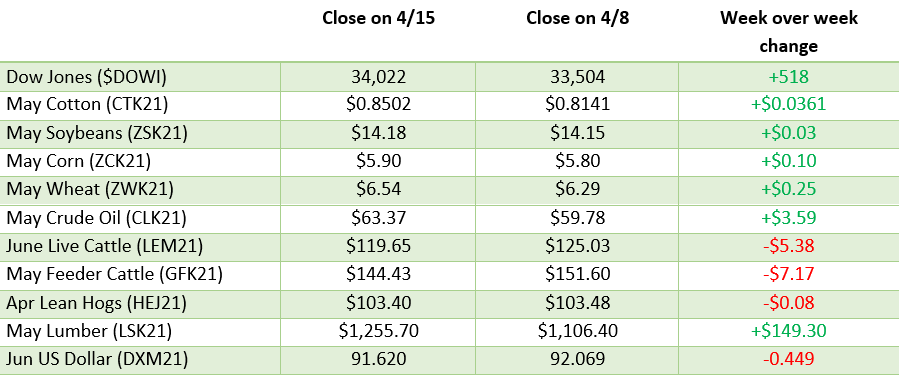

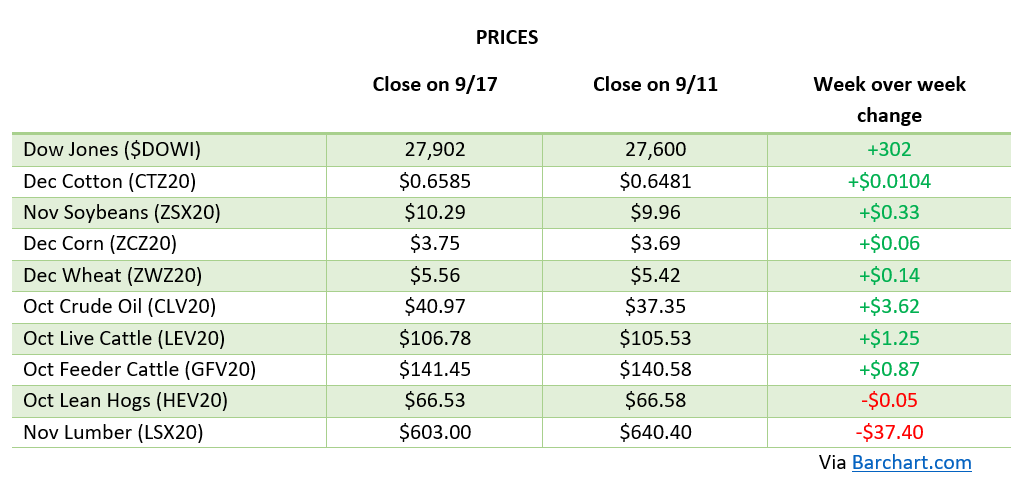

Corn had a volatile week much like beans having a limit down day on Thursday then a strong recovery on Friday. Corn had had a choppy trade this week before Thursday but the collapse in soybeans and soybean oil brought corn down with it. The bearish news for corn was that it was expected to rain in the drought stricken upper Midwest. This rain is much needed and will help but more consistent rainfall over the coming weeks would be needed to help the crop more. The rain will likely pressure markets lower to start the week if forecasts were accurate. If it does not rain as much as predicted it could fuel the bulls to continue from Friday. The dip on Thursday allowed some bulls to get back in the market at an attractive area while the bullish news remains the same.

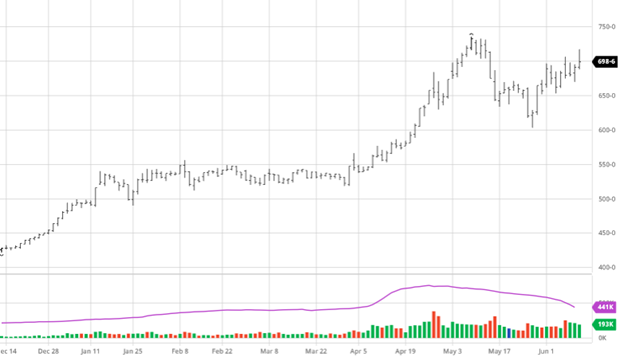

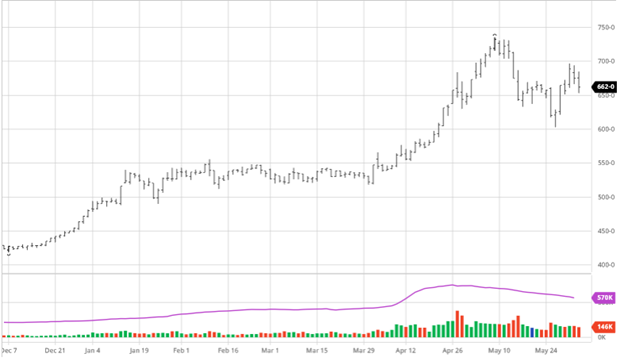

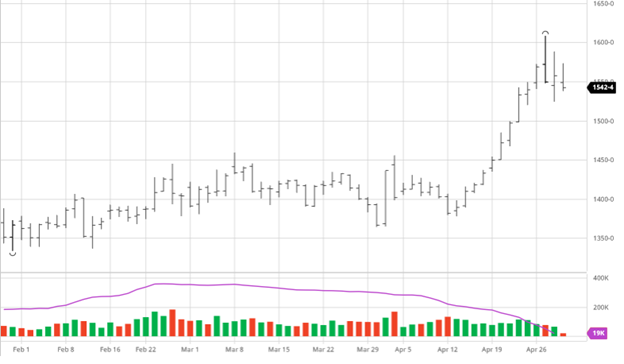

Soybeans nosedived on Thursday as they took full advantage of the expanded limits and fell over $1. The pressure on beans has been coming from the soybean oil and crush markets as crush numbers have decreased and soybean oil prices have fallen rapidly. With US yield estimates coming in around 52 bpa the price levels from earlier in the year would be hard to get back to. South America had a good bean harvest so there is not as much stress on the supply side like there is for corn. If dryness continues into the summer and yields begin to take a hit we could see a rebound for the bulls. The trade over the next week and half going into the June planted acreage report will give us an idea of what to expect in the report at the end of the month.

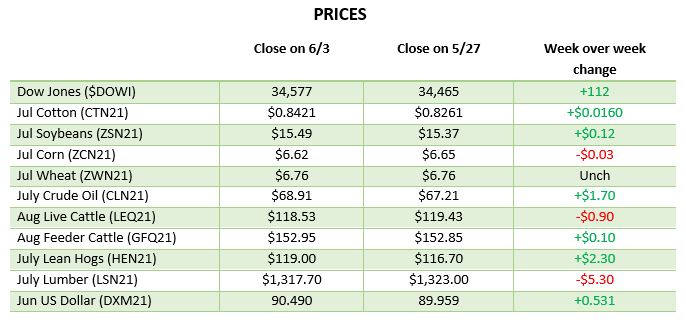

Dow Jones

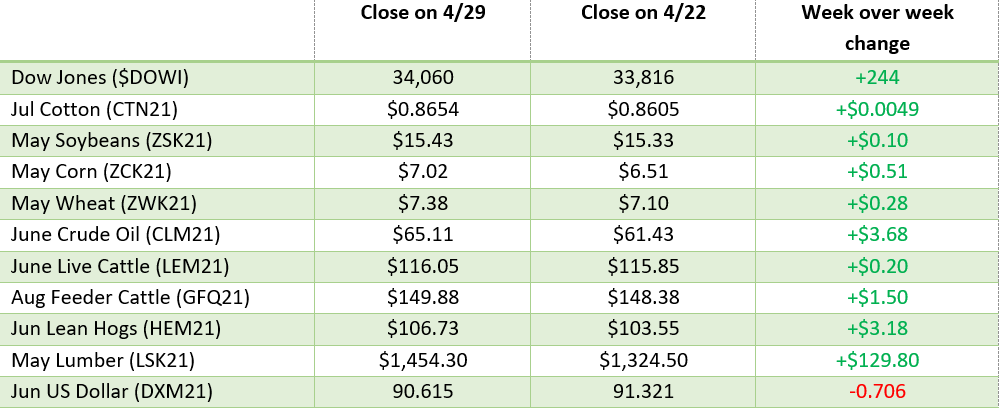

The Dow suffered loses on the week as the Fed announced they would begin looking at raising rates to help combat inflation. Although they said the plan would be to not raise til 2023 the market seems to think that timeline will probably be moved up if inflation accelerates.

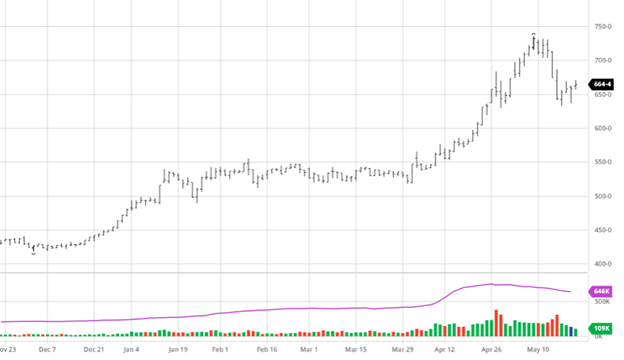

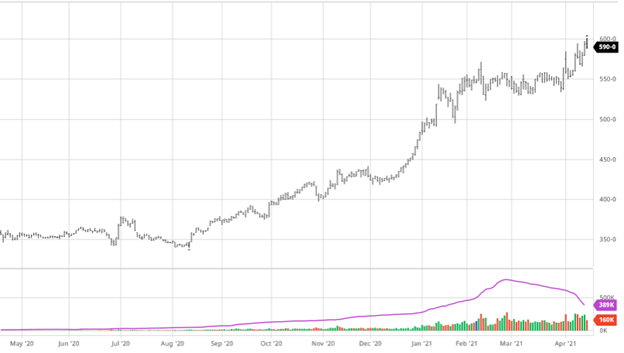

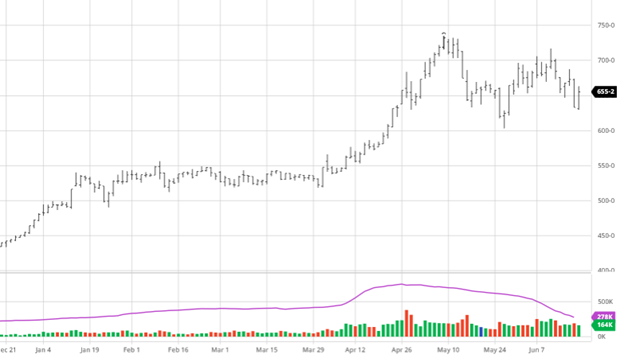

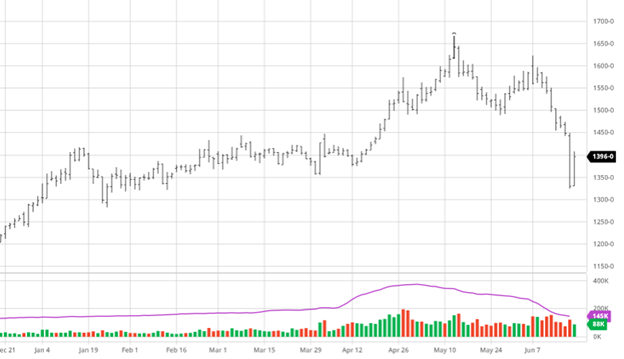

Lumber

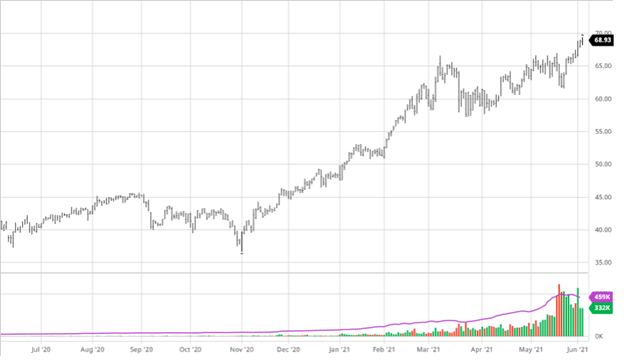

Lumber prices have dipped recently but are still at very high levels historically. Check out our recent post about the lumber market and what all has been going on.

Podcast

Check out our recent podcast with Dr. Greg Willoughby: We’re talking with Greg in the new episode about being a “plant doctor”, weather patterns, GMO & organic produce, crop history, technical advances, level 201 education on agronomy, the agronomy equation, Helena Agri, soil biology, American v European agriculture, Greg’s early background in livestock, and the advancement of native plants to modern produce.

https://rcmagservices.com/the-hedged-edge/

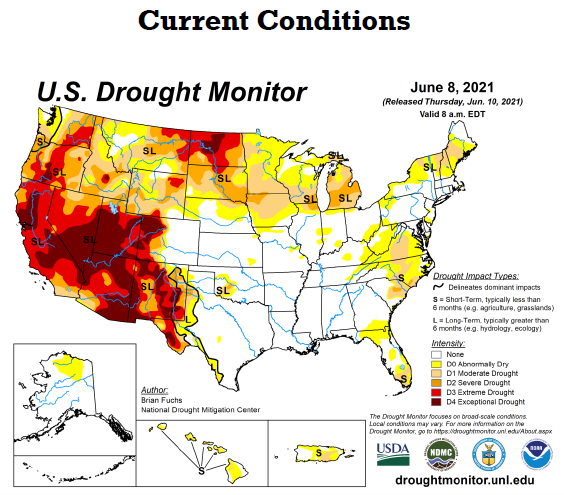

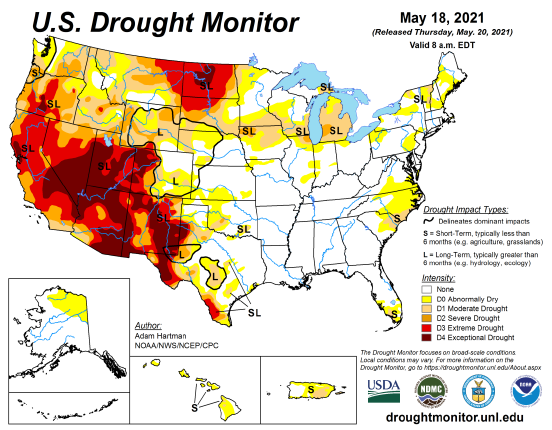

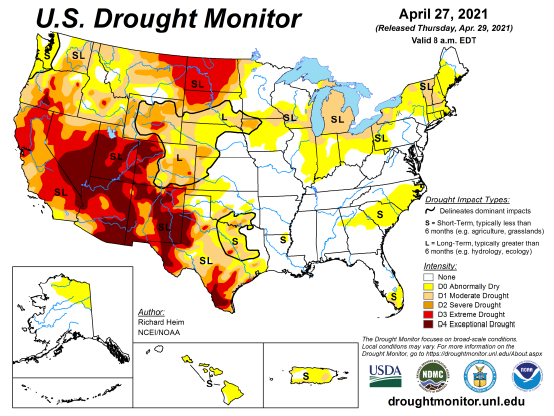

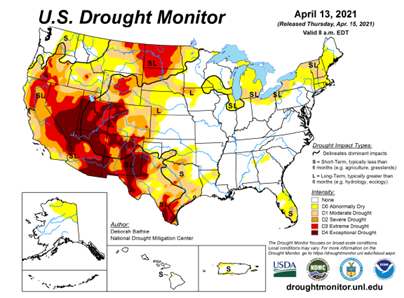

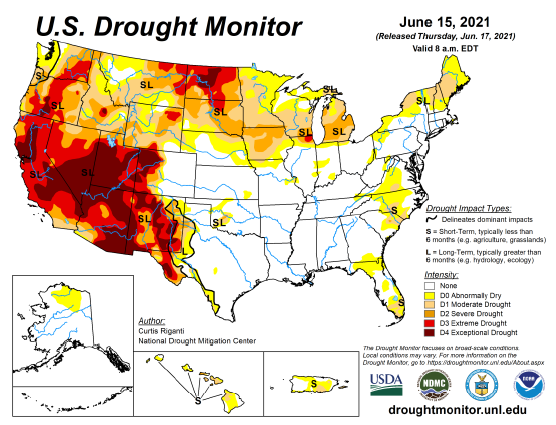

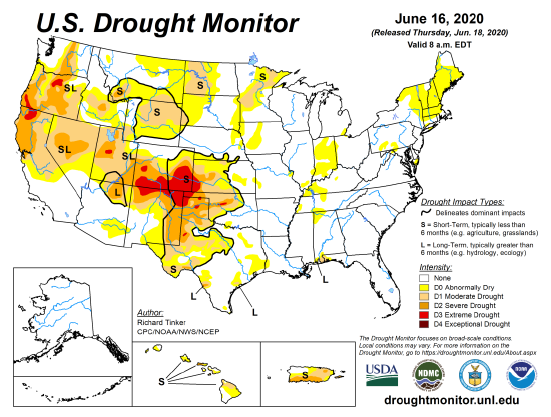

US Drought Monitor

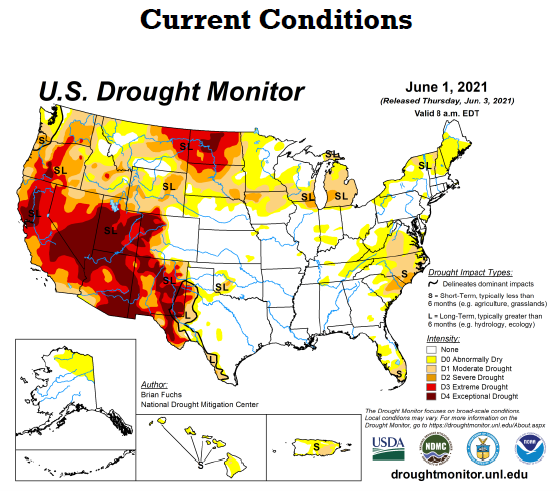

The map below shows current drought conditions and the continued problems in the upper Midwest. Drought conditions continue in the Midwest with some areas getting relief over the weekend. For reference the second chart below is this time last year.

Via Barchart.com