Lumber Weekly

- The quest for today’s value remains elusive.

Last Week:

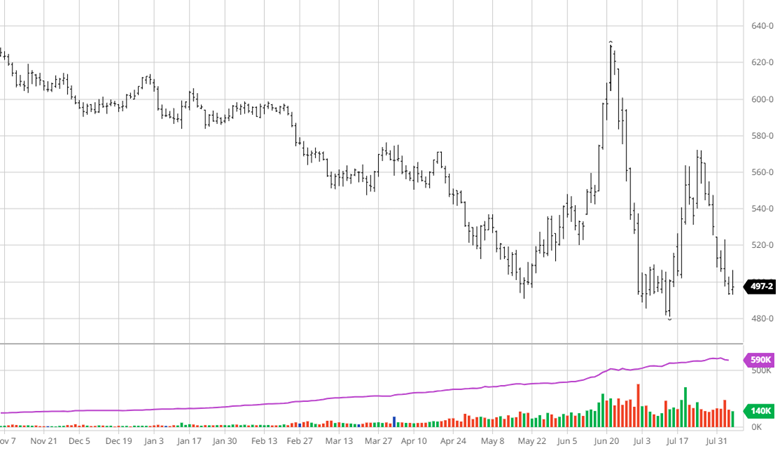

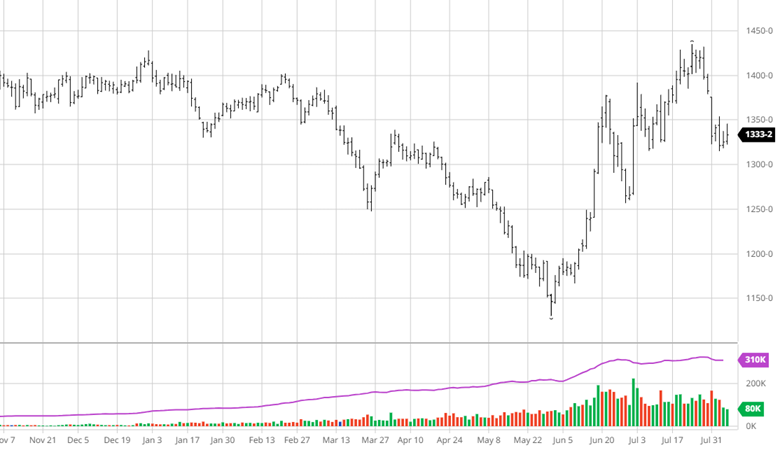

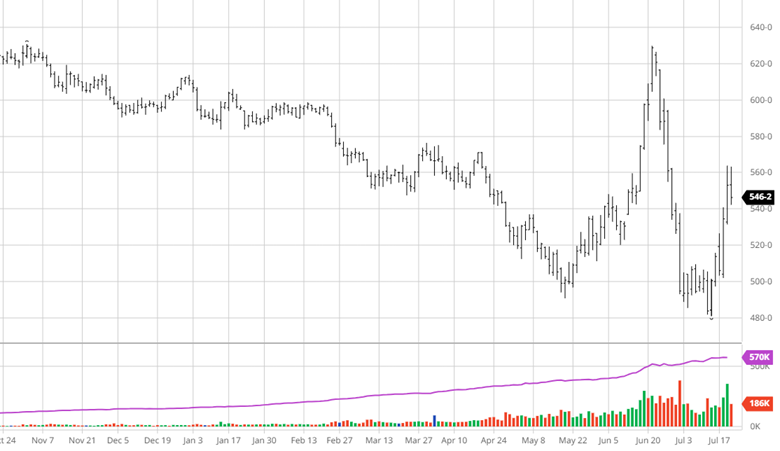

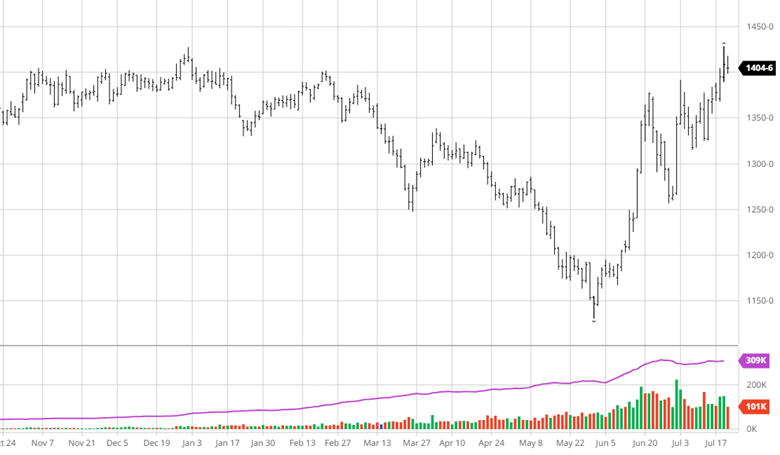

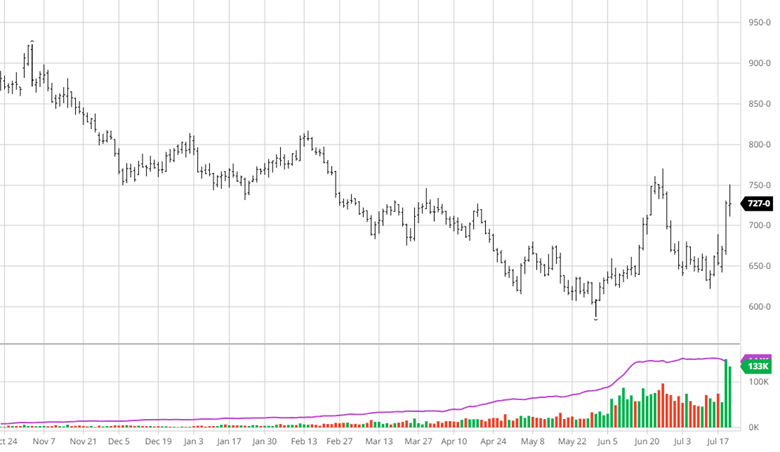

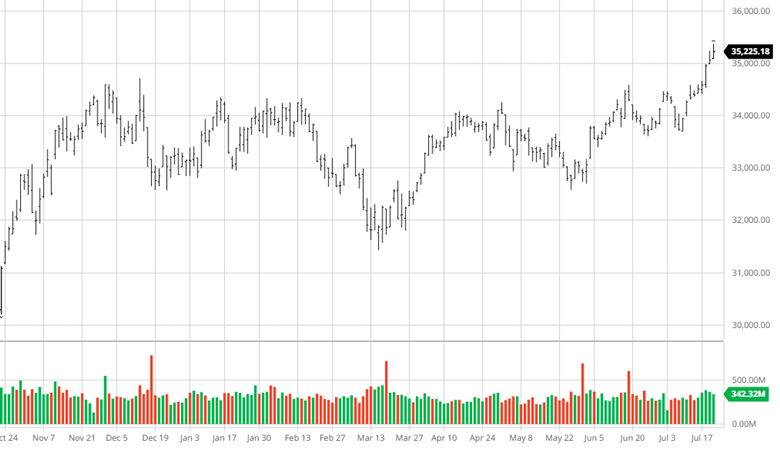

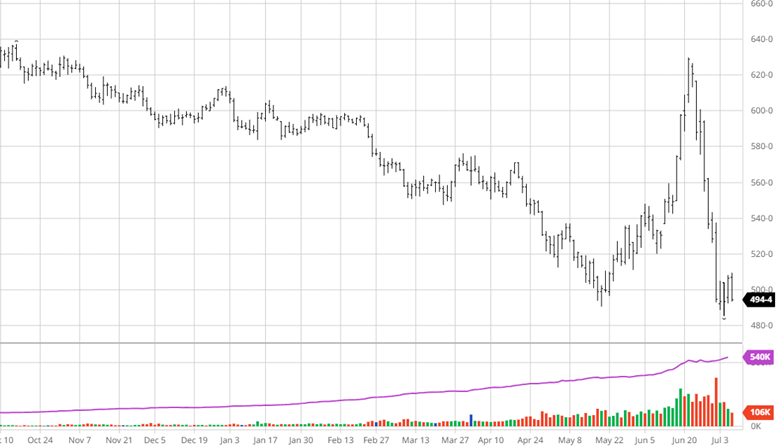

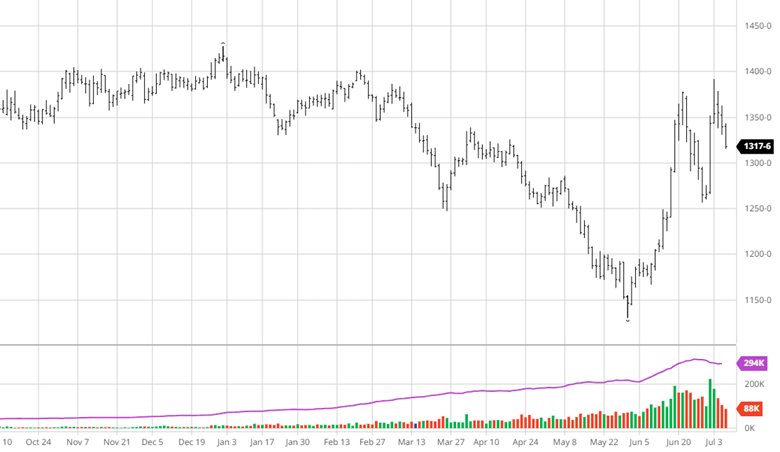

The futures markets fell another $19.50 as a weak cash market dominated. The makeup of the trade was the funds selling while the industry bought back shorts or got long. In this part of the cycle, all the focus is on the cash market. I am surprised at the extent of the erosion. In a hurry to raise prices, the mills did not establish a base level. The chase is on to find that level. The futures guys are hoping for a lessening of the fund selling next week could bottom futures. While I agree, it could be a tough week ahead.

Factors:

The struggle continues to determine the value of this commodity. The factors affecting the price are less production out of Canada—the slowing of Euro shipments, and the JIT inventory management strategy. The demand data shows a steady pace of construction, and reports from the field are of a good wood flow. Under these conditions, the commodity’s price will remain at or above breakeven. The reality is that the price continues to drift into the red for the mills. The lower price is also digging into the margins of most of the industry. The Milton Freeman School of Economics says that inflated profits are met with long-term deflation. That may be the easy answer here.

We have to go back to the actual supply and demand factors. The supply gap in housing continues to widen as family formation outpaces construction. There are limits to construction. Labor and government regulations are extending the timeline of all buildings. That lag is very positive long-term for housing. I did see something thought-provoking for the first-time home buyer. Here goes…

The first-time home buyer has roughly $100,000 saved for a down payment on a $350,000 home. These are estimates based on today’s data. If the buyer does an analysis, they see that they are earning 6% on $100,000 today. Buying a home, they would have $250,000 debt at roughly 8%. That is the 7.5% mortgage and the additional home expenses. Now the appreciation of a home averages 5% historically. At 8% the buyer loses 3% a year. If they do not buy a home, they make 6% on $100,000 with potential saving increases.

Summary:

This year’s actions of the lumber market highlight an industry preparing for less demand. While there isn’t data confirming a downturn, the marketplace stays guarded. I did look for less demand by the third quarter. I also looked for less supply to offset the decrease. This market doesn’t react that smoothly. At some point, the multifamily sector will show a slowing. Then the single-family sector will see a pause. In a JIT environment, prices will remain under pressure. That could be around for a long time. The good news is the market will continue to get caught short. The middle of the market can continue to benefit from those spikes.

Daily Bulletin:

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

Commitment of Traders:

https://www.cftc.gov/dea/futures/other_lf.htm

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

312-761-2636