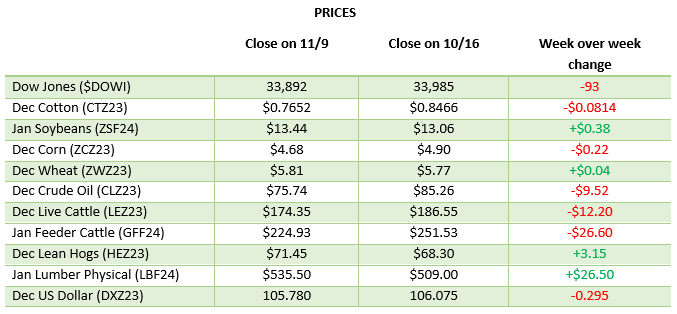

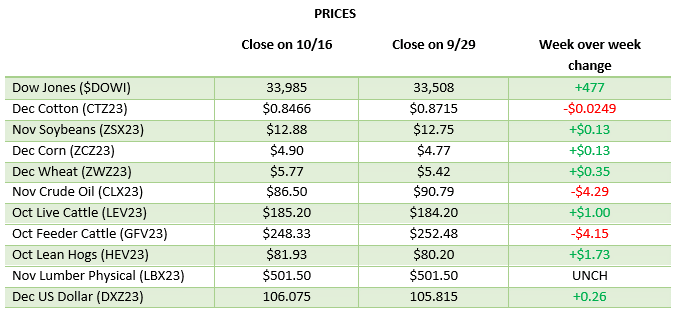

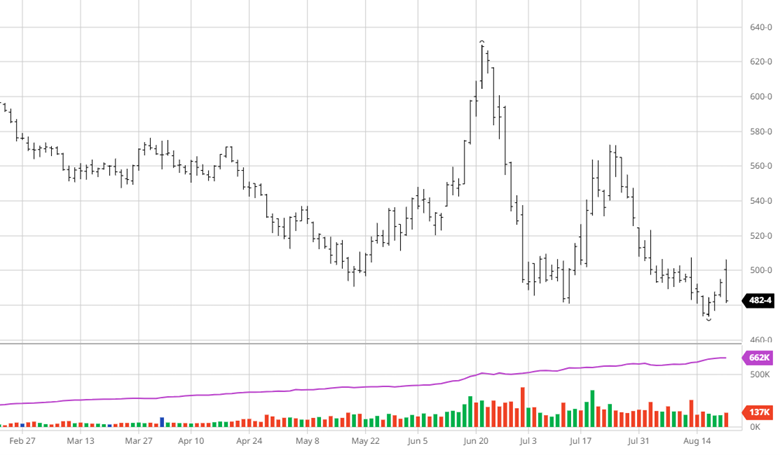

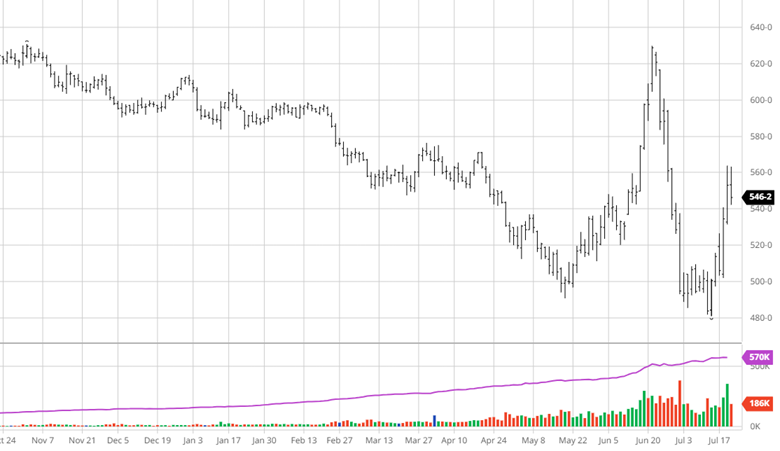

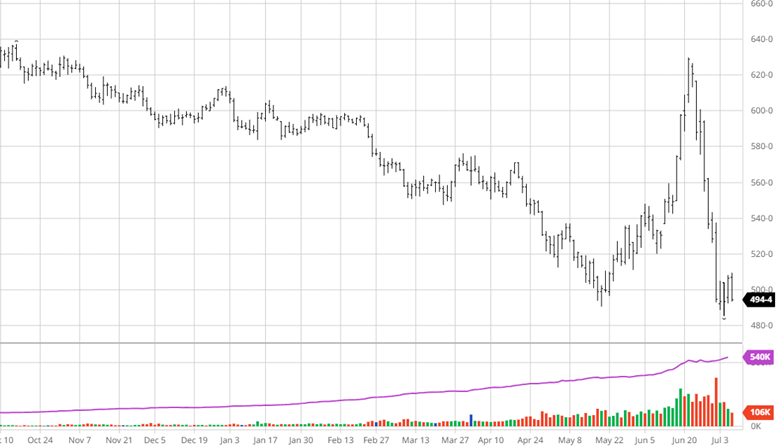

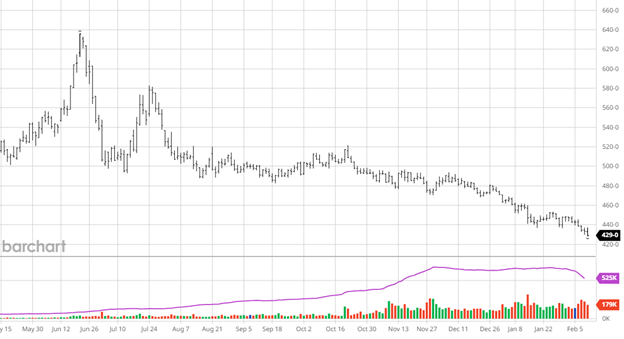

Corn has had a rough 6 months and continued lower with bearish sentiment and funds being short. The USDA report had higher Brazil corn production than the CONAB numbers by 10.25 MMT. The market has been looking for any good news to help put a floor in and that has not materialized. The one bright spot in exports is that we are ahead of pace to both Japan and Mexico for the year while China’s demand has been poor heading into the Lunar New Year. The USDA report pegged 23/24 US corn stocks at 2.172 billion bushels, close to the pre-report estimates.

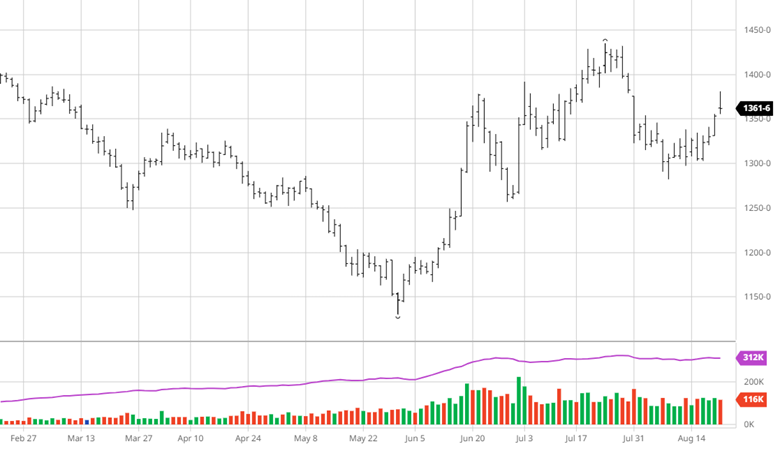

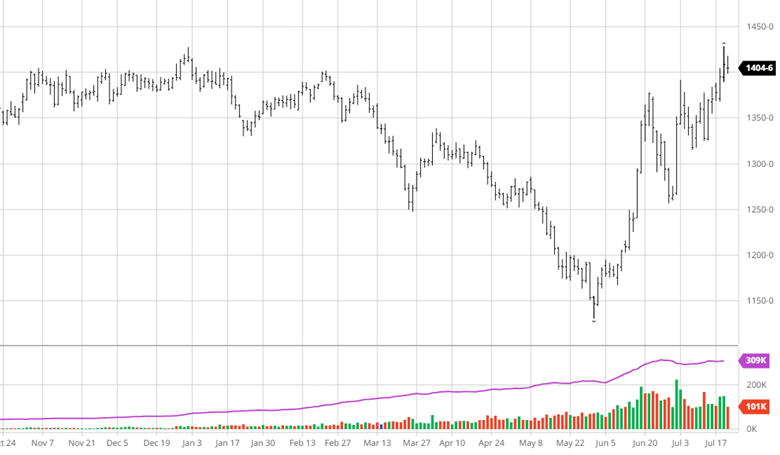

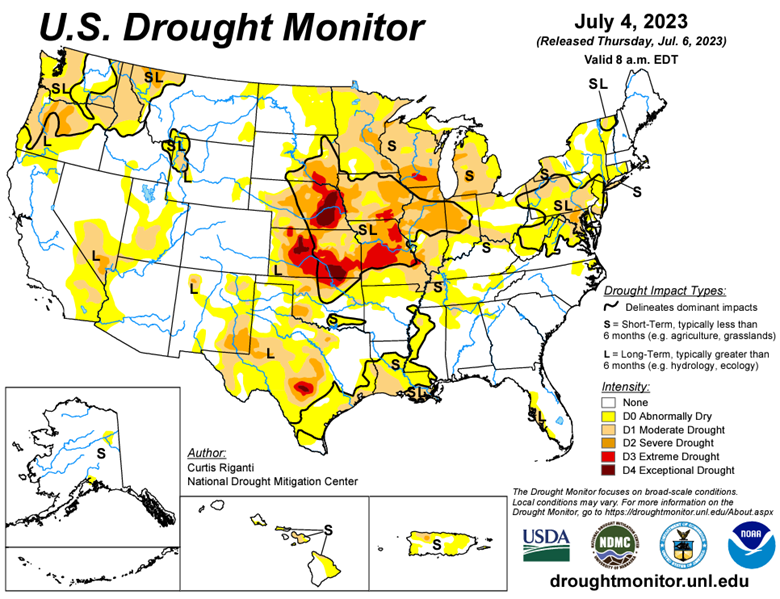

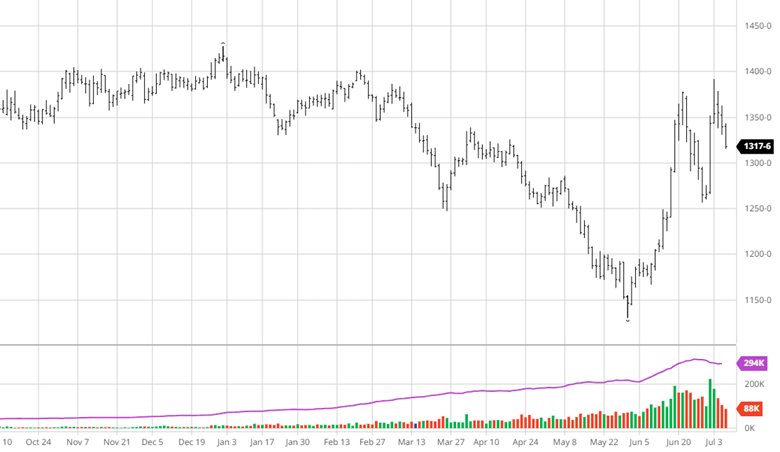

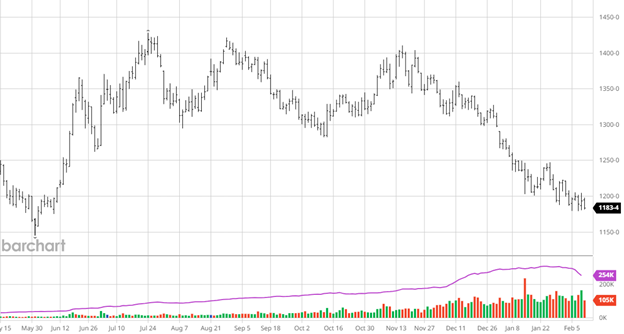

As bad as the news, or lack of news, for corn has been, the news for beans has been worse. In this week’s USDA report the US bean stocks came in at 30 million bushels higher as exports struggle. Brazil bean production came in above expectations as well with a 156 mmt production (trade estimate of 153.15mmt). With a quiet period occurring during Chinese Lunar New Year it is unlikely to see strong exports and weather is neutral to bearish in South America.

Equity Markets

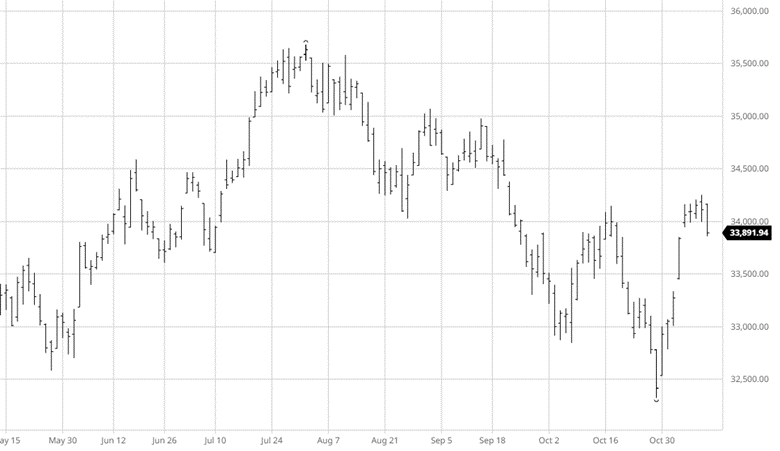

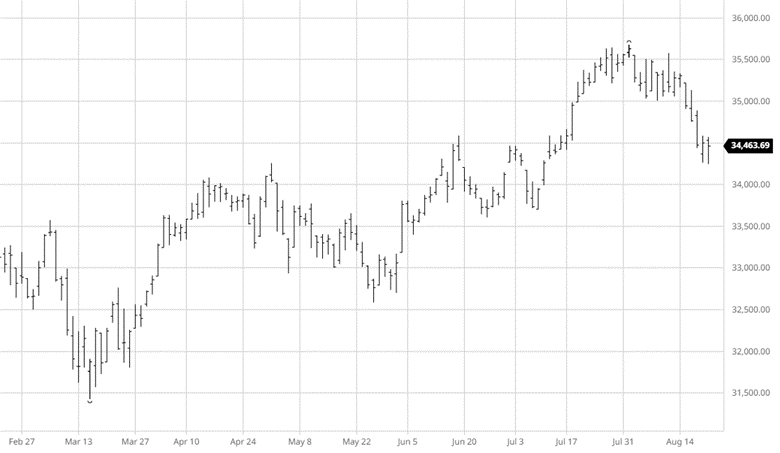

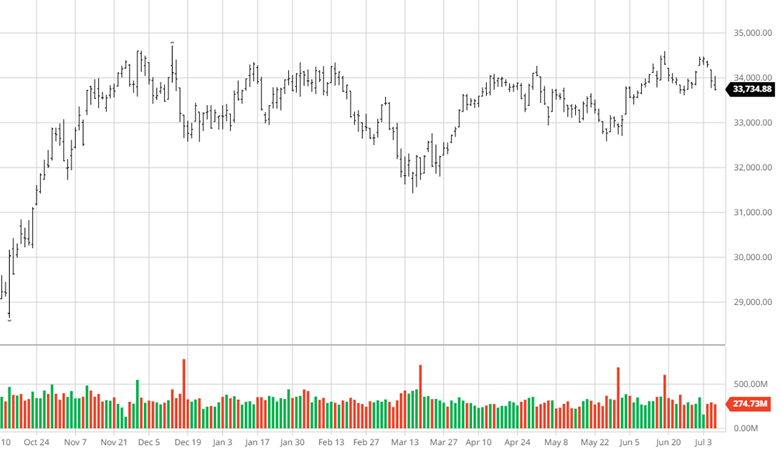

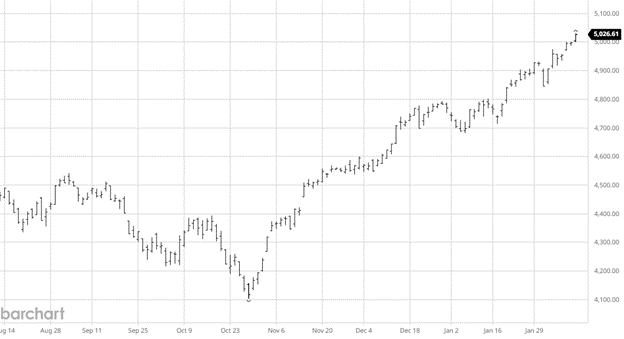

The equity markets continue to climb as the S&P 500 closed over 5,000 for the first time on Friday. The market has been pulled higher by the same stocks that have gotten it to this point in the magnificent 7 and AI stocks rallying. Analysts are debating whether the rally should broaden in 2024 or remain top heavy as it has started. The Fed will likely keep rates where they are until at least the summer.

Other News

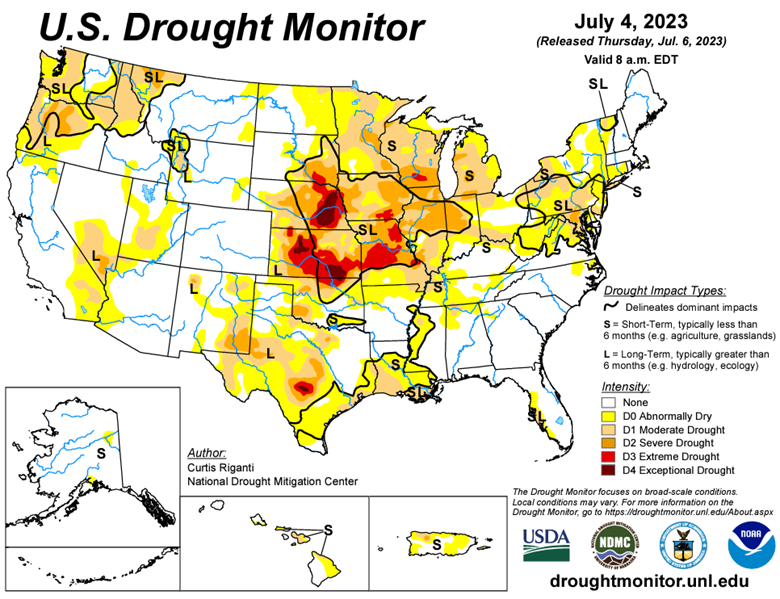

- The bearish USDA report continued to weigh on the markets as South American production came in above expectations, still higher than many private estimates.

- Thanks to Chip Flory and Davis Michaelson for having Jody Lawrence on their internationally known and critically acclaimed AgriTalk radio program last Friday. Here is the link.

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.