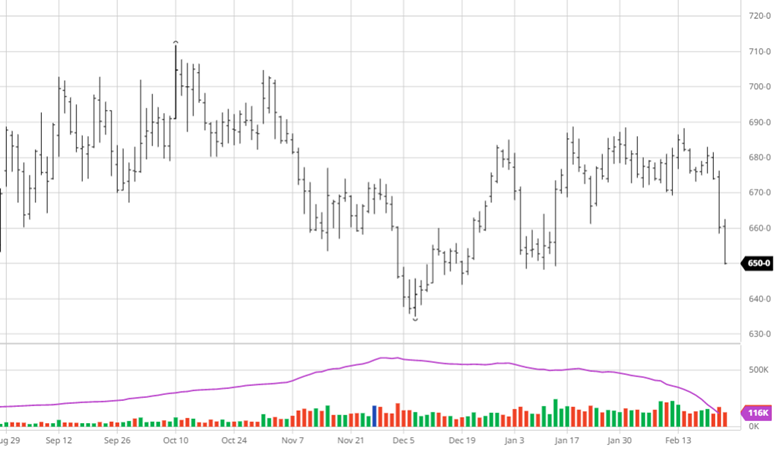

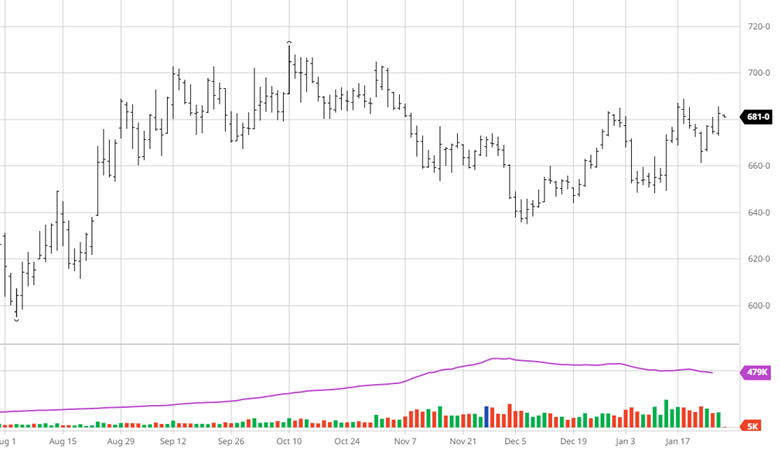

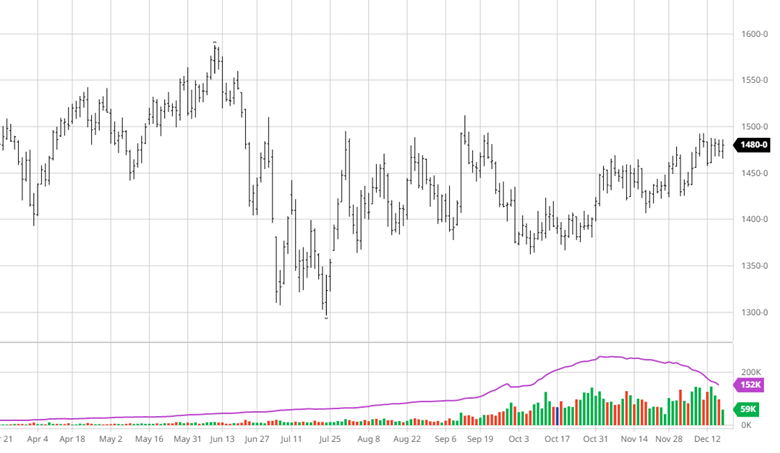

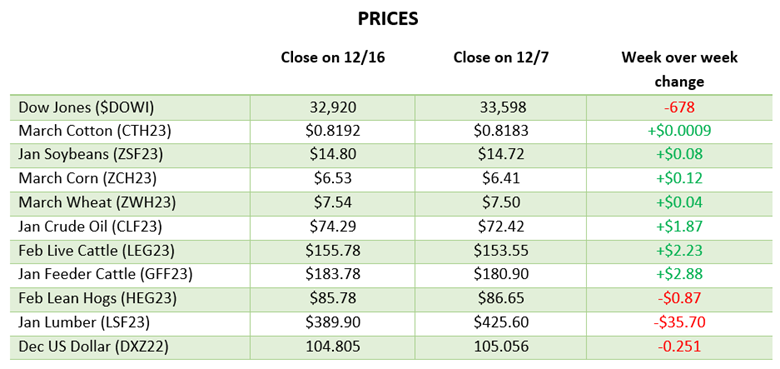

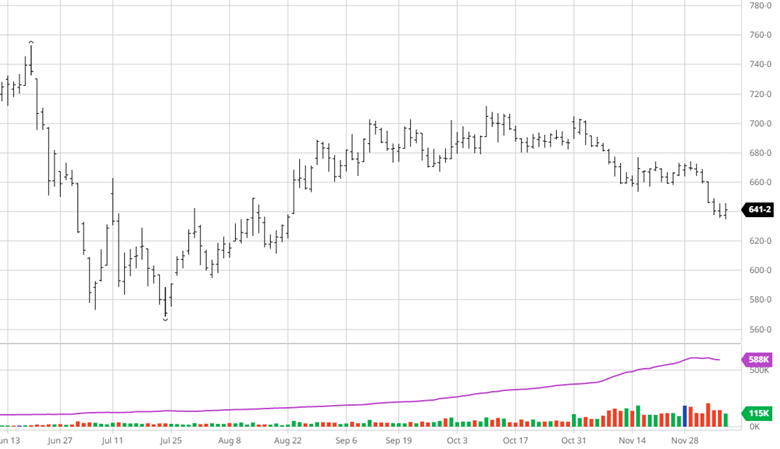

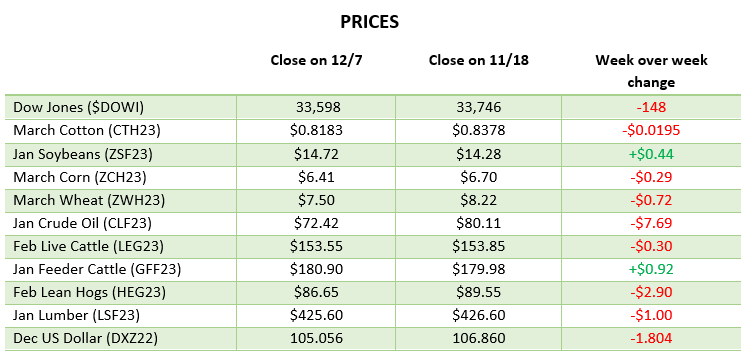

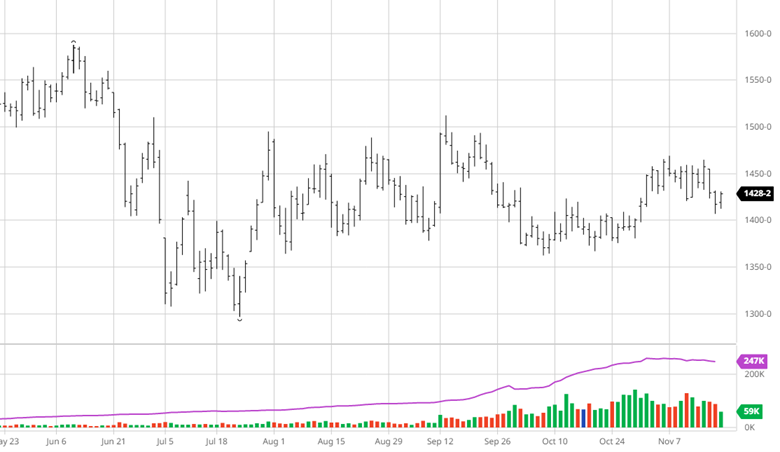

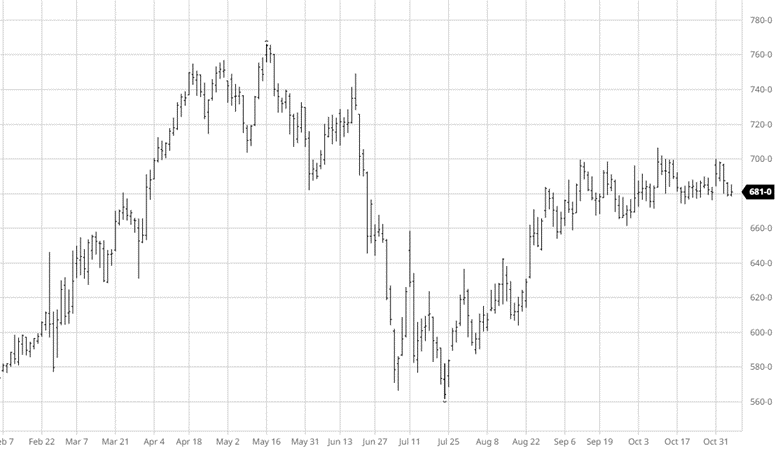

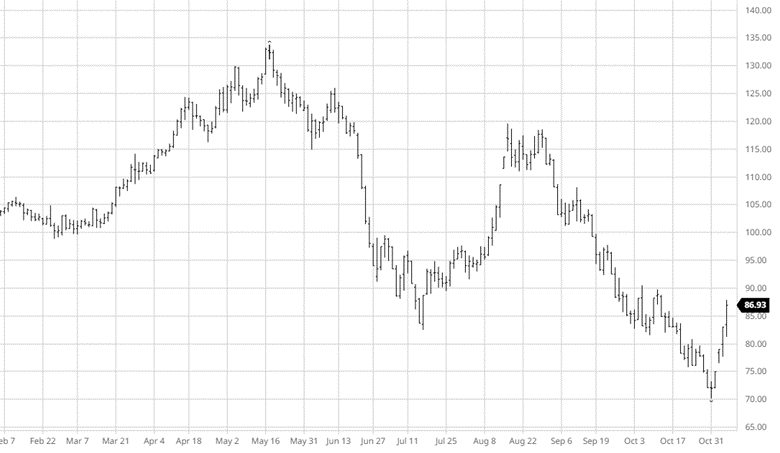

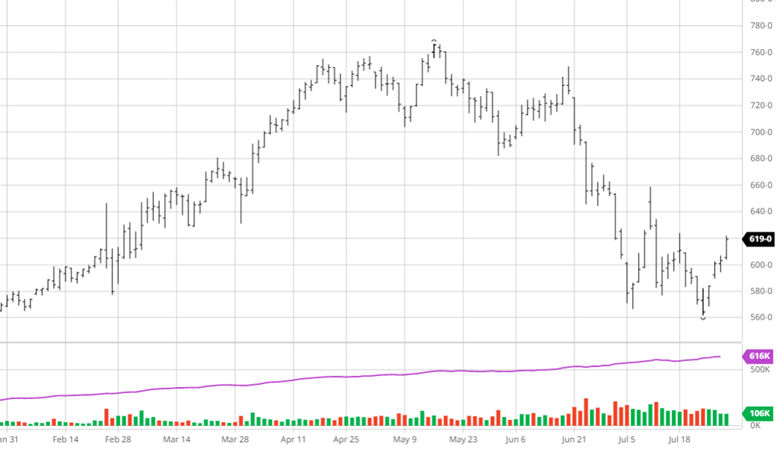

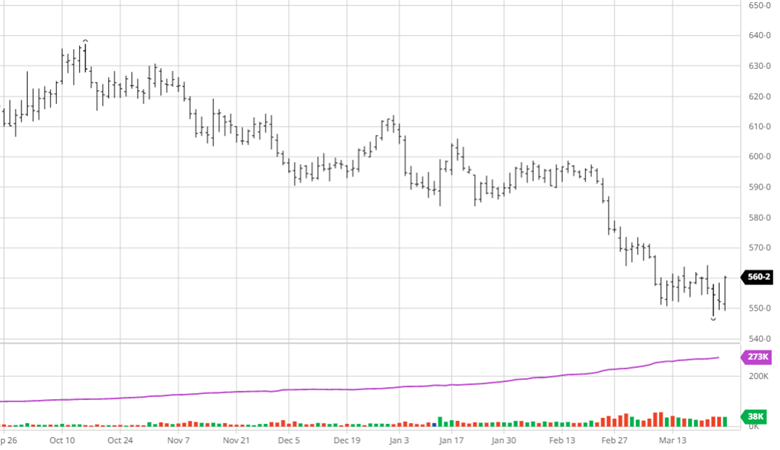

Corn leveled out over the past couple weeks after its move lower into the mid $5 range. Good exports and continued problems in Argentina have been able to keep corn from moving any further lower while funds continue to offload long positions. Corn will continue to trade here until the prospective plantings and quarterly stocks report on the 31st that will play a role in its next move. There could be surprise news that gives it a bump higher or lower but for overall directional change something surprising would need to be in the report. How the USDA adjusts for further losses in Argentina and unpredictable world demand will be two questions to look for in the stocks report.

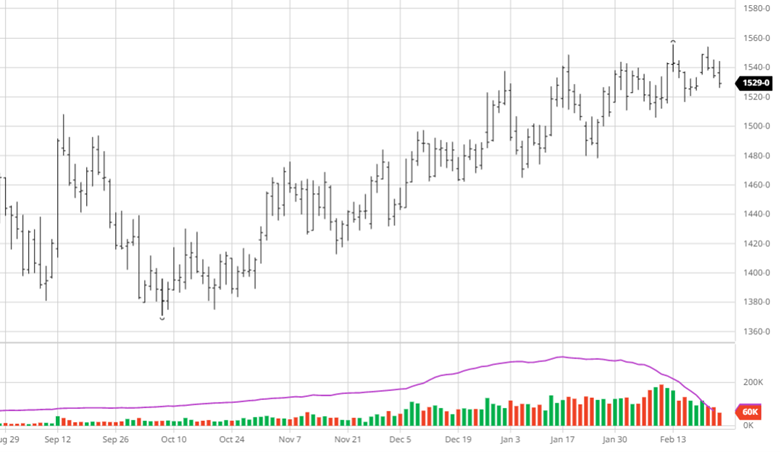

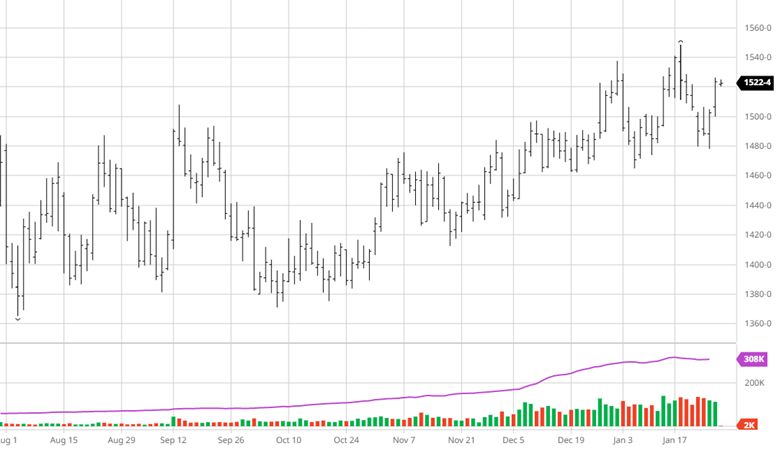

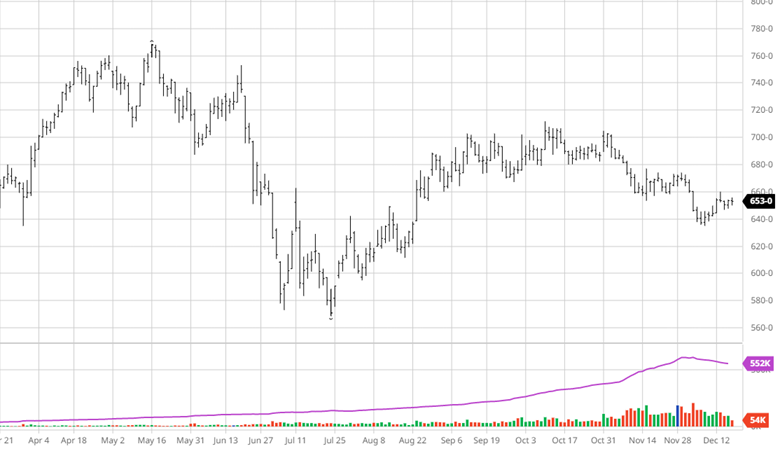

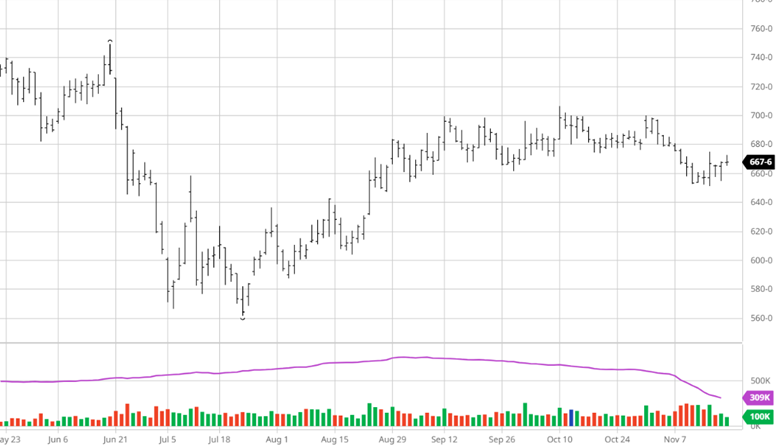

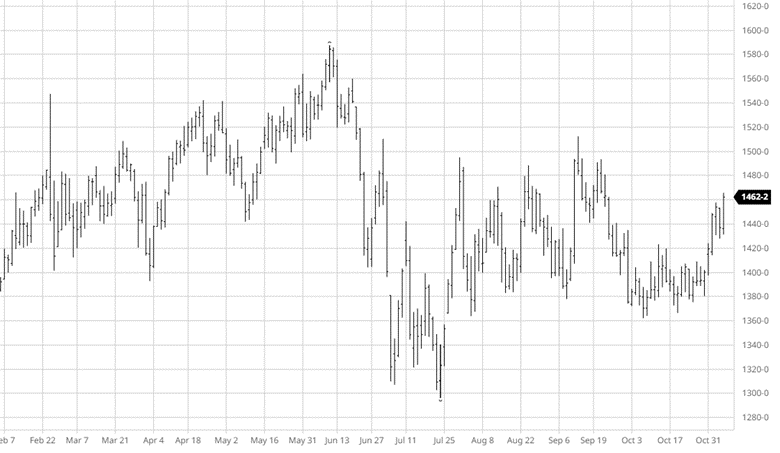

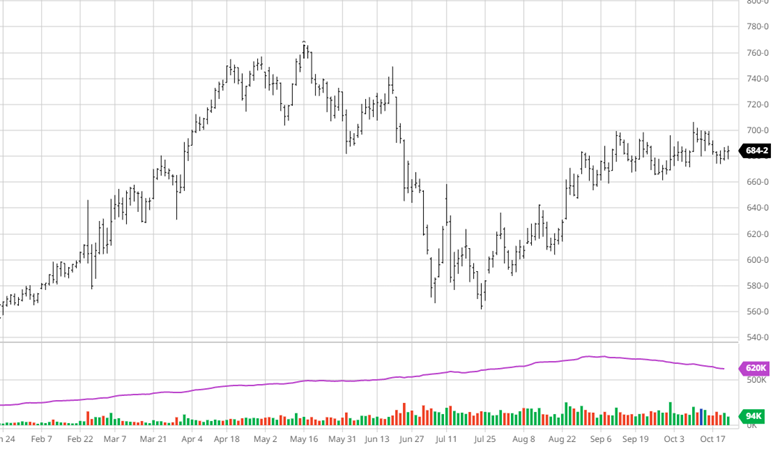

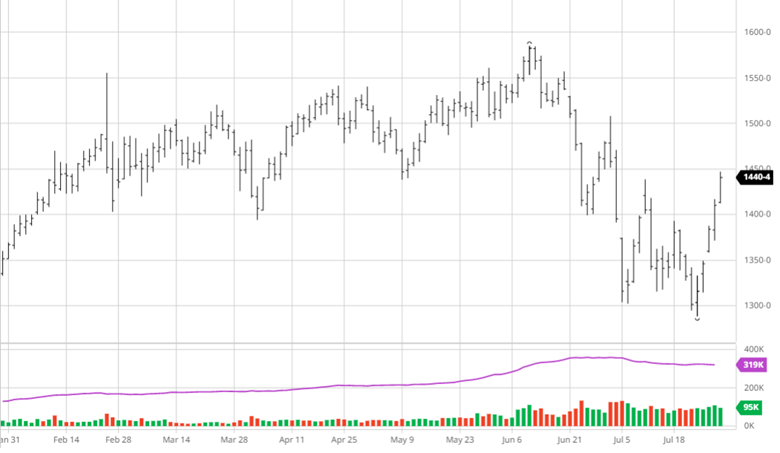

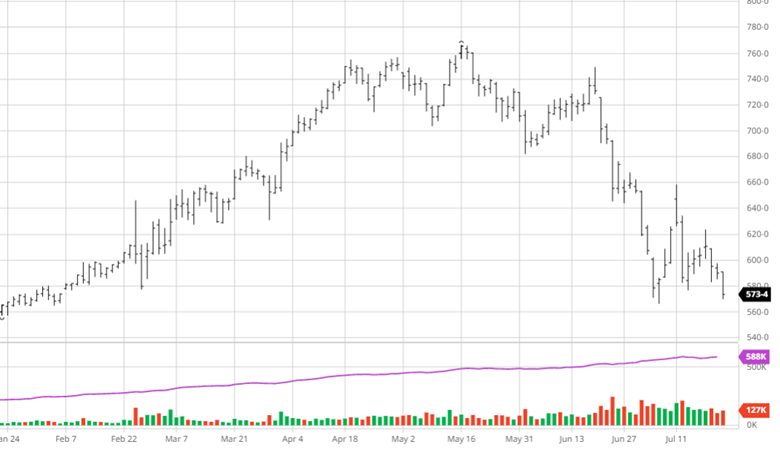

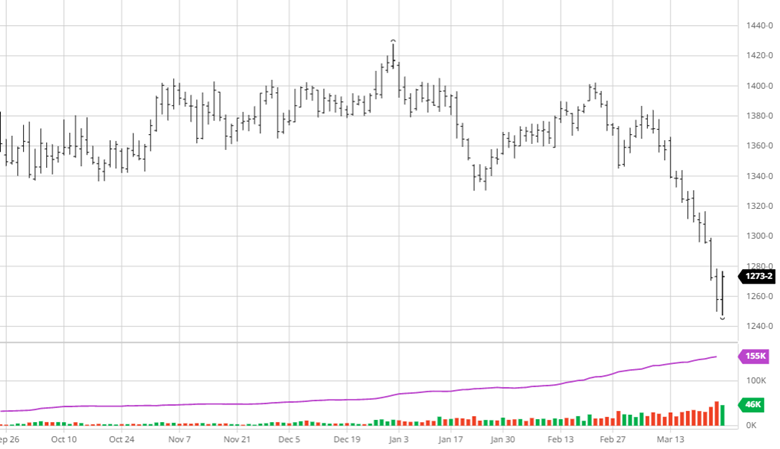

Soybeans finally caved and followed corn and wheat lower after putting up a good fight. Brazil’s record bean harvest is under way and with insufficient storage they have to get rid of them driving prices lower to keep US beans even remotely competitive. Like corn the funds are legging out of their long held long positions making the moves sudden and large. Beans saw a nice bounce to end the week making up for Thursdays losses. One would expect the markets to calm down a little next week as the report looms large for any further downward pressure or welcome support.

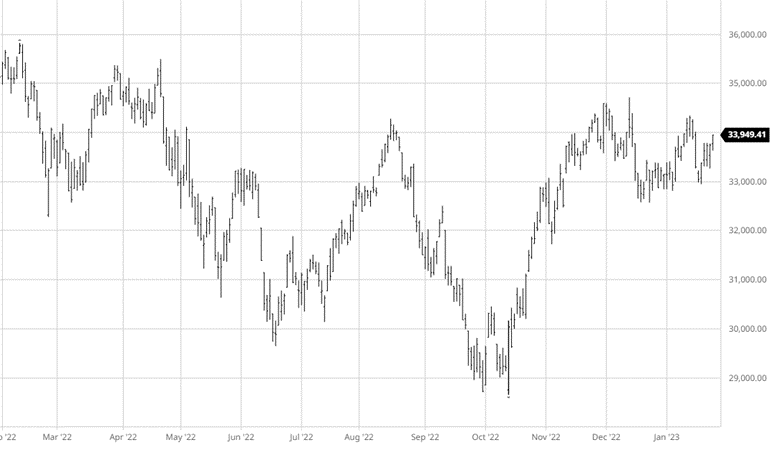

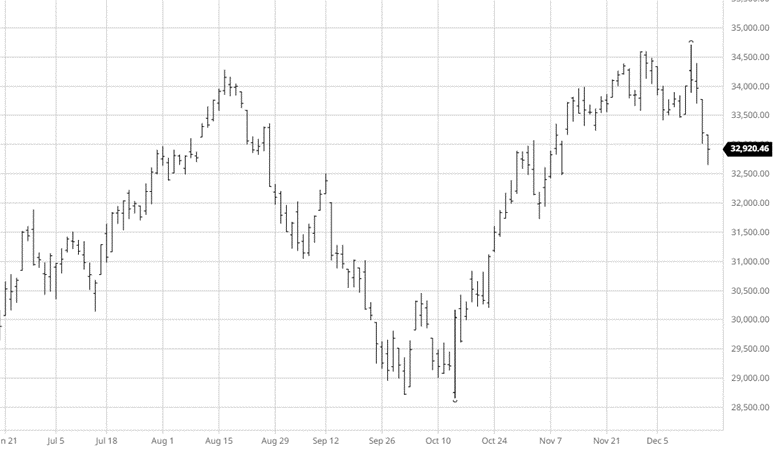

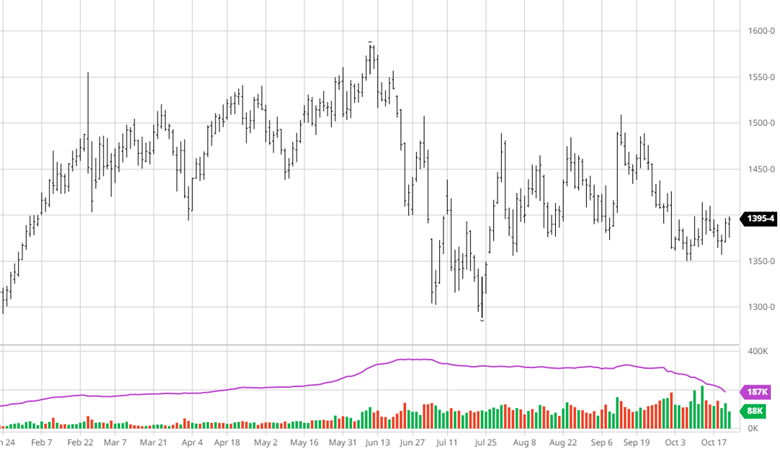

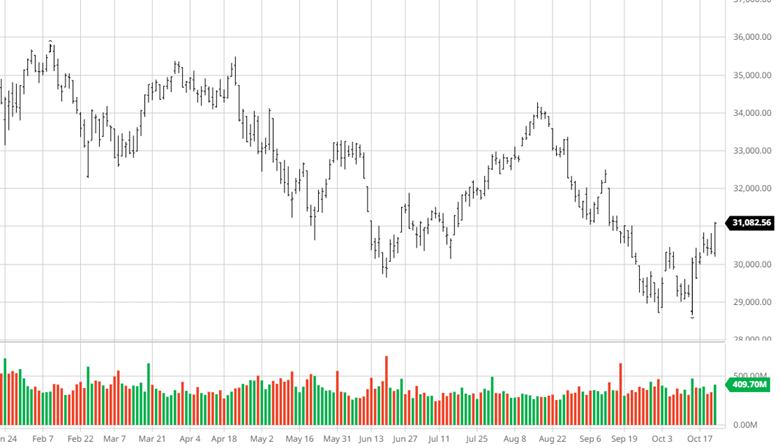

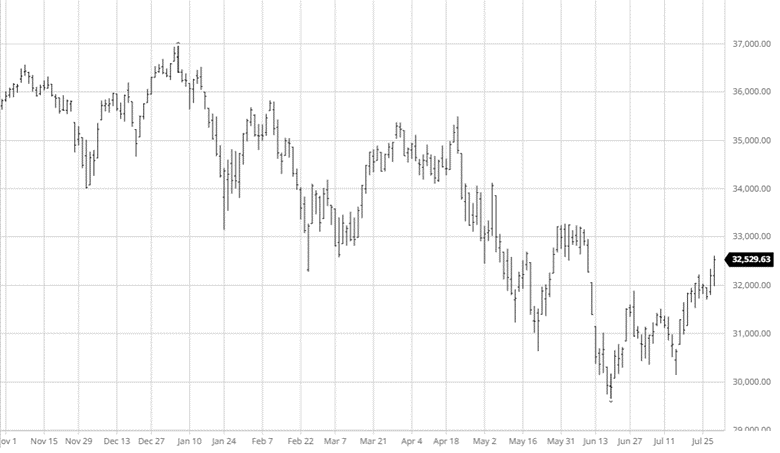

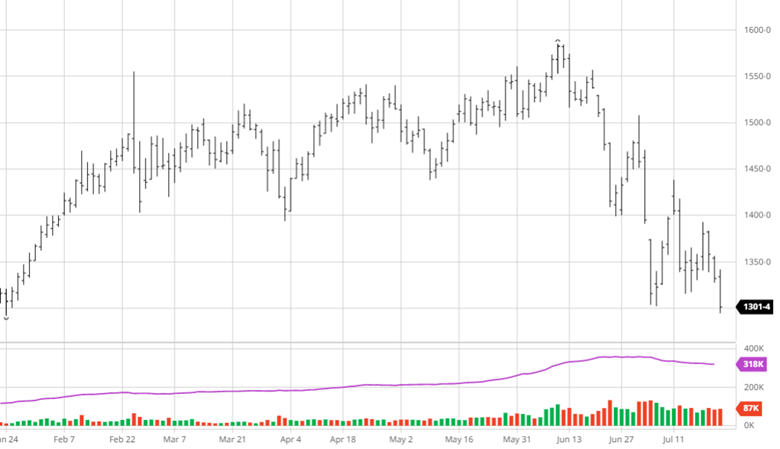

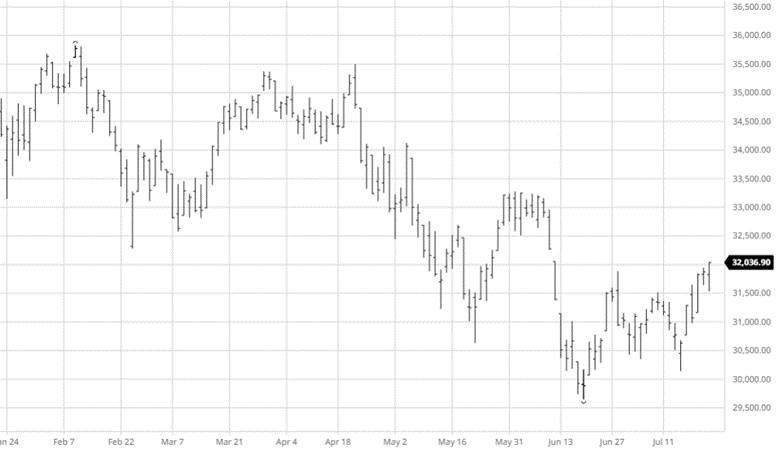

Equity Markets

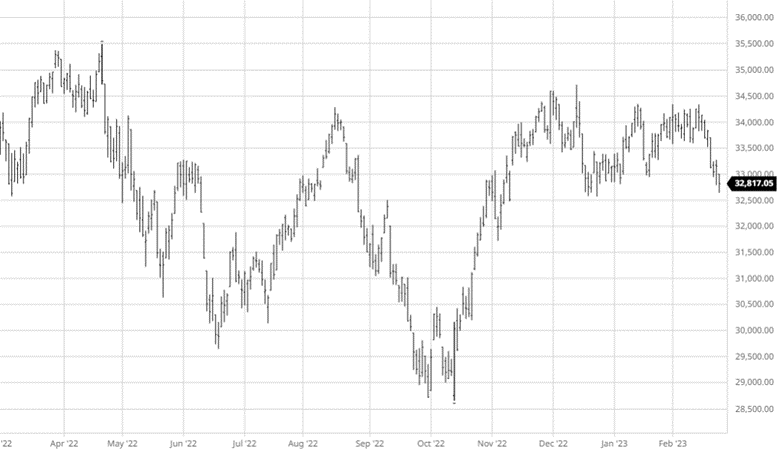

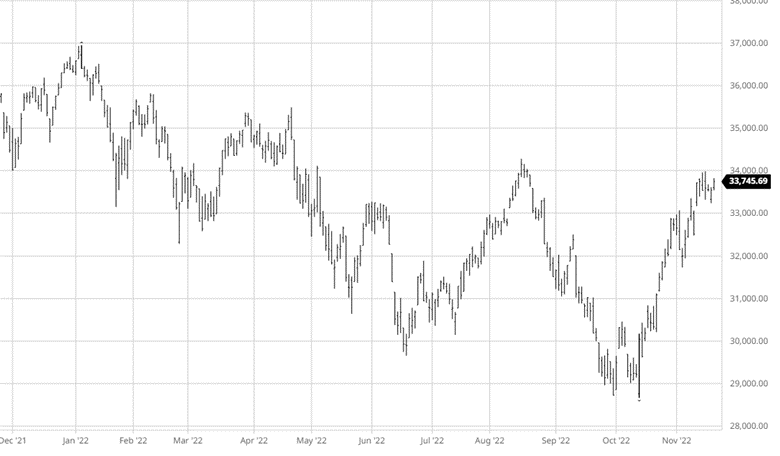

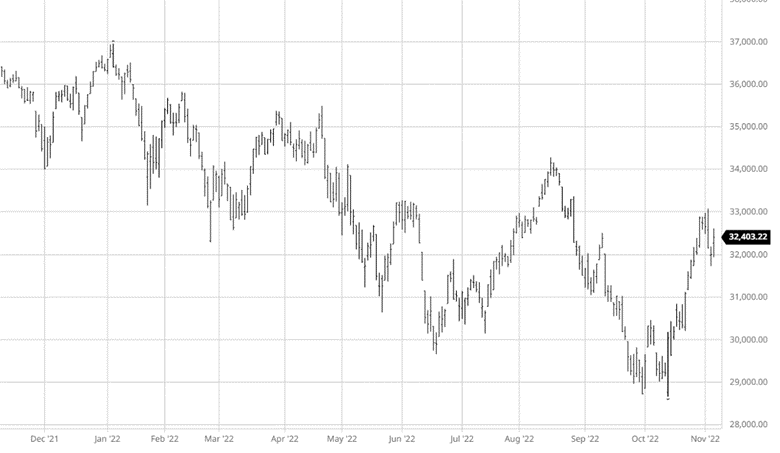

The markets continue to be confused as they look for guidance that does not appear to be coming. Sec. Yellen this week flipped back and forth on whether or not they would increase deposit insurance for a period of time to help calm fears while the Fed went ahead with its 25 point rate hike. The banking issues make analysts think the Fed could cut rates before the end of the year helping tech stocks but ultimately the Fed likely wont cut rates until we are in a recession.

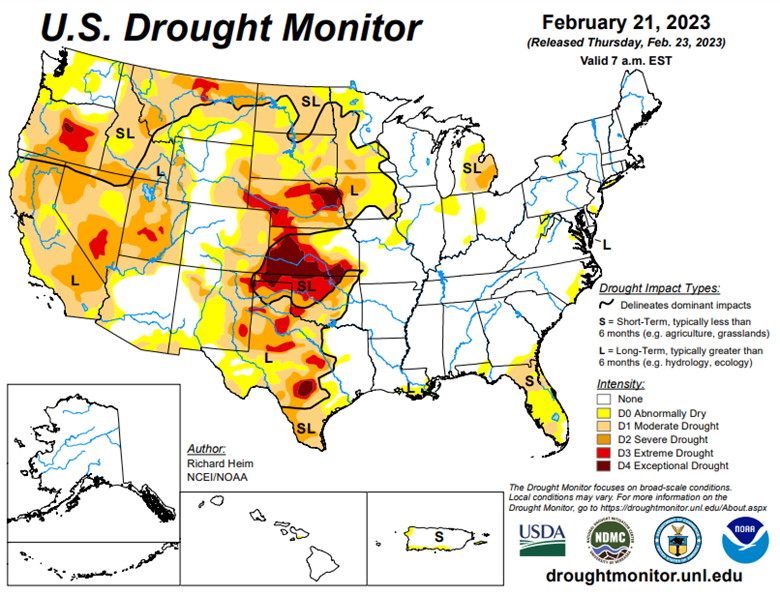

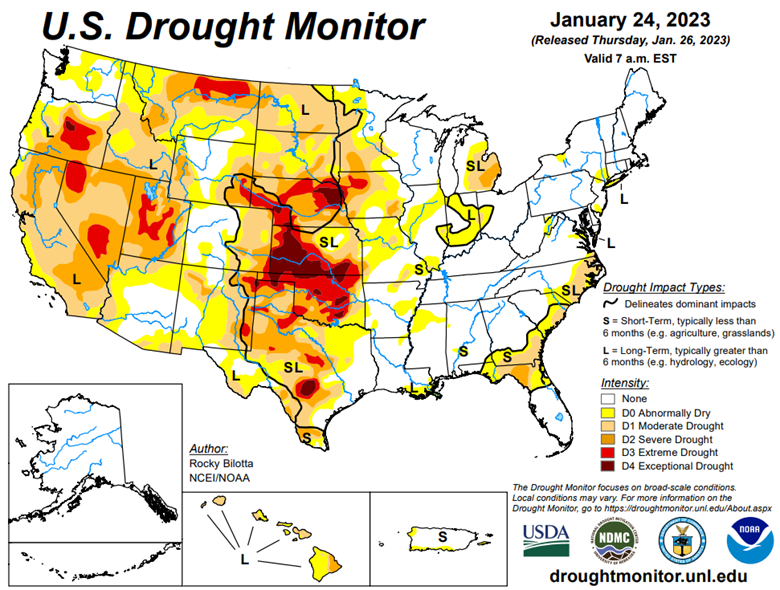

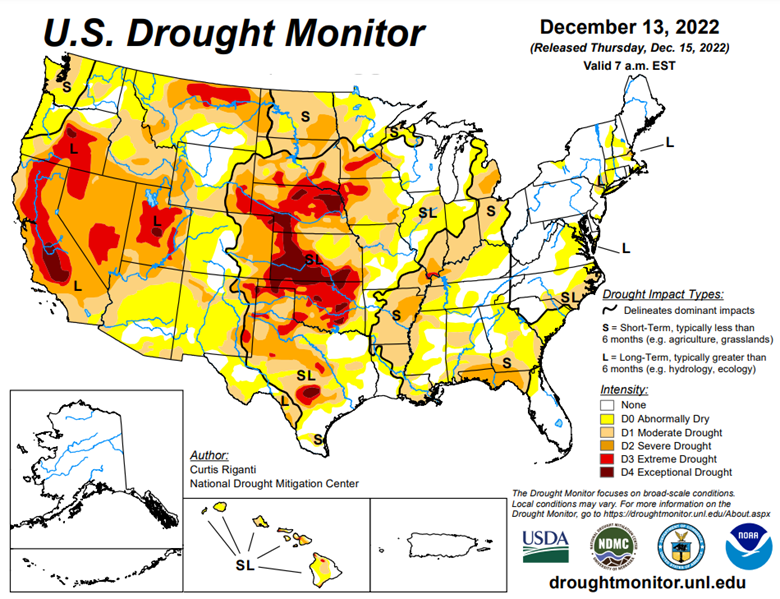

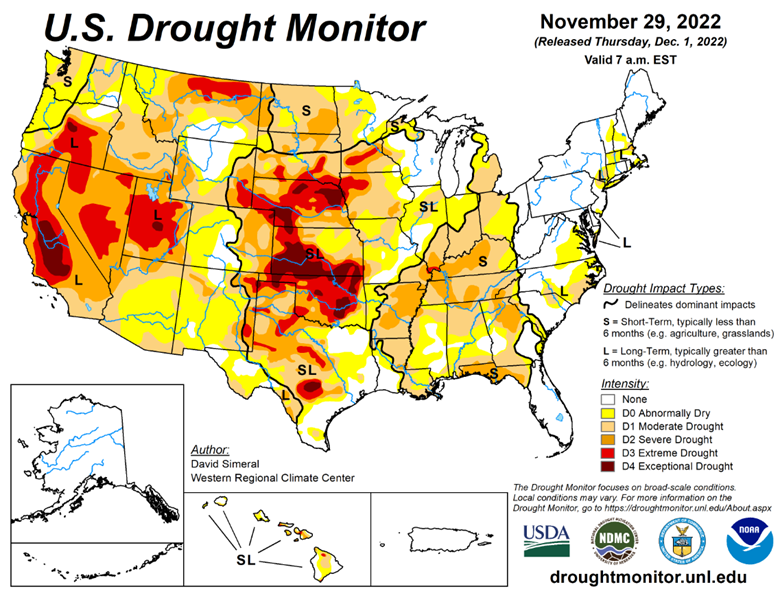

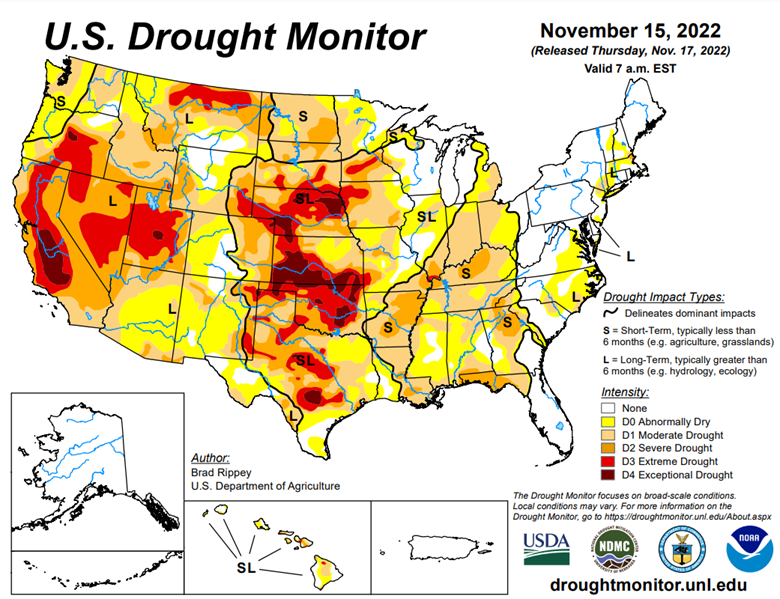

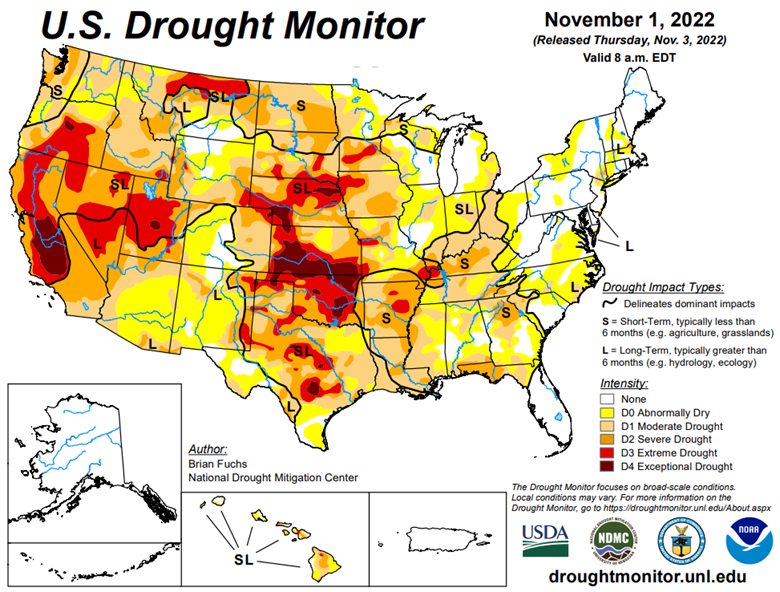

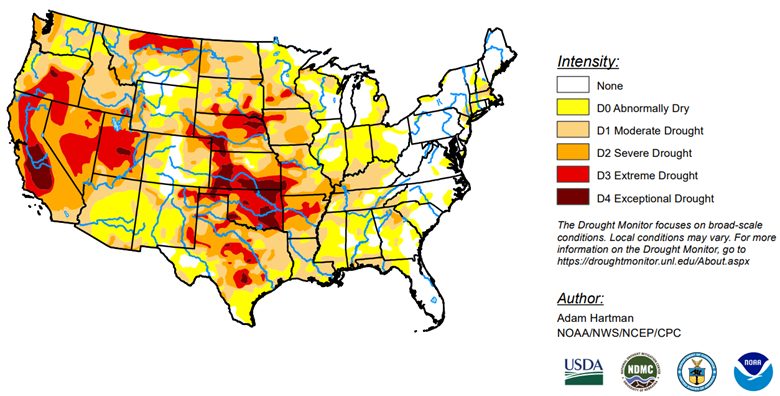

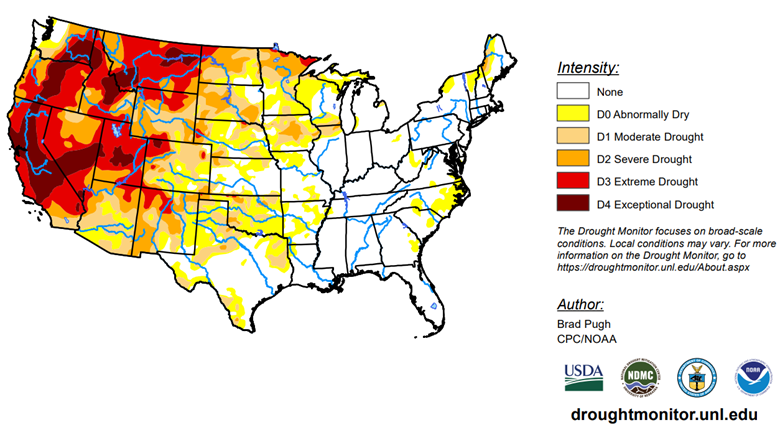

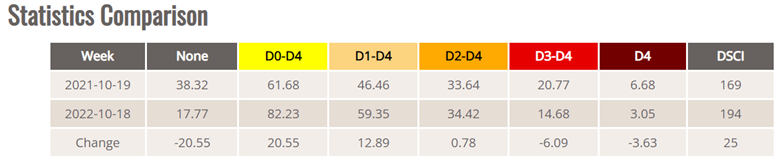

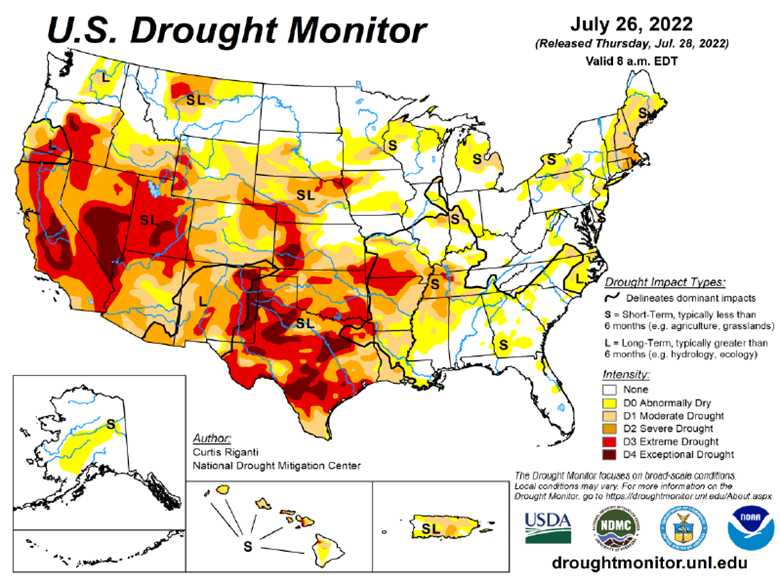

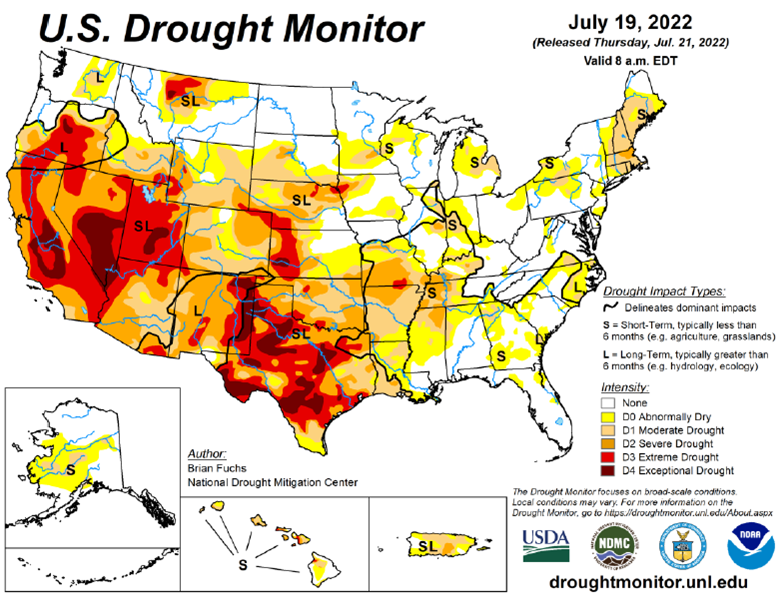

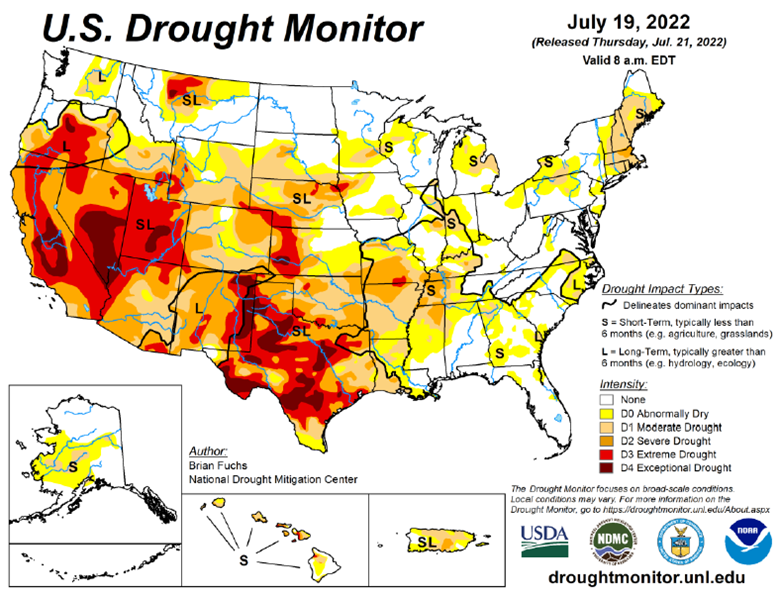

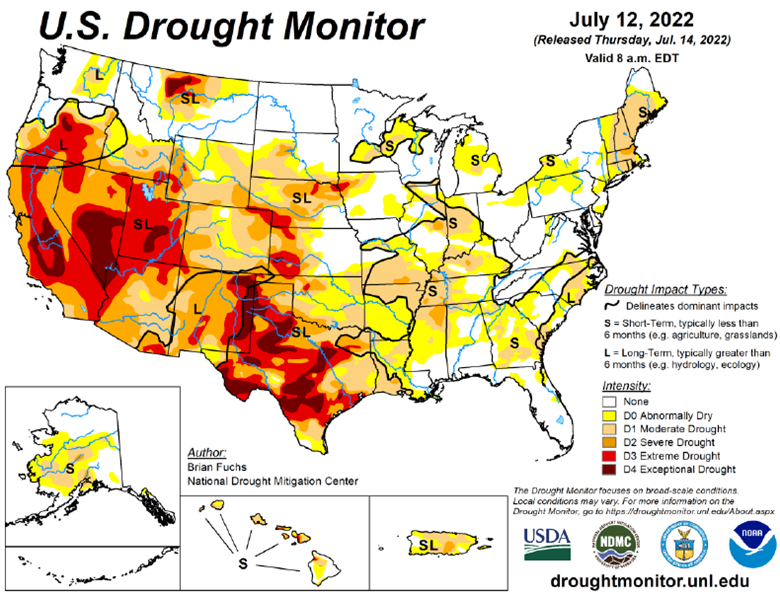

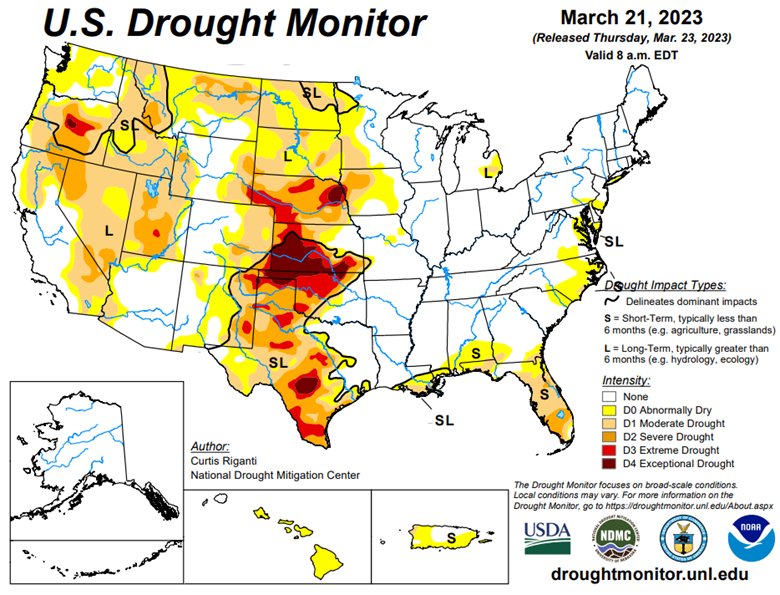

Drought Monitor

The eastern corn belt has gotten plenty of moisture so far this winter with the western corn belt needing more heading into the spring.

Podcast

With every new year, there are new opportunities, and there’s no better time to dive deeply into the stock market and tax-saving strategies for 2023 than now. In our latest episode of the Hedged Edge, we’re joined by Tim Webb, Chief Investment Officer and Managing Partner from our sister company, RCM Wealth Advisors. Tim is no stranger to advising institutions and agribusinesses where he has been implementing no-nonsense financial planning strategies and market investment disciplines to help Clients build and maintain wealth and reach financial goals since

Inside this jam-packed session, we’re taking a break from commodities, and talking about the world of equities, interest rates, tax savings, and business planning strategies. Plus, Jeff and Tim delve into a variety of topics like:

- The current state of the markets within the wealth management industry

- Is there a beacon of hope, or is it all doom and gloom for the markets?

- Other strategies to think about outside of the stock market and so much more!

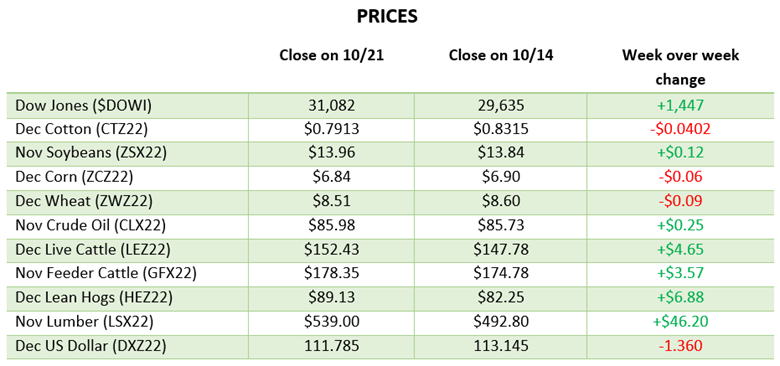

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.