AG MARKET UPDATE: JULY 21 – 28

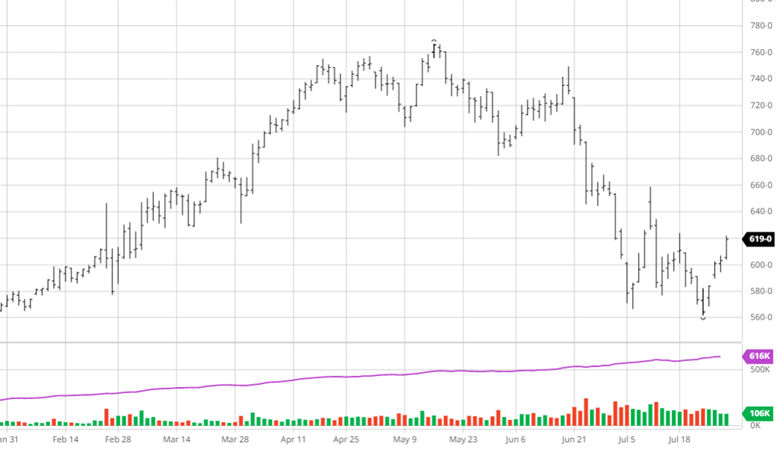

Corn bounced back this week as hot and dry August forecasts returned across the western corn belt, and eventually are forecasted to move east right in the middle of pollination. To be clear – hot and dry while pollinating is less than ideal. In addition, the weekly crop ratings came in lower with the national good/excellent ratings estimates at 61%. Ratings have lowered 6% in the last month, and with the current forecast this trend is likely to continue. All these factors together, along with a weaker US dollar, helped the rebound for the week. While this turnaround has been nice on prices, the yields are a concern, and it will continue to be important to monitor pricing into the weekend and start of trade on Sunday.

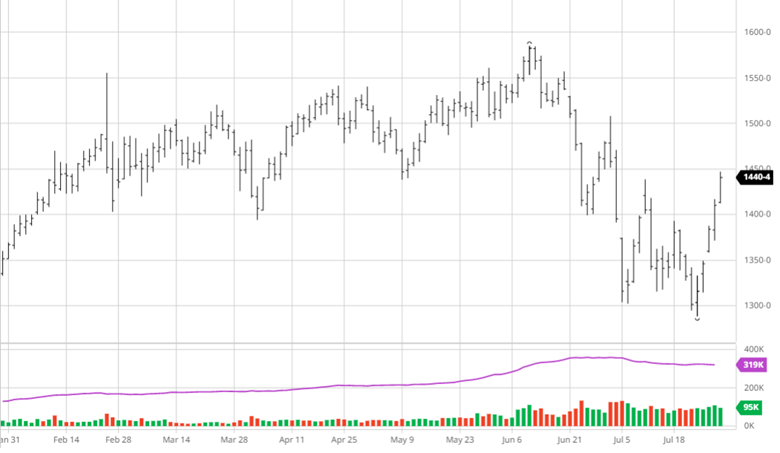

The forecast change has also been supportive of bean prices as August is an important month for yield development. Soybean supply and demand has been tighter over the years and if we lose 1 or 2 bushels in national yield it will result in a big hit to world supply. September beans traded over the $15 mark for the first time in a month with this week’s gains. The November contract has the potential to reach back over $15 with the current momentum, assuming no new bearish forecast changes over the weekend. Soybeans good/excellent ratings came in at 59% nationally, following the worsening trend that corn has had, losing 4% g/e in July.

Russia and Ukraine

Reports were that Russia and Ukraine had agreed to a safe export corridor, and then…. Russia bombed another port (imagine that)… so that did not last long. Russia wants any obstacles to Russian agriculture exports to be eliminated, which seems unlikely. White House spokesman John Kirby either majorly misspoke or lied this week claiming that there were 80 ships ready to leave the ports with 20 million tons of Ukrainian grain. The largest grain shipping vessels can only hold about 60,000 tons so if there are 80 ships. Quick math here = they will only be able to ship 4-5 million tons. Luckily this did not spook the markets as traders knew this to be the case with SovEcon saying there are no more than 10 such ships ready to ship grain. The mines remain in the shipping corridors and this conflict will continue to drag out through the summer.

Equity Markets

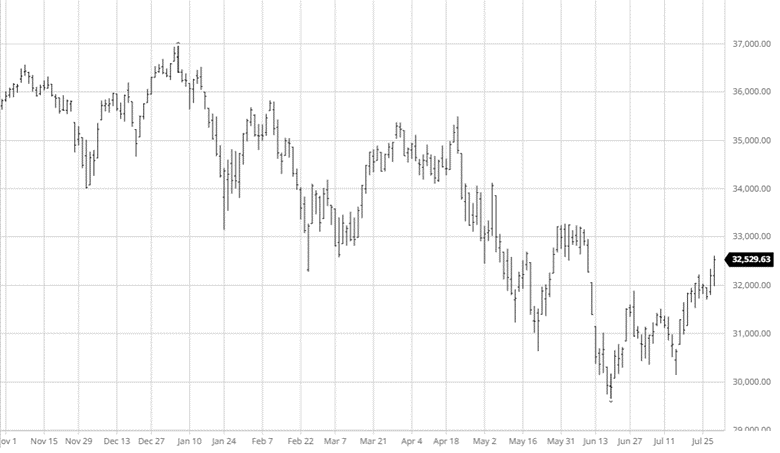

The equity markets had a good week following a few down days with some strong earnings and some misses. The Fed unsurprisingly raised rates 75 points this week leaving what comes in the next rate hike up in the air. The 2nd quarter GDP posted another negative number after posting a negative first quarter. Historically 2 consecutive quarters of negative growth signals a recession. There are lots of challenges right now with inflation still a major problem but with companies lowering guidance for the rest of the year the current economic slowdown may continue.

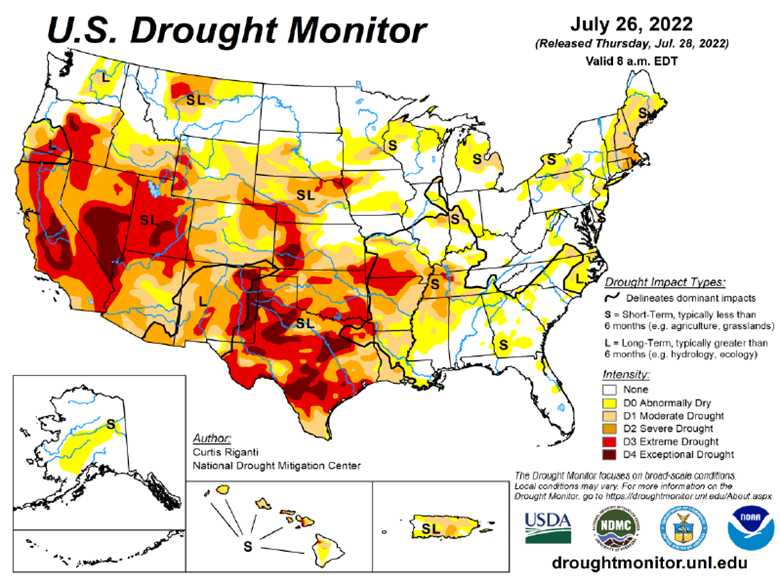

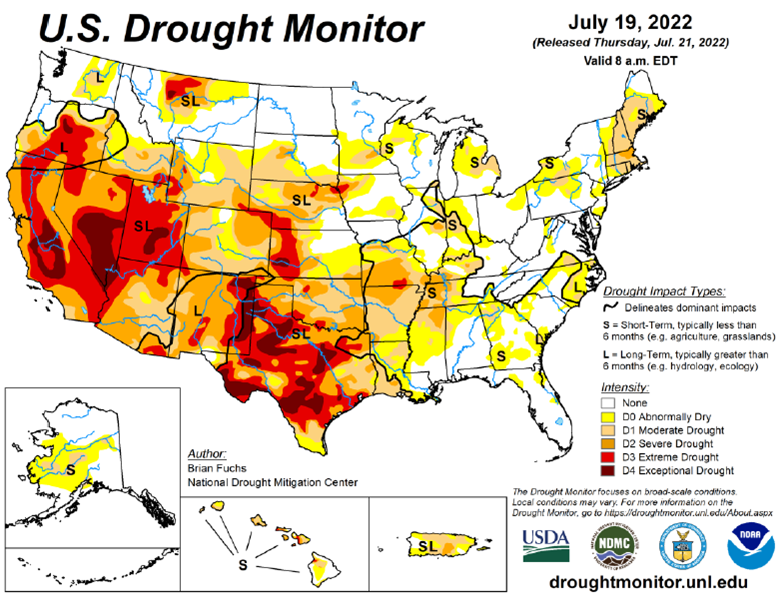

Drought Monitor

The drought monitor below shows where we stand week to week.

Podcast

Are the Fed’s hikes starting to dampen inflation? Oil, grains, and metals have all fallen from their highs. But the rarely spoken of Cotton market was one of the first to crack…falling from 1.58/lb to 0.95/lb in just a few short days. We’re digging into this sharp drop and just why and how Cotton is involved in seemingly everything with RCM’s very own cotton king, LOGIC advisors Ron Lawson.

In this episode, Ron is giving us the low down on how and why he believes it’s not Dr. Copper which acts as the global economic barometer, but how Cotton is the real Canary and leading indicator on global demand. In between those talks, we’re covering all things Cotton including crop insurance, irrigated vs dry land, the scam that was Pima and Egyptian Cotton, the process of cotton – which countries have it, which want it, ginning it, spinning it, dyeing it, global commodity merchant co’s pushing it around, and even micro-plastics, climate change, and how Cotton always flows to the cheapest labor source. Finally, we’re walking in some high Cotton putting Ron in the hot seat. Will we ever get the growth back? Tune in to get these critical hot takes — SEND IT!

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.