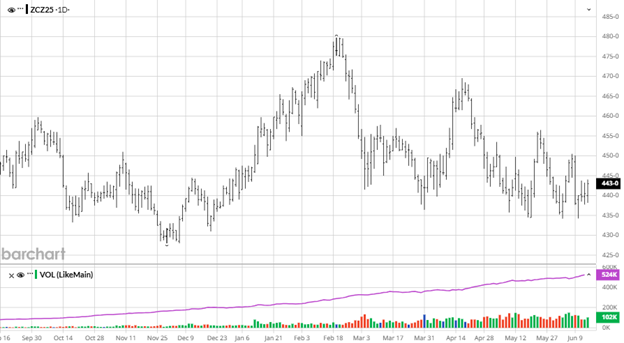

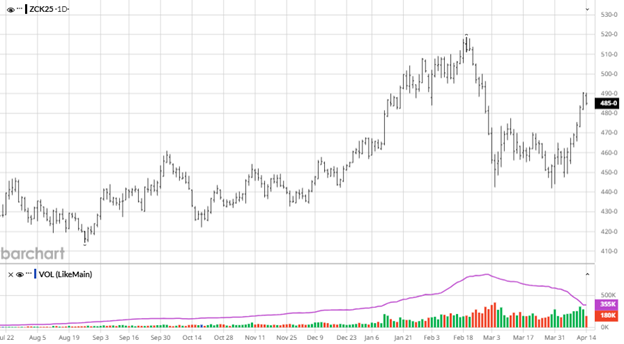

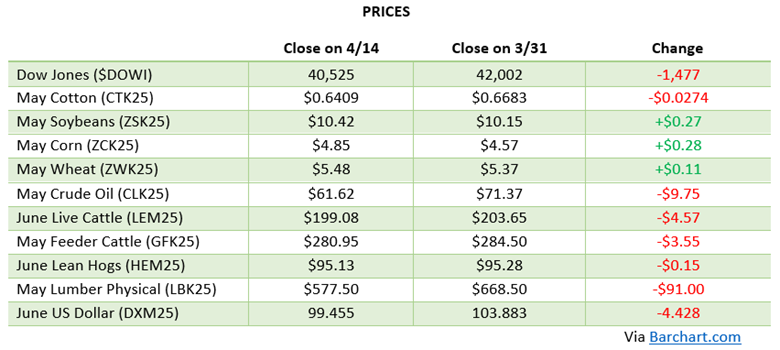

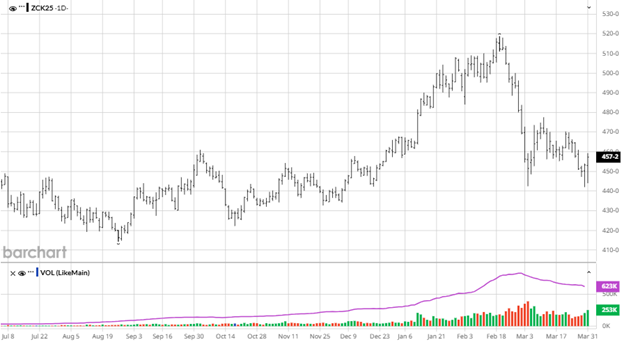

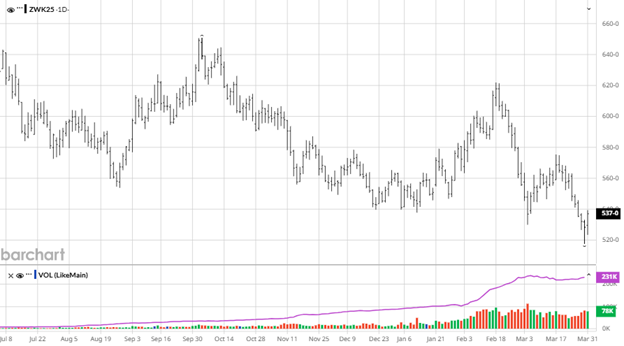

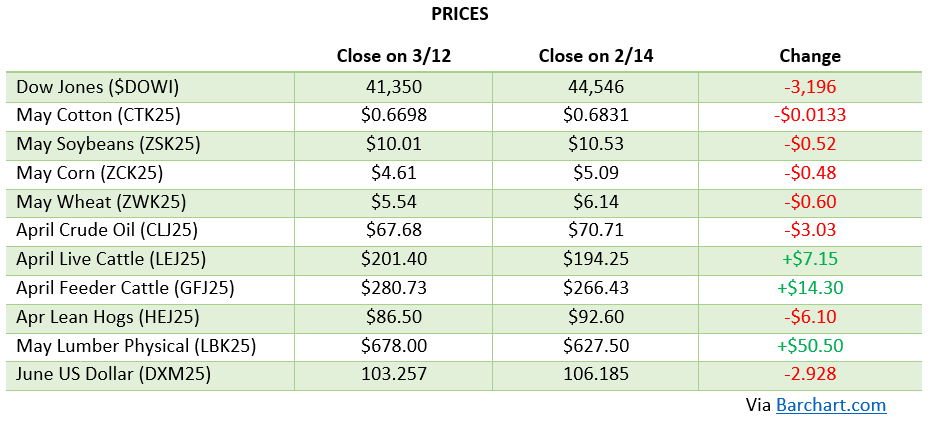

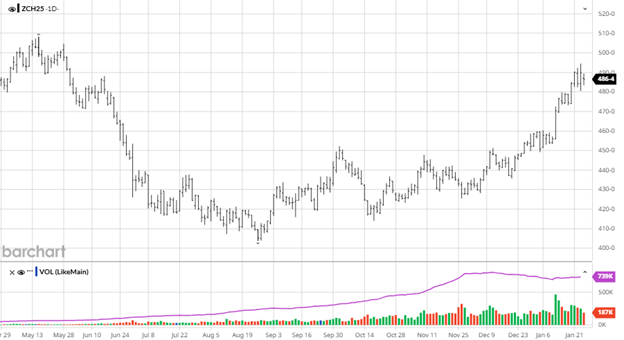

Corn continues to struggle but saw a solid bounce this week after hitting new contract lows. U.S. weather has largely been non-threatening, with most areas benefiting from favorable summer conditions—though pockets of stress remain, particularly in the Southern Plains and Southwestern Corn Belt, where upcoming heat could pose challenges. In South America, Brazil’s main corn crop is estimated to be over 10% larger than last year’s. With strong production expected from both the U.S. and Brazil, the global supply glut remains a key headwind, continuing to weigh on prices over the past few months. The corn crop had a G/E rating of 74% to start the week.

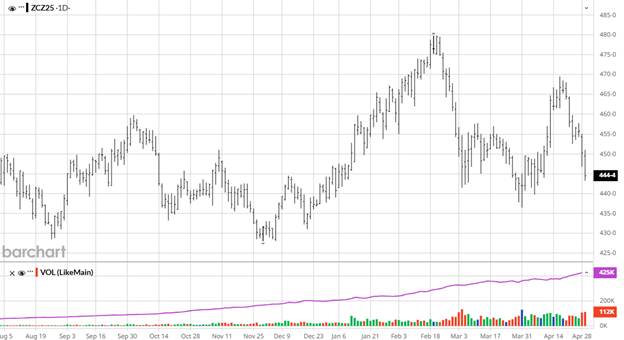

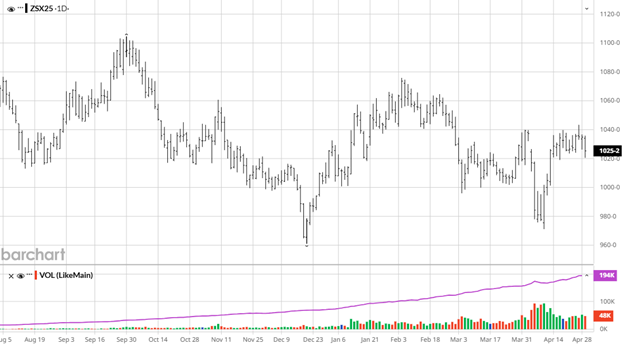

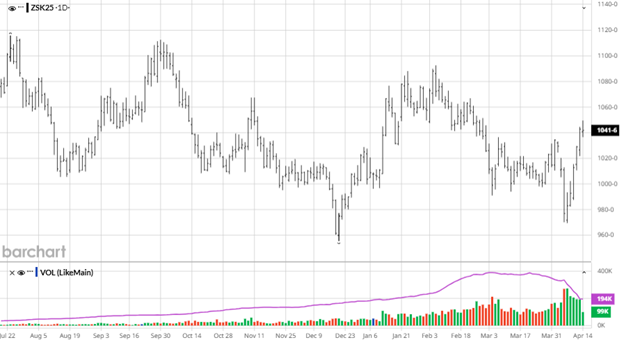

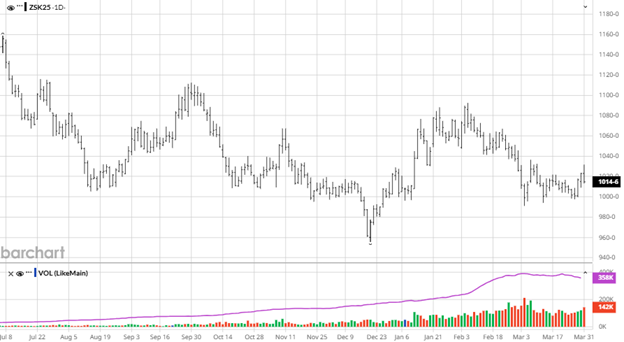

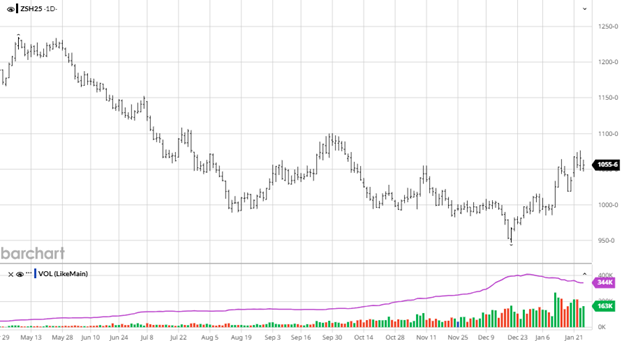

Soybeans, like corn, had a solid week following a recent dip. Prices have held relatively steady, trading in the $10–$11 range. Favorable U.S. weather has supported early crop development, but late-July heat could pressure some of the later-planted areas. Globally, Brazil remains on pace for a record soybean crop, while Argentina is facing some production challenges and policy-related uncertainty that has slowed farmer sales. November soybean futures ended the week just above all major moving averages (20, 50, 100, and 200-day), setting the stage for a key technical test as we head into next week. Beans had a G/E rating of 70%, better than expected.

Soybeans, like corn, had a solid week following a recent dip. Prices have held relatively steady, trading in the $10–$11 range. Favorable U.S. weather has supported early crop development, but late-July heat could pressure some of the later-planted areas. Globally, Brazil remains on pace for a record soybean crop, while Argentina is facing some production challenges and policy-related uncertainty that has slowed farmer sales. November soybean futures ended the week just above all major moving averages (20, 50, 100, and 200-day), setting the stage for a key technical test as we head into next week. Beans had a G/E rating of 70%, better than expected.

Equity Markets

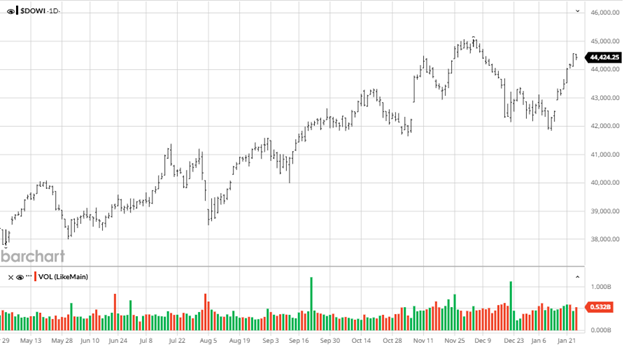

Equity markets continue to push higher, setting new records as the AI trade returns to the spotlight ahead of earnings season. Meanwhile, the Trump White House is adding volatility, with markets reacting to shifting headlines around the future of Fed Chair Jerome Powell. While Powell’s position appears secure for now—at least through the next eight months—any change could rattle markets, as evidenced by the sharp reaction to a recent false report.

Other News

- The last two USDA reports lacked surprises, good or bad, which has created a trade focused on weather.

- The USD weakness continues as it holds around 98, off the recent lows of 96 and well below the recent highs around 108.

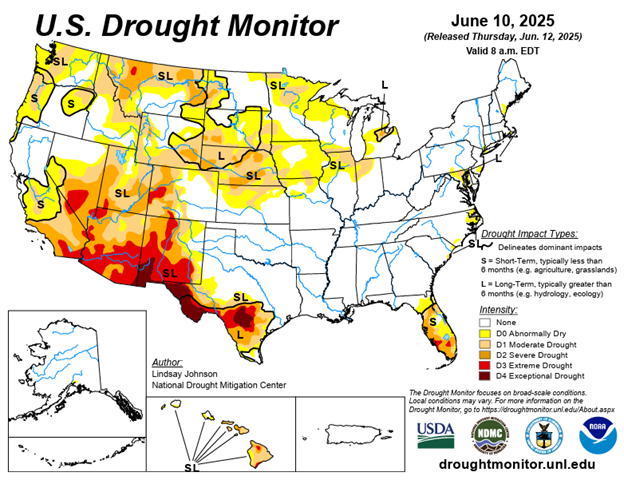

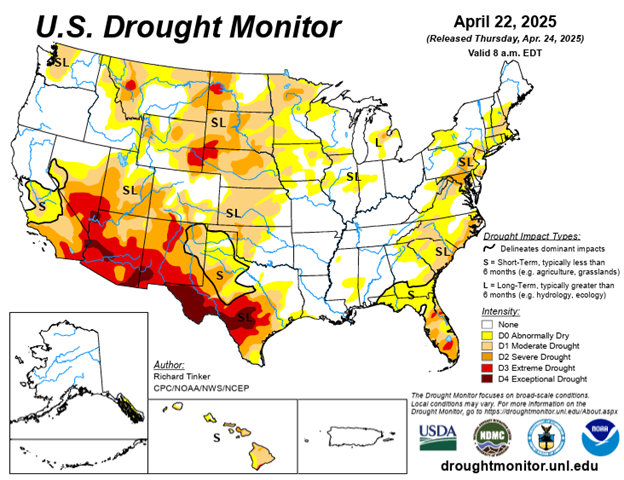

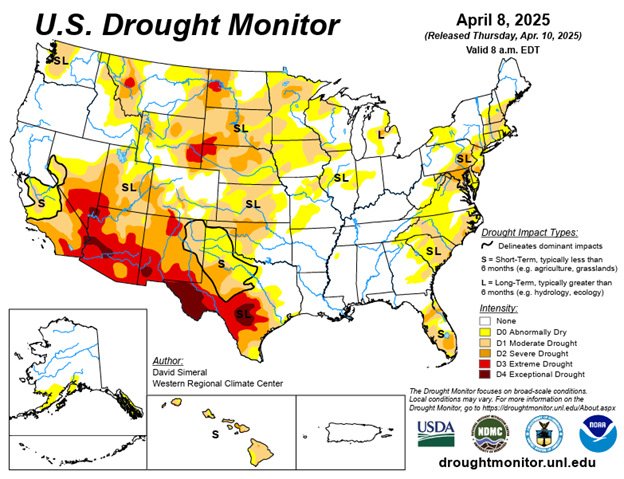

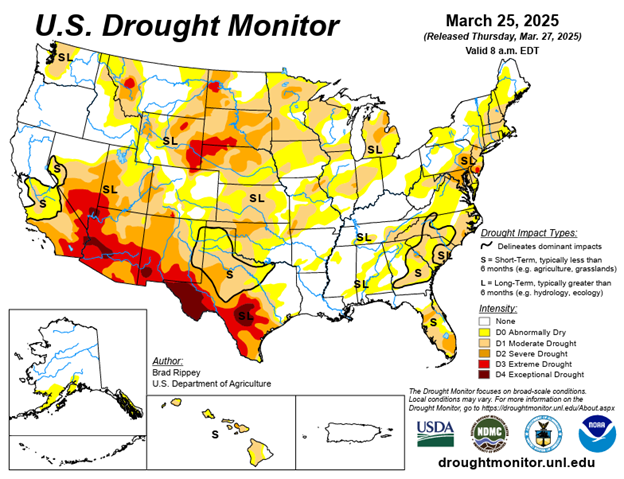

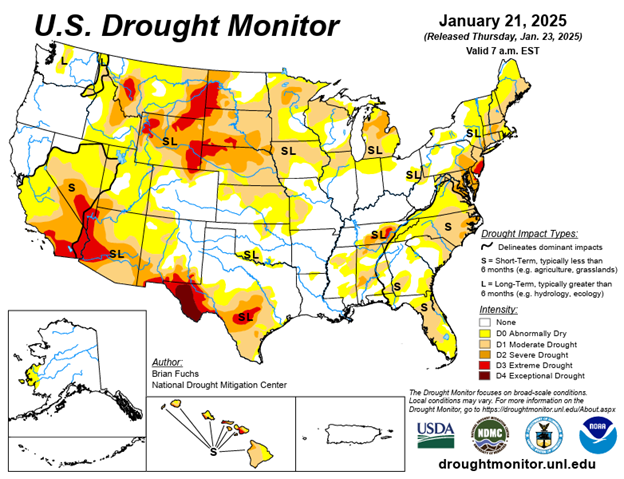

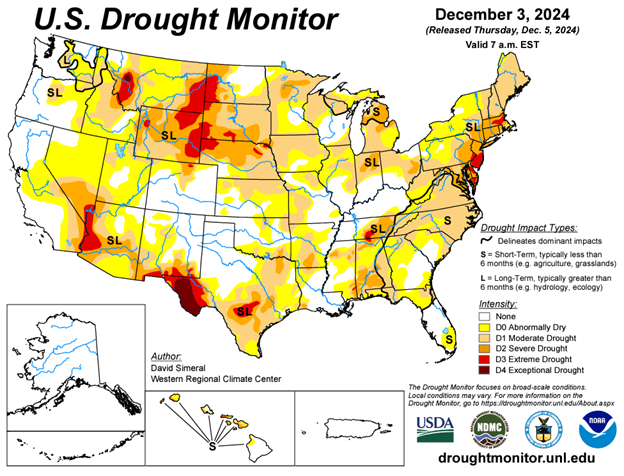

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.