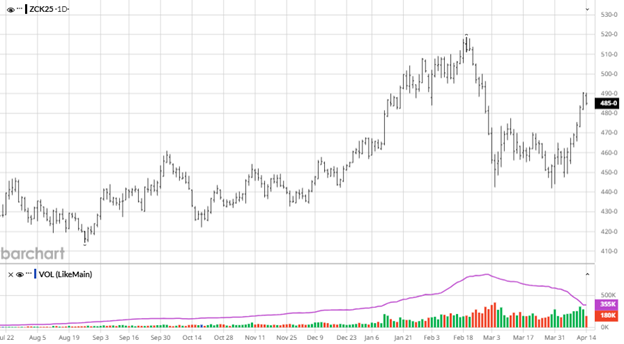

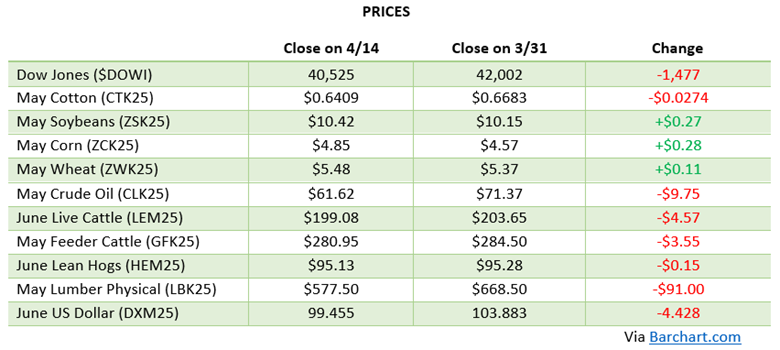

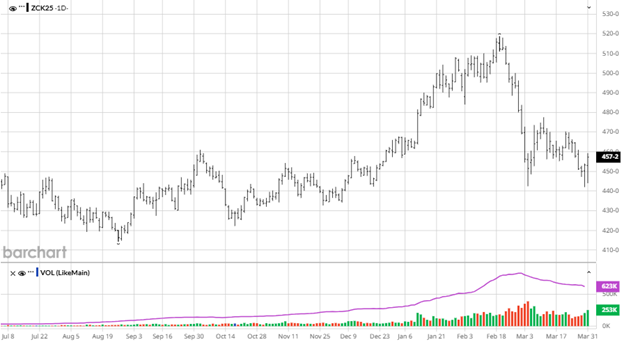

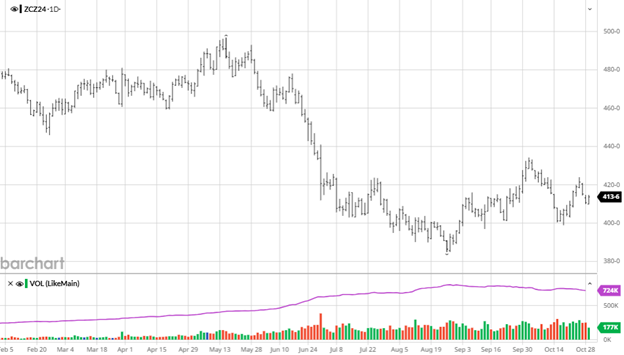

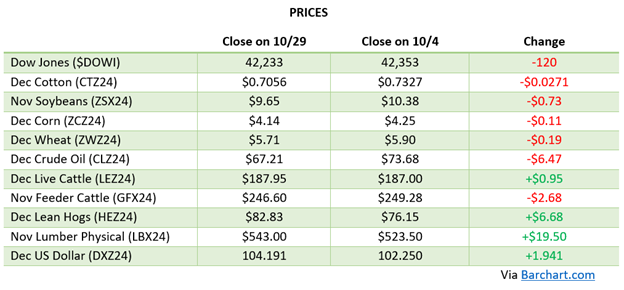

Corn has been under persistent pressure since Memorial Day weekend, with funds aggressively liquidating long positions built up over the spring. Managed Money has sold hard across the corn market going on the last 3 weeks, while the pace has slowed, they could continue selling if they want. The primary catalyst has been a combination of favorable planting weather, excellent crop establishment across the corn belt, and a crude oil market that has been retreating as Iran peace talks progressed. The June WASDE brought few surprises on corn. USDA described the 2026/27 corn outlook as “virtually unchanged” from May, with ending stocks coming in at 1.942 billion bushels and the season-average farm price forecast held at $4.40 per bushel. Old-crop 2025/26 ending stocks ticked up slightly to 2.145 billion bushels on a modest increase in imports, keeping carry extremely comfortable. The one positive was exports, but it was not enough to keep corn up close to $5. 96% of corn has been planted with a 67% good/excellent rating to start the week.

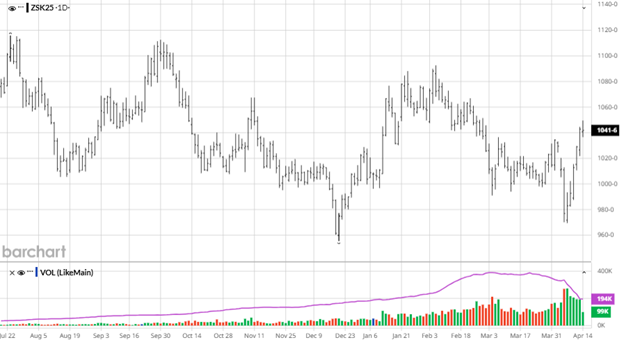

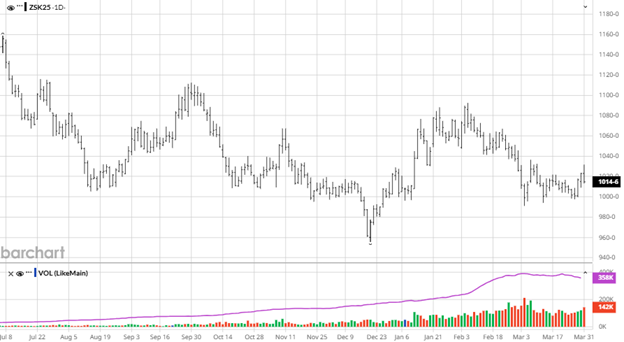

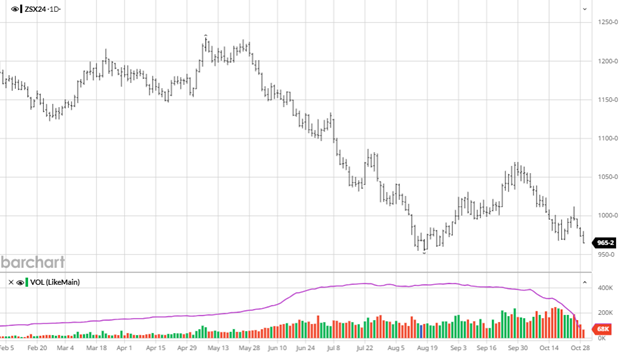

Soybeans have been caught in the same fund liquidation wave as corn, though they’ve shown more resilience given the tighter fundamental backdrop established in the May WASDE Report. July beans settled near $11.15 heading into the June 11th report. The soybean complex did find a brief bounce mid-period on continued strong crush margins and some renewed optimism around a potential Trump-Xi bilateral trade framework, but it didn’t hold. Planting pace has been exceptional, with 92% of beans in the ground and South American supply estimates remain large, with USDA maintaining Brazil’s 2025/26 crop and making only minor tweaks globally.

Soybeans have been caught in the same fund liquidation wave as corn, though they’ve shown more resilience given the tighter fundamental backdrop established in the May WASDE Report. July beans settled near $11.15 heading into the June 11th report. The soybean complex did find a brief bounce mid-period on continued strong crush margins and some renewed optimism around a potential Trump-Xi bilateral trade framework, but it didn’t hold. Planting pace has been exceptional, with 92% of beans in the ground and South American supply estimates remain large, with USDA maintaining Brazil’s 2025/26 crop and making only minor tweaks globally.

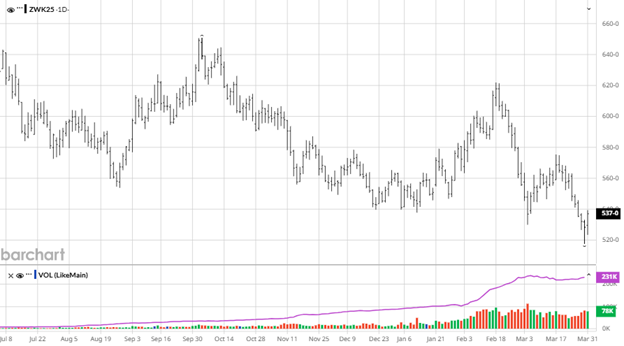

Wheat has been the most volatile market of the period, but not in the direction bulls had hoped. After touching multi-year highs in mid-May on the back of the historically small U.S. winter wheat crop, both Chicago SRW and KC HRW futures have been in a steady slide. July SRW dropped from around $6.36 to the $5.86 area during the period before attempting a bounce, while July KC HRW fell from the mid-$6.70s to the low $6.30s. The catalyst for the pullback was a combination of timely rains arriving in Kansas and Nebraska late in May, some improvement in crop conditions relative to the worst-case scenarios, and funds taking profits after an extended rally.

Wheat has been the most volatile market of the period, but not in the direction bulls had hoped. After touching multi-year highs in mid-May on the back of the historically small U.S. winter wheat crop, both Chicago SRW and KC HRW futures have been in a steady slide. July SRW dropped from around $6.36 to the $5.86 area during the period before attempting a bounce, while July KC HRW fell from the mid-$6.70s to the low $6.30s. The catalyst for the pullback was a combination of timely rains arriving in Kansas and Nebraska late in May, some improvement in crop conditions relative to the worst-case scenarios, and funds taking profits after an extended rally.

Equity Markets

Equity markets have continued an impressive run with volatility recently and profit taking in some of the high flyers leading to a few heavily lower days. With inflation still a worry many investors believe that we are likely to see a rate HIKE before the end of the year rather than another cut.

Energy Markets

Crude oil has been the dominant macro variable across all markets and the primary driver of the grain complex selloff over the past two weeks. WTI has fallen sharply from its spring highs above $110 per barrel as Iran peace negotiations have progressed, at times with apparent momentum, though the path has remained anything but straight. The headline to end the week that there is an apparent Memorandum of Understanding to end the conflict in the Middle East took crude back below $85 to end the week.

Other News

- The June 30th USDA Planted Acreage and Grain Stocks reports are the next major scheduled market events. Any meaningful deviation in final corn or soybean planted acres from the March Prospective Plantings survey will be a significant market mover across the complex.

- The New World screwworm situation in Texas received its first mention in the WASDE narrative this month, a reminder that animal agriculture has its own emerging risks to monitor alongside the geopolitical backdrop.

- Cotton has pulled back with the broader commodity complex as crude oil retreated, removing some of the energy-driven premium that had made natural fiber more attractive relative to synthetics. Producers should continue to evaluate hedging strategies to protect margins at still-profitable price levels.

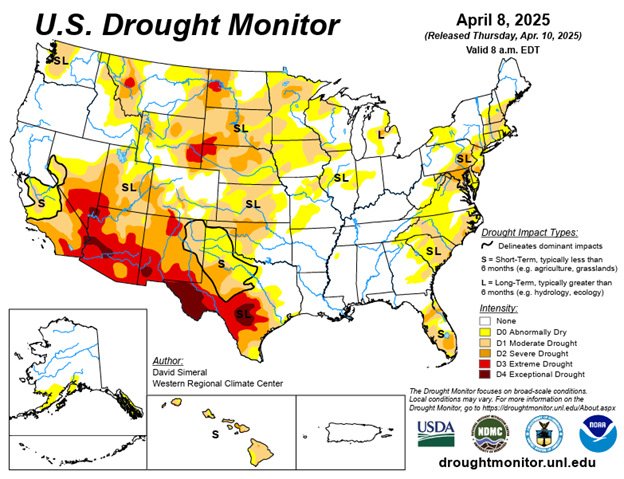

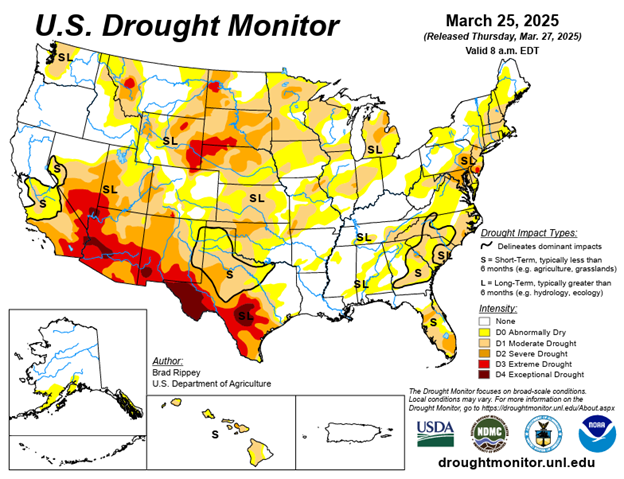

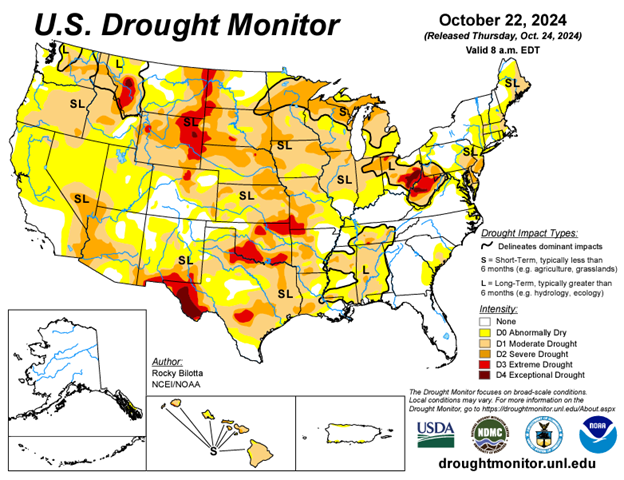

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.