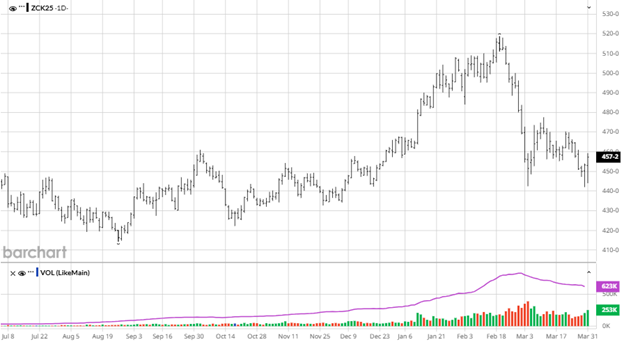

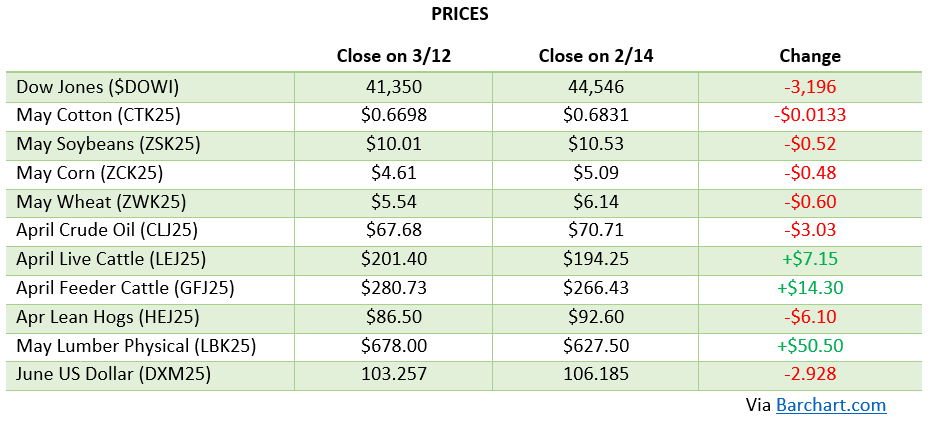

Corn has been trading sideways since the end of October and nothing from today’s USDA Report gives it reason to change course. The main news for corn has been the lack of news. Corn did dip 20 cents in late November but bounced back to the middle of the range it has been in around $4.45. In today’s USDA report they kept US production the same while raising the export forecast by 125 million bushels, lowering US ending stocks to 2.029 billion bushels. The global stocks number was also revised lower with production cuts to other countries, including Ukraine. While the report was modestly bullish corn will need some more news to leg up to the $4.60 range as South America is off to a great start.

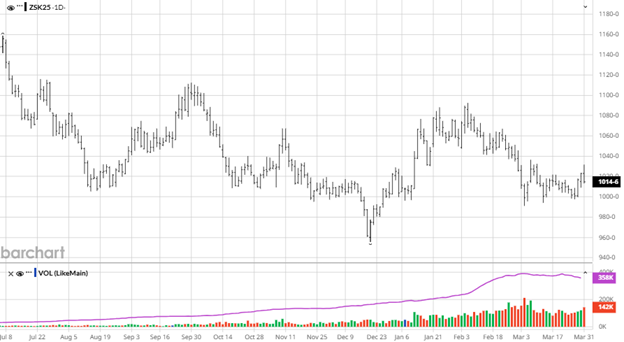

Beans have tumbled off their recent highs as the rocket higher ran out of fuel and has been giving back those gains. The USDA left US production the same with an overall neutral report with no major surprises. Global stocks were slightly raised as Brazil, India and Russia offset tighter supplies elsewhere. With no news to turn this recent downtrend around the market needs positive China trade news desperately as that was the initial “news” to drive markets higher.

Equity Markets

Equity markets have rallied from the November dip and are within a couple % of new all time highs. The markets are expecting another rate cut this week and would be surprised if there is not.

Other News

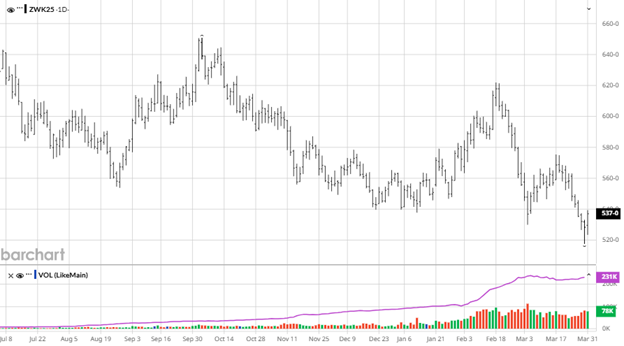

- The wheat numbers were mostly unchanged and did not have any major news to change the direction of trade but could turn around on global trade news.

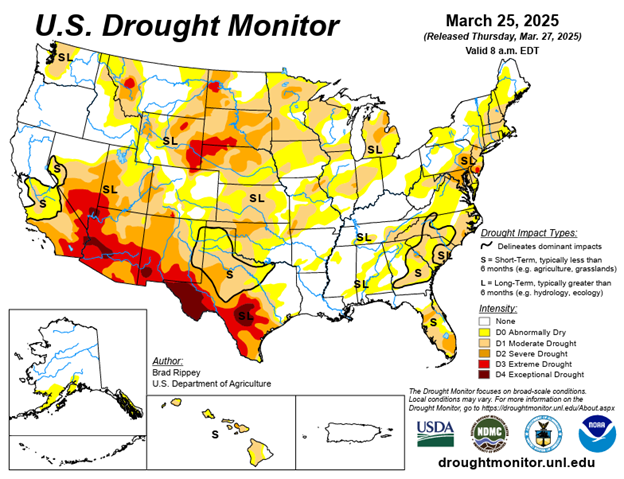

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.