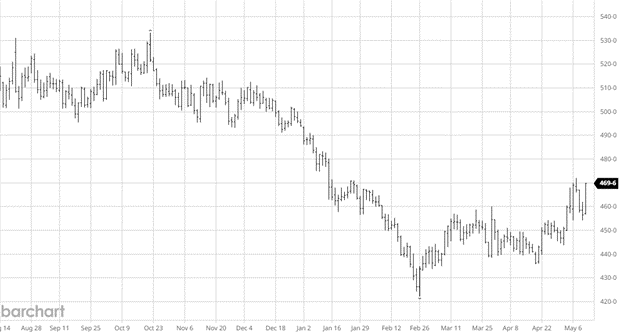

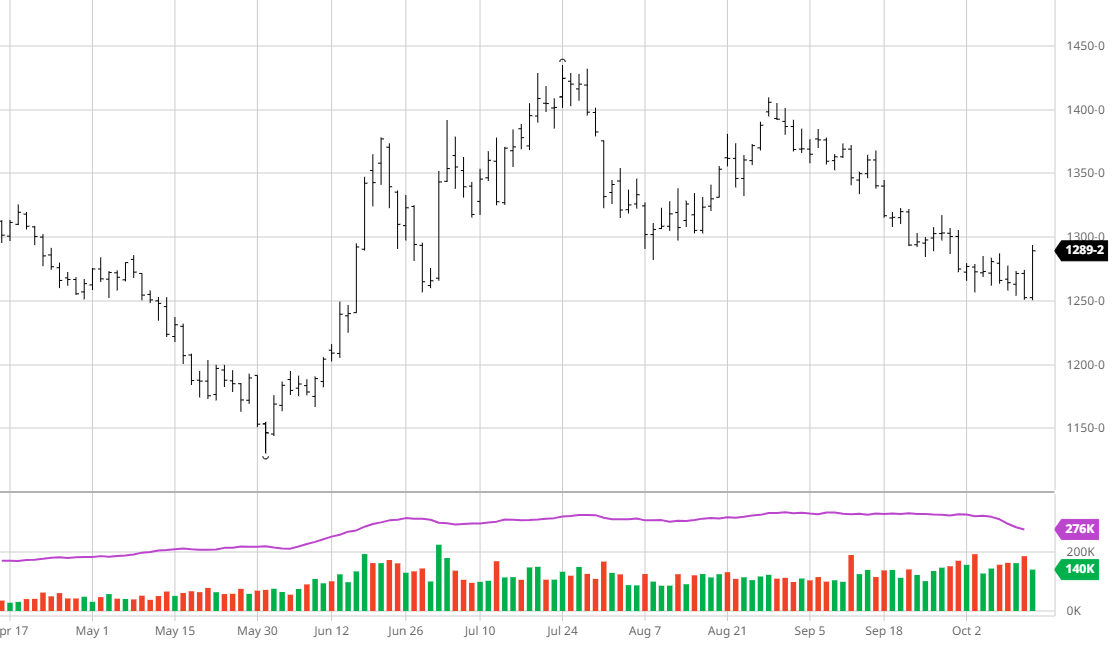

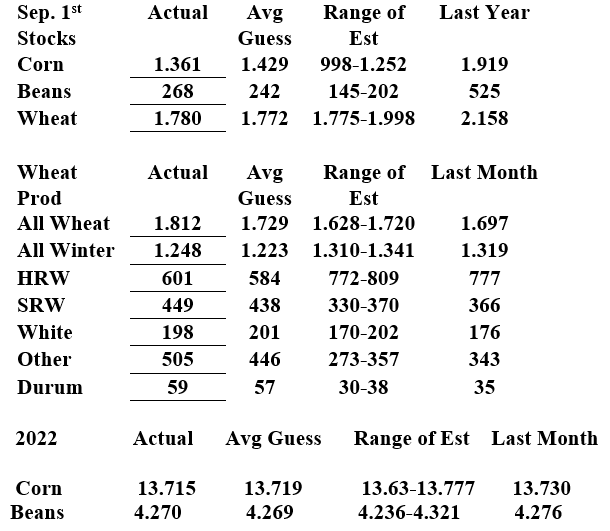

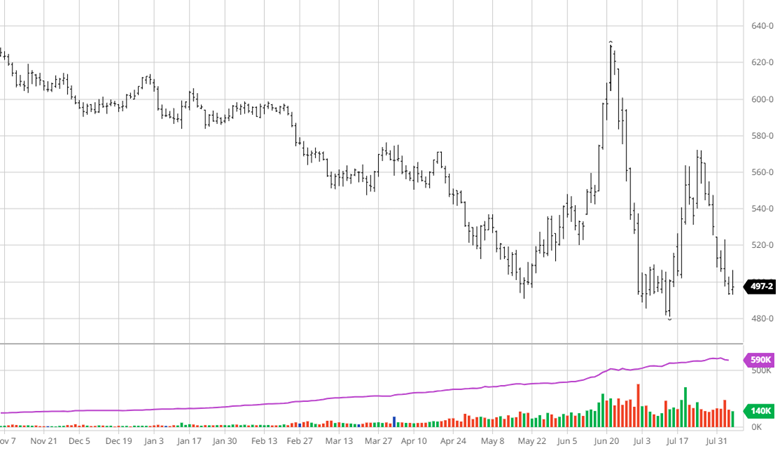

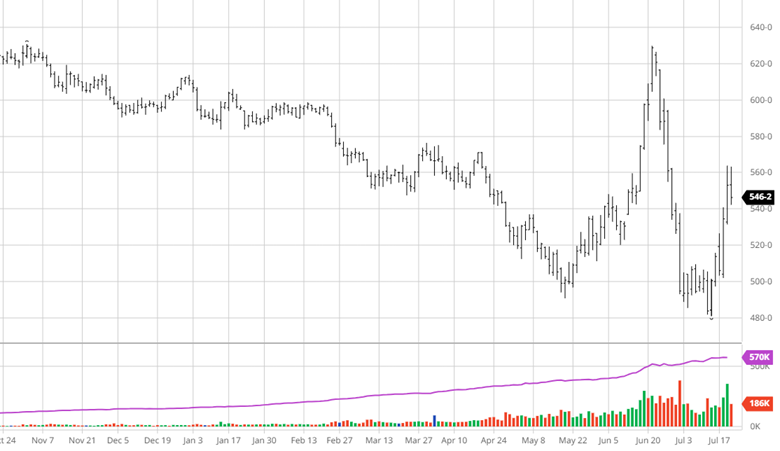

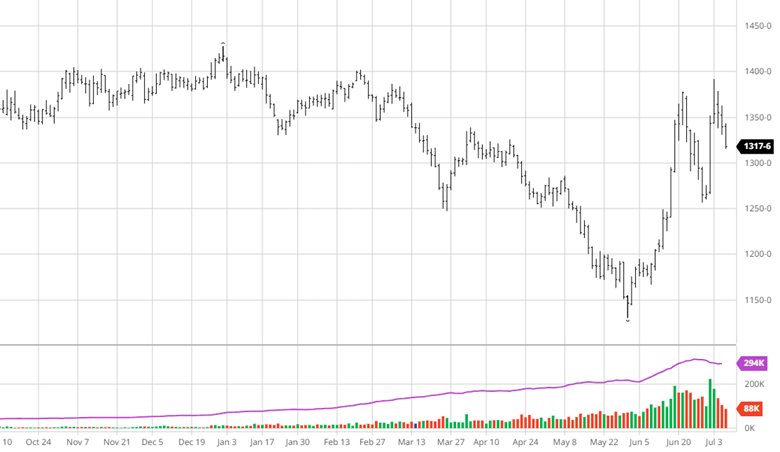

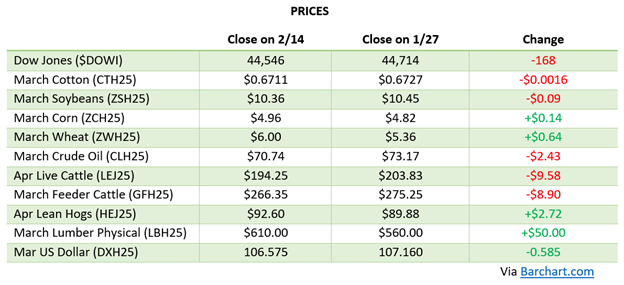

Corn rode the wave higher following the updated USDA numbers in the January report with old crop prices settling into a range and 2025 steadily moving higher. The funds are long 1.8 billion bushels and staying long which is helping this market higher with the general fear being a huge corn acreage number for this year that could present a problem. South American weather remains consistent with non-threatening forecasts while the US has a striking cold few days coming. There are multiple items supporting a continued grind higher from here, but funds have their hand on the scale so keeping an eye on what they do and what the technicals are saying will be important as well as harvest data out of South America. It is never too early to look at making sales for the 2025 crop year once you know your breakeven. You can always look at re-owning it on paper if the market really makes moves higher.

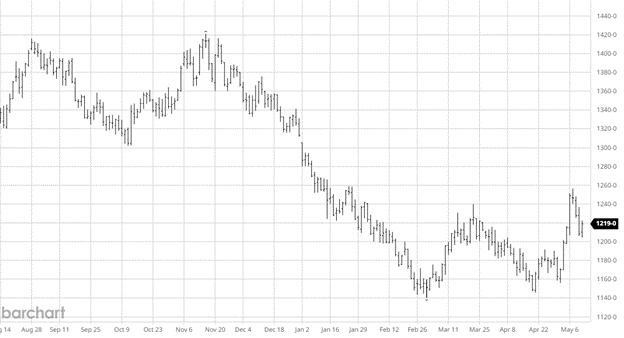

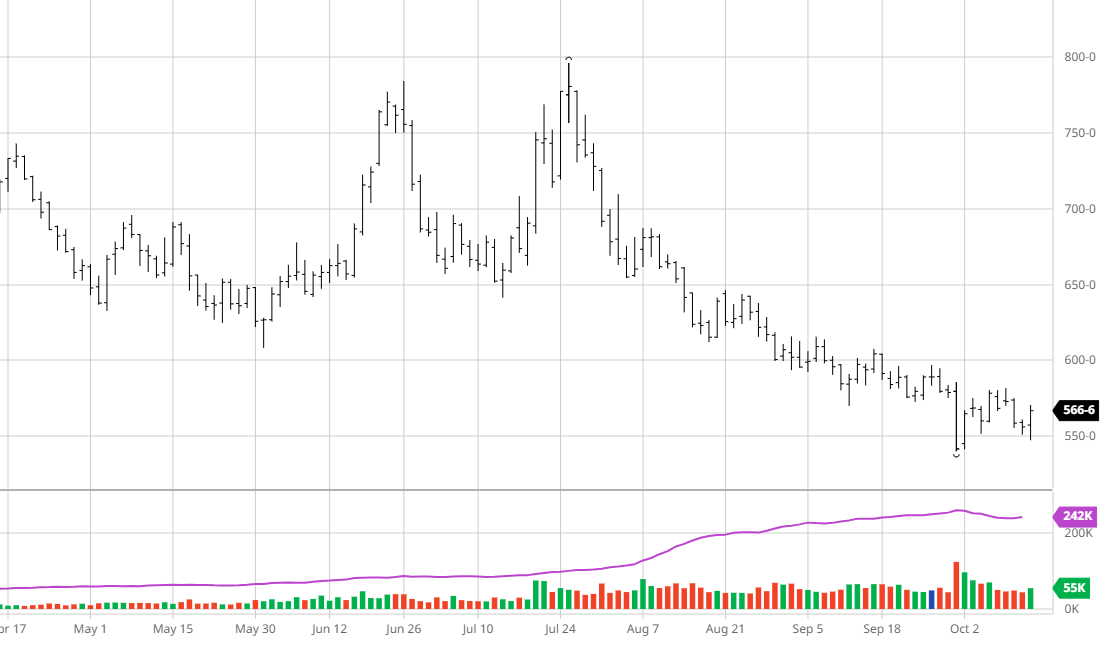

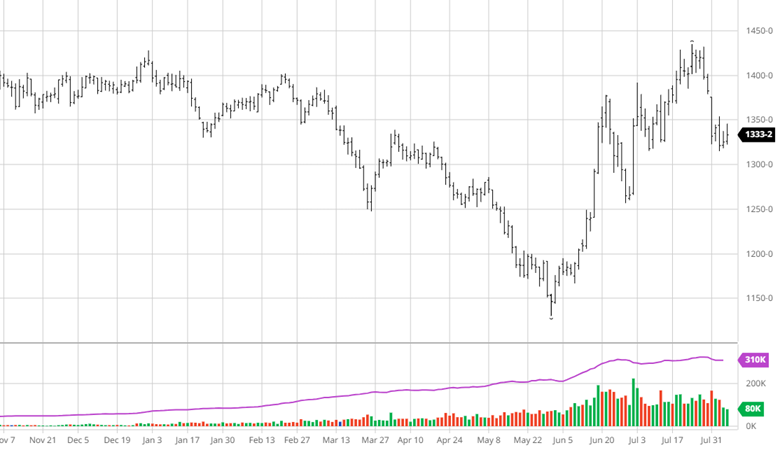

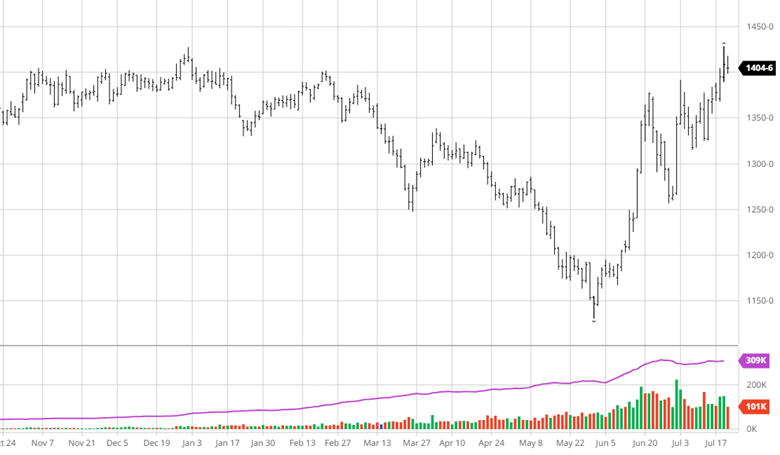

Soybeans have been trading flat since the January USDA Report bump. South America’s record crop present price challenges to the US as we are not the main supplier for the world anymore. A renewed trade war with China would certainly have negative effects again on the soybean market. South America yield numbers and any tariff wars will be the main news in the market until planting begins. Beans inability to continue the rally like corn is not surprising but the corn-bean price ratio that we are seeing is going to make for some interesting conversations when planting is decided.

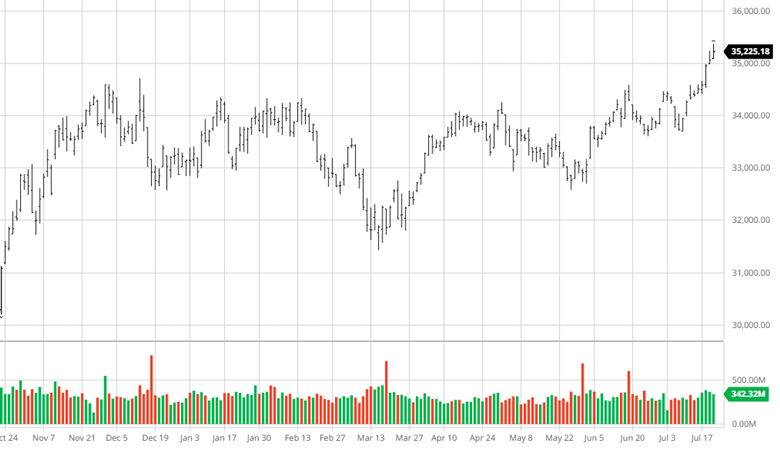

Equity Markets

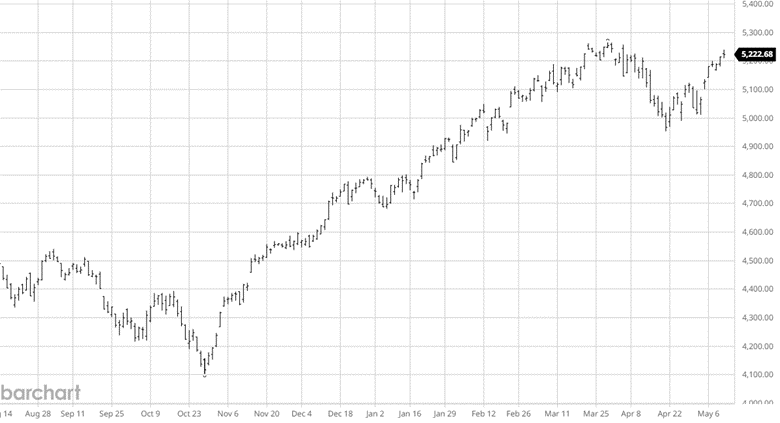

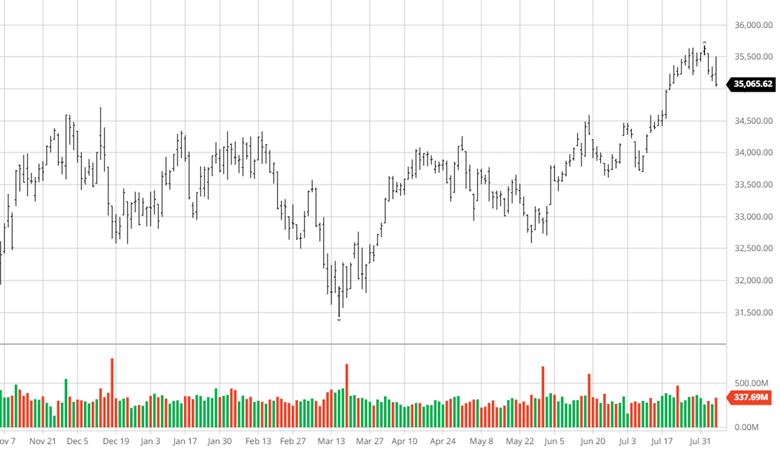

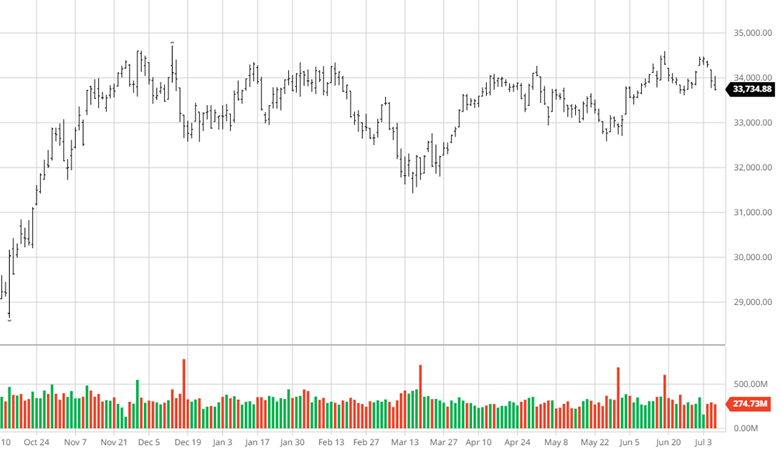

The equity markets have been volatile as we start the year with the Magnificent 7 taking a break while managers repositioning for expected moves (or lack thereof) from the Fed. With the constant talk of tariffs and then delays to implementation, it provides a volatile market within different sectors.

Other News

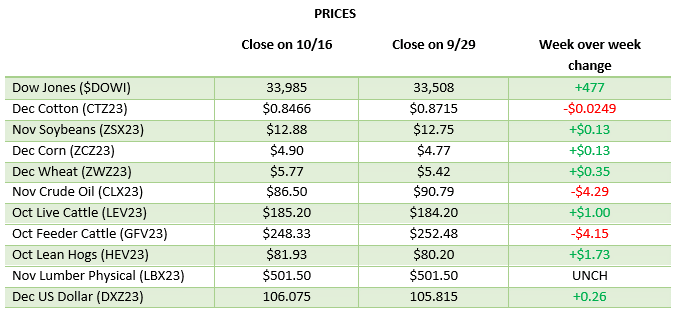

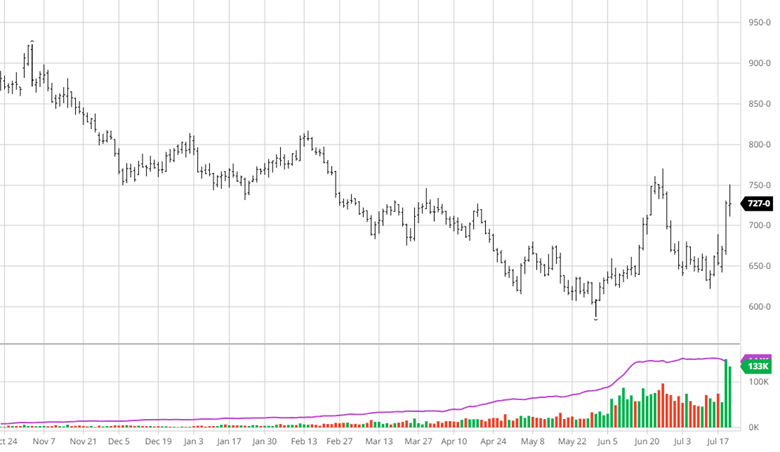

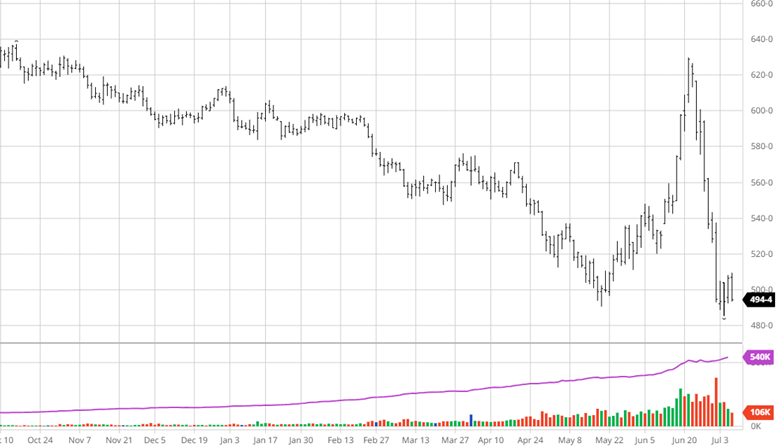

- Wheat has moved higher recently with record cold weather and winterkill concern driving it to a technical breakout.

- Livestock prices have pulled back this month but are still at strong prices as the head count in the US remains on the small side.

- Tariff announcements remain at the top of mind of the markets as uncertainty is the main issue with no clear guidance and kicking the can down the road.

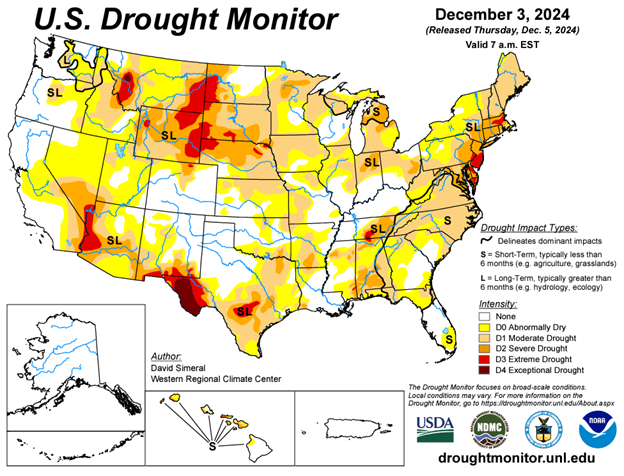

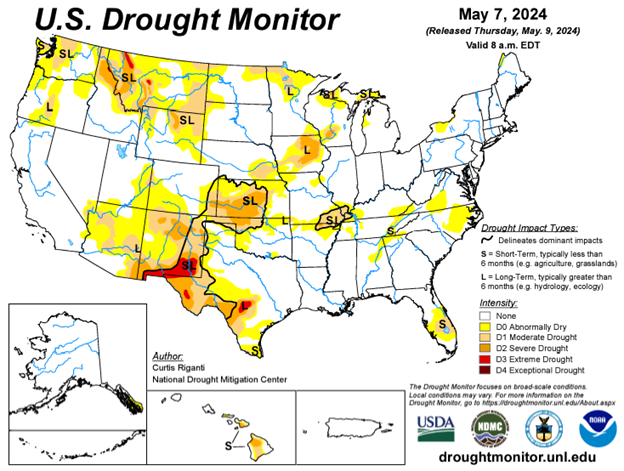

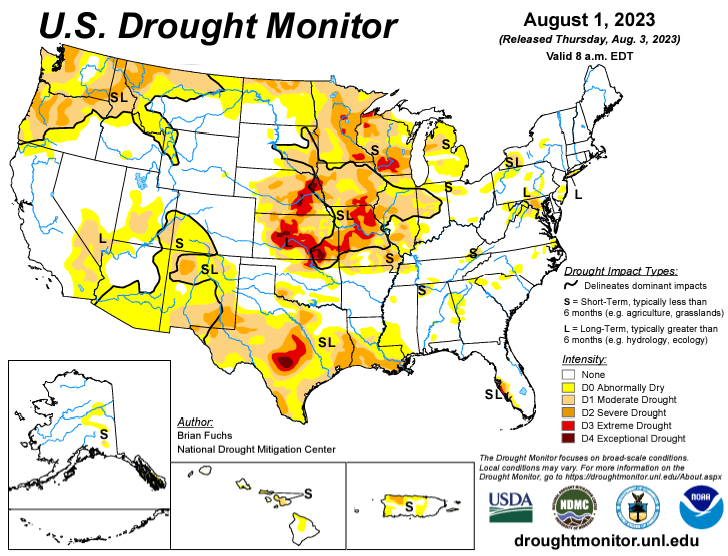

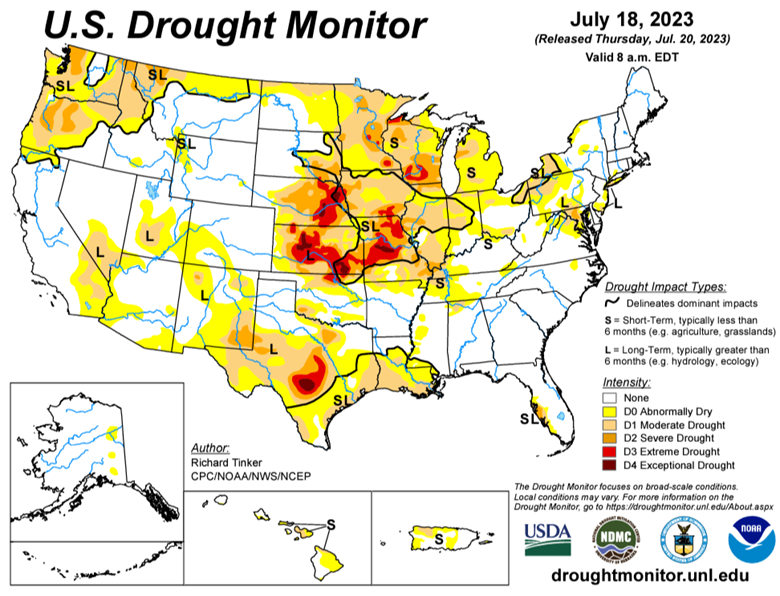

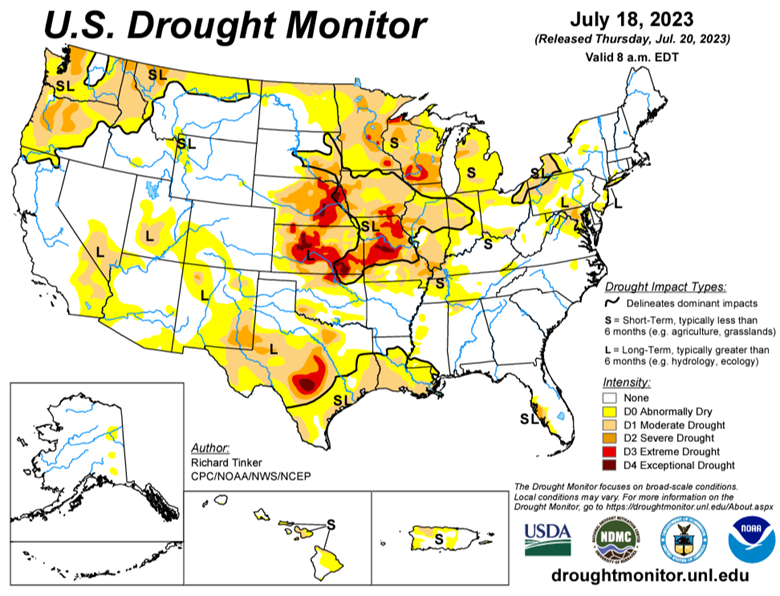

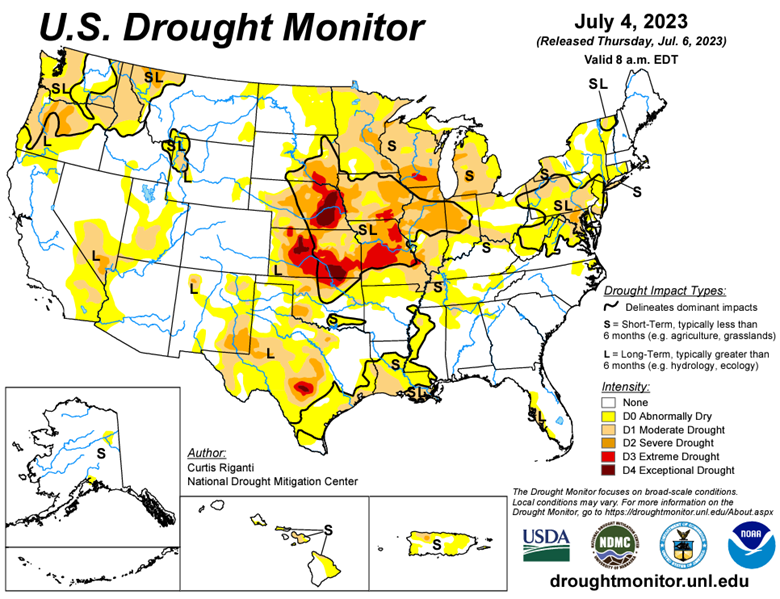

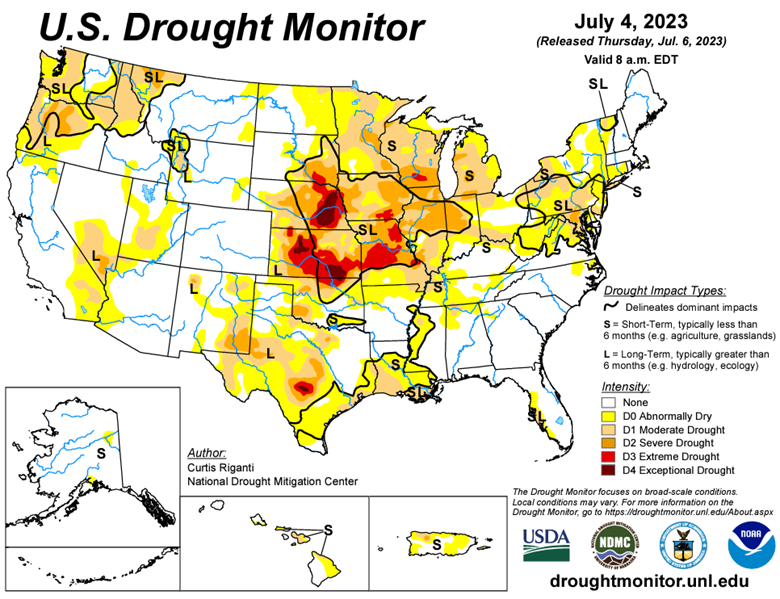

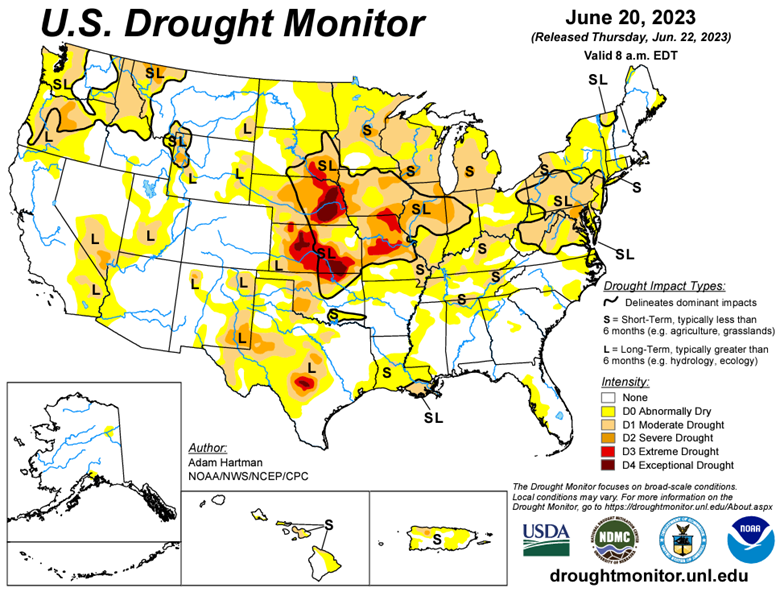

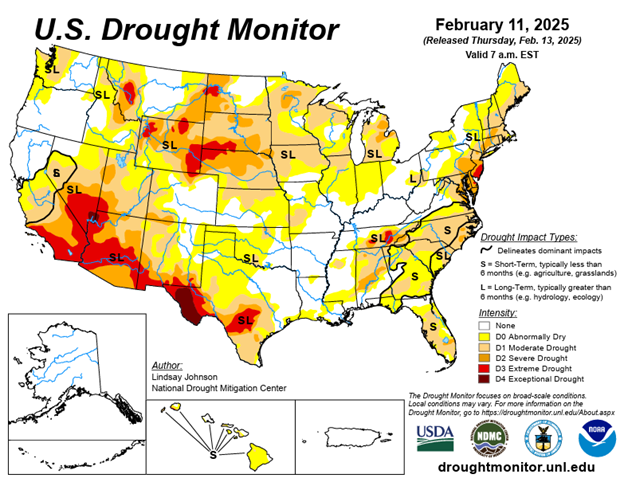

Drought Monitor

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.