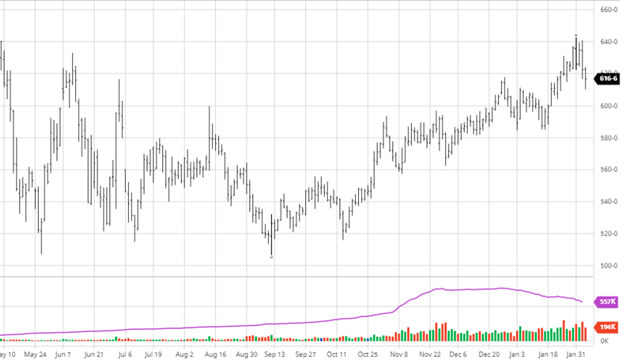

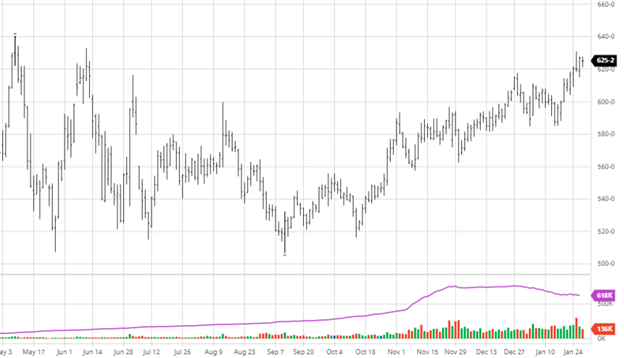

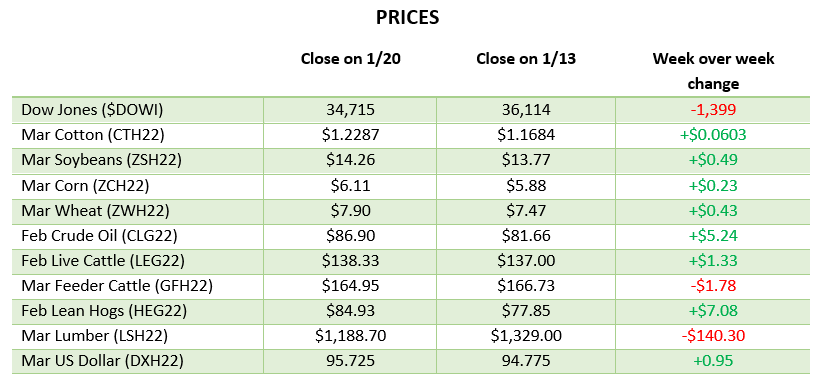

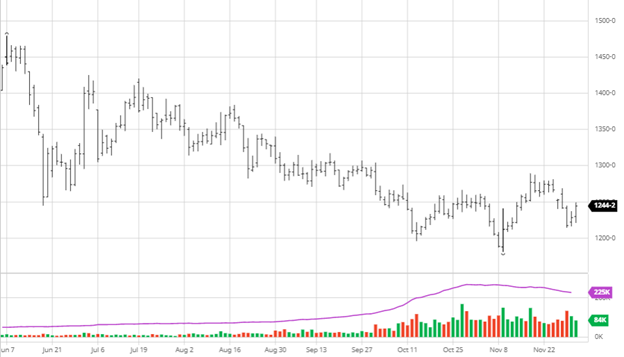

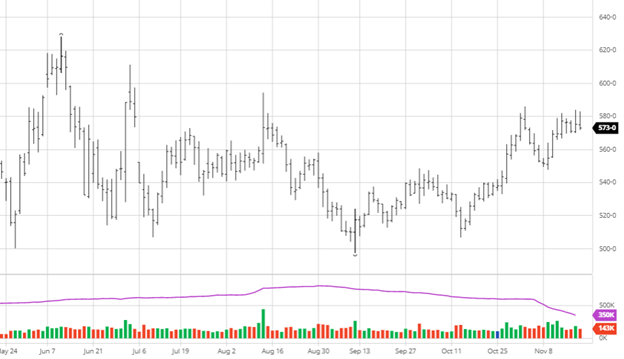

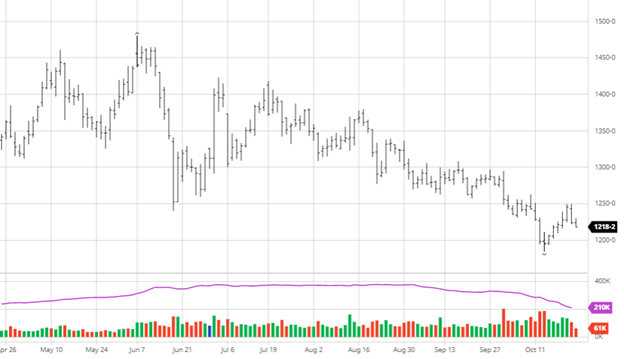

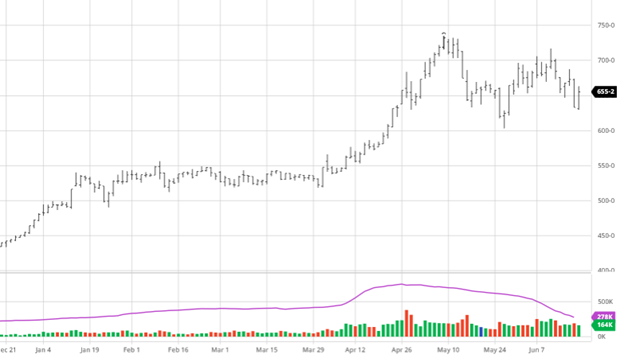

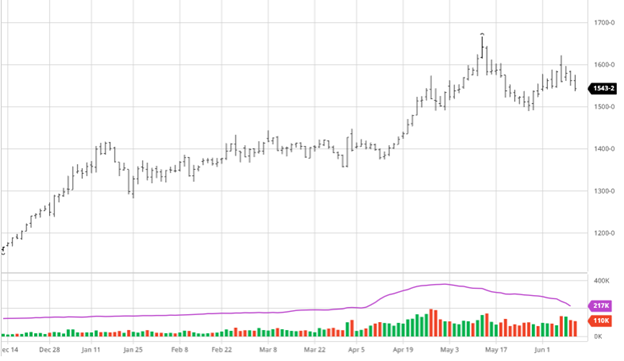

The numbers came in above trade estimates but were lower than the previous months’ report. The USDA kept the U.S. ending stocks at 1.540 billion bushels and lowered the world ending stocks to 302.22 million tonnes while reducing Brazil’s yield. Following the report, it came off the highs for the day before roaring back up to end the day. Thursday’s trade was interesting as halfway through trading, the markets did a 180-degree turn and fell lower on the day after being sharply higher across the board for a large intraday range. This was brought on by producers selling and speculative positions taking profits. The large intraday volatility has not been as present in the market as this summer, but Thursday’s trade is a sign that volatility should be expected at these price levels. The USDA’s numbers for Brazil and Argentina are still above what private analysts and CONAB are reporting. The market seems to be on the analysts’ side when it comes to the struggles in South America. The weather outlook remains the same for the trouble areas as it will be hot and dry in the same areas and wet in the same.

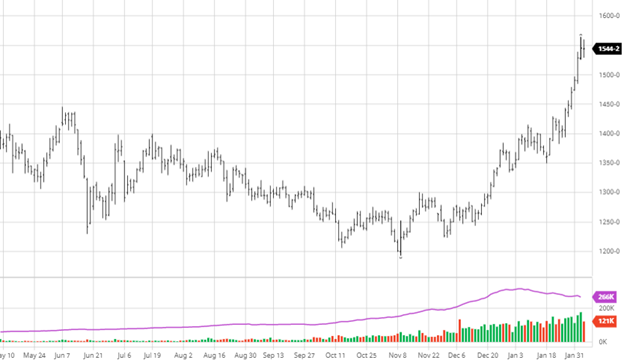

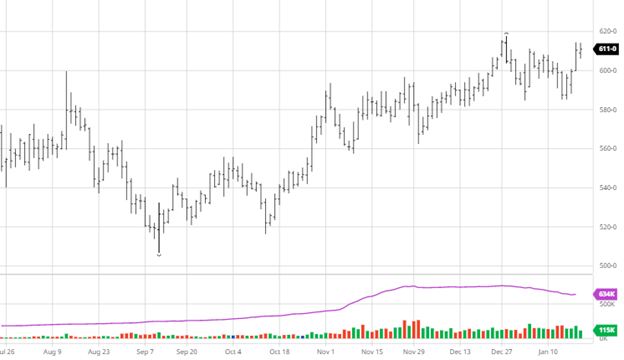

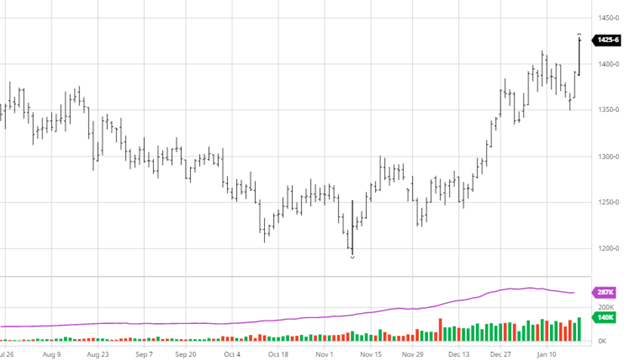

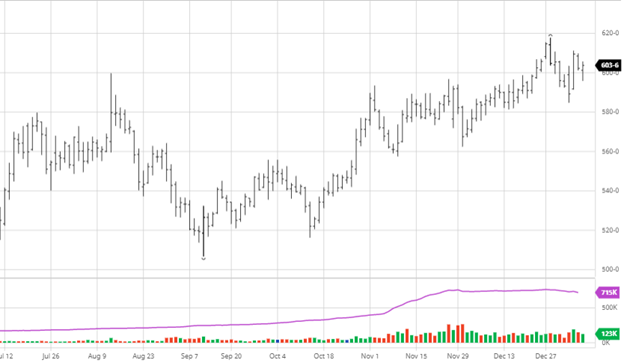

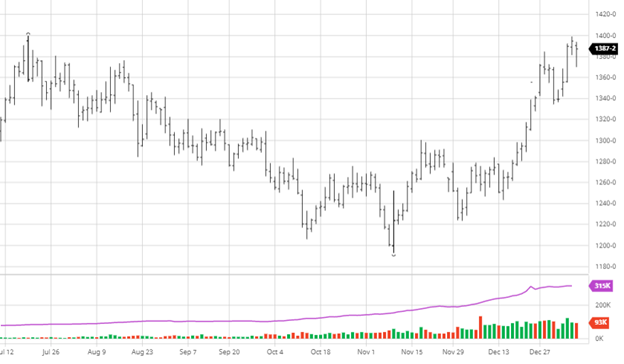

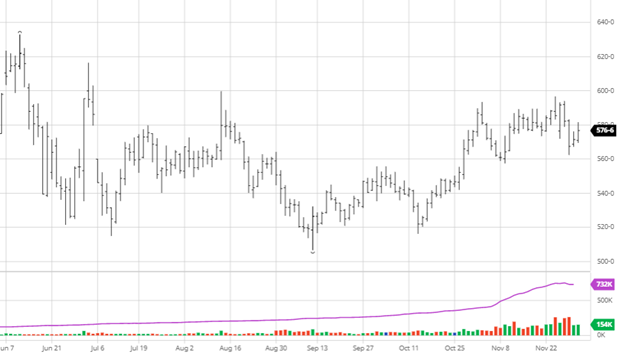

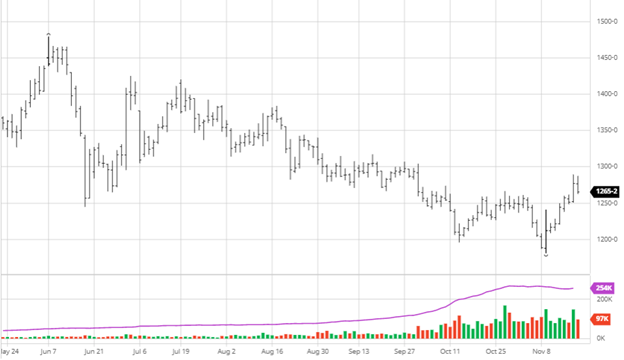

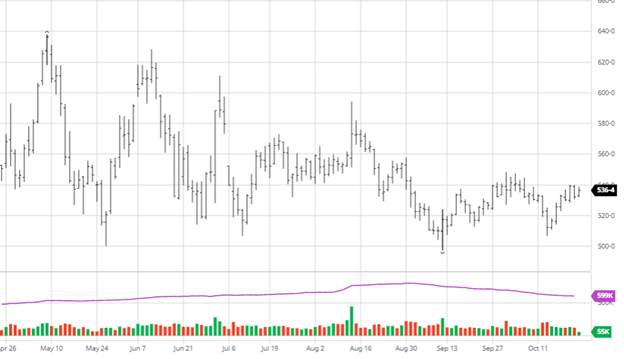

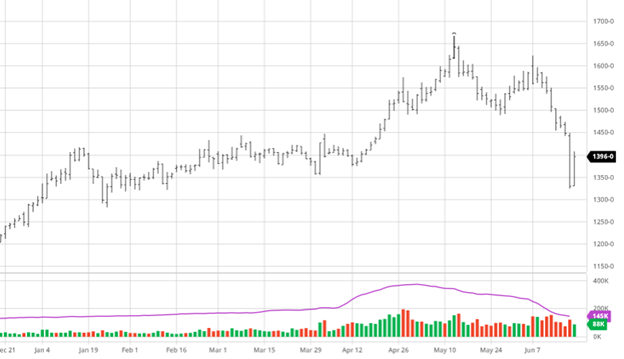

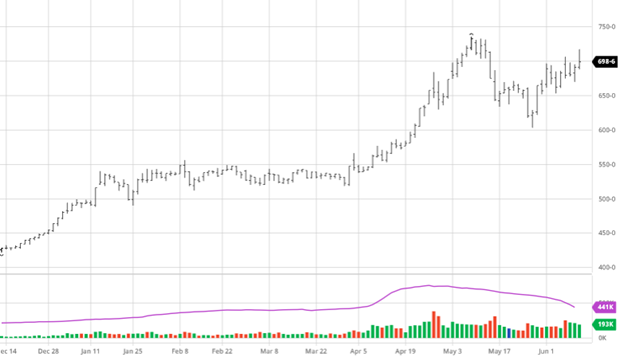

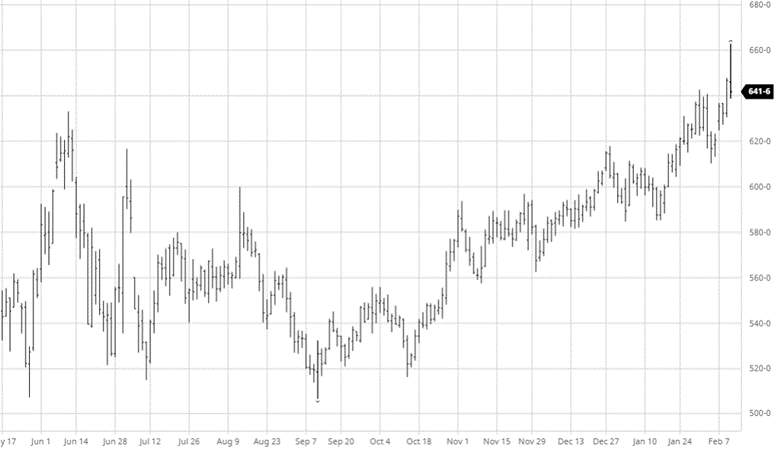

Soybeans continued their run higher despite Thursday’s pullback. The most significant change in the report came to soybeans as the USDA lowered Argentina’s production by 1.5 million tonnes and Brazil’s 5 million. As much of a correction that the USDA made, some analysts still feel these are too high, and their crop will continue to get smaller. With the continued hot and dry weather in Argentina and southern Brazil mixed with the wet harvest in northern Brazil, mother nature is not doing South America’s crops any favors. CONAB released their estimates on Thursday and were well below the USDA numbers, so it’s safe to listen to their numbers and analysts over the USDA right now, it would appear. The two-year chart is below so that you can see the journey of how we got to this point with the great run since early November. Thursday produced the same wild volatility as corn, which saw a 67 ½ cent range while falling off the highs.

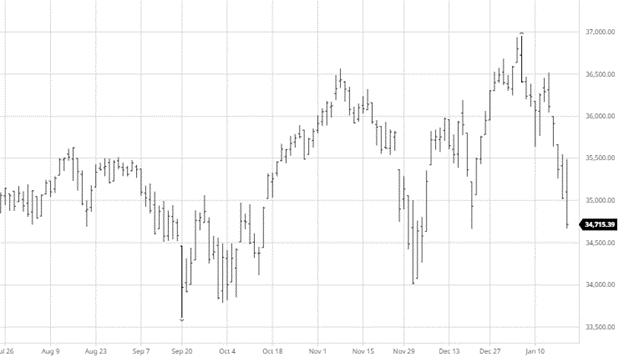

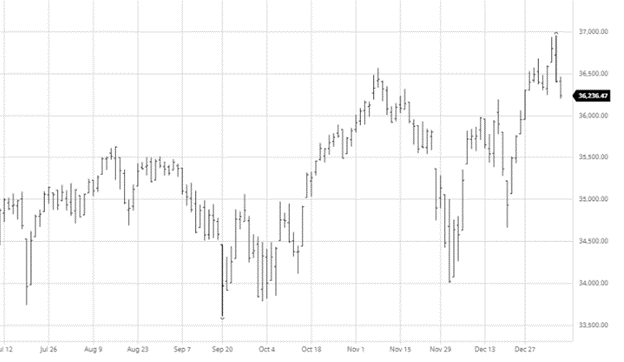

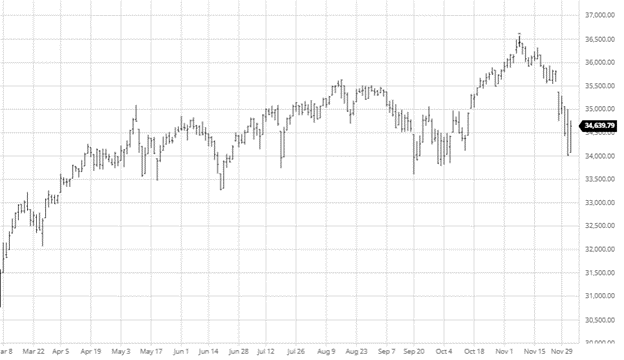

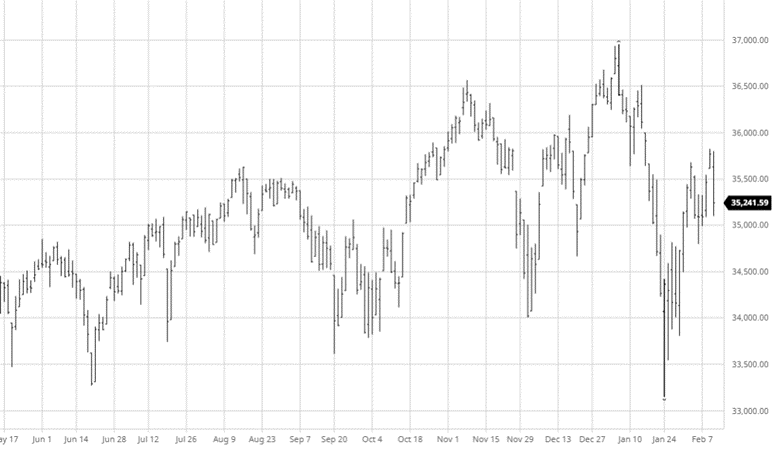

Dow Jones

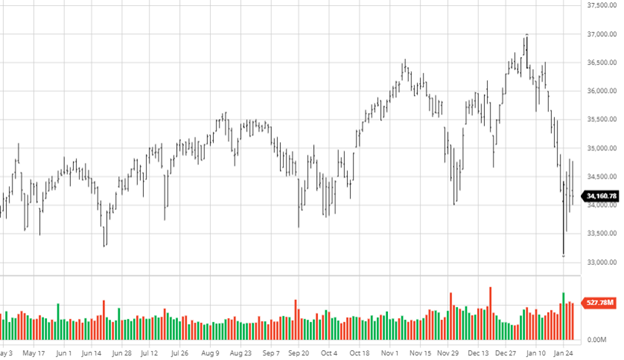

The equity markets have been quieter lately, with small gains on the week, but the uncertainty of what lies ahead remains. The inflation number came in at 7.5% year over year, the highest increase since February 1982. With inflation sticking around and treasury yields jumping, the 10-year treasury topped 2% for the first time since August 2019; it is understandable why the markets have the jitters. Will the market hang out where it is, retest the lows, or try to continue to claw back its losses from January? The market can’t figure it out, so I won’t try to predict for you.

Podcast

Tune in as biotech guru Dr. Channa S. Prakash discusses everything from Alabama football, genetics as one of the most extensive agricultural advancements, the most significant risk factors to feeding the world over the next 30-50 years, plus everything in between.

Why producing crop plants with a much gentler footprint on the natural resources will help feed the growing population. How 75% of the world’s patents in agriculture gene editing are coming from China. Understanding that trying to impose restrictions on our ability to grow food can be a considerable risk to agriculture. Listen to hear about these topics and more!

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.