Cattle markets are at multi-decade highs, and producers are facing both incredible opportunities and serious risks. In this first radio edition of The Hedged Edge, hosts Jeff Eizenberg and Ben Hetzel dig into the realities of managing cattle risk when prices are running hot.

Joining the conversation are Dwayne Bowman, President of Dakota Western Bank, and Joe McKitrick, a North Dakota rancher, who share their perspectives on:

- Why tight cattle supplies are driving record highs.

- The risks of inflation, feed costs, and consumer “trade-down.”

- How bankers and ranchers view tools like LRP, futures, options, and forward contracts.

- Opportunities in feed, grain, and basis markets across the Northern Plains.

- Why communication and discipline are critical in today’s cattle market.

Whether you’re a rancher, banker, or market watcher, this episode will give you a practical look at how to navigate risk — and why now may be the most important time to have a marketing plan in place.

____________________________________

____________________________________

Check out the complete Transcript from our latest podcast below:

Bulls, Bears, and Beef: Risk Management When Prices Run Hot

Jeff Eizenberg 00:51

Welcome to the first ever radio version of the hedge edge podcast. I’m your host, Jeff Eisenberg, and I’m here, joined with my co host, Ben Hetzel. Ben, we made it big. We’re on the radio.

Ben Hetzel 01:02

Yeah, buddy, it’s fantastic to be here with you today, and I can’t wait to get into this, and I gotta thank you for all the work you’ve done to get this up and running gov of the inaugural show.

Jeff Eizenberg 01:14

Absolutely no thank thank you as well. Couldn’t have done it without you. And you know a lot of our listeners are going to recognize your voice straight away. You know you’re from the local lemon community. You’re the CEO and general manager of Scranton equity co op for myself, for everybody who’s listening, I’m a bit of a newer voice to the area, and the managing director of the host of the show, RCM, ag services. I thought it’d be a good idea just to give a little bit of background, Ben you and I, we teamed up about a year ago. Really, the idea that we had when we first got together was to support the local Co Op and the community around with additional education and information about risk management and hedging services that we’ve been providing in and around the Dakotas and throughout the I states and other parts of the country. But really, you know, the more we talked and the more we got talking about education, the idea of the show kind of came alive. And since this is the first episode, I thought no better person than you to give us a quick recap and give the listeners an idea of why, why we’re going to do this show. Why should they listen? So if you don’t mind, yeah,

Ben Hetzel 02:26

sure. You know, the landscape changes pretty drastically year to year, it seems like. And the way production, AG, is it has changed over my career. Anyway, one thing that hasn’t changed is the risk. I mean, there’s, there’s a ton of risk in production. Ag and and so our mission with this podcast is, as you said, that this inaugural start to what you used to do on the hedged edge, first you want to provide the farmers and ranchers, AG, producers, end users, any professional with tools and resources that they need to navigate the markets today and maximize margins, reducing risk in their business. Secondly, you know, I want to highlight the importance of building that right team. We’ve talked about our conversations. You know, that’s the banker, the insurance agent, suppliers, whether it’s agronomics or other, having that agronomist close to your business, your broker, grain buyer, metal buyer, and all also your people that are on the operation every day with you and, and it’s just, it’s all about bringing that team closer and and and minimizing risk In your operation.

Jeff Eizenberg 03:40

Yeah, no, that’s, that’s right, and it’s, it’s been kind of the heart and soul for you and for me our entire careers, and as you get talking to more and more people, least as I have and you’ve, you’ve shared with me, it’s also about longevity and legacy. For a lot of people, the ability to not just turn a profit this year, but set up their operations, their farm, their ranch, to pass on to the next generation. Pay back their banker today, you’ll find we’ve got a guest banker on the on the line, so he’ll be happy to hear that. And with all of this said, we’re excited to be able to share this platform with you. Each week. We’re excited to bring new guests and new new team members from around the local community together to have these discussions. So again, thank you for taking the time to put this one together. All right, now that we’ve walked through why we’re here, let’s jump into today’s episode, bulls, bears and beef. All right, joining us today. We’ve got Dwayne Bowman. Dwayne’s the president of Dakota western bank, and Joe mckich. Joe joins us from Bowman, North Dakota, where he’s actively ranching, and it has been his entire career in production agriculture. So gentlemen, Dwayne Joe, are you there? Able to able to hear us? I’m here.

Joe McKitrick 04:59

Do. Yes, Jeff, All

Jeff Eizenberg 05:02

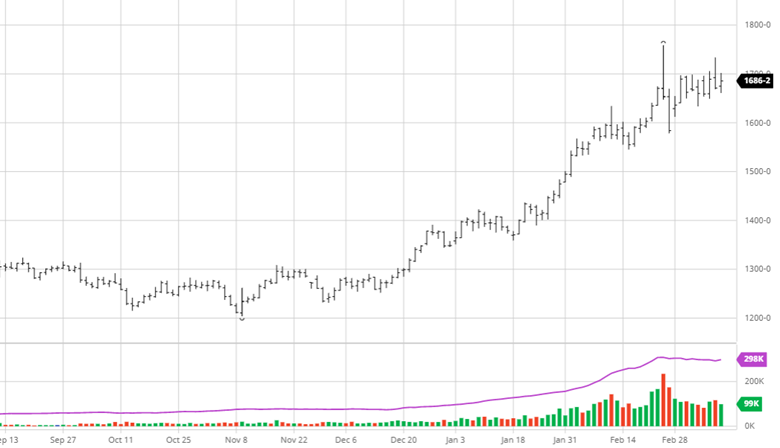

right, thanks for jumping on and joining us. We actually Dwayne is in studio with with Ben, so we’ve got the two of them together, which is great. And Joe’s off in Montana today. So again, thank you both for jumping in you know today and where we where we’re going here with this first episode is, let’s just jump in and talk about cattle why not? Right? It’s the hottest market. There is grain markets. Well, we’ll save that for the end. But with cattle prices are at all time highs. Wanted to kind of start out with a couple quick stats, and then have you guys really share what’s going on, boots on the ground style. You know, I think many people have heard, if they didn’t already know, this is the smallest us cattle herd in 70 years, 70 years since 1951 there’s 86 point 7 million head out there on feed that is highly un contrast to the 2019 peak pre covid numbers, 94 point 7 million. So we’re way down. Number one, number two. This one’s pretty interesting. I think we all know it, because if any of you are like me, my wife goes to the store or Costco, they’re paying up big time for beef. The Department of Labor Statistics noted that the average retail ground beef price is over $6 a pound. That’s up over $2 or 50% from five years ago. So prices are through the roof and hitting our pocketbooks, but yet, still, the price keeps going higher. And we’ll get to some questions at the end as how do we cure this? But before we get there, I kind of want to hear straight away from Joe what’s going on out there in the field. You know that we talked last week, before we did this call about the cattle on feed report and cattle on feed had been pointing to lower placements nationally, and particularly in the south. But up by you in your area, it’s a little bit different. What’s going on?

Joe McKitrick 06:53

Joe, well, thanks for having me on Jeff. As far as placements go the North looks so much better than the South because of the screw worm issue we have and but one thing that you know is an interesting take on the placements is Texas. The Texas feeders are competing for feeders up north and feeders in Oklahoma because they can’t get the feeders, their feeder cattle out of Mexico right now. So it’s creating a demand up here that’s that’s higher than normal on a seasonal basis, and also making it so that the Oklahoma feeders are the same basis as we are dealing with here. So it’s kind of a unique situation to add on to, as you said, already a very large shortage of feeders in general. Yeah.

Jeff Eizenberg 07:48

And the the other part is that you’ve got some quality ground. Obviously, had good condition and good grass, so people are bringing it your way. Is that been something you’ve seen as well? A trend in your direction?

Joe McKitrick 08:00

Yeah, there was a lot of yearlings contracted early. People were, you know, excited about the price we saw in June with yearlings, so they went ahead and contracted them. You know, fear of the unknowns of the marketplace, as we saw now. You know, the market has fully gotten better and better, and there’s a lot of yearlings starting to show up last week, this weekend, next week. The, you know, in the three, four state area, sale barns are starting to receive a lot of yearlings, and receiving them on a very high demand. I mean, the prices just keep going up every day. The Northern index is, you know, some version of 375, 380, on an index sphere. So the prices we’re seeing are just phenomenal. But again, there is a, you know, there, there’s a visible shortage as far as what’s available up here.

Jeff Eizenberg 08:50

Yeah, that makes, makes good sense. And that’s the kind of the gets to the crux of the problem, right? It’s that we’re, we’re trending higher. There’s a lot coming in, and people are looking to sell, taking, taking profits effectively out of the market. How are people feeling about these high prices?

Joe McKitrick 09:07

Well, so 2025, brought in a, a whole new market for us. And like I say, in June, you know, we thought that as producers, they, you know, that was already record prices. And so everybody the video sales saw that to where the volume in June was almost a flip flop of a normal July, meaning the volume of July went to the June sales. And so it’s, it’s just a function of, you know, 2014 and 2015 isn’t a far distance in most people’s memories. And so they That was a short lived bull market. And so people just want to make sure they capitalize on what is in front of them. So, you know, we saw a lot of activity early. There’s still calves for sale, no doubt, but there is a lot of contractor calves already.

Jeff Eizenberg 09:52

And then Dwayne, from your perspective, people are selling. They’re taking profits. They’ve locked in. Some of the opportunity to market. Question starts coming back is, what’s next? Are they thinking about replacing this herd, and in what way are they able to leverage the banks to come in and support buying new calves at this at these heightened prices? Is it even feasible? What do you think?

Dwayne Bowman 10:17

Well, good question. You know, it wasn’t that many years ago, I remember sitting down with one of my producers, you know, it’s probably six, seven years ago, and you know, when we were doing projections on there, and we figured, you know, we needed to get to about $1.70 on a cap to break even for him. And you know that time abs are probably worth about $1.45 and needed to see $1.70 so here we are. Fast Forward, you know, to 2025 and we saw $3 and then we saw $4 and now I’ve even seen some five point cans at about five bucks. So it’s gone up so fast that, you know, I think, if anything, there’s some fear now in the market, as Joe referenced, you know, it’s 1014 2015 that was very short lived. So everybody’s still got that fresh in their mind. But yet, you know, right now, this is it’s going to be, it’s going to be awfully fun. When it comes to the end of this year, these guys are going to have the most money they’ve ever had in their pocket. Last year was a really good year for us in the ranching country here, but we were dry, you know. So yes, you were getting record calves at record cap prices, but they weren’t hanging on to a lot of extra heifers. You know, they were selling down, still on numbers, just because we were so dry, they didn’t have hay in their hay yards. The pastures look pretty bleak. And now this year we’ve received, you know, tremendous rainfall along with these record prices. So there’s a lot of optimism. You know, your question as far as, are they going to replace right now? You know, I would say on the cow calf site, you know, really, that we’re not seeing a lot of demand to increase their numbers. You know, they still remember when they paid 2800 bucks for a red heifer 10 years ago, and never really did pay for that red heifer. So paying 4500 now, there’s not a lot of guys doing that. They’re, they’re holding their numbers. So they might buy a few back, but they’ve also, they’re selling that call Cal for 2300 bucks so they can afford to buy back. You know, $1,000 more, $2,000 more on the feeder side, I think we will see the guys. You know, they’re going to continue to to buy, you know, whether it’s yearlings or whether it’s feeder calves, because they’re coming off of, you know, probably the most money they’ve ever made. So they have to put that money back somewhere. You know, they’re, they’re either, they’re either going to be paying income taxes, which both of them like to do, they’re going to have to put it back into cattle. So it’s, it’s going to be a little more challenging on the on the hedging side, when it looks, when you look on the board and and you’re looking at, you know, a $300 loss at this point, but yet, they know they’re going to have to put it back into cattle.

Ben Hetzel 12:18

Yeah, it’s going to be really interesting. Jeff, too, you talk about what happened the last time we seen prices spike, and this one being such an extreme, comparatively value wise, as a producer myself, small scale, you try to try to remember those things and do things different this time. So whether using futures and options or an LRP product to mitigate some of that risk. You might find yourself looking back on this last summer, earlier spring, and I wish I wouldn’t have bought that insurance or put that position on as a cow calf guy. Now, feedlot guys that are buying numbers and doing that, you know they got to be prudent and hedge their risk diligently. But you know, as a cow calf guy that maybe 10 years ago, never even thought about hedging those calves this year might have been looking, and maybe even in the last few years, looking at hedging them. They’re born or unborn, possibly, you know, and as that product’s changed, it’s it’s made it a little bit different this year. It seems like it’s a little more expensive early on, but the value is much higher too. So value of using that tool, but, you know, we’ll get into that a little later. I think Jeff too that, you know, it’s, it’s still not a, it wasn’t a mistake to to buy that insurance. And some people, probably, I’ve heard it from others that they probably think, man, you know, I wish I would have done that. It’s, it’s kind of a trap that I think producers can get in, and hopefully we can shed some light on why that’s that’s a good thing to be doing anyway. But going forward, it’s going to be interesting to see what the trend is. Continue to edge these calves right after they’re born on an LRP, or start getting into futures and options and understanding those tools that are available to them. I think the trends will definitely depict a new direction based on what’s going on this year.

Speaker 1 14:17

If you want to listen back to this episode or find past episodes of The hedged edge visit kbjm.com or kndc radio.com under Listen Live and podcast options, or either stations free mobile app under podcasts.

Jeff Eizenberg 14:32

Ben, you mentioned something when we spoke the other day about the kind of misconception in the country that the banks are actually forcing people to put on these hedges and lock in losses. And you know, when you’re talking about losing on the calf rate as you buy it, what are your What are you guys thoughts in general, about this?

Dwayne Bowman 14:51

Yeah, like speak a little bit on the bank side, you know, I mean, no, I mean, we’re not forcing guys to lock in, you know, to put on losses. Obviously, the guys that are buying feeder cattle. Buying yearlings. We want them to be prudent and be doing some hedging, and just they’re putting so much money on the table right now, so they know they have to have some type of protection on there. But I don’t think anybody’s going to force anybody into taking a losses. We’re hoping you know that they’re going to be able to when they’re buying. Hopefully that that it looks like a break even at at worst, but definitely be doing need to be doing some type of protecting on, on their end, on the cow calf side, you know, as Ben talked about, you’re seeing more and more guys that are getting comfortable using LRP, a great tool to help kind of take, you know, to lock in some prices for them. And then we’re seeing a lot more guys that are just forward contracting, you know, a lot more hitting the video sales early. And they they understand that so much better. You know, hedging is a is a scary word for a lot of lot of producers, still. But when they forward contract and just know, hey, October delivery, I got 398, that 650, pounds, they know exactly where they’re so they like, they like that part of it. But the hedging is, is definitely going to be, definitely going to be a big piece going going forward, on the on the feeder side, on the fat site, just because there’s so much money at play this year.

Ben Hetzel 16:02

Yeah, that brings up an interesting point the way in that, when we talk about grains, and just for a moment, even though we’re not going to spend a lot of time on today, but oftentimes, in this geography, forward contract, particularly the because you could lose it, you could get hail, you could get lots around different things that happen to lose the job or lose the quality that you’ve guaranteed to the market. So that’s where the futures and options piece or or a product like LRP would would really kind of protect you. But we were pretty comfortable selling cash. And, you know, generally, if they’re on the ground and they’re healthy today, you’re going to be able to be able to sell them. And you know, you it wasn’t that long ago we had a storm called Atlas. If your cattle are contracted in November and we’re in a wet cycle right here, as you mentioned, and it’s you wonder if that’s crossed some producers minds, like, what happens if we get a bad one, you know, maybe they aren’t selling 100% likely not. But if they’re selling a high percentage, and the risk is there that something could happen, it’s usually doesn’t devastating level, but there’s some risk there.

Joe McKitrick 17:15

Going to your comment Ben, about, you know, hedging and doing something with the cow calf side. And we’re, I’m hearing it a lot in our travels that, you know, that was just a waste of money, or the put option, they bought more so the lrps, but they were a waste of money. And, you know, all too much marketing and egg is done on a recency bias. So you know, now that we got 2025 the big run of 25 under our belt, and the recency bias says that was a waste of money. You know, that’s one thing that I’d encourage, is that, you know, don’t give up on adding some protection, because the time that you don’t need it is right around the corner is the time you do need it. And obviously 2025 if you did nothing, that was the best case. But typically somewhere right around the corners when, when you do need your hedging program. So I think that’s an important piece of that conversation.

Ben Hetzel 18:10

Yeah, and I’m glad you went there, because I, I’ve felt like we, we had to touch on that, because, again, you know, personal experience, and obviously you live it every day. Dwayne sees it every day, Jeff, he’s he’s in the trade every day. It’s so important to protect yourself against the risk. And if you’re making money, when you put that edge on, it wasn’t a waste, waste of time or effort or money, because your point is market turn at any given moment, and you’re going to need it, because it may fall faster than it came up, and it catches you by surprise and but yeah, and that was part of that misunderstanding too. Is, you know, a lot of people get in that trap. Well, yeah, I wasted that $60 a head on my LRP, which, when I bought LRP, I said to my agent the day I did it, I said, Well, tomorrow, this might be a mistake, which it was, because it rallied big time. The next day, they said, This may look like, not be a mistake. It may look like a mistake. And I hope I’m wrong in doing this, because that’s a unique tool, just like an option, that it’s a fixed cost, and if the market keeps running, you’re going to capture some of that gain. It’s really unique. And I think producers need to know that, you know, just because you buy that product doesn’t mean you out of the market. You still have opportunity.

Dwayne Bowman 19:29

No, you’re right there. You know, Ben, that’s exactly what we’re hoping for. You know that you never have to use that tool. You know, as Joe said, the best thing the person could have done this year was nothing. Well, that’s we’re right around the corner from where you you know, things could turn the other way, really, really fast. And it’s, it’s the insurance, you know, it’s just the insurance that you’re going to be able to sleep at night having that protection on. Obviously, the bankers, we want to have that as well. We want to have that risk covered. The producers need to have that same thing. And it’s, you know, that’s why we put crop insurance on, you know, that’s why they put hail insurance on, so they can sleep better at night. They hope they never have

Jeff Eizenberg 19:58

to collect on it. Yeah, we’re talking. Working with Dwayne Bowman here, the president of Dakota, western bank. So Dwayne, when we talk about that right there, the relationship with the banker, I think that’s so important. You know, we have a lot of people that you know doing futures and options and other transactions that require the bank to be aware and communicative about where they stand with their potential gains, losses and margin calls. And, you know, we’re on the radio waves, and we use the word margin call, somebody might turn us off straight away. But the reality is that that can happen, and having that open line of communication with the bank in advance is paramount. And so, yeah, I just give you this chance to speak to that. And you know, the way that your bank handles, kind of working with their, their ag loans, whether it’s cattle, grains, whatever it might

Dwayne Bowman 20:47

be, yeah, I mean, the biggest thing when we’re putting their, their operating note together, or putting their note together to purchase the feeder cattle, obviously, a big part of that, a piece of that, is the risk protection, and it’s going to come at a cost, you know, whether it’s going to be put options, you know, and we’re going to build that in, or whether it’s going to be crop insurance. Going to be crop insurance, you know, we’re going to build that into the into the note, we have to manage our risk, and they’ve got to manage their risk. So it’s just, it’s a cost of doing business, but it’s, it’s no different than, than any other business out there. Like you said, it’s, uh, I think if anything, it’s just a lot of lot of producers still are just scared, you know, they don’t know enough about the marketing. They don’t know enough about risk protection, futures contracts, things like that. They’re they don’t have enough knowledge on it yet, but it’s a necessary piece to continue to get educated on. And that’s where I think this, this show is going to be kind of exciting, because hopefully it’s going to provide some opportunities for producers to get educated.

Jeff Eizenberg 21:38

Yeah, thanks, Dwayne, that’s that’s the goal. And really appreciate your feedback and being there to answer those questions in office, and you know they’re there locally. So that’s that’s great. Switch it over to Joe again, where Joe mckich from Bowman? Joe one kind of old trading fallacy out there. Maybe it’s the truth. Maybe it’s not. Is that higher prices cure higher prices. And so here we are. We’re higher prices. What’s it going to take the cure? Cure these higher prices. For the consumer, really? I mean, the the rancher, hey, keep on going. But for the for the consumer, we’re feeling the pinch we’ve got. The other day, I actually, I got a text message from friend up there and in Bismarck, and it was a picture of McDonald’s, and below the drive thru window, it said, financing available. So we all know beef is expensive. What’s it going to take?

Joe McKitrick 22:33

Well, I think you know, going to the McDonald’s conversation, the CEO was on again, and he talked about, it’s his lower to middle income consumers that they’re having a hard time getting them to come in the door. They’re skipping breakfast and eating at home, and he’s assuming that they’re skipping a meal altogether. So any of the consumers that have a household income, I think he used of 100,000 or less, they’re seeing a decrease in traffic. And so, you know, that’s always the fear. You know, the Packers, the funds, their job is to, you know, get prices as high as they can. They’re not really in it for that longevity of as much as today’s price. And what can they make a profit out of it today and and, you know, so that just say, what is going to limit demand? That’s to be seen. But obviously, if McDonald’s is saying that we’re limiting some demand today, the concern is permanent demand loss, since beef high and the wife goes home and makes a different meal, and then the family is okay with that meal, you know, based on pork or chicken, five years down the road when beef not as high, obviously, chicken still going to be cheaper, pork still going to be cheaper than beef at that time. Are they going to stick with that and not, you know? So we have more permanent demand law. There’s already conversation with a few fast foods are mixing pork with their beef for for ground beef. So concern of permanent demand laws is what is on every producers radar, that that the ones that we sustain the industry over a 20 year span, and we’re not just in it for the short term gain, like a fund is or, you know, packer is for the day. So I think that’s the real conversation is, how high do we have to go? We went to 475, and made during covid, and there’s a lot of forecasts that will get there fairly easy again that’s to be seen.

Jeff Eizenberg 24:28

Yeah, you know, from from where I sit, I’m feeling more and more as I talk with gentlemen like yourselves, then it’s really going to take the rebuilding of the herd and the numbers getting higher to drive that pricing back down. What are your thoughts? How long is it going to take to really, truly rebuild a herd?

Joe McKitrick 24:47

Well, so there’s two packers that have came out recently and said that, you know, we’re dealing with anywhere from three to six more quarters of really tight supply. And then, you know, getting to more normalization. What? How? However they define it. They did not define it in their in their notes. But you know 2027 being closer to more normalization. So assumably, we’re going to see some herd expansion somewhere along the journey that provides that

Speaker 1 25:15

want more agricultural market expertise. Listen to full episodes of the hedge edge podcast, wherever you get your podcasts, or visit RCM, ag services.com, get the complete market analysis and strategies you need to succeed.

Jeff Eizenberg 25:29

The other question that’s going to come into play here Dwayne is interest rates. You know, we know President Trump’s been pushing for lower rates. What are your thoughts? How is interest rate play going to either support or impact the the herd expansion on the cattle side,

Dwayne Bowman 25:47

yeah, you know, really what I’ve seen the last few years with rates going up, it hasn’t had nearly as much impact on the Ag side as you’d expect. You know, land prices have been strong as ever. Have continued to go up. So in a producer actually said this to me the other day. He said, you know, interest rates, to me don’t mean, don’t, don’t mean nearly as much as as commodity prices. And he’s right. You know, commodity prices and weather are a much bigger factor and impact than interest rates. So I think we’re going to see interest rates go down. I don’t think that’s going to have a big impact on what cattle prices do, you know, like you were talking what kills, you know, high prices. You know, it’s high prices. And I think what, what we’re finally going to see at some point right now, the consumption, beef consumption in the US has been very stable. The last three years, it’s been right around 58 pounds per capita. So that isn’t changing. So at what point, you know, does the price cause them to go elsewhere? Chicken is still, you know, twice the consumption that beef is, but you talked about, you know, the $2 difference there is, I don’t think it’s enough difference right now that the consumer still knows that they enjoy, that their lifestyle, they know what they like. And we are, we’re definitely in a in a lifestyle to where we know what, what we appreciate, what we like, and as long as we can afford it, we’re going to continue to stay that way, like you talked about financing, you know, I thought this was kind of interesting. I heard this the other day about, you know, people love convenience, so DoorDash, you know, they love that. And you know, they’re gonna order that cheese burger from McDonald’s, and they’re gonna get fries and they’re gonna get their frosty. And next, you know, they’ve got a $17 meal, and they’re paying five bucks data delivered. So they’ve got 22 bucks, and they’re putting it on a credit card that they’re not paying off at the end of the month. Jeff, so you’re right, yeah, and that’s the lifestyle. So it’s going to come a point when they can’t, you know, make those payments, when they really are feeling the pinch. That’s where there’s going to be some lifestyle changes. And then we may see some adjustments on beef.

Joe McKitrick 27:36

I think Dwayne brings up a good point there too. That’s worth noting. Is the even though beef high, it’s not like chicken and pork are dirt cheap. Those competing meats have done a good job of trying to follow beef up, yet stay a little bit cheaper so that they maintain their demand. But if you notice that, you know that those meats are that’s just kind of in a silent move. So it’s not as big a disparity as one would say.

Ben Hetzel 28:07

The interesting thing would be the margins at the production level, you know, is, is the producer that’s raising, you know? And I know it’s all pretty well confinement related production, but where’s the margin, and all that landing. Jeff, you and I had a conversation the other day about what some of these fast food chains might be doing to encourage that middle class, lower class consumer to come into the store or the restaurant and and buy some, buy the meals, or whatever fast food. And it’s really interesting, they’re, they’re focusing a lot. If there’s traditionally a burger joint, you know, say, McDonald’s or or one like that, that, you know, first thing a lot of us think of is the Big Mac or some kind of a quarter pounder type thing. They really focus in there. They’re happy their daily specials, or whatever the meal deals around chicken.

Jeff Eizenberg 29:05

Yeah, I think we, think we saw, we looked it up. McDonald’s CEO came out and said, Oh yeah, we’re gonna bring back the value meal. And they have six new value meals. Well, five out of six are chicken, chicken related. So there, there you go. They’re trying to drive towards profitability. Shifting course here to the last question. Ben, I think this one is really slated for you, if you think about it, you know you got your finger on the pulse of the grain market, there at Scranton, at the at the elevator and the Co Op. Where are you feeling like the opportunities are in thinking about from the feed side and from the ranching side, is there really, is this a level that people should be coming in and thinking, Okay, how should I lock in and forward price some of my my feed?

Ben Hetzel 29:51

Yeah, we’re seeing some increased interest in locking in grain longer, earlier, longer, you know, whether or not you. Seasonally, this is traditionally. Maybe we’re coming into that, that lower price point where nervous ramps up the volume hitting the facilities and basis widens out. But I think some of them are trying to get ahead of it, even trying to figure out, how can we get some corn or maybe a different sheet stuff laid in earlier and have more of it on hand. I’ve actually heard of some feed lots building bins because they want to store more supply, which, you know, there’s all kinds of arguments around whether that’s a good idea or bad idea. It depends on your operation, probably as much as anything of what, what’s prudent there. But, you know, we got a big drop, especially geographically for us, we’ve got some pretty big drops staring us in the face, and it’s going to be tough to keep all of it moving at once. You know, locally, we’ve got as good a wheat drop as we’ve had. And it may not be a record, but it’s, it’s not gonna be too terrible, far off. And for some producers, and you know that’s, that’s just one of the crops they’re raising at extremely high levels of production this year, sharing a lot of good yields on other other crops, whether it’s keys, canola, flax, all of them are really good this year. And then we got probably what looks to be one of the the best corn crops I’ve ever seen. And I know Dwayne and and Joe. You guys travel this area a lot, too, and it kind of looks like Minnesota around here. You know this corn you drive down the road, you can’t see over the fields, and a lot of times the corn doesn’t get that Paul and and the height of corn isn’t always the the whole story, obviously. But when you talk to growers, it’s they’re just talking about how phenomenal is. So there’s opportunities coming for these guys buying feed. I guess to me, anyway, it feels like basis should widen out, you know, a little bit anyway, from where we’re at. And the big question will be how much export business that we pick up because of the lack of the soybean export program. You know, the facilities on the coast, the P and W, the Gulf, they’re going to have to elevate grain to keep the facilities buzzing. So they’re going to be looking to fill it with corn or wheat, you know, here in this this next quarter. So, you know, it looks like, even if China were to come in and be interested in some beans, it’d be tough for the US to execute on the P and W a bean program with what’s been put on the books for corn. So as long as demand stays high, maybe we, maybe we slot no here, you know, protect your risk on the board, you know, and, and the basis risk based on seasonality,

Jeff Eizenberg 32:44

makes sense, and Joe as your what’s your sense on that bin building at the on the feed lots, something you see as you travel?

Joe McKitrick 32:53

Well, there’s a lot of conversation about how to take advantage of it. You know, for the first time in probably two decades, you know, like southwest Kansas has a negative corn basis in areas and there’s just a loop. There’s a massive amount of corn growing this year, and like Ben saying, it looks like Minnesota in areas that are fringe acres, and maybe they’re normally 60 to 85 bushel or 100 and 100 plus.

Ben Hetzel 33:21

So yeah, say it 150 plus.

Joe McKitrick 33:25

Oh, yeah. I mean, I never thought we’d have a hot, you know, a 2023, corn crop, again, in the fringe acres, but it looks like we’re going to, and, you know, you get into western Kansas from north to south is there is a mountain of corn this year western South Dakota, same thing. So, yeah, there’s conversation of how to, you know, there’s a lot of places that are going to make a wet corn pile that would maybe normally make a small one, that are going to make, you know, one day last three quarters of the winter or something. And so, yeah, there’s a lot of conversation how to take advantage of this, you know, the large crop and and really large basis at harvest too.

Jeff Eizenberg 34:05

Looking ahead into 2020 end of 25 and end of 26 What are your thoughts, Joe,

Joe McKitrick 34:12

so 25 was a a demand driven market, and as we go into 26 we’re getting into a supply driven market, where the shortages of supply or the constraint is becoming the larger, and so the structure of the market changes. The safety of a demand driven market is greater this you know, the clarity of that it’s going to go higher is greater than a supply driven because there’s so many outside forces that could affect supply exports the Mexican import. So I think the you know, the conversation leads to what could potentially put a final top in this market, and and one of them is the NCBA is putting a lot of pressure on the USDA to do something about this Mexican feeder cat. Import situation, the Texas yards, you know, there’s a lot of Texas yards that make a living off of feeding Mexican feeder cattle. And in fact, the largest feed yard conglomerate in the US is only at 40% capacity, and not totally because of no imports of Mexican feeder cattle. But there’s a, you know, that’s a part of the situation. So, you know, what could put the final top in is, you know, the opening of the border. The other thing that’s, you know, transpired since last week is the Trump’s tariffs are now under pressure, judicially, yes, and if something like that changed to where Brazil could ship directly to the US. And so when you add in that, we’re increasing Australian imports as fast as as they can do it. And then you add in the Brazilian side, and then you put this, you know, the screw worm situation, in the rear view mirror. That’s a lot of headwinds for the market to keep going higher. And so then the supply driven side of it in 26 becomes a question mark of how, how is that going to affect supply? Obviously, demand is not going to fall out of bed, so we still have demand, but we don’t have demand as a driver. That takes us to a whole nother level from here, where, whereas supply of supply stay tight, we could go quite a bit higher. But given the factors at bay that are being held at bay, if any of them come alive again, there is serious risk to the market. And as we talked last week, there’s a lot of air gap to the market too. We came a long ways, really fast in 2025 and markets like to take it away as quick as they put it on too.

Jeff Eizenberg 36:42

So that’s the old other trader story. Yeah, take it away as fast as it came. Yep, exactly.

Speaker 1 36:48

If you’re enjoying today’s show, check us out on Facebook. Just search RCM, ag services for market updates and tips. Find us on Facebook today.

Jeff Eizenberg 36:57

Dwayne Ben, any

Dwayne Bowman 36:58

final thoughts? Well, I think, just to piggyback a little bit on what Joe said, you know, I think he’s exactly right. You know, the, I would say the imports is going to have even a could have a potential bigger impact than, than we keep talking about. You know, our US, cattle being down. I think we’re down 500,000 but we’re, what do you say? Jeff, 86 point 7 million cattle in the in the US. But I think globally, it’s 1.5 7 billion, you know. So the US is really a small piece of this. So the imports could have a have a huge impact. Tariffs could have a big impact, compared to the demand side, as Joe talked about, I think that’s going to stay pretty

Ben Hetzel 37:32

stable, yeah. And I think one, one last comment I have in regard to the beef talk, what a scenario to be in, though, good demand, as good as it’s ever been, not only domestically, but good demand for us, beef globally. And now you’ve got some supply constraints that can fuel the fire. So from a commodity standpoint, it really doesn’t get any better than that, you know. And so one without the other can be fun, but if you have them both, and you’re on the right side of it, it can be really exciting. But again, you know, where does that end? Where’s the party shut down? And so that’s, that’s really what we’re here talking about. And navigate markets and situations that whether it’s good or bad, like you said, Jeff, so happens the cattle market is fun to talk about today. Wheat markets, so, you know, we’ll get into that. But regardless, if you’re at the top, there’s tools out there, you know, RCM, egg services, whether it’s Jeff out in Ohio, some of the other brokers around the mid states here, or myself in Scranton, North Dakota, Scranton, equity. The tools are there. We’re more than happy to help people understand them, and that’s why we’re talking about it.

Jeff Eizenberg 38:50

That’s good. Well, you know, again, today’s been a great day. It’s been great to kind of talk with all of you guys. Obviously, Dwayne and Joe for joining the show and Ben shared at the beginning is that this is the most important part, is that you’ve got a team around you. There’s people in and around the area that are knowledgeable about different parts of the business, that have had different types of experiences. Come if you’re on the on the grain side and the you’re talking to a rancher, ranchers talking to a corn or wheat farmer, it’s just a different conversation. And you can learn something you pick something up, obviously, having great quality relationships with your bank, your co ops, your brokerage firms, again, be super important, particularly in these difficult times, whether the top or bottom of a market, the emotional cycle that We’re in is real. And again, our goal, and having having this show on the radio is is to be able to share experiences like Joe’s and Dwayne’s events in my my own through throughout the radio waves, and get some feedback from you all, and hoping that you stop into the co op or give Ben a call, or just check in on. The podcast and catch up with us next week.

Corn made slight gains on the week with very volatile intraday markets. The Ukraine and Russian news continue to stay in the market and will likely dominate headlines until it ends. Other news worldwide is that South America got rains in southern Brazil and Argentina, with dry central and northern Brazil. Russian officials announced that they would suspend fertilizer exports through the end of the year, presenting a supply crunch across the world. This week’s USDA report was nonexistent in the markets as there were no surprises. As mentioned last week, Ukraine’s corn crop may not get in the ground as only 60% of seed is on farm; this will be important moving forward as world balance sheets get tighter.

Corn made slight gains on the week with very volatile intraday markets. The Ukraine and Russian news continue to stay in the market and will likely dominate headlines until it ends. Other news worldwide is that South America got rains in southern Brazil and Argentina, with dry central and northern Brazil. Russian officials announced that they would suspend fertilizer exports through the end of the year, presenting a supply crunch across the world. This week’s USDA report was nonexistent in the markets as there were no surprises. As mentioned last week, Ukraine’s corn crop may not get in the ground as only 60% of seed is on farm; this will be important moving forward as world balance sheets get tighter.

Soybeans made small gains this week despite the wild intraday volatility. The USDA trimmed South American production again in this week’s report as they continue to baby step lower to what will be a smaller crop. World edible oil prices were up on the week pulling bean oil and soybeans higher. The Black Sea area’s worry and trade have affected the oils market, not just wheat.

Soybeans made small gains this week despite the wild intraday volatility. The USDA trimmed South American production again in this week’s report as they continue to baby step lower to what will be a smaller crop. World edible oil prices were up on the week pulling bean oil and soybeans higher. The Black Sea area’s worry and trade have affected the oils market, not just wheat.

Wheat fell hard this week with an expanded limit down the day with a small bounce on Friday heading into the weekend. All the short wheat positions that were getting run over had the opportunity to get out this week with the move down. However, the unknown in eastern Europe and China having its worst winter wheat crop on record means there is still upside with volatility. Friday’s gains were welcome to see after three days of large losses. The cash market will be essential to follow as it will help determine the fair market value.

Wheat fell hard this week with an expanded limit down the day with a small bounce on Friday heading into the weekend. All the short wheat positions that were getting run over had the opportunity to get out this week with the move down. However, the unknown in eastern Europe and China having its worst winter wheat crop on record means there is still upside with volatility. Friday’s gains were welcome to see after three days of large losses. The cash market will be essential to follow as it will help determine the fair market value.