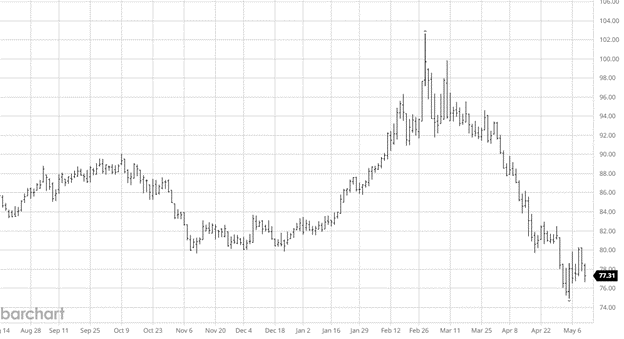

Recap:

The challenge coming into the year was curbing enough production to offset the slowdown in housing. The economics are simple. Demand slowed at a quicker pace than most would have expected. The question now becomes whether demand is slowing at a pace that hurts the market. Are we done?

Since 2019, all I have heard was the amount of business showing up on traders’ desks, even at the COVID lows. Every bearish run was only temporary. I have not heard those words all year. It looks like the old business has now run out of steam. Without China and Europe, our market has to rely on interest rate fluctuations to add sales. That is a tough reality, but at least we see an uptick in interest when rates pull back.

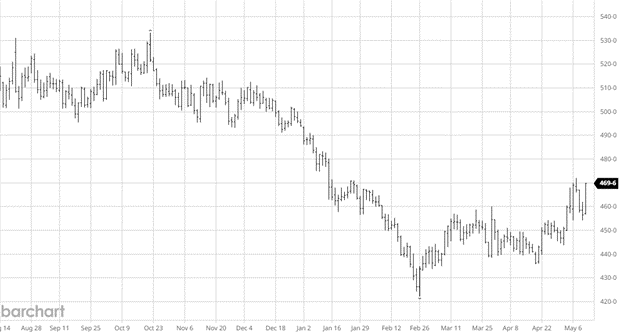

I believe I am making a case for why futures dropped $58 in three days and $100 in seven weeks, not a bearish call. Reality has set in. Lumber, being a very efficient market, has drained much of the excess. The two traditional takeaways from this cycle are that the lows aren’t in. There will be a constant struggle for the rest of the year. The other takeaway is that now the trade will run inventories down to dirt. We are in the middle innings, so don’t get too bearish.

Note: There is no changing the way a commodity can be produced 24/7 and is so tied to the economy. There is no formula, swap, or EFP that will help. Historically, mills set up reloads and then abandoned the strategy. They move to contracts, etc., and then abandon that strategy. Any way you look at it, in a falling market, the mills need to protect supply, not push it out. Oversupply comes in a quick second. On the buy side, I saw limited selling this week even though the market fell $58.50. Those with inventory have no excuse. It is a one-button push, back to the grind.

Technical:

The computer is pushing the market lower, but the technicals don’t see it. The critical point is 424.50. That is major support. If the futures market gets there, it will be after adding a ton of longs. As of Tuesday, they continue to add. This doesn’t end well. That said, the longer-term indicators are entering into an oversold condition. It takes time for that to create itself, but it’s something to watch.

FYI, the tech read last week was up.

Daily Bulletin:

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

The Commitment of Traders:

https://www.cftc.gov/dea/futures/other_lf.htm

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636

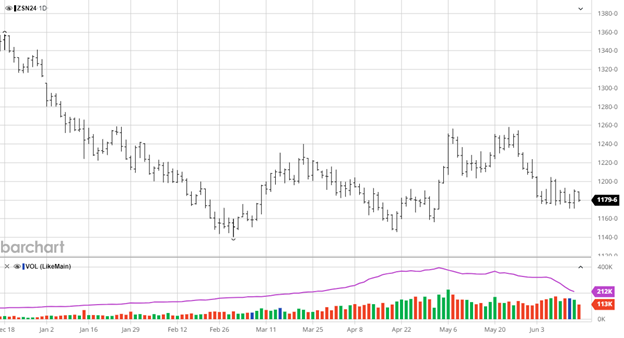

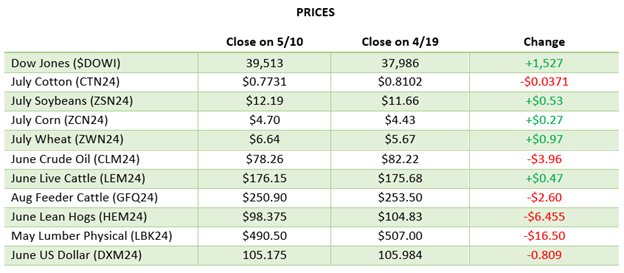

Beans are lower over the last 2 weeks with them settling into a flat trade this week. The USDA report was uneventful despite the USDA cutting another 1 mmt from Brazil’s bean crop. US exports were revised lower and ending stocks rose as the slow pace of exports continued. With no major surprises and no major weather/production issues yet there is not much bullish news outside of CONAB’s Brazil production estimate which is 207 million bushels below this week’s USDA update.

Beans are lower over the last 2 weeks with them settling into a flat trade this week. The USDA report was uneventful despite the USDA cutting another 1 mmt from Brazil’s bean crop. US exports were revised lower and ending stocks rose as the slow pace of exports continued. With no major surprises and no major weather/production issues yet there is not much bullish news outside of CONAB’s Brazil production estimate which is 207 million bushels below this week’s USDA update.