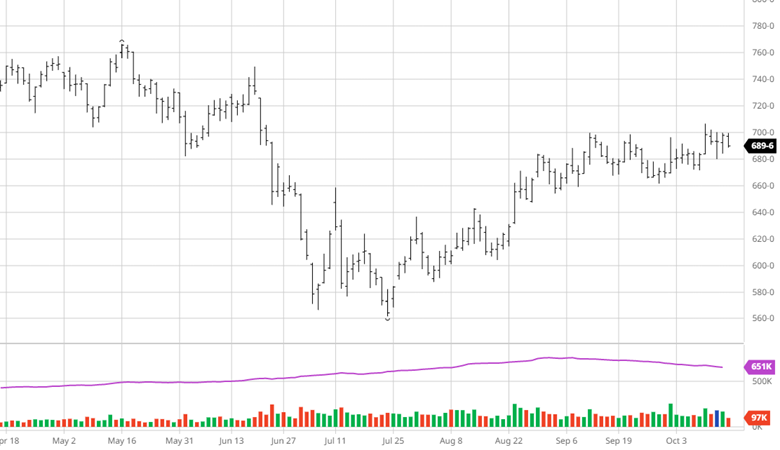

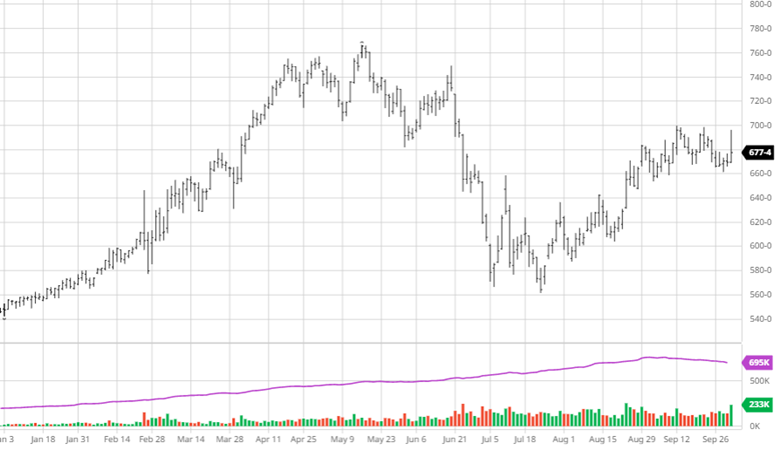

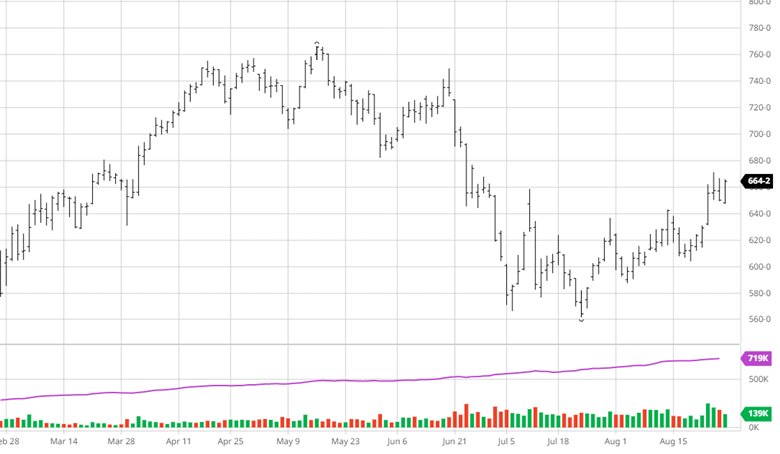

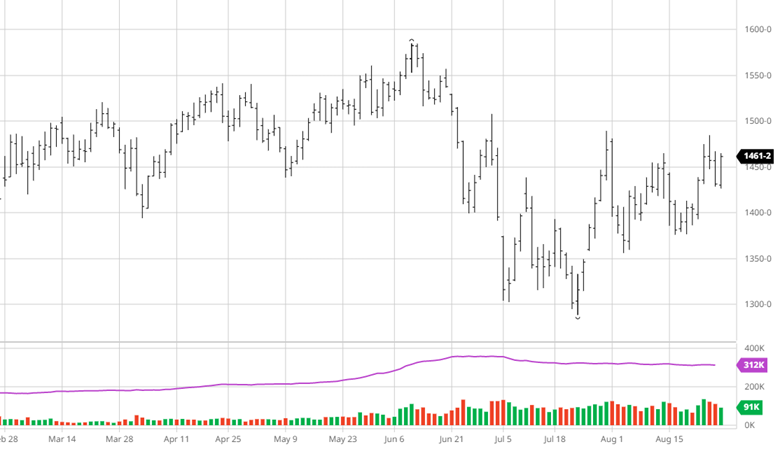

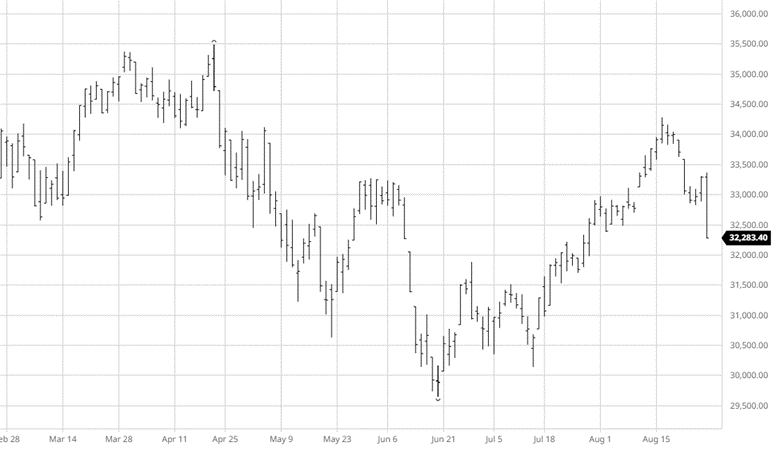

Weekly Lumber Recap

11/6/22

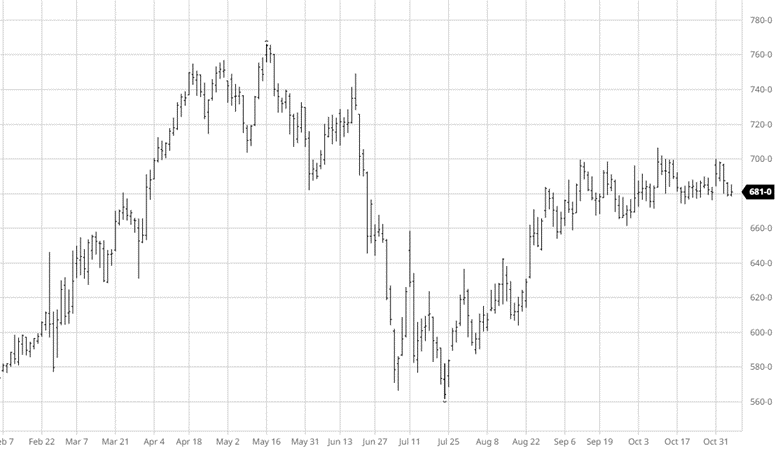

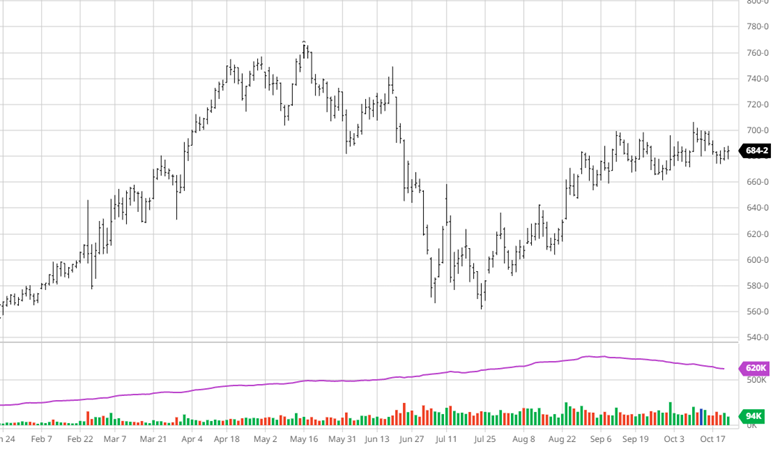

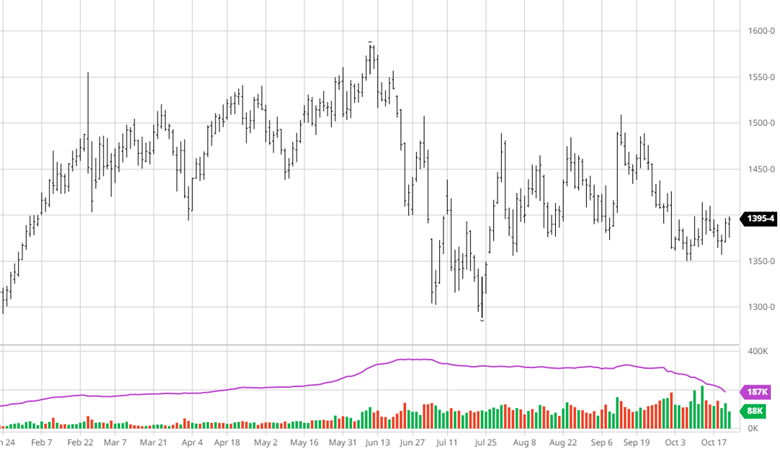

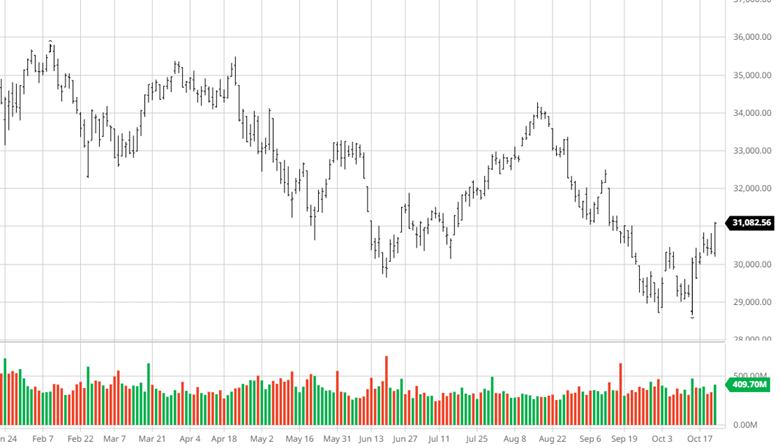

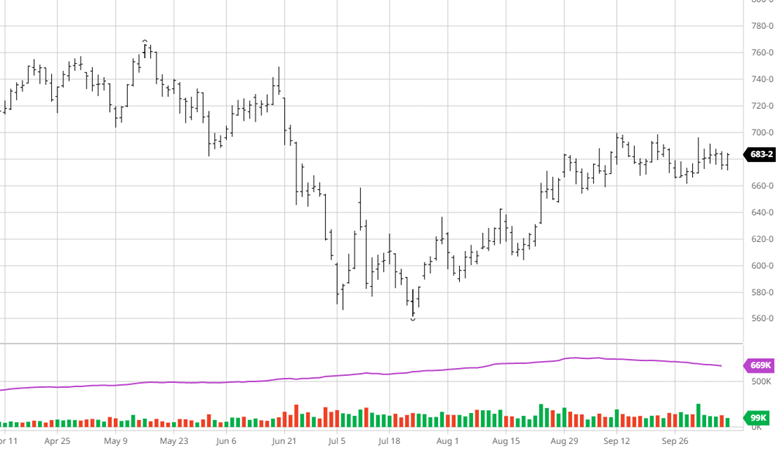

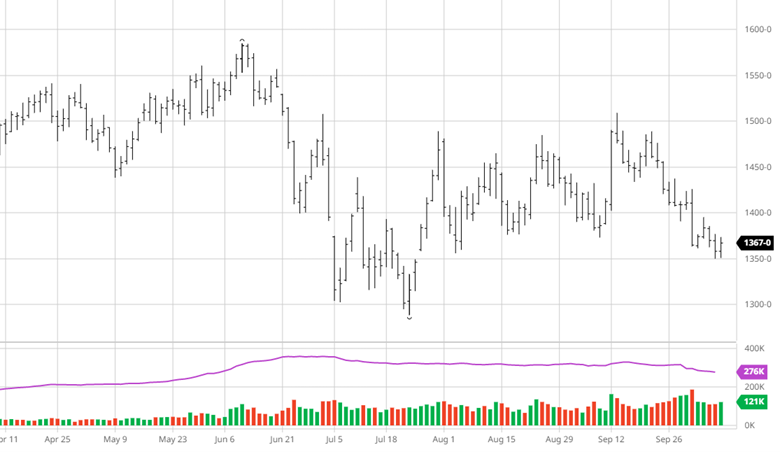

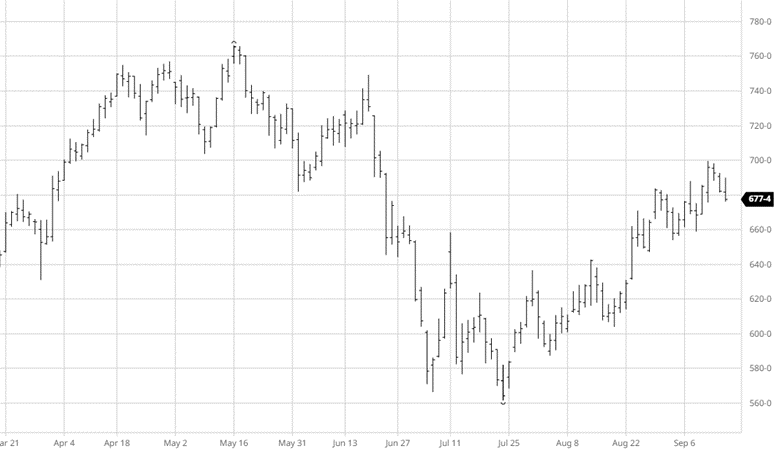

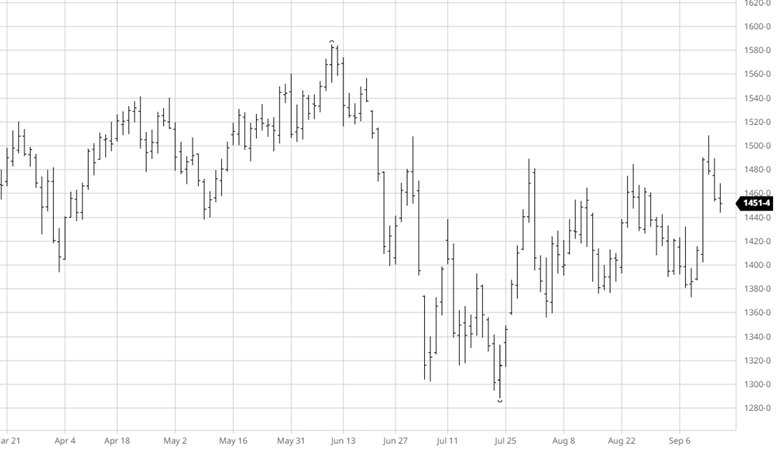

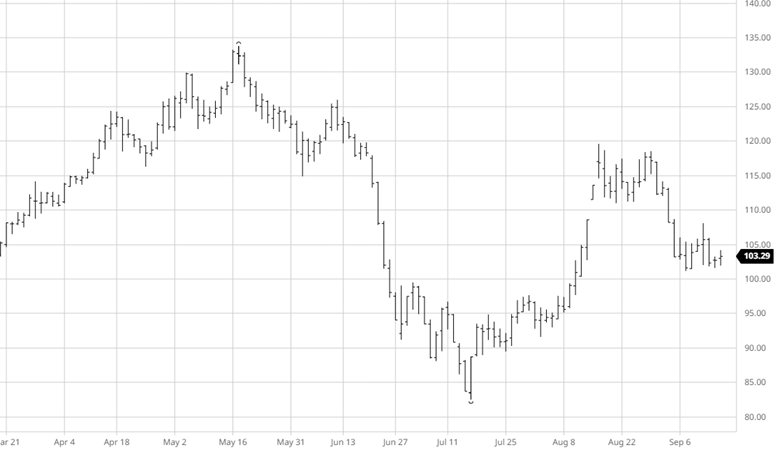

It has been 11 straight weeks of a trading range between $430 and $550. I have been able to cover virtually every negative or positive effecting this industry during that time. What we do know today is that single family homes are no longer affordable which will show in the data at some point. On the multifamily side there continues to be very profitable sales and/or rentals. Given those two points the question becomes how much wood needs to be taken out of the market before it reaches equilibrium. Let’s rehash some of the key points to see if any are indicators yet.

The builders are going to lock it down going into 2023. That is a given. I am seeing indications that the buy side is already gearing up for it. There is no building of inventories. It is a buy as needed cycle. With prices going down, it is a simple and efficient process. Just remember a zero inventory policy when construction isn’t dead sometimes backfires but in any case it will keep things lean. To sum it up, we are looking for a falloff in starts and a general zero inventory policy.

Supply will be curtailed. There will be continued moderate reductions. I expect to see less Euro as they work through the winter. I still expect to see a pickup in China. They have not been in the market for a very long time. Finally, we always have rail disruptions from the possible strike in a few weeks to winter issues. There will be less wood in the system.

The problems today are all the unknown’s. This is driving the zero inventory policy in the US. Someone said it well Friday when she mentioned that the Fed is “burning growth.” To be clear they are slowing down an overheated economy. An economy that they overheated. This back and forth will cause something to break. If the only thing to break is housing then we are close to being done. If there is more we will feel that effect.

The trade has many unknowns and stuck in a range. This upcoming week has the election and probably news of preparations for a possible strike. It’s hard to be short futures but I don’t expect to see much cash activity because of it.

Buy January calls and take the rest of the year off….

NEW CONTRACT:

Lumber Futures Volume & Open Interest

CFTC Commitments of Traders Long Report

https://www.cftc.gov/dea/futures/other_lf.htm

Lumber & Wood Pulp Options

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636