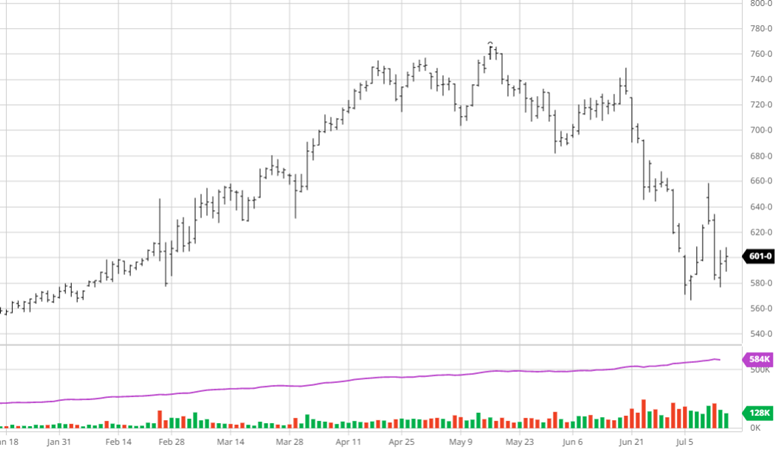

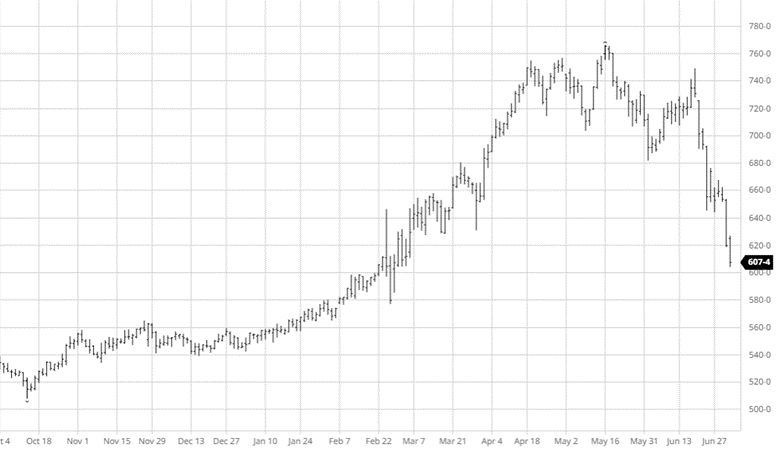

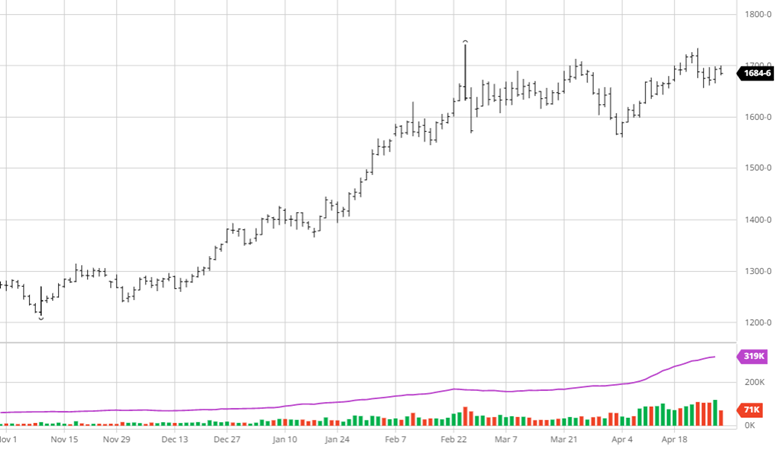

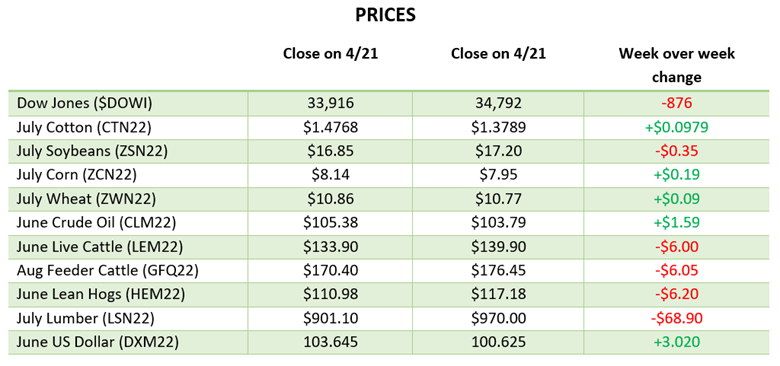

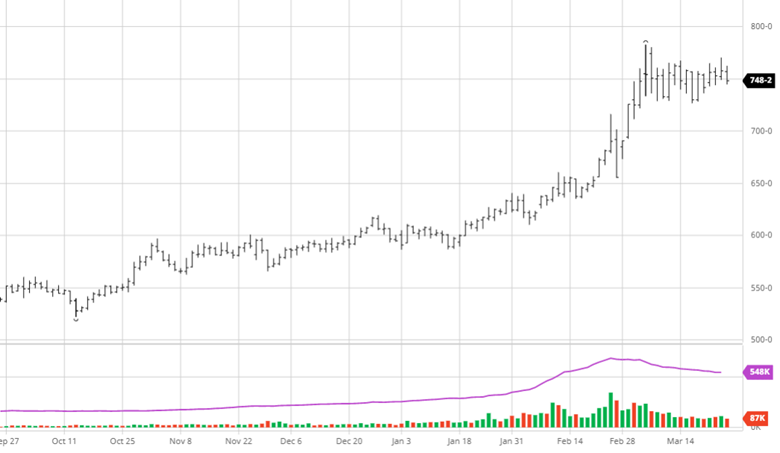

Corn had a volatile week suffering losses to drop back to levels it saw at the start of last week. The USDA report on Tuesday this week wiped out the gains from last week after a bearish report. Ending stocks came in higher than expectations, not by much, but enough to be bearish. The recession fears affect every market and corn is no different as ending stocks will grow as less ethanol is produced and other uses will lower. The weather is the bullish factor in the market right now with hot and dry conditions expected across much of the corn belt during pollination. The longer this weather outlook stays, the more bullish it will become as yields struggle. Russia says they have agreed to a safe export corridor for Ukrainian grain.

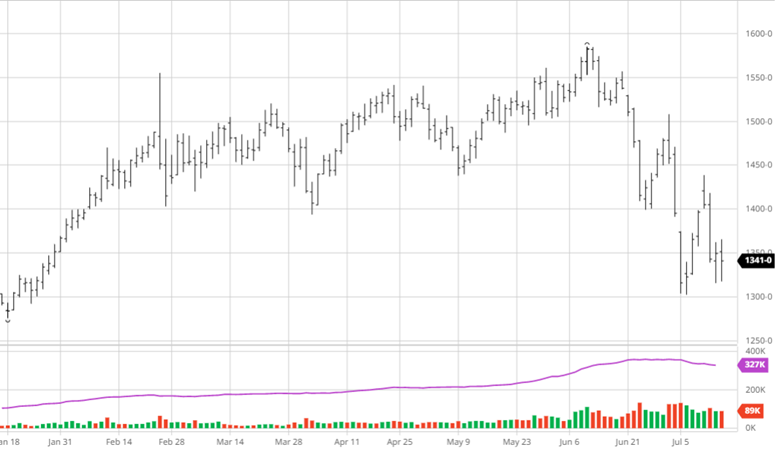

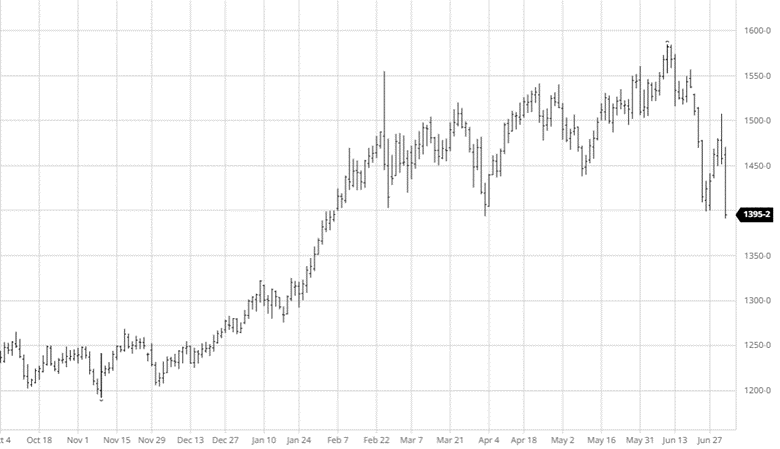

Soybeans took it on the chin post report just like corn. While the report numbers were not overly bearish the loss in crude oil and soy oil prices have weighed on beans lately. The weather issues for corn are not as big a concern for soybeans (yet) but will be something that could come up in the future. South American yields are still hard to get a full picture of with the USDA still differing from many estimates. China canceled a bean purchase on top of a poor export report for the week.

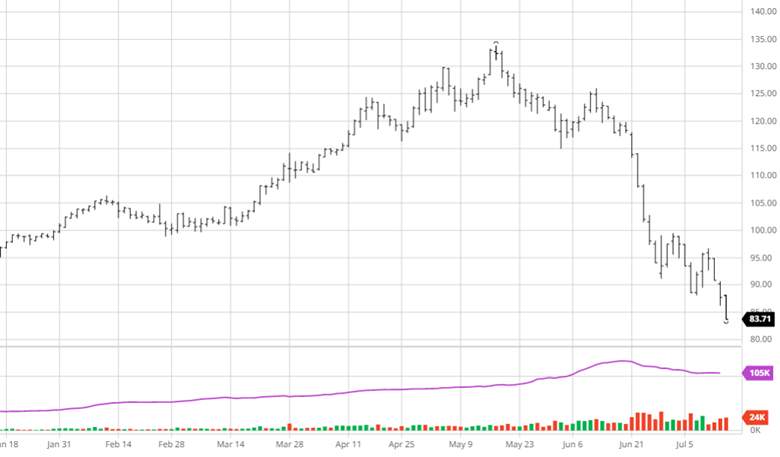

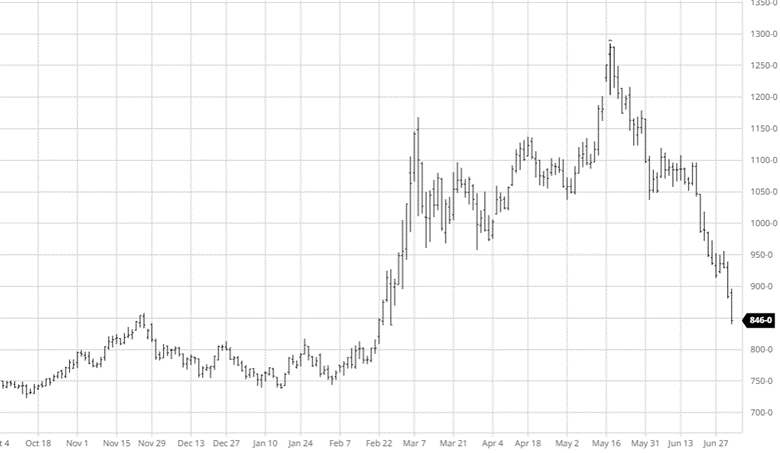

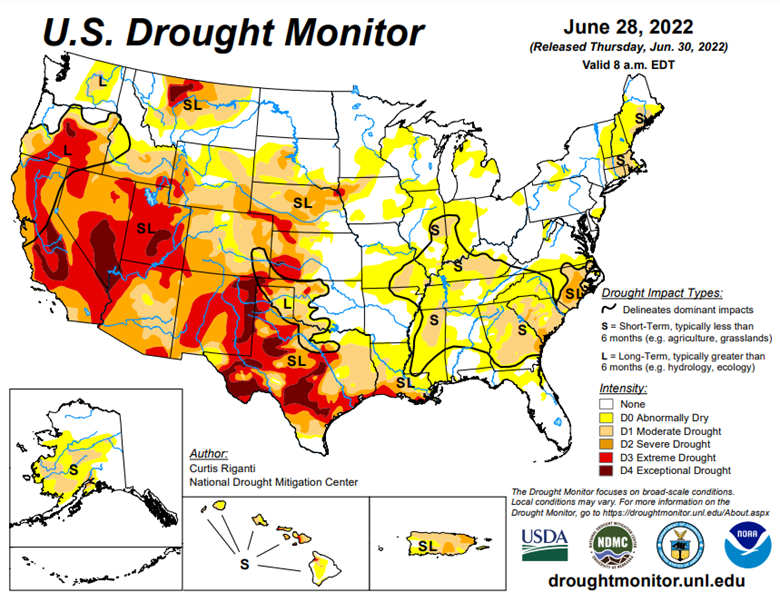

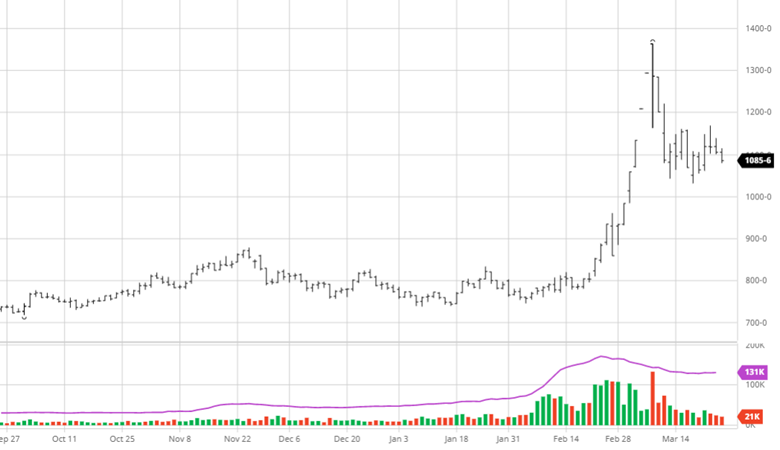

Cotton has continued its move lower despite widespread abandonment in west Texas. This comes from the expect of demand destruction with a potential worldwide recession ahead and producers sitting on plenty of supply. Prices could be even worse if the US was having a good growing season, but the demand destruction along with a very strong US dollar does not help cotton. With the loss of many hedgers in the market due to the loss of crop, specs will be the market mover, trading on technical indicators, not fundamentals, for the foreseeable future and will decide the direction with mills on the sidelines too.

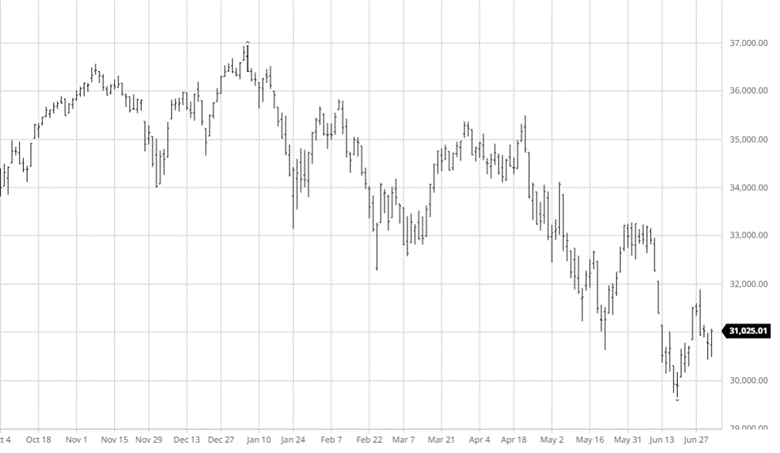

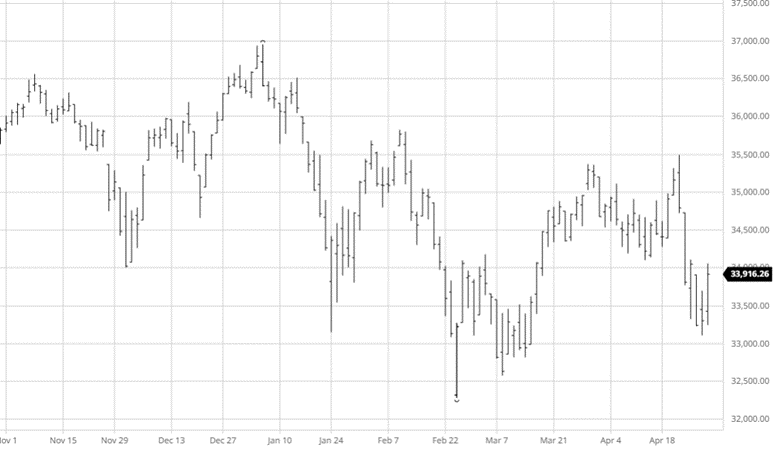

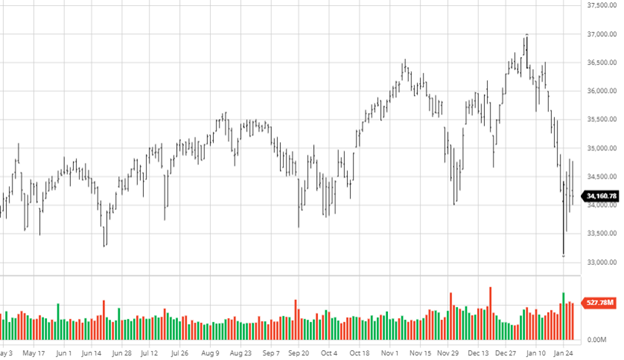

The equity markets continue their game of “recession or not” with the up and down trade. Another hot CPI number of 9.1% came in this week, the market was expecting it to be in the high 8s so this was still a bad number. While commodity prices have come down other areas of the market remain painful. Earnings this week were disappointing for banks kicking a market that was down and needed some positive news. The market will continue this back-and-forth game until everyone decides we are in the clear or the recession is unavoidable.

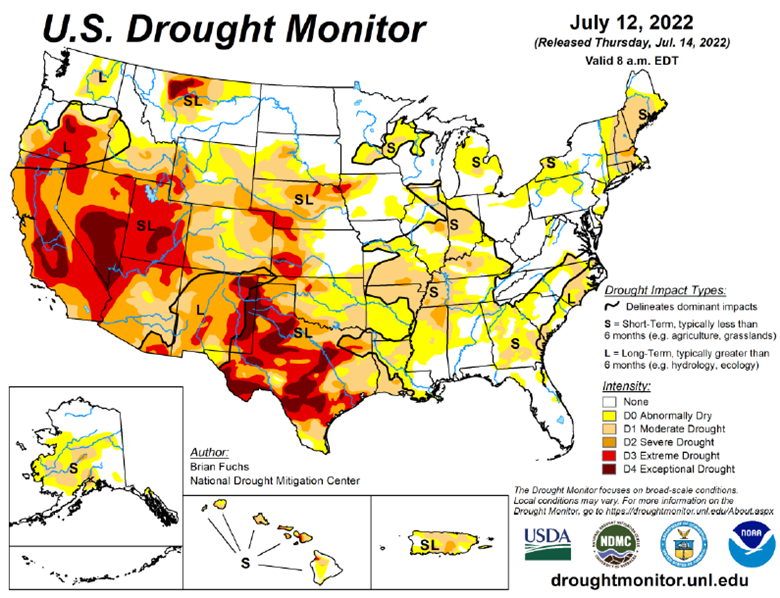

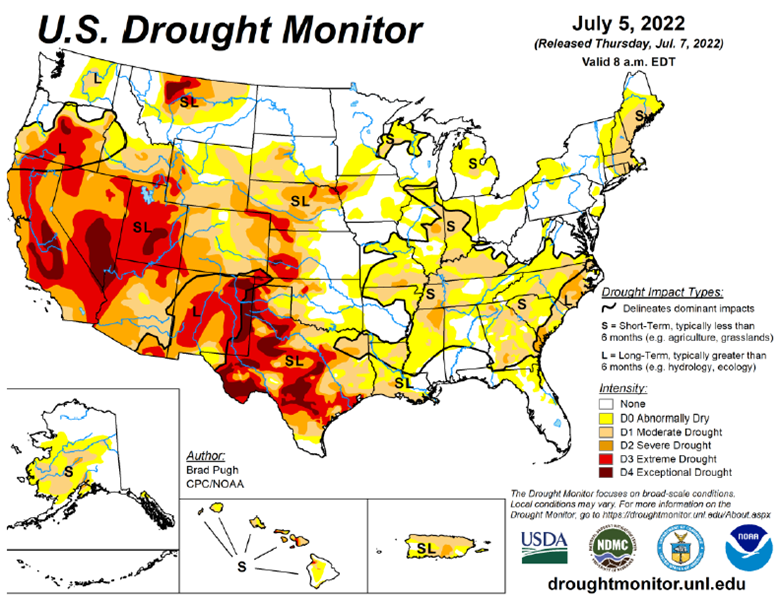

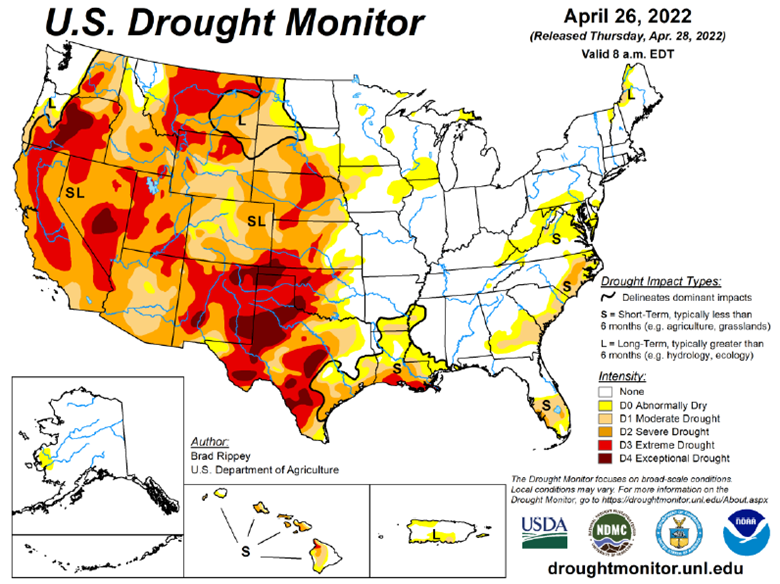

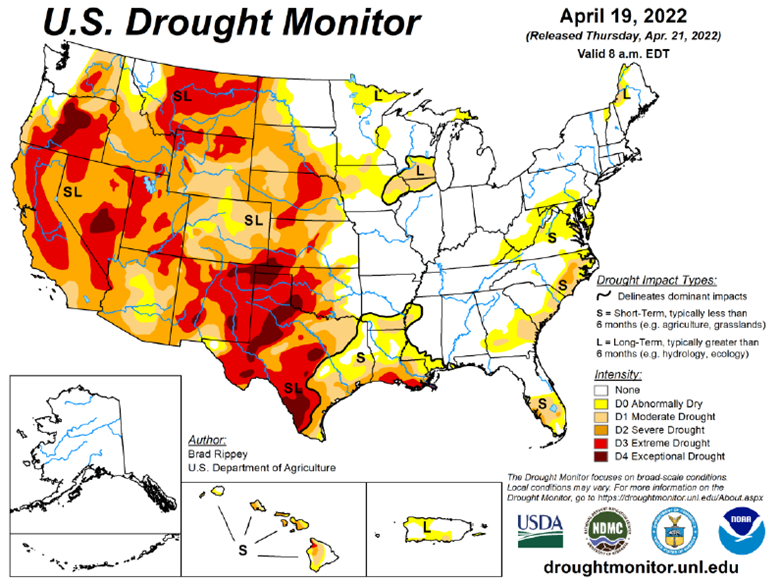

The drought monitor below shows where we stand week to week.

Podcast

There is an agriculture tug of war happening across the nation, impacting America’s farmland. Fertilizer prices are continuously fluctuating, and it has us taking a page the “The Clash” should we stay, or should we go?! And we aren’t the only ones. Many farmers are asking their agronomist and chemical salespeople, “what will fertilizer cost me the rest of the season, and what are my options if I don’t want to go all-in on my typical fertilizer treatment plan?”

In this episode of the Hedged Edge, we are joined by a special guest who needs no introduction in his local circle, Dick Stiltz. Dick is a 50-year veteran of the fertilizer and chemical industry and is the current Agronomy Marketing Manager of Procurement fertilizer and crop protection at Prairieland FS, Inc in Jacksonville, IL. He is at the pulse of the current struggle and here to discuss the topic at hand.

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Corn reacted negatively to the Stocks and Acreage report this week despite there not being any surprises and the numbers coming out close to pre-report estimates. Planted acres came in at 89.921 million acres (89.861 million estimate) and June 1 stocks were 4.346 billion bushels (4.343 billion estimate). The bearish news is improving weather after the 4th of July with rains expected across most of the corn belt. The concern over the wet spring causing prevent plant acres in ND and MN does not appear to have come to fruition with high prices motivating farmers to get the crop in the ground. Trading resumes Tuesday morning after the long weekend so any change in weather or world news could lead to a volatile opening after another kick in the teeth on Friday.

Soybeans had a good week making solid gains before dipping after the report and then getting crushed today (Friday). The bean planted acres was 88.325 million acres (90.446 million estimate) and June 1 stocks was 971 million bushels (965 estimate). The acres number was surprising as it came in 2.121 million acres below pre-report estimates. While the favorable weather for corn is also favorable to beans, they have a different story than corn to follow. Chinese demand needs to return to the market but 2+ million acres of production is a lot to be off by. The inability for Soybeans to break out higher following the report shows that they still have a fight ahead of them and that outside market risks likely have an impact on prices. Friday’s trade hit beans hard and the long weekend holds uncertainties.

Wheat moved lower on the week pre-report and continued lower after it with no surprises only to get crushed on Friday. All wheat planted acres were 47.092 million acres (47.017 million estimate) and 660 million bushels in June 1st stocks (655 million estimate). After a tough Friday, wheat has plenty of non US weather related news to follow and any developments over the 4th of July weekend will be seen on Tuesday.

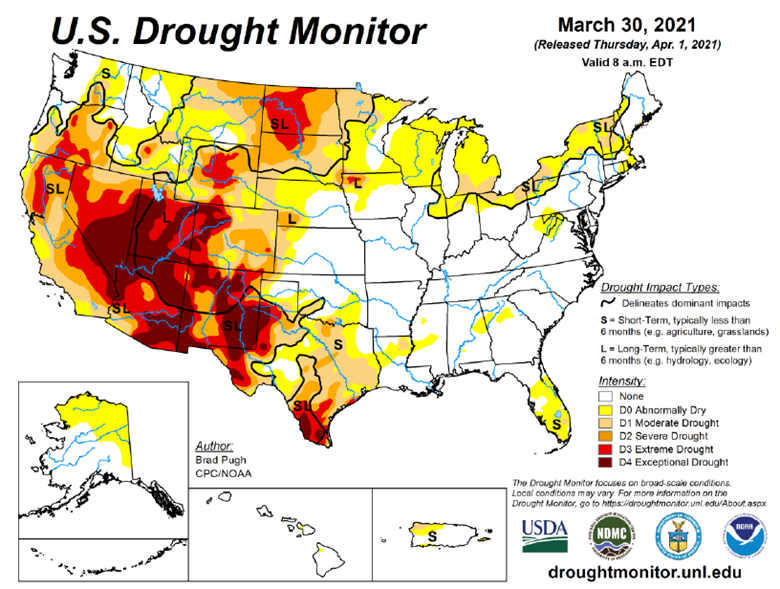

As you can see in the chart below cotton has had a rough 2 weeks. With demand expected to decrease with the possibility of a recession coming, this reaction is clear and puts fiber prices at the mercy of the economy’s future. The other side to this is that US production will likely be lower than expected with so much dryland in west Texas and other serious drought areas (see map below) expected to not produce a crop. Growers planted 12.5 million acres in 2022, up 11% from last year.

The equity markets were relatively flat on the week after a few up and down days. The market headlines keep being “market rallies as fear of recession lessens” or “market falls as recession fears remain” so the market is still looking for guidance as it continues lower. July’s news will be similar to June with inflation and the Fed being the main drivers.

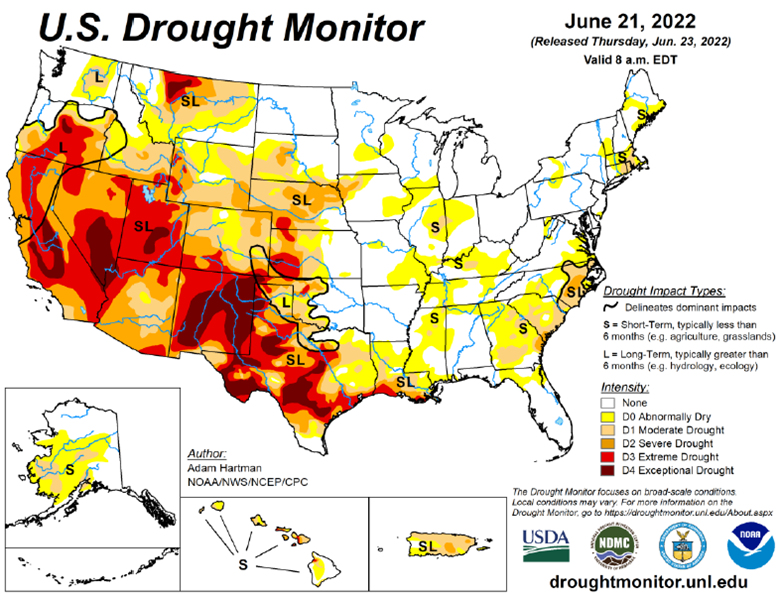

The drought monitor below shows where we stand week to week.

Podcast

There is an agriculture tug of war happening across the nation, impacting America’s farmland. Fertilizer prices are continuously fluctuating, and it has us taking a page the “The Clash” should we stay, or should we go?! And we aren’t the only ones. Many farmers are asking their agronomist and chemical salespeople, “what will fertilizer cost me the rest of the season, and what are my options if I don’t want to go all-in on my typical fertilizer treatment plan?”

In this episode of the Hedged Edge, we are joined by a special guest who needs no introduction in his local circle, Dick Stiltz. Dick is a 50-year veteran of the fertilizer and chemical industry and is the current Agronomy Marketing Manager of Procurement fertilizer and crop protection at Prairieland FS, Inc in Jacksonville, IL. He is at the pulse of the current struggle and here to discuss the topic at hand.

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Corn continues to move higher as planting has gotten off to a slow start in the US and Brazil’s safrinha crop is facing drought conditions, shrinking their crop. The wet and cool forecasts remain into May for the north and eastern corn belt which will make it unlikely to see much planting progress in those areas. The rain will be welcome in the western corn belt that has been dry and making slow progress in planting, but the rain will be welcome for the soil even if it slows planting for a day or two. The ongoing conflict in Ukraine continues to decimate their infrastructure as Russia destroys ports and has seized stored corn to sell as their own. China was a buyer of corn this week and will hopefully continue to show up on exports as demand from other buyers has slowed. Limits have been increased at the CBOT for some commodities and corn will now have a 50 cent limit starting May 1 from the current 35 cent limit.

Soybeans had a small dip this week after its nice run higher from the previous dip at the end of March. Soyoil prices continue their move higher pulling beans with it while meal struggles. Indonesia placed a palm oil ban on both refined and unrefined product. The slow start to planting will ultimately roll into affecting soybeans like corn but we aren’t at panic mode yet. The start to the year has been less than ideal when the world stocks need a great year. Beans daily trading limit will move up to $1.15 effective May 1st.

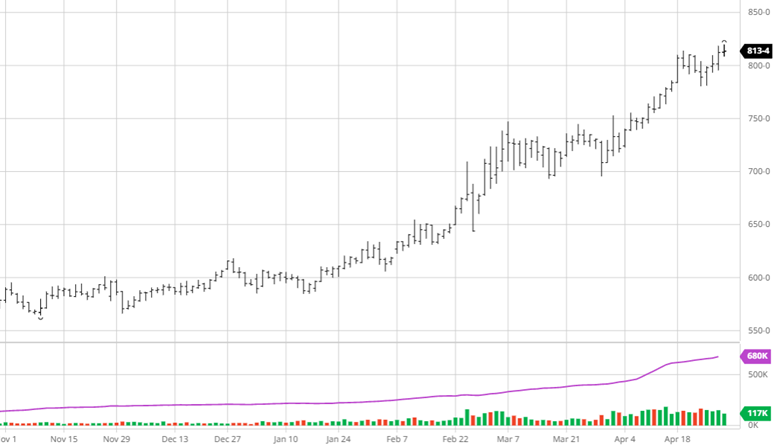

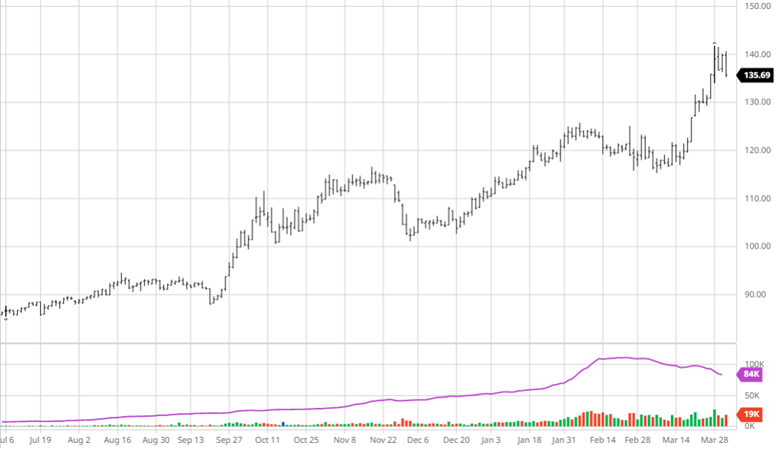

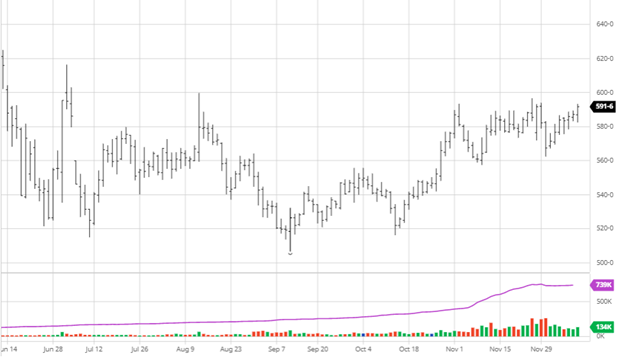

July cotton traded limit up (7 cents) on Thursday to set a new contract high at $1.4768. Export data from last week was better than the last few weeks. Cotton’s problem appears to be a lack of world supply mixed with (so far) not ideal growing conditions in Texas. Forecasts for rain in Texas are very welcome but will need to be widespread and a large amount to help the drought. (See drought map below)

Dow Jones

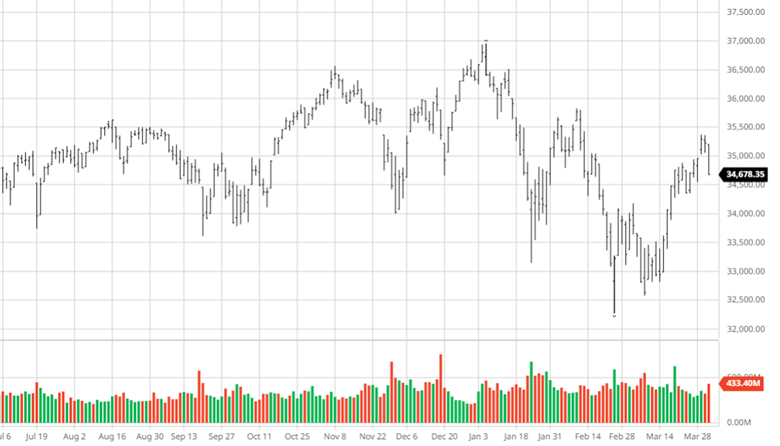

The Dow was down this week as volatility continues to be in the markets as earnings continue to come across with some large companies getting crushed and others posting solid numbers. Tech companies have had a good week after getting run over the past couple months. This may not be the bottom for tech but it is nice to see some good numbers and some support.

The drought monitor below shows where we stand week to week.

Podcast

RCM Ag Services put a unique spin on National Agriculture Day by going international. That’s right, we jumped right into international waters with Maria Dorsett from USDA’s Foreign Agriculture Services for an interesting discussion about linking U.S. agriculture to the rest of the world.

Each year, March 22 represents a special day to increase public awareness of the U.S.’s agricultural role in society, so why not take it one step further by bringing in a global component? As the world population soars, there’s an even greater demand for producing food, fiber, and renewable resources. That’s why we’re taking a deeper dive into the USDA’s trade finance programs, like the GSM-102, which supports sales of U.S. agricultural products in overseas markets and supports export growth in areas of the world that are seeing some of the fastest population growth.

So, jump aboard (no passport needed), as Maria discusses how U.S. companies use GSM-102, what the program features, and the benefits that it offers!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

A bullish USDA Prospective Plantings report for corn saw both old and new crop corn getting a boost on Thursday. The USDA sees corn-planted acres for all purposes in 2022 at 89.5 million acres, down 3.87 million from last year and well below the average trade estimate of 92 million. Several factors might have played into this number but going from 92 million acres at the USDA Ag Forum to this number a month later is very interesting. Input prices and supply chain woes likely played a major role in the USDA predicting more bean acres than corn as the cost per acre to raise corn will be very high this year with the risk of not receiving all inputs in time. On top of the fallout of the war in Ukraine, this lower number should see tightening on the world balance sheets even with a record yield this year.

Soybeans had a bearish report as the USDA came out with 91 million planted acres in the US for 2022. This would be a record for planted acres and 4 percent higher than last year, with planted acreage being up or unchanged in 24 of the 29 estimating states. Fewer inputs are needed per acre to grow beans than corn played a major role in the shift in acres year to year. How the market trades in the next few days will be interesting to watch as 91 million is a lot of acres, but the world needs it, so will it actually be enough?

Wheat remains vulnerable to Ukraine and Russia news while also figuring out its value in the world market. Wheat acres came in at 47.351 million, lower than the pre-report estimates — 2022 winter wheat planted area at 34.2 million acres and (23.7 million HRW, 6.89 million SRW, 3.62 WW) 11.2 million acres of spring wheat. China’s poor crop and the issues with the U.S. crop seem to be priced into the market possible, but for the time being, Russia’s war in Ukraine will be the market moving news.

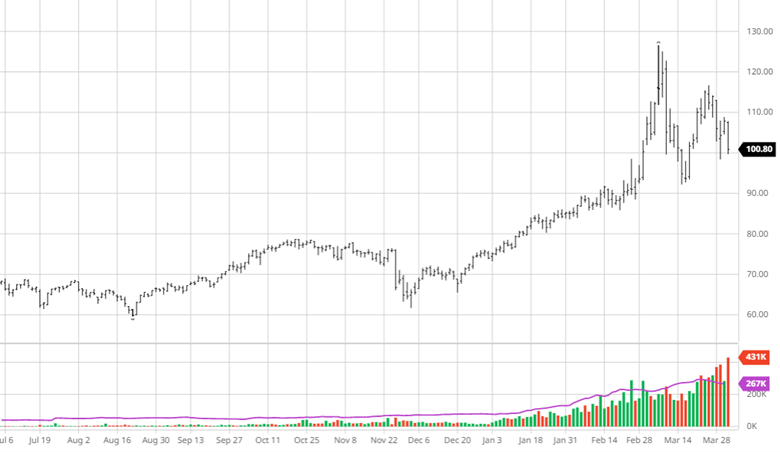

Cotton made another jump higher this week before falling following the report. Cotton acres came in at 12.2 million acres, up 9% from last year. Many growing areas have been dry this winter and could use a spring rain to help improve planting conditions. World demand is still present, so the US will have buyers if they can produce a crop. The old and new crops have been over $1 for several weeks now, making it easier to plant than when it was in the 50 cent range a couple of years ago.

Crude continued its move lower this week with a couple of large intraday ranges. The Biden administration announced that it would release 1 million barrels of oil a day from the Strategic Petroleum Reserves to help fight higher gas prices. The big dip came from rumors of progress in peace talks in Ukraine that seemed incorrect as the conflict continued. The Biden administration also wants to make companies with leases on federal land “use em or lose em” but that would take months to years to go from 0 production levels. When Democrats want to shift to EVs and other “green” energy, it is hard to see why companies invest capital when that party wants to get rid of their dependency as fast as possible.

The equity markets fell slightly during the week due to Thursday’s fall into the close of trading. The 2/10 yr treasury yield inversion has been the main talking point this week as it could be a signal of a recession. While it does not always mean there will be a recession, we have not had a recession without that happening, even though it is usually over a year later. Q1 ended this week after a few months of losses, volatility, confusion, and inflation, and it is hard to see it calming down anytime soon.

The drought monitor below shows where we stand heading into April compares to last year.

Podcast

RCM Ag Services put a unique spin on National Agriculture Day by going international. That’s right, we jumped right into international waters with Maria Dorsett from USDA’s Foreign Agriculture Services for an interesting discussion about linking U.S. agriculture to the rest of the world.

Each year, March 22 represents a special day to increase public awareness of the U.S.’s agricultural role in society, so why not take it one step further by bringing in a global component? As the world population soars, there’s an even greater demand for producing food, fiber, and renewable resources. That’s why we’re taking a deeper dive into the USDA’s trade finance programs, like the GSM-102, which supports sales of U.S. agricultural products in overseas markets and supports export growth in areas of the world that are seeing some of the fastest population growth.

So, jump aboard (no passport needed), as Maria discusses how U.S. companies use GSM-102, what the program features, and the benefits that it offers!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Corn has continued to trade in the same range since early March as the markets wait for next week’s acreage report from the USDA. This is a major market-moving report historically, so expect volatility either way. IHS Markit’s current estimates were for 91.42 million acres of corn, while Pro Farmer came out with 91.9 million. While these numbers seem realistic and may ultimately be right, I would be surprised if the USDA came out with anything lower than 92 million. The big question is, will higher inputs cause fewer acres even though there are higher prices, or will it be flipped? All eyes will be glued to the markets for the report, with the only other market-moving news until then will be developments in Ukraine.

Soybeans continued their steady climb while corn and wheat calmed down. Next week’s report will be important for beans as well. Some analysts expect more bean acres this year as some farmers switch corn to beans in favor of lower input costs. IHS Markit estimates 88.58 million acres while Pro Farmer estimates 87.8 million. This is a good size difference showing uncertainty around the bean number with prices this high. South America’s weather has become less newsworthy so expect the market to position itself into the report unless there is any unforeseen news.

Wheat’s craziness cooled off this week as many people have completely gotten out of the market until there is less uncertainty. With no significant news this week on the path of the fighting in Ukraine, the markets stayed in a smaller trading range compared to the past few weeks. The world wheat outlook is not very bright with the problems in Ukraine, China’s awful crop, and the struggles with the US crop, expect balance sheets to get tighter. World sanctions on Russia will play out in the wheat market if everyone stops buying Russian wheat; China will likely shift their buying to them and change up the trade dynamic of countries. The major news moving forward is still Ukraine.

Cotton has had a good few weeks with the May contract topping $1.30. Many in the industry have expected this move higher, but its reluctance to do it has been frustrating. With a tight market and world demand, this growing season will be important. Analysts estimate that between 11.7 and 13 million acres will be planted, which is much higher than last year’s 11.2 million acres.

Dow Jones

The equity markets made gains again this week as markets appear to be holding their breath, hoping that we have bottomed while also figuring out what to expect ahead. With several rate hikes expected this year, the markets will price those in accordingly and should not be shocked when it happens. Inflation concerns remain as oil prices bounced back over $100 and may stay there for the foreseeable future with no resolution to the war in Ukraine in sight.

RCM Ag Services put a unique spin on National Agriculture Day by going international. That’s right, we jumped right into international waters with Maria Dorsett from USDA’s Foreign Agriculture Services for an interesting discussion about linking U.S. agriculture to the rest of the world.

Each year, March 22 represents a special day to increase public awareness of the U.S.’s agricultural role in society, so why not take it one step further by bringing in a global component? As the world population soars, there’s an even greater demand for producing food, fiber, and renewable resources. That’s why we’re taking a deeper dive into the USDA’s trade finance programs, like the GSM-102, which supports sales of U.S. agricultural products in overseas markets and supports export growth in areas of the world that are seeing some of the fastest population growth.

So, jump aboard (no passport needed), as Maria discusses how U.S. companies use GSM-102, what the program features, and the benefits that it offers!

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

As of 2022, there are 7.9 billion people in the world, which is anticipated to hit 10 billion by 2050

Did you know that by 2050, the world is expected to feed almost 2 billion more people than we do today? As the global population continuously rises, a significant amount of food will need to be produced over the next 30 years.

But before you get to overwhelmed with that thought, it’s imperative to know that the need for more production creates opportunities. In fact, in 2020 alone, 19.7 million jobs were related to the agriculture and food sectors. We cover these areas in this What It Takes To Feed the World infographic. So, let’s take a closer look into how each of these categories work together to help pave the way to feeding 25% more of the population over the next couple of years. Here’s everything you’ll need to know:

Download the Infographic

FINANCIAL INSTITUTIONS / INSURANCE

Due to inflation (we cover farm inflation here) and superior advancements in farming technology (seed, equipment, etc.), the cost of doing business is extraordinary.

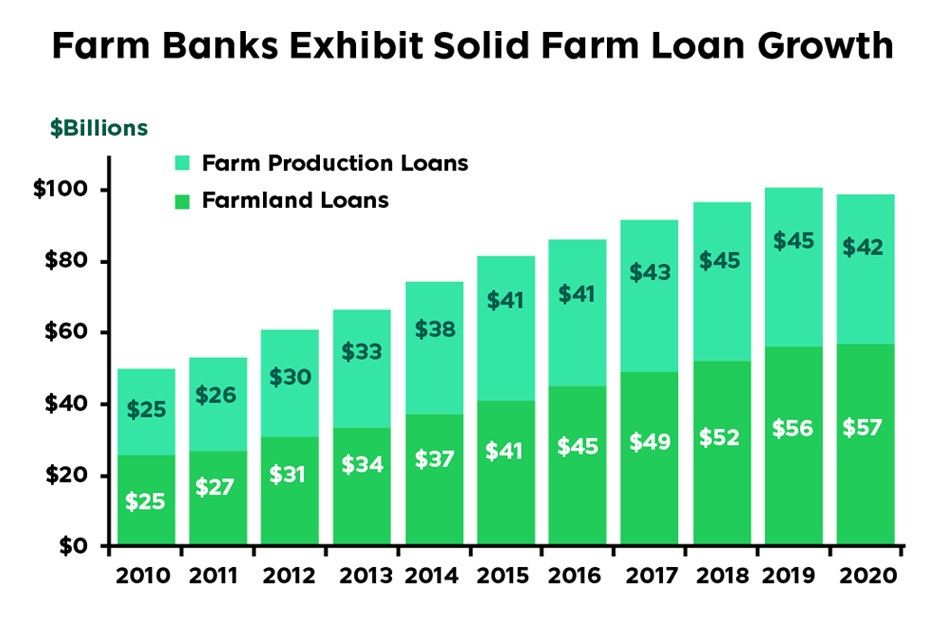

As a result, banks and other financial institutions have become the pillar of the agriculture community. From financing farmers, purchase of seeds and chemicals to providing insurance to protect the farmers on through to commercial lending and trade finance programs; without banks, agriculture, as we know it today, does not exist. As a standalone example, consider that in the U.S. alone, during 2020, farm bank’ lending was $98.6 billion despite the global economic slowdown. As the demand to produce continues to grow, there is minimal question that the need for capital will grow along with it.

Source: Federal Deposit Insurance Corporation & American Bankers Association Analysis

SEED / CHEMICAL:

Before the farmers can get to work, they need seeds and, subsequently, fertilizers (watch our fertilizer forecast here) to reach the full potential of every acre of land. From the genetics to the production to the distribution companies, one could argue that continued innovation of this industry is vital to the future of agriculture.

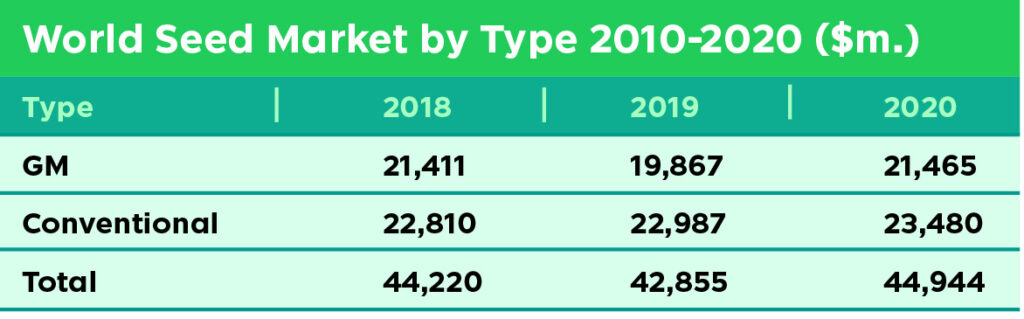

In 2020, the commercial seed market alone reached an estimated $44.9 billion in annual revenue. With the global pressure on to produce, the world can no longer afford to have underperforming years of production, placing even more pressure on this sub-sector of agriculture to continue to develop treatments on both the organic and GMO sides (watch The Future of Feeding the World Podcast here).

Source: IHS Markit – @2021 IHS Markit

EQUIPMENT

With the growing demand for food-producing land due to the world’s growing population, advances in technology have seamlessly made the farming process more efficient, profitable, and undoubtfully safer. Modern farms and agriculture equipment have significantly evolved by incorporating sophisticated technologies like sensors and GPS to driverless equipment with new autonomous machinery.

These enhancements to heavy equipment are essential to farmers, allowing them to no longer apply certain things uniformly, like fertilizing or watering the field. But instead, farmers can use minimal effort to target specific areas of their fields. Let’s look at some of these added benefits due to technology:

Farmers have higher crop productivity.

There is a reduction in the overuse of water, fertilizer, and pesticides.

The price of food production is at a lower rate due to less manual labor.

Improves the safety of farmworkers and machine operators due by incorporating the use of drones and various software. Check out this podcast with Dr. Steve Irwin on technical platforms here.

Groundwater and rivers are experiencing less runoff of chemicals.

Undoubtedly, innovation of this business sector will continue to evolve and play a major role in the necessary production increases ahead.

GRAIN PRODUCERS

One hundred fifty years ago, work was hard for grain producers, but the job was simple – till the land, plant the seed and let mother nature do her job. As time passed and our global population grew and the demand for our arable land has grown exponentially; all of which, leads to the grain producers of today having the most important job in the world.

The work of the few is to feed the many. Since the post-WWII era, the number of farms has steadily been reducing, placing even greater pressure on those in production areas to continue managing their operations, focusing on profit margins, and working the inherently volatile world of commodity prices.

Imagine a 5,000-acre farm producing trendline yield corn of 180 bushels per acre. Quick raw math based on today’s price per bushel of $6.00 puts gross revenue at 5.4 Million dollars. Noting the rapidly rising costs of inputs (seed and chemical), labor and energy prices, a return to August 2020 prices of $3 would be a massive hit and likely take down such an operation.

All of this is to say that today’s job requires greater collaboration with others in the business than ever before (see section below on intermediaries and risk management).

INTERMEDIARIES/RISK MANAGEMENT

Commodity markets are highly unique in that both end-users and physical producers of a product can proactively buy and sell their input and or production in an open market before being produced via a forward contract or hedge.

To hedge is to manage risk and, in most cases, lock in or protect the profits margins. As discussed above, grain production is a highly volatile business, just like the purchase side (see end-users and commercials below).

Through intermediaries and risk management experts, farmers and end-users gain timely market information, access to markets, and ultimately execute the majority of their forward pricing. Whether through the use of futures, options, swaps, or even physical contracts developing and coordinating a risk management plan is essential to the long-term health of our global commodity infrastructure.

The CME Group is the world-leading commodity exchange, and their global branding says it best – “CME Group, where the world comes to manage risk.”

RCM Ag Services also falls into this category. We provide full-service risk management and advisory solutions to our local area producers and commercial agriculture operations around the globe.

TRANSPORTATION/LOGISTICS

COVID introduced unexpected stresses on global food systems, creating many immediate and rapid challenges to secure food availability. If a worldwide pandemic taught us anything, we know that supply chain management and transportation play a vital role within the agriculture industry. Agriculture logistics ensure that items like food, machinery, and livestock from all over the world are transported with a continuous, optimal flow from the manufacturers and suppliers to the producers and ultimately delivered to consumers.

Some of the most imperative agriculture supply chain and logistics management activities include production, acquisition, storage, handling, transportation, and distribution. Effective logistics is critical for guaranteeing customer satisfaction and meeting demands on time with high-quality products. In addition, logistics should also meet specific standards and operational objectives for efficiency in agriculture policies like:

Protection of the environment

Sustainable distribution practices

Food safety and security

Animal welfare (for transporting livestock)

With the growing population largely expected in developing countries, most of which have poor infrastructure, we can expect the need for massive investments into transportation and logistics operations in the years ahead (this is NOT a stock tip!).

COMMERCIAL AND END USERS

The penultimate step of the process is grain reaching a commercial elevator before going on to the end-user to be converted to a final product. Some producers deliver straight to the end-user in areas where that is an option.

Traditionally, commercial elevators accept farmers’ grain and then ship it to the end-user, either by rail, barge, or other means.

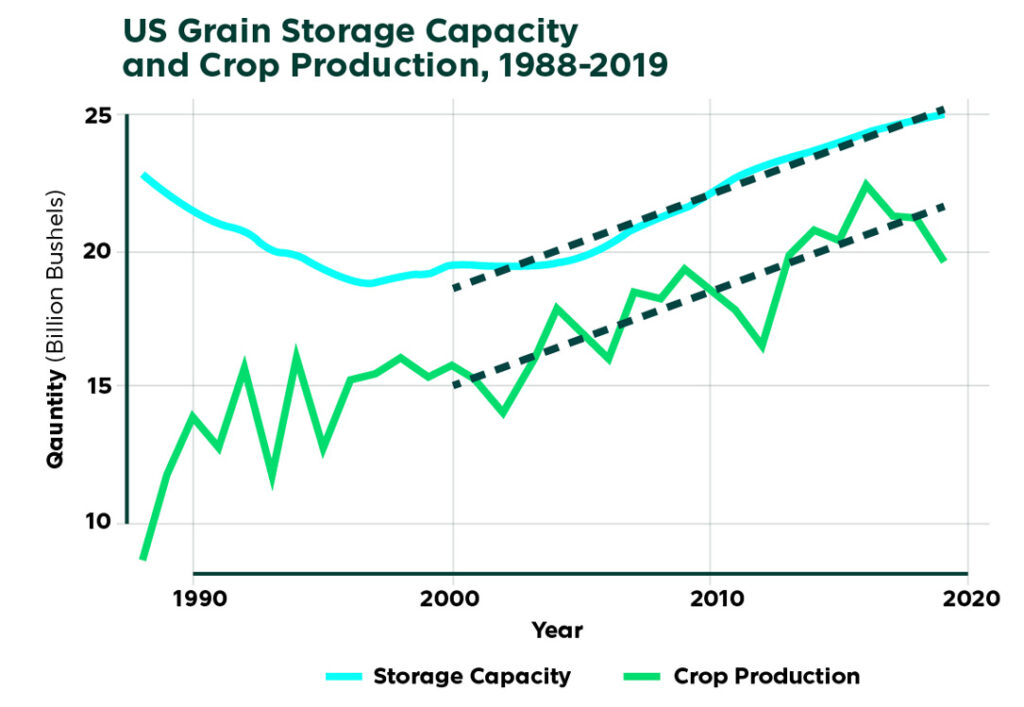

With the continued upward trends of production, it is no surprise, that grain storage capacity has consistently grown. In fact, it is on pace with increases in crop production over the last 20 years and by all accounts is likely to continue to grow.

Source: Farmdocdaily

Along with the enormous capacity, commercials and end users also carry a tremendous amount of of price / volatility risk requiring a proactive and disciplined risk management approach to maximize the margins of their operation and keep the system moving forward.

In 2018, $139.6 billion worth of American agricultural products were exported worldwide, with elevators playing a significant role in that process. The commercials and end-users are essential for getting the product from the farm into your home on the table.

FEEDING THE WORLD IN THE FUTURE

Bringing awareness to how the agriculture industry is vital to feeding the rapidly growing world is pivotal as we continue to face unprecedented challenges in global food security. However, there is a silver lining. We already know what must be done; it is figuring out how to do it that could be problematic. The world must unite and understand that each of these areas highlighted in the infographic is very complex, employs millions of people worldwide, and is vital to the growth of the agriculture industry as well as producing the necessary food for the future.

Download the Infographic

CONTACT AN AG SPECIALIST TODAY

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact us today to speak with an ag specialist at 888-875-2110!

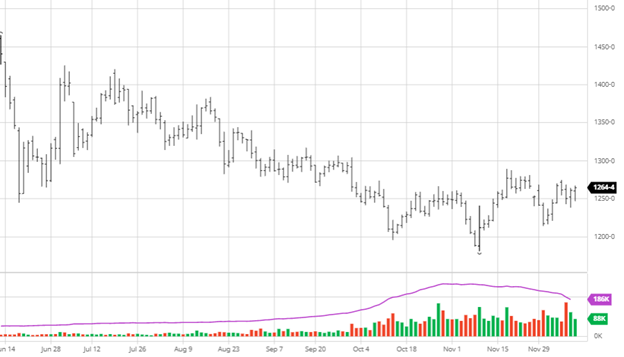

Corn continued its rally this week as grain bulls and inflation continue to drive it higher. The yield losses in South America continue to have news around it as the reality of significant losses begins to set in. Too much rain and heat or not enough rain and heat have been driving the issues, with very few areas having excellent growing conditions. With the Chinese New Year coming up, China will disappear from the export reports for a little bit, but once they come back, the market will have a better idea of where Brazil and Argentina sit. If the rumored losses come to fruition, we could see China increase its purchases. Corn has continued its rise while wheat struggles to make up its mind with confusion around the Russia and Ukraine situation. Any escalation there will result in more bullish factors in the market. Despite some volatility, energy prices continued their rise, with crude oil hitting a new high this week. Ethanol plants will continue to produce even with higher corn prices as long as their margins remain strong despite resulting in less fuel consumption. Many energy companies think we could see $100+ Crude in the next few months.

Soybeans continued to move this week on similar news as corn with South America’s issues and continued world veg oil strength. With strong veg oil prices pulling beans along with it as long as that lasts, we can expect some support under beans with any lower moves. Like corn, if private estimates of losses to the South American crop become a reality, we should continue this run higher. If China comes back from Chinese New Year and starts picking up bean purchases, mixed with world veg oil prices could see this rally continue. Acreage estimates for 2022 have been coming out, with Informa pegging the US bean crop at 87.8 million acres. This is slightly higher than the 87.2 million acres from 2021, but we have a long way to go before we get to that point.

Equities had quite the week with large intraday trading ranges as the market does not seem to make up its mind. This week, the Fed’s decision to leave interest rates as-is means we should expect a raise from the March meeting. The Fed also said they would adjust asset purchases moving forward. The tensions between Ukraine, Russia, and NATO remain a large question mark, but it appears Putin may not do anything until after the Olympics. This will be important to keep an eye on for equities and commodity prices.

The cotton market has held in this $1.20 range for the last ten trading days. World demand is there, and this bull market could have room to run if inflation sticks around with other supply chain bottlenecks. We could continue to see this strength last into the spring when planting starts until we get a better idea of what the U.S. cotton crop will look like this year. With rising consumer demand, the cost of production and transportation in the next few months could see volatility.

Podcast

Tune in as biotech guru Dr. Channa S. Prakash discusses everything from Alabama football, genetics as one of the most extensive agricultural advancements, the most significant risk factors to feeding the world over the next 30-50 years, plus everything in between.

Why producing crop plants with a much gentler footprint on the natural resources will help feed the growing population. How 75% of the world’s patents in agriculture gene editing are coming from China. Understanding that trying to impose restrictions on our ability to grow food can be a considerable risk to agriculture. Listen to hear about these topics and more!

This week, corn had a good rally following a couple of big down days last week. The December USDA report was released on Thursday with minimal changes and differences between the numbers and pre-report estimates. World stocks were slightly higher than pre-report estimates at 305.45 million metric tons (304.47 MMT estimate) and marginally higher US stocks. The USDA did not make any adjustments to the South American crop estimates as they remain patient; we should expect next month to see a change. Continue to keep an eye on SA weather as any continued problems could play out in the market heading into the holidays.

Soybeans, like corn, saw a modest bounce following a couple of bad days last week. The expectation of a bearish report proved incorrect as the USDA left the stock numbers unchanged. The exports seem to have been slowing down and remain well short of the Phase 1 deal with China, so we could expect to see the export numbers lowered and ending stocks raised if there is no strong buying into the end of the year. All in all, the report lacked any market-moving fireworks.

The Dow had a strong week bouncing back from its dip as there were plenty of buyers buying the dip. As fear of the Omicron variant relaxes and positive news on the vaccine fighting this strain, this cycle of the variant worry may have already hit and bounced back in the market. Many analystsare calling for a rally into the end of the year with many firms releasing their top picks for 2022. The CPI numbers will be released at the end of the week and will play out in the market on Friday.

Wheat

Wheat prices have been falling the last week and continued falling after the report. Australia and Canada had larger production than expected. Another important development specific to wheat will be the tensions between Ukraine and Russia, as any escalation would cause problems for wheat exports from Ukraine.

Podcast

For the past year, commodity prices have perpetually soared and continue to trend higher. We’re diving into the fertilizer forecast with a unique guest, Billy Dale Strader, a branch manager for Helena Agri-Enterprises in Russellville, KY., who is truly at the epicenter of the rising fertilizer prices.

Billy Dale planted his agriculture roots on his family-owned farm and has managed regional seed and chemical sales at Helena for the past decade. In this week’s pod, we tackle the big question for farmers and ultimately end-users — is the impact of higher-priced inputs, like seeds, chemicals, and fertilizer, on the supply and demand for the major U.S. crops? Listen or watch to find out!

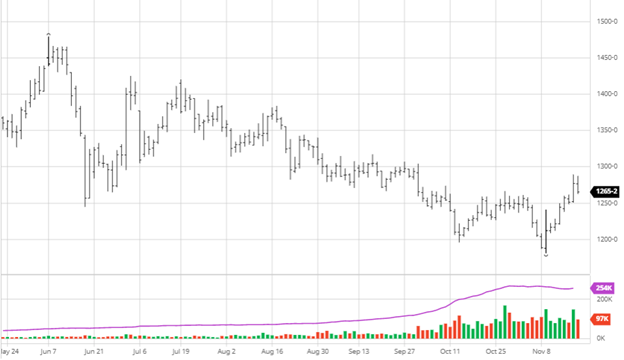

Corn has seen a good bounce since the Nov 9 USDA report and has traded relatively flat the past few days despite some intraday volatility. There was no specific market-moving news to fuel this rally but tidbits here and there to help fuel overall positive sentiment. IHS Markit updated their acreage for 2022 planted acres estimate with corn coming in at 90.8 million acres, 2.5 million lower than 2020. Ethanol production stays hot as the weekly grind rose to 312 mbu, up 7 from the previous week and well ahead of the USDA estimate for the year. With increased input costs going into 2022, the decrease in acreage makes sense, as balance sheets will be tighter. As harvest nears the end, eyes turn to South American growing conditions for the months ahead.

Soybeans, like corn, have seen a solid rally since the USDA report. Soybeans continued their rally on Thursday until the EPA announced they would release their renewable fuel mandates by the end of the week. As the Biden administration has not been much of an ally for the ag sector, the decline on the coming news makes sense. Soybeans had decent exports this week as buyers keep showing up in the market even as prices trek higher. Continued demand from exports will help support beans, and it will be interesting to see how many beans get stored and who took advantage of higher prices with forward pricing. We will see this play out in the cash & basis market come the spring, but we expect most farmers to store corn for now. IHS Markit estimated the 2022 bean acreage to be 87.9 million acres, 700,000 acres less than 2020.

The Dow struggled this week as earnings continue to come in, but market volatility seems to be expected with the holiday season coming up. The Fed can still raise rates this year, and the Biden administration has not yet announced their nominee to head the Fed (either keeping Powell or someone new).

Cotton

Cotton has had life in the $1.10+ range for a while now as demand overseas is high for U.S. cotton. Growers have seen mixed yields across the country but nothing too surprising to the market. Cotton demand does not seem to be slowing down anytime soon as the world still is coming out of the pandemic, and some countries still have major restrictions.

Podcast

For the past year, commodity prices have perpetually soared and continue to trend higher. We’re diving into the fertilizer forecast with a unique guest, Billy Dale Strader, a branch manager for Helena Agri-Enterprises in Russellville, KY., who is truly at the epicenter of the rising fertilizer prices.

Billy Dale planted his agriculture roots on his family-owned farm and has managed regional seed and chemical sales at Helena for the past decade. In this week’s pod, we tackle the big question for farmers and ultimately end-users — is the impact of higher-priced inputs, like seeds, chemicals, and fertilizer, on the supply and demand for the major U.S. crops? Listen or watch to find out!

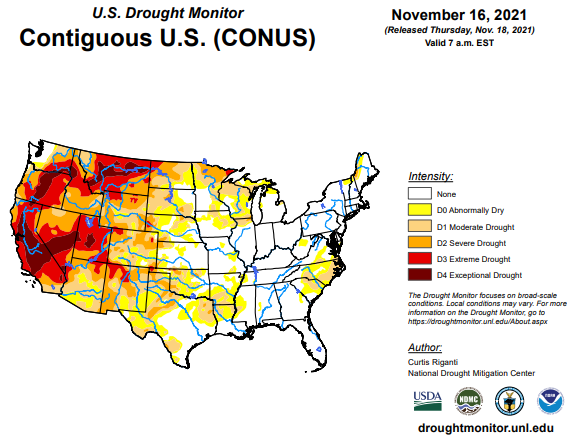

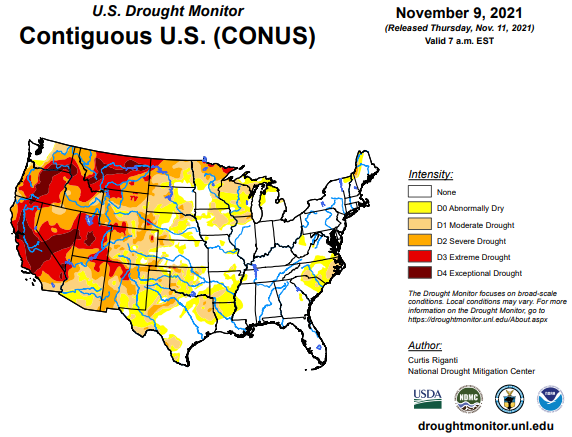

U.S. Drought Monitor

The maps below show the U.S. drought monitor and the comparison to it from a week ago. The outlined areas in black are areas that the drought will have a dominant impact.

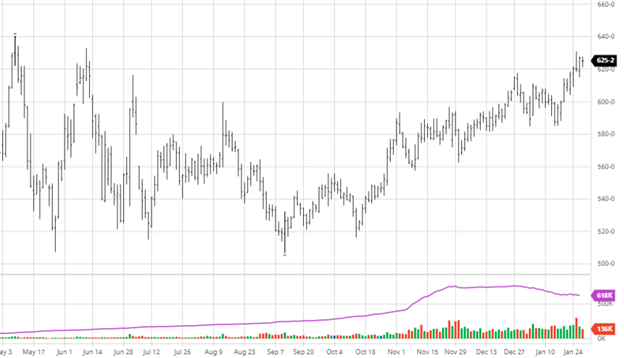

The Hedged Edge is back, and we’re jumping into the thick of the commodity markets with RCM’s own King of Cotton – Ron Lawson. Cotton prices have exploded since the COVID crash, rising more than 236% from the March 2020 lows. While prices have backed off from the October 8th high, cotton is one of the purest supply + demand-driven markets around the world and has caught fire along with the global inflation bug currently running rampant across many commodity markets.

Will it be hedge fund influence in cotton that costs consumers more this Holiday season or will the continued logistical issues tie up cotton at ports send consumers scrambling to eBay for their “snuggies”? For cotton producers, merchants, spinning mills, and banks financing the backbone of the cotton supply, risk management must remain at the top of mind for the remainder of this year and into 2022 (as the current cycle is likely to continue to last for at least the next 12-18 months.) We’ll dive into the thick of it in this episode and more — Hold on to your hats and enjoy!

RCM Ag Services is a registered DBA of Reliance Capital Markets II LLC. Trading futures, options on futures, and retail off-exchange foreign currency transactions are complex and involve substantial risk of loss and are not suitable for all investors. Loss-limiting strategies such as stop loss orders may not be effective because market conditions or technological issues may make it impossible to execute such orders. Likewise, strategies using combinations of options and/or futures positions such as “spread” or “straddle” trades may be just as risky as simple long and short positions. There are no guarantees of profit. You should carefully consider whether trading is suitable for you in light of your circumstances, knowledge and financial resources. You may lose all or more than your initial investment. You should not rely on any of the information herein as a substitute for the exercise of your own skill and judgment in making such a decision on the appropriateness of such investments. Opinions, market data and recommendations are subject to change without notice. Reliance Capital Markets II LLC shall not be held responsible for any actions taken based on this website or attached links. Parties acting on this electronic communication are responsible for their own actions. Past performance is not necessarily indicative of future results.