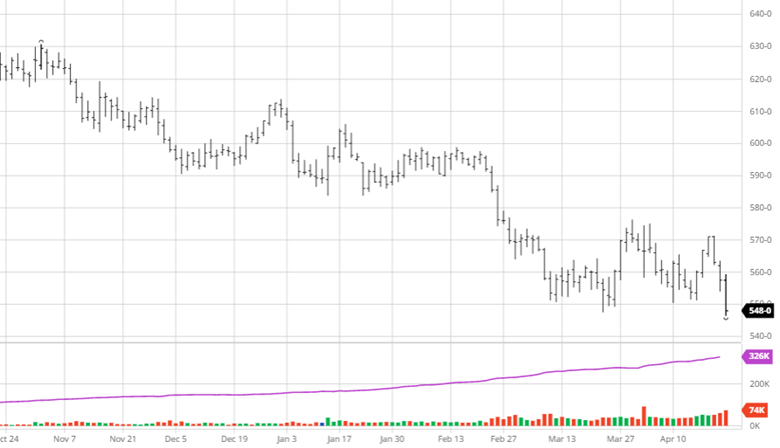

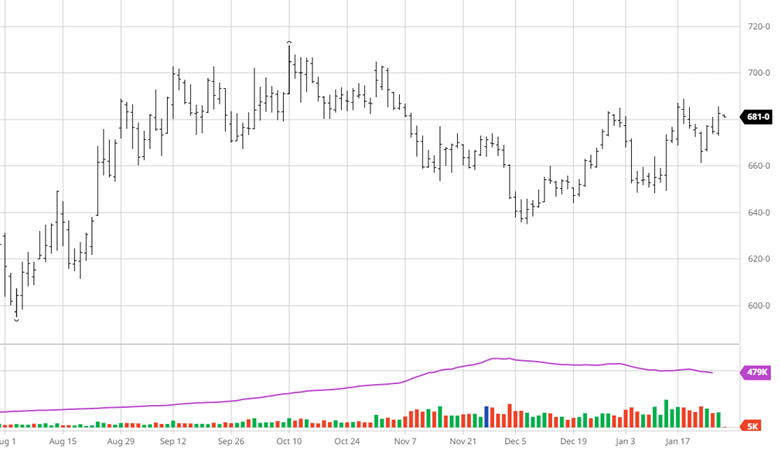

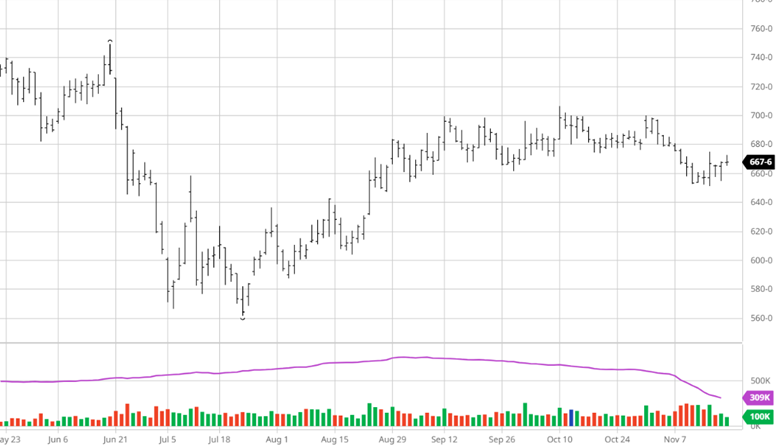

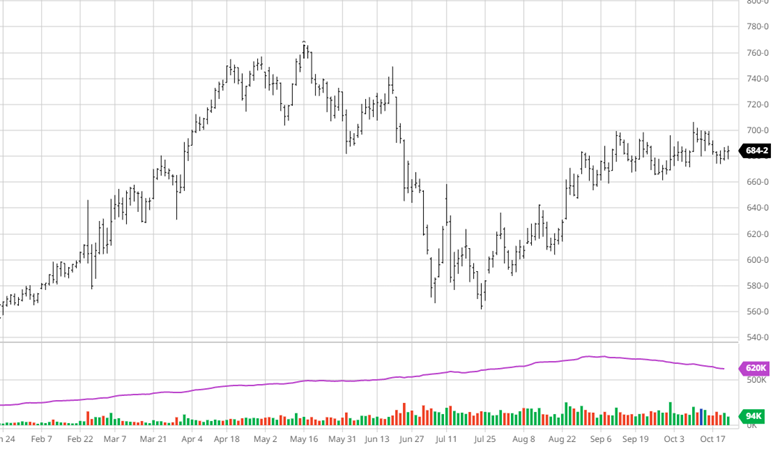

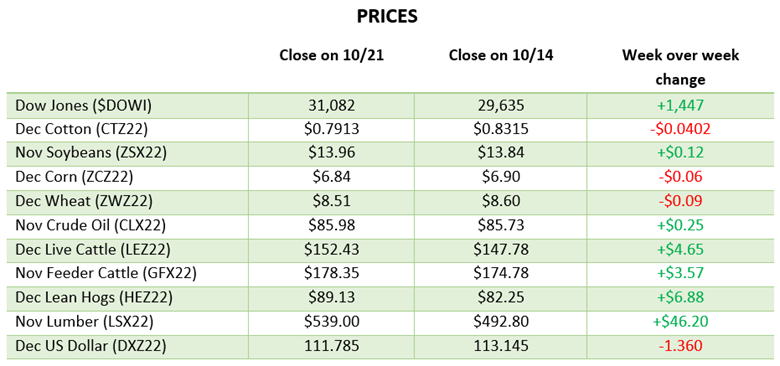

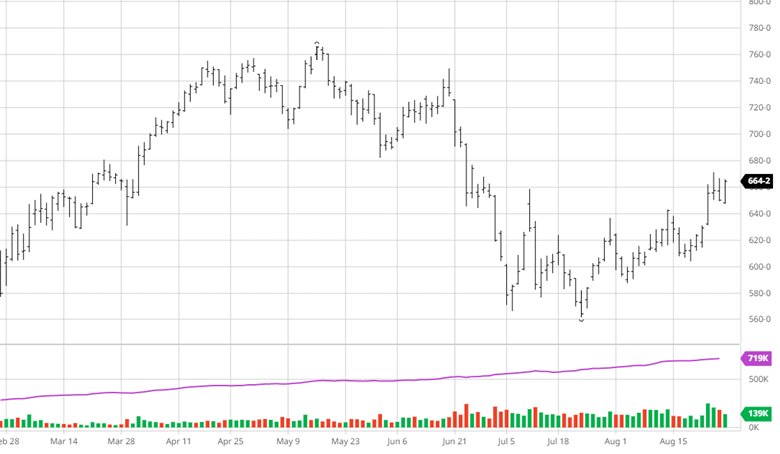

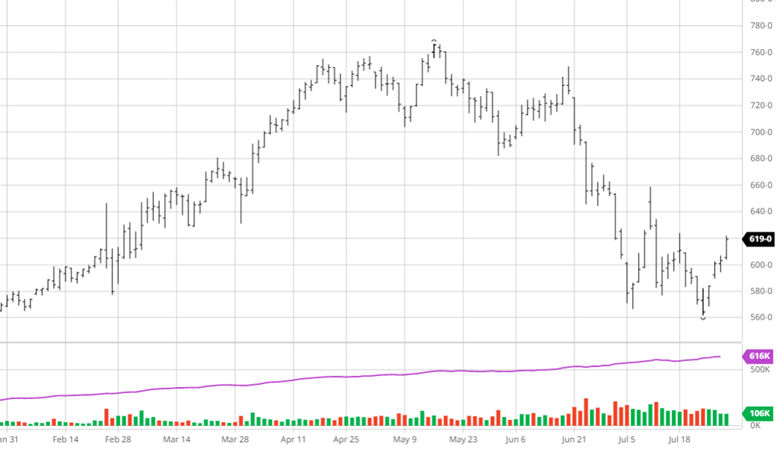

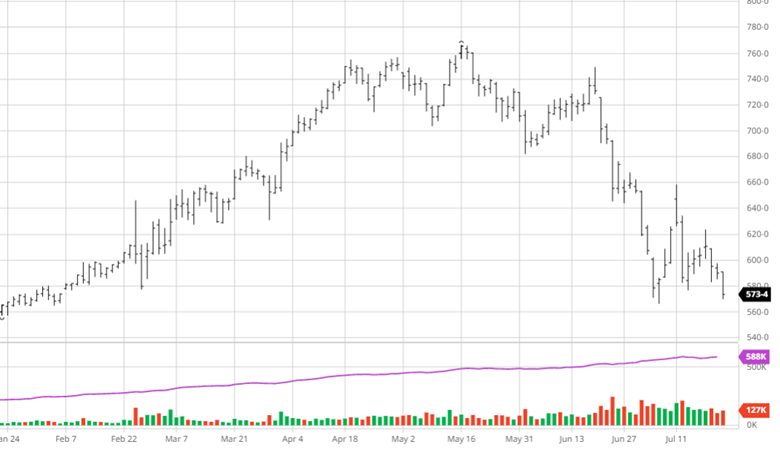

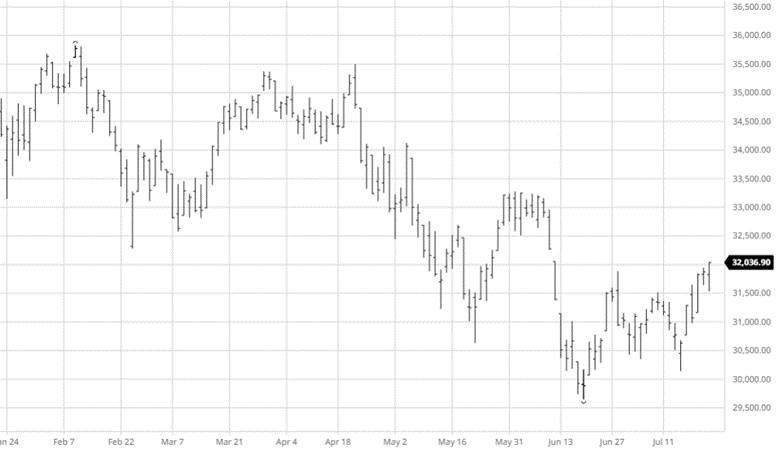

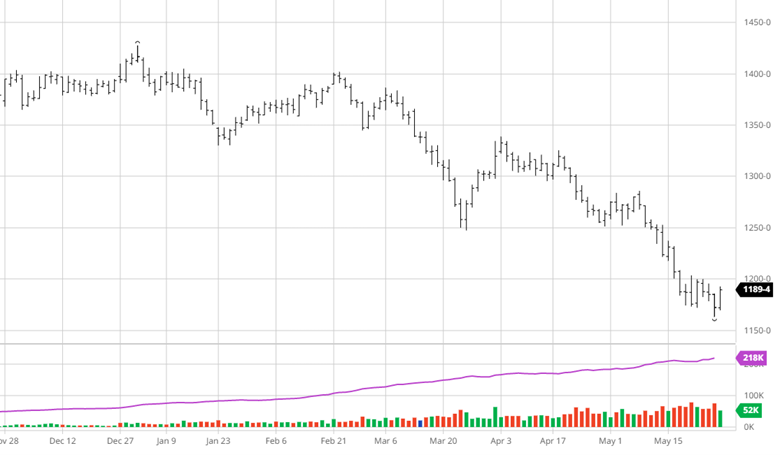

Corn had its best 2 week stretch in quite a while. As you can see from the chart below this has been the first meaningful rally, we have seen in 2023. As corn planting was 81% complete to start the week, ahead of the average pace, the trade has started to look at the weather outlook as we head into June. A dry pattern has begun forming in the coming weeks as it begins to warm up across the corn belt. While the heat in June is not overly worrisome it will be important to keep an eye on it as a warm dry June, followed by a hot dry July, could be plenty to do some serious damage to the US crop. We are a long way from this becoming a reality but a few weeks of dry heat to start June could help this rally keep some momentum or at least not give back the recent gains. Exports continue to be disappointing, and the extension of the Black Sea grain corridor isn’t bullish, but as usual the focus will be on final planted acres and weather in the coming weeks.

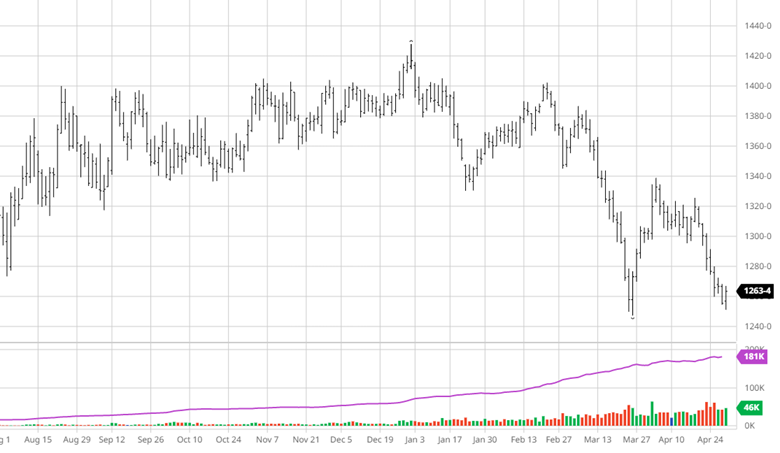

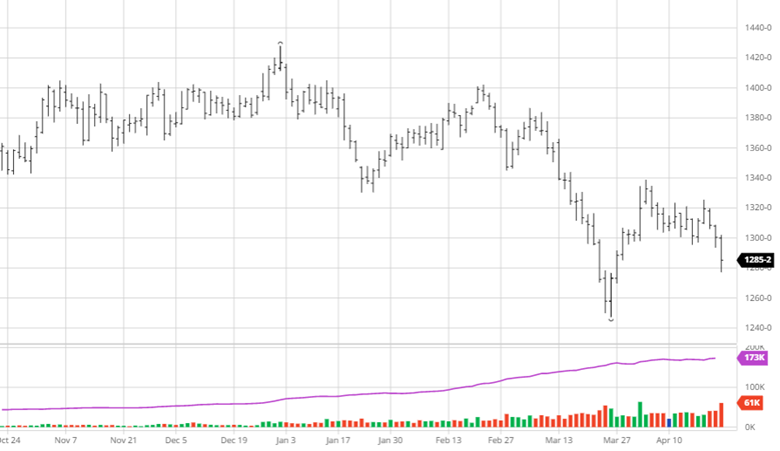

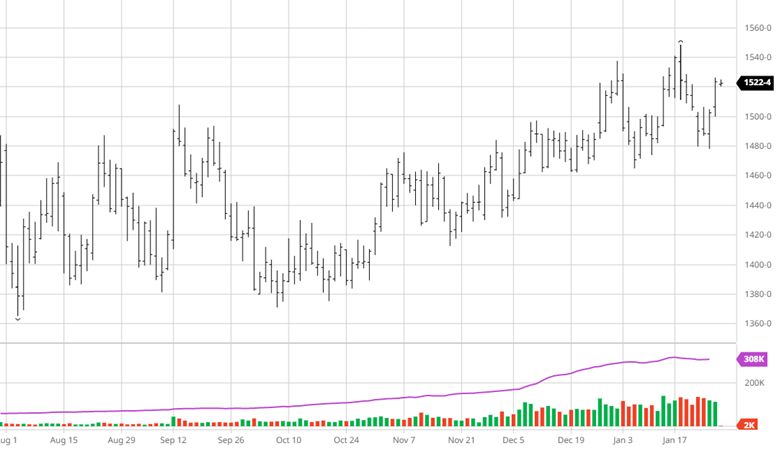

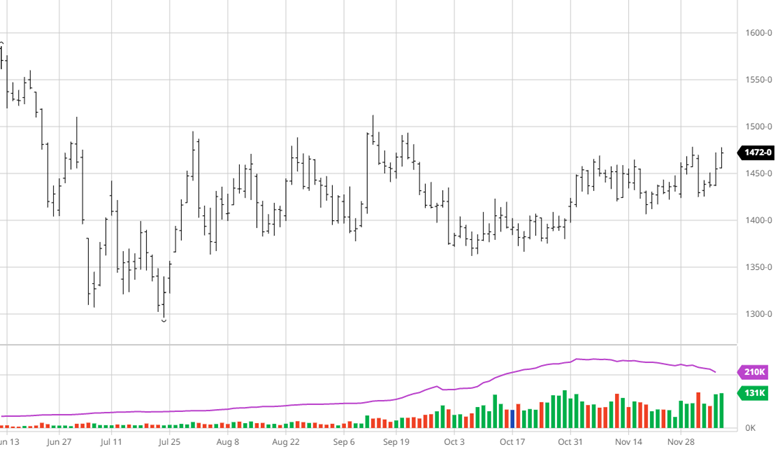

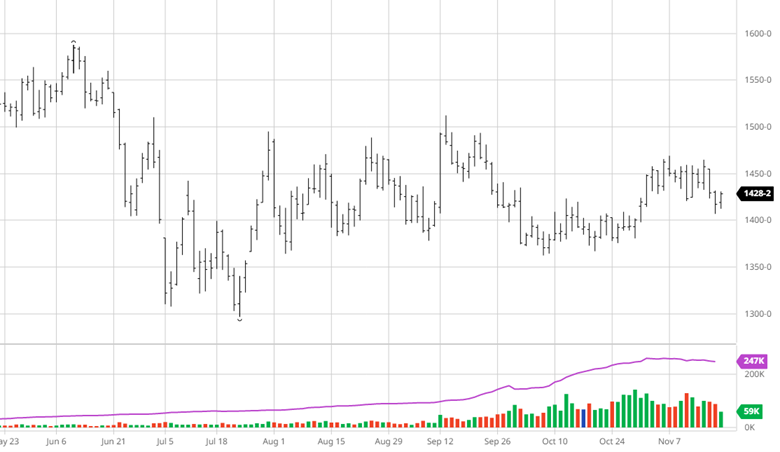

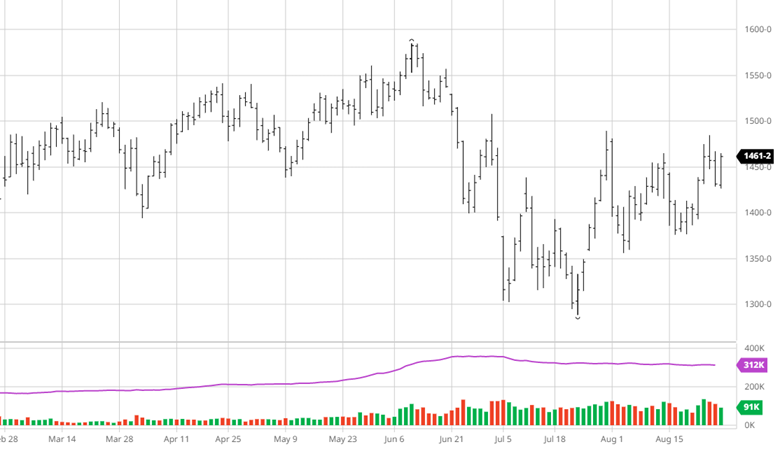

Soybeans can’t get any momentum as South American beans continue to be the preferred option in the world market. November futures made a new low this week before getting a modest bounce on Friday heading into the long weekend. As demand continues to struggle the USDA will likely continue to trim exports in the next report, which will add to ending stocks for 22/23. Beans were 66% planted, ahead of the average pace, as weather concerns won’t hit the soybean market just yet. Beans are lacking any bullish news as they wait for a spark but struggle to find where it will come from.

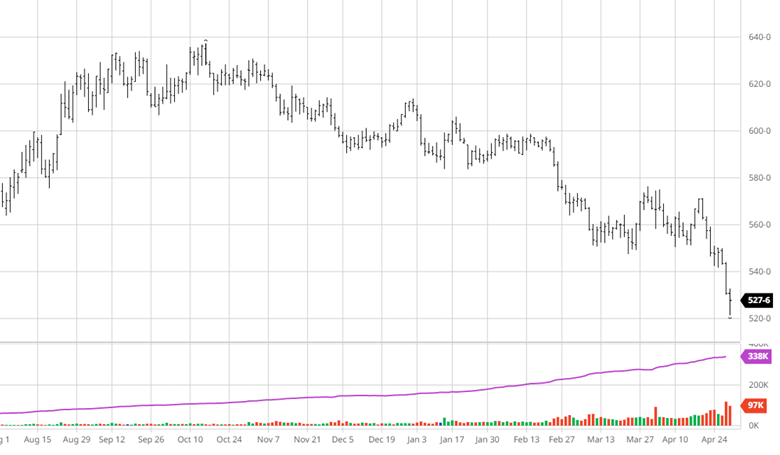

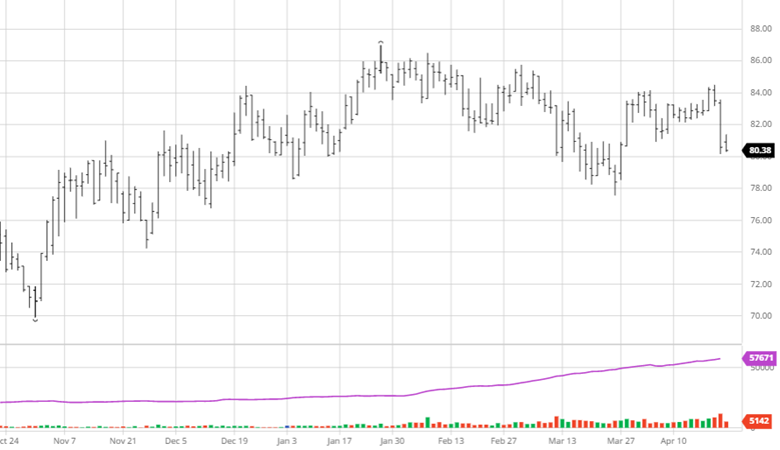

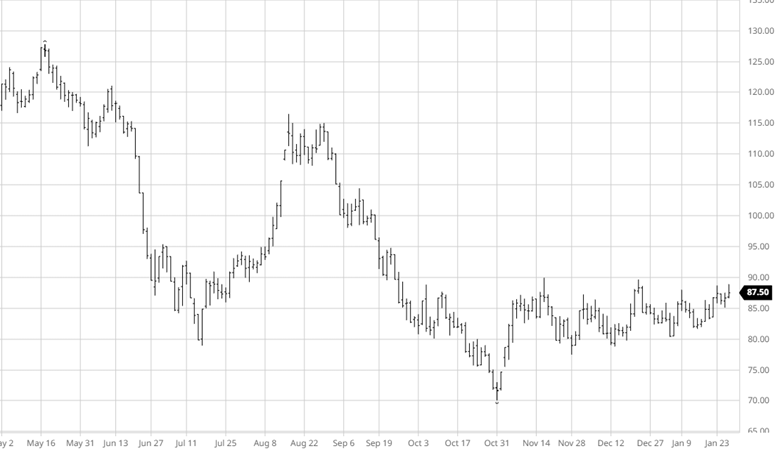

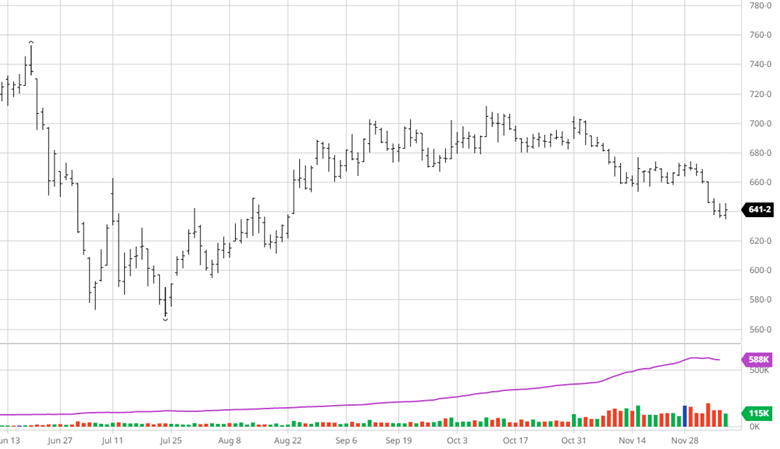

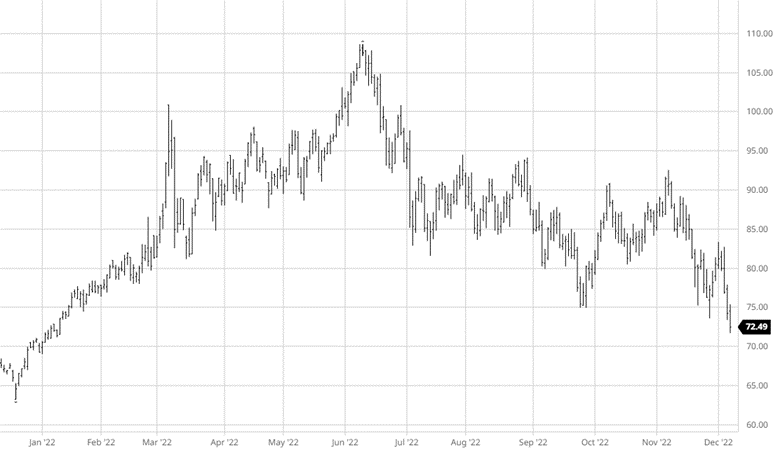

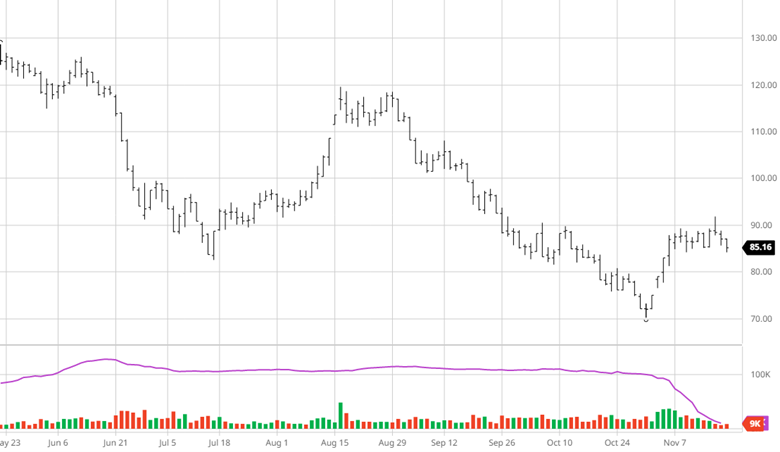

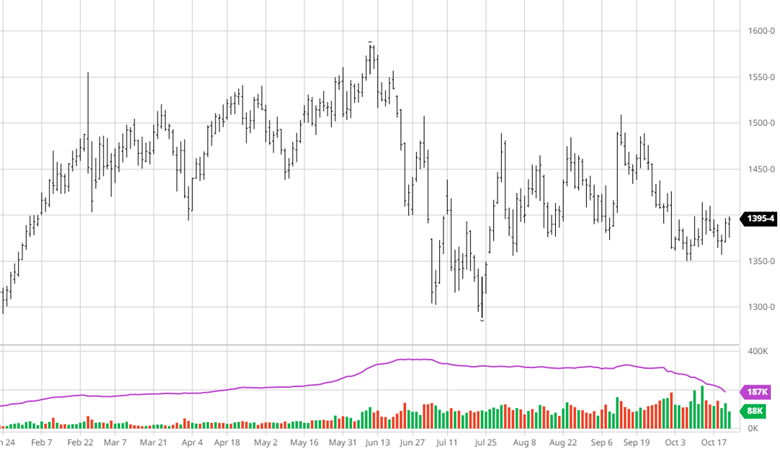

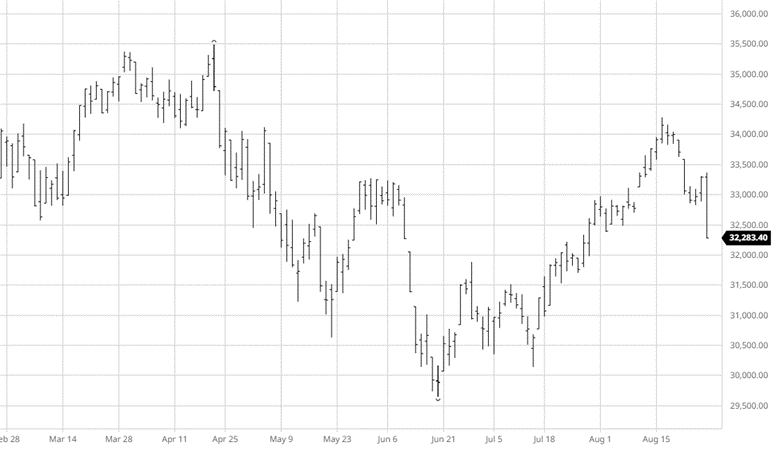

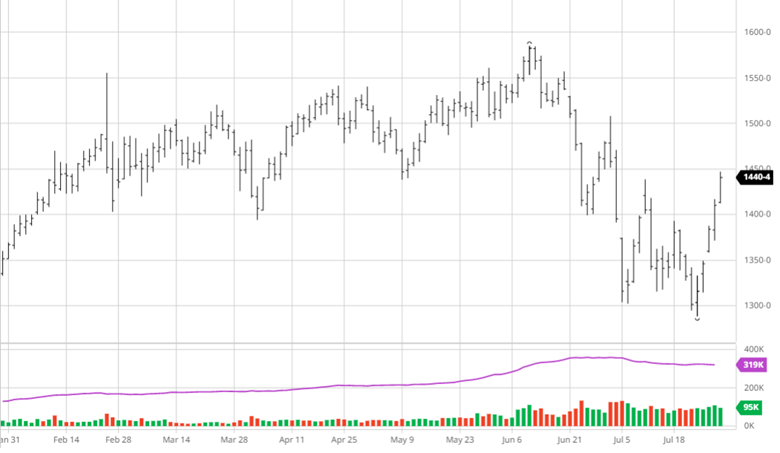

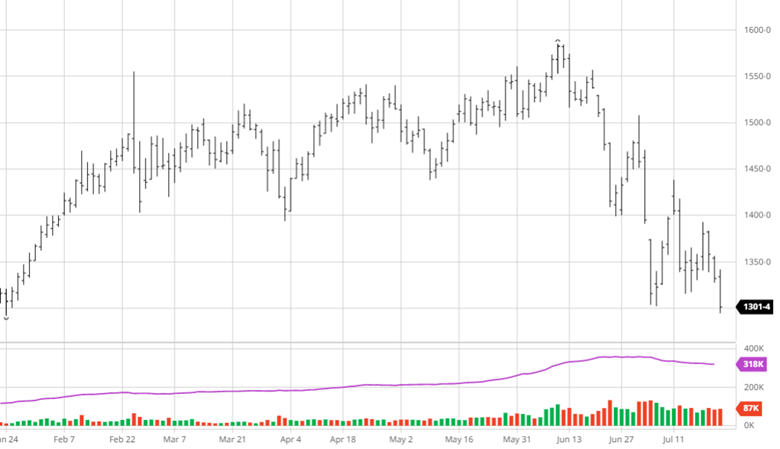

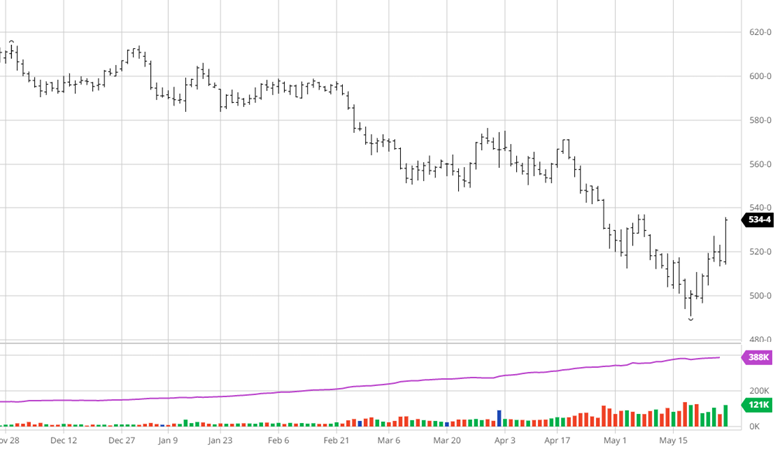

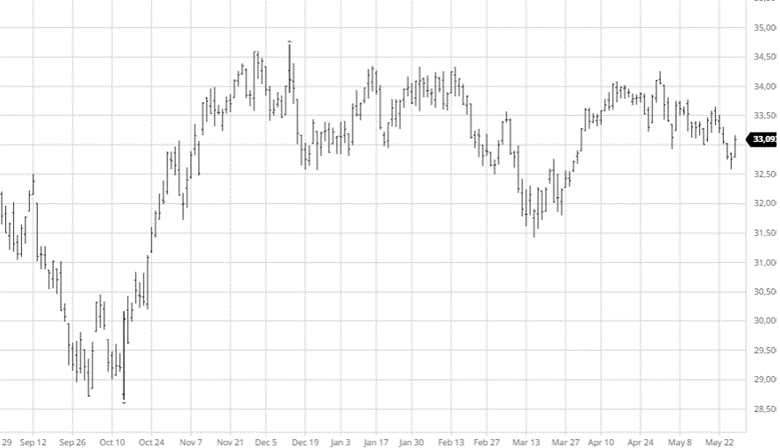

Cotton had a volatile week as seen in the chart below. When these opportunities present themselves, you do not want to miss the opportunity to hedge your risk. Have a plan and be prepared if there is another 5-cent spike that could make a big difference in your bottom line and potentially a good spot to place a hedge. The 78-84 cent range of Dec 2023 cotton has been consistent with pops to the upside and dips back to the bottom. The world economic outlook and US weather will be the main drivers moving forward into the long weekend.

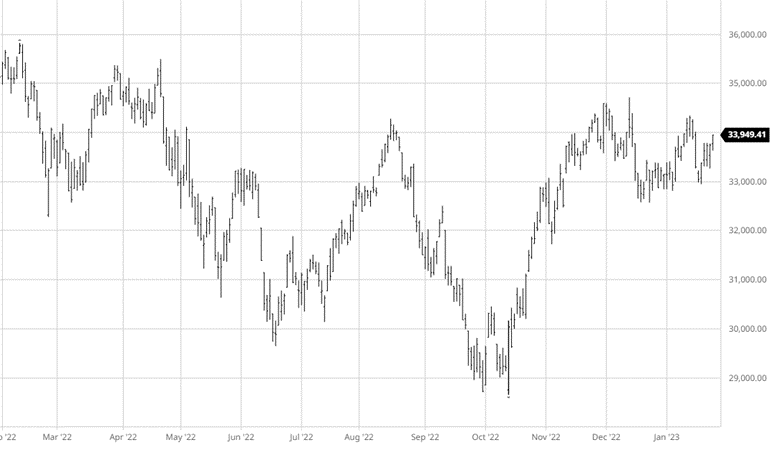

Equity Markets

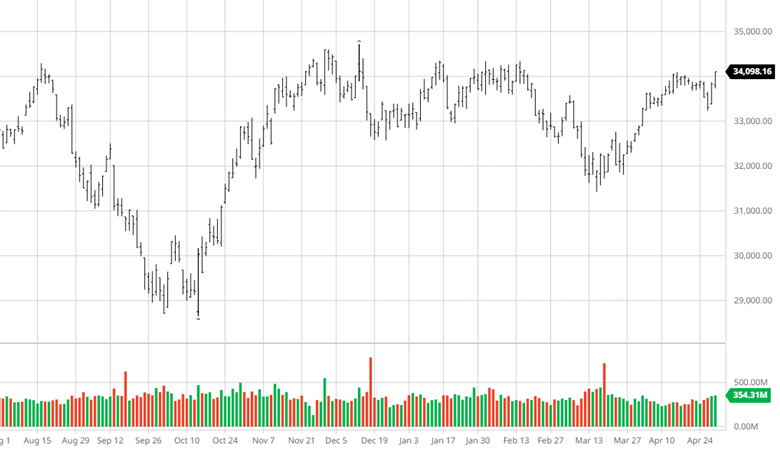

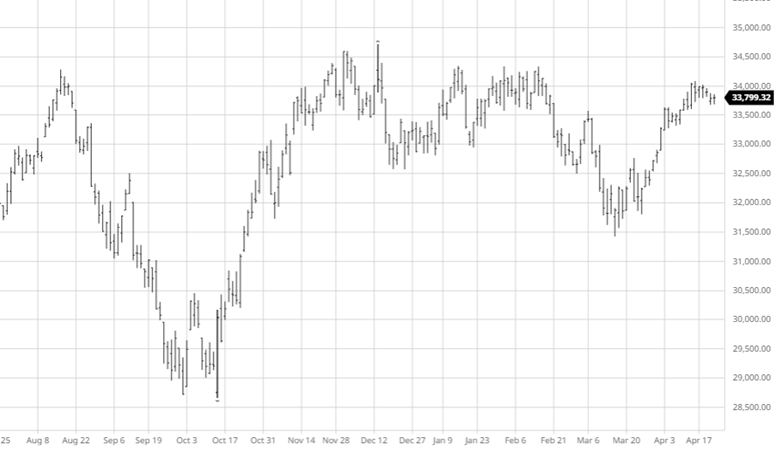

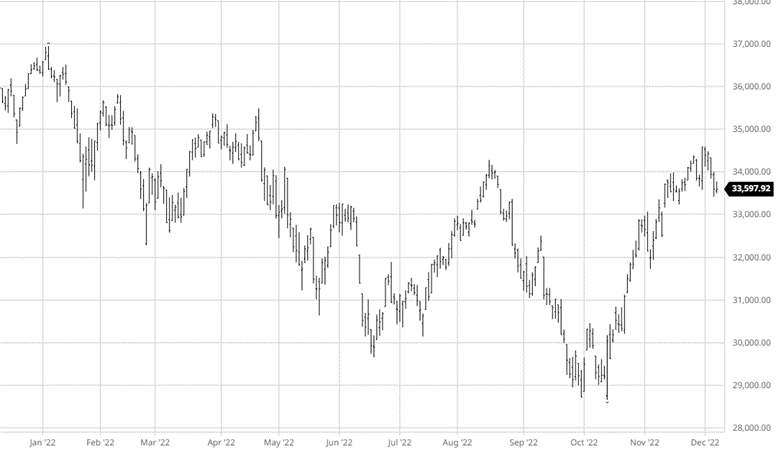

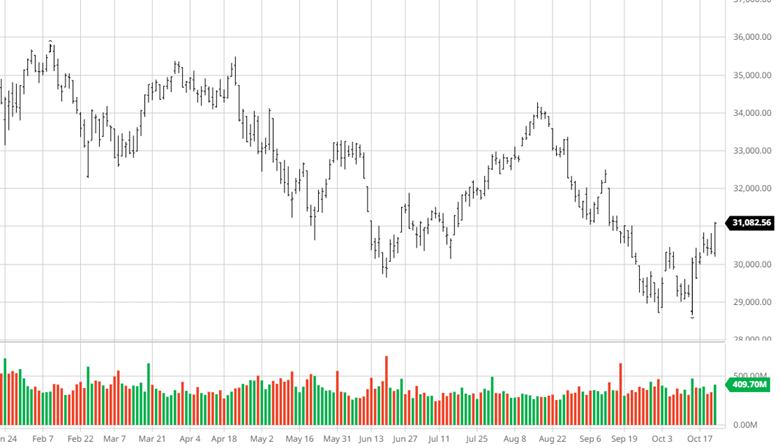

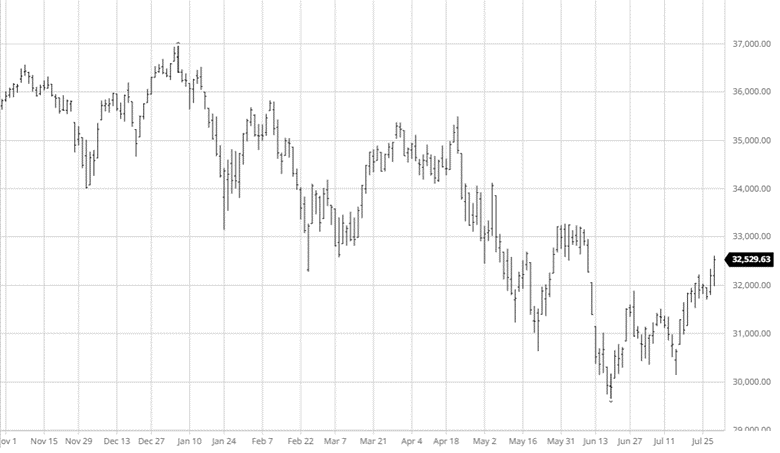

The equity markets continue their mixed run of late with the DJI continuing to struggle while the S&P and NASDAQ stocks see gains. NVIDIA was the big winner of the week as chips and AI have investors’ focus. While the jury is still out on Artificial Intelligence and what role it will play in the coming years, one thing is clear, investors don’t want to miss the boat even though we do not know if the boat is the Titanic or the USS Missouri.

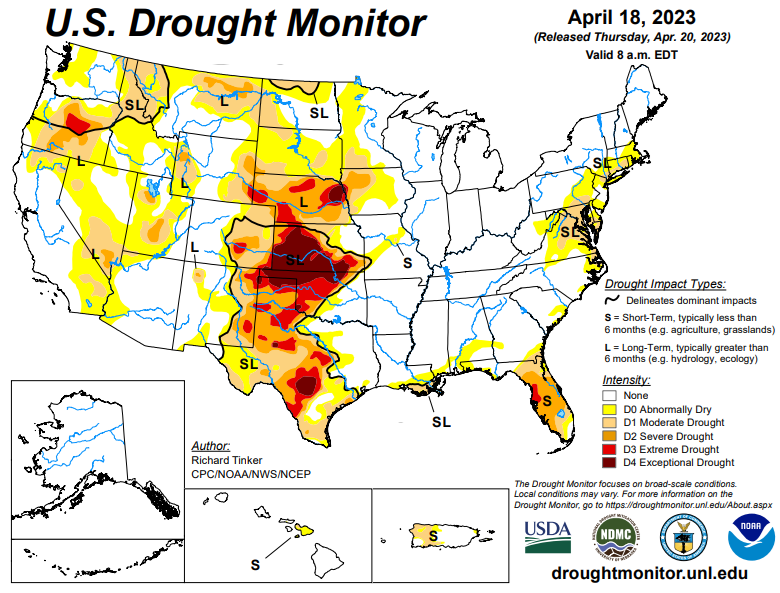

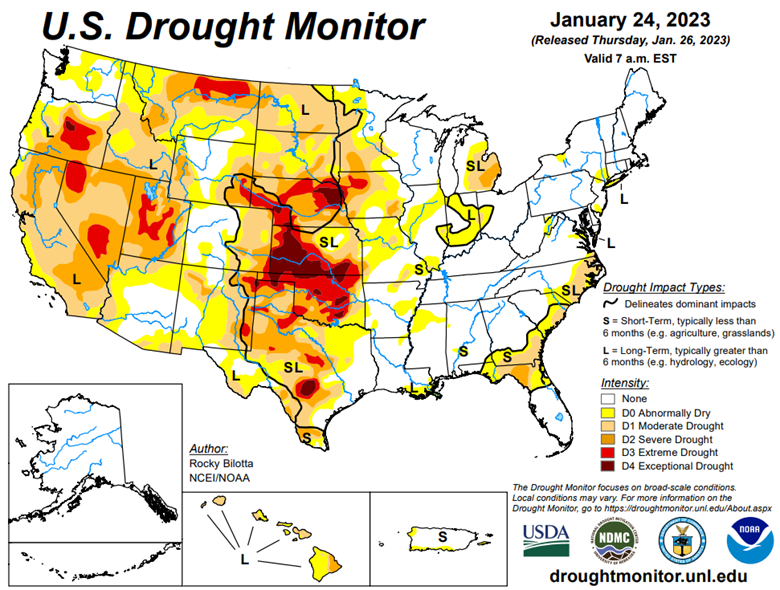

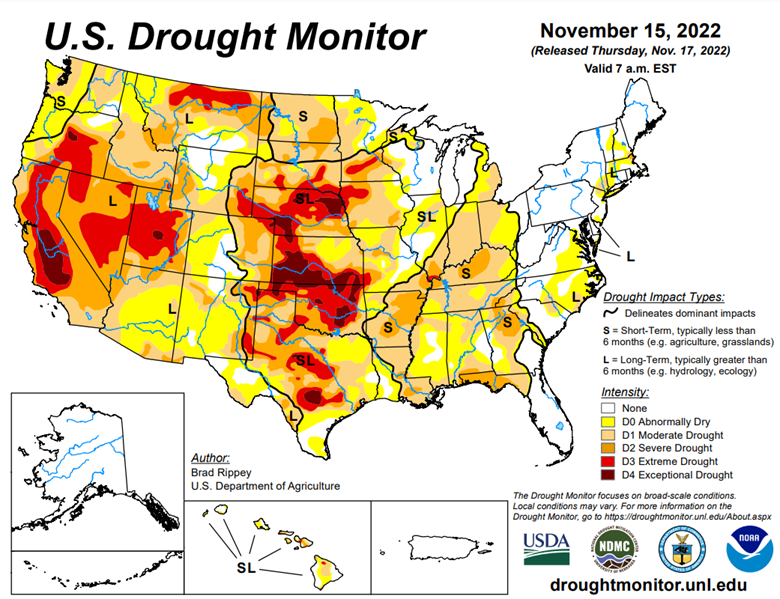

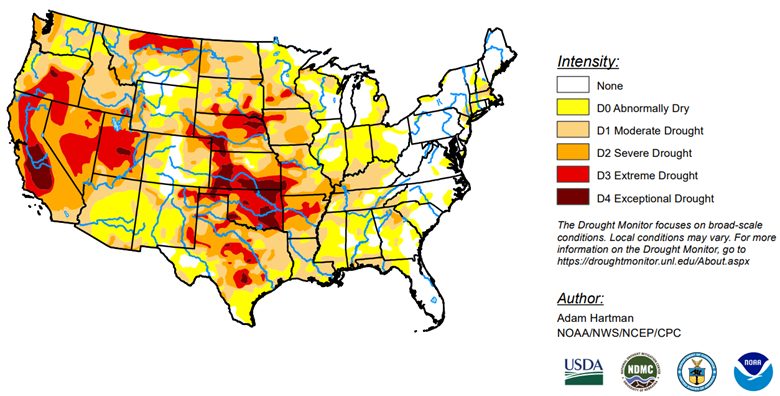

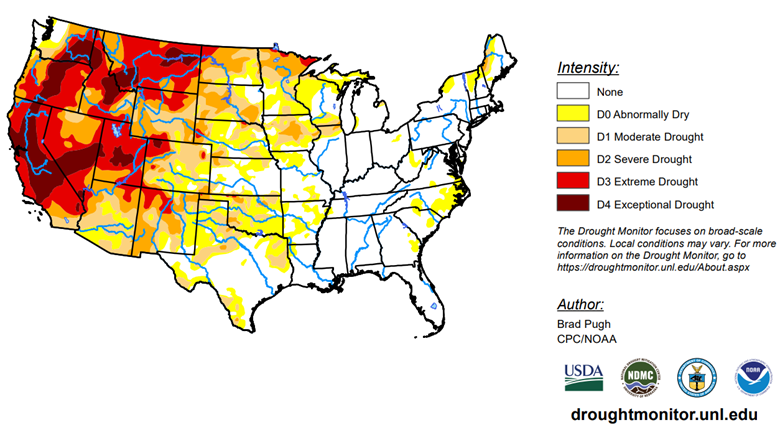

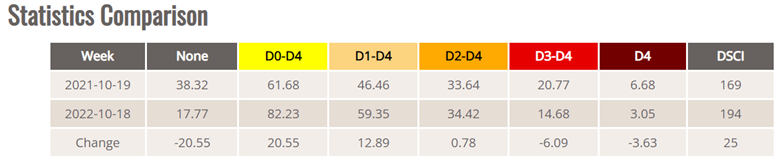

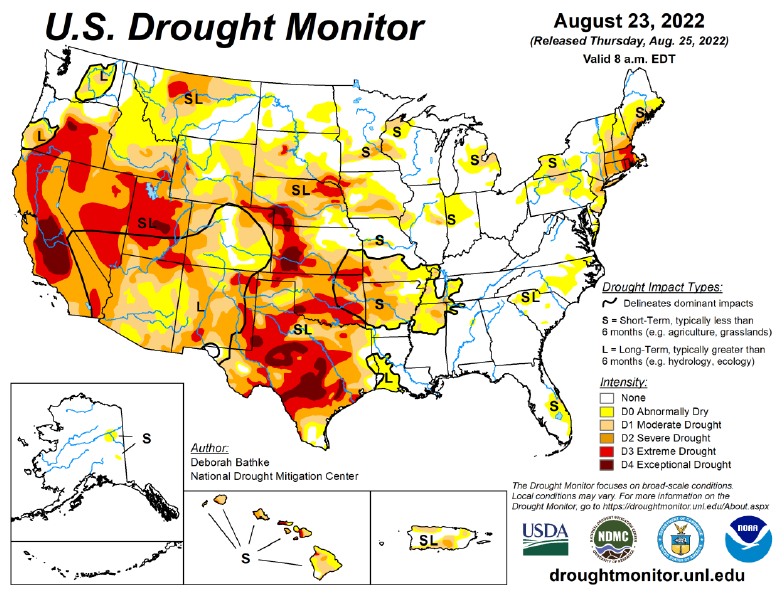

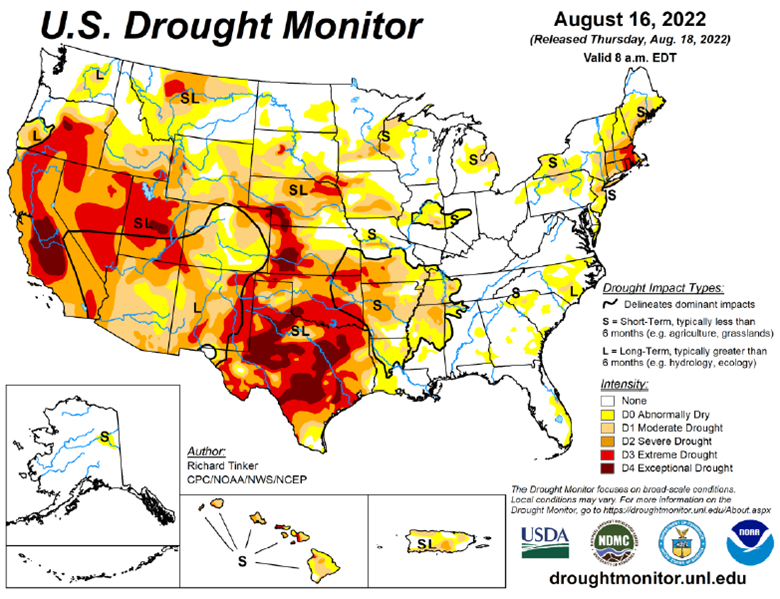

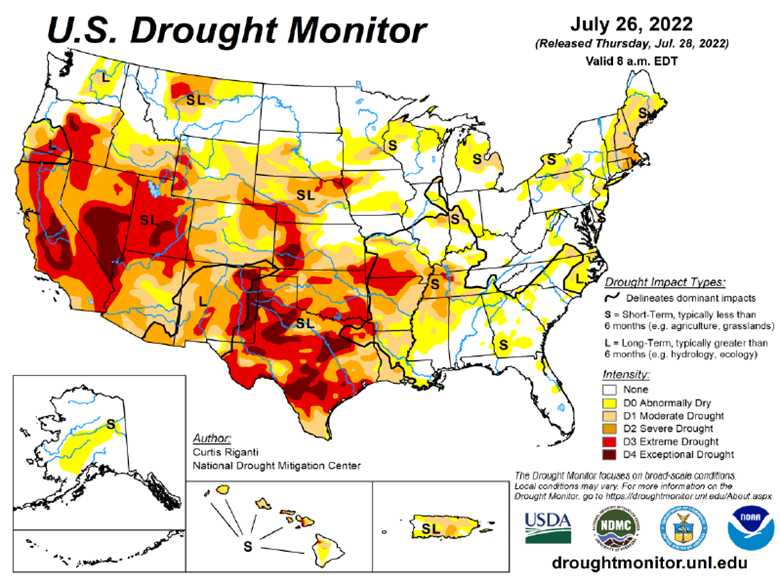

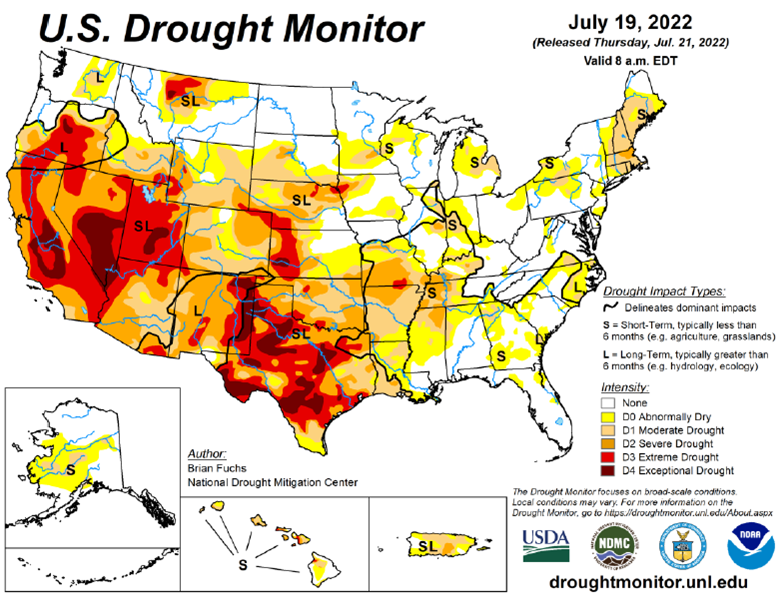

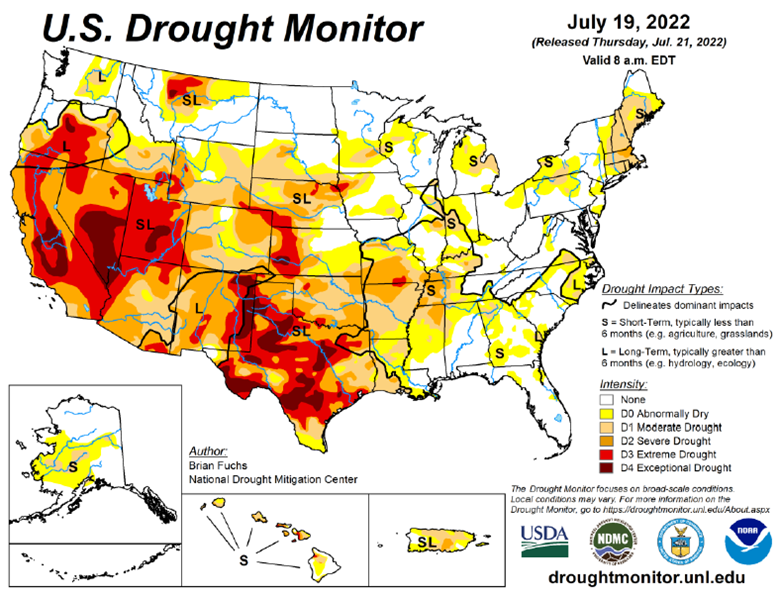

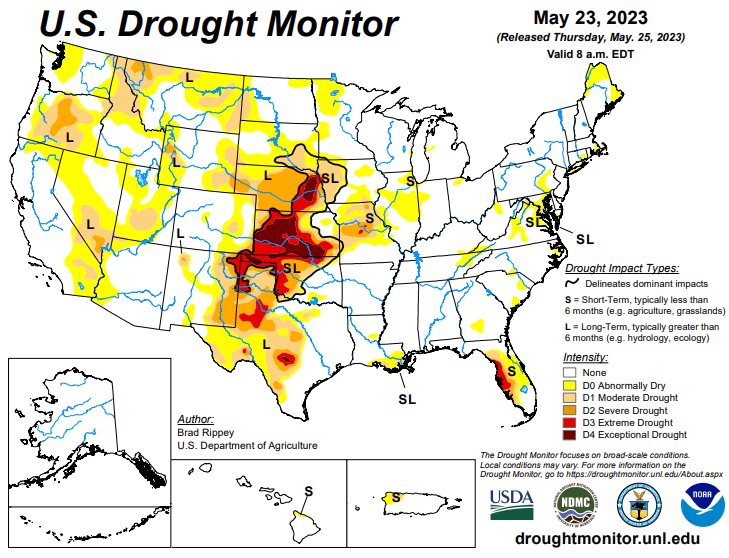

Drought Monitor

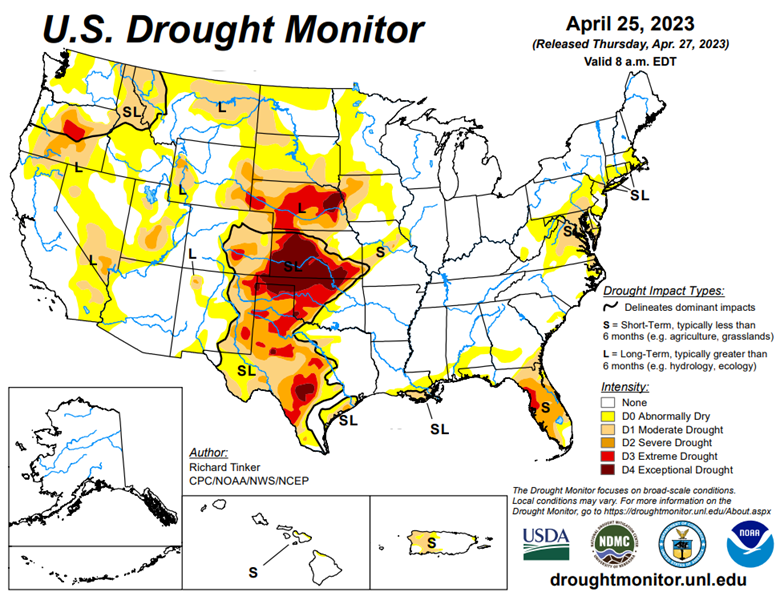

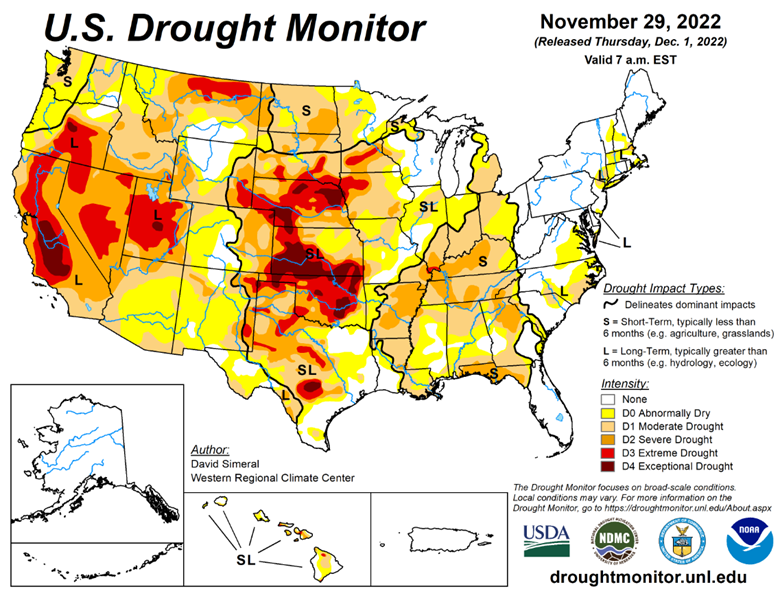

The drought monitor below shows the struggles in the weestern corn belt as the eastern corn belt is in good shape as planting wraps up.

Podcast

With every new year, there are new opportunities, and there’s no better time to dive deeply into the stock market and tax-saving strategies for 2023 than now. In our latest episode of the Hedged Edge, we’re joined by Tim Webb, Chief Investment Officer and Managing Partner from our sister company, RCM Wealth Advisors. Tim is no stranger to advising institutions and agribusinesses where he has been implementing no-nonsense financial planning strategies and market investment disciplines to help Clients build and maintain wealth and reach financial goals since

Inside this jam-packed session, we’re taking a break from commodities, and talking about the world of equities, interest rates, tax savings, and business planning strategies. Plus, Jeff and Tim delve into a variety of topics like:

- The current state of the markets within the wealth management industry

- Is there a beacon of hope, or is it all doom and gloom for the markets?

- Other strategies to think about outside of the stock market and so much more!

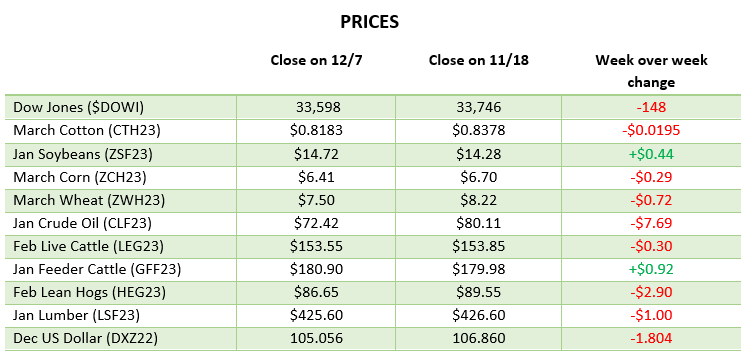

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.